|

시장보고서

상품코드

2065456

인공지능(AI) 기반 의료용 스케줄링 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Medical Scheduling Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

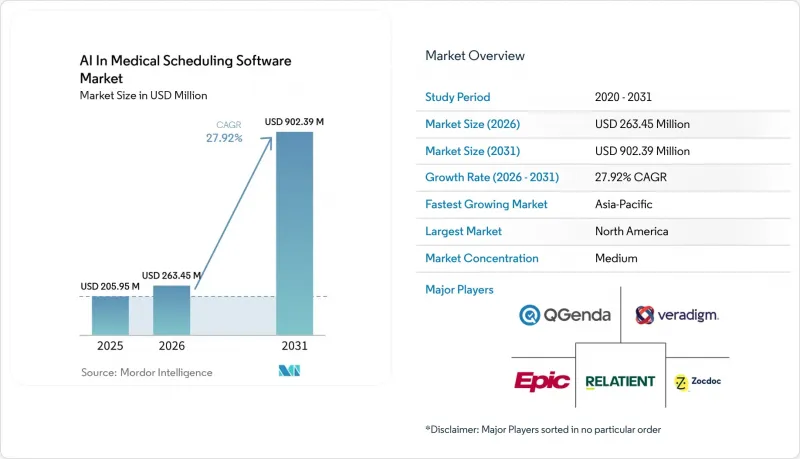

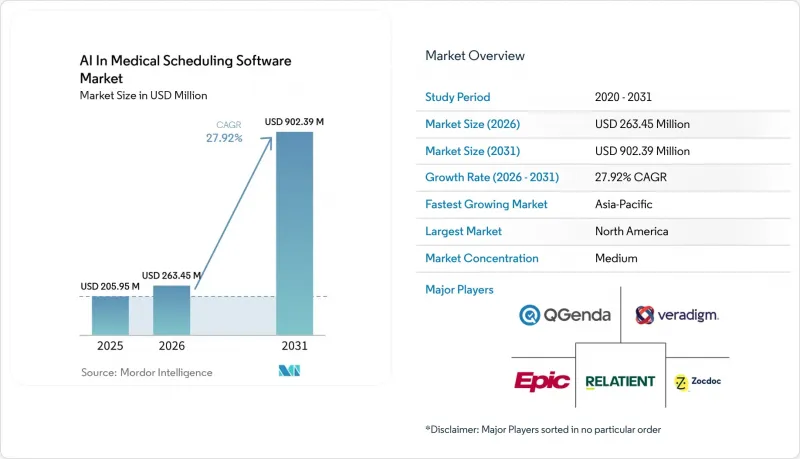

인공지능(AI) 기반 의료용 스케줄링 소프트웨어 시장 규모는 2025년에 2억 595만 달러로 평가되었습니다. 2026년 2억 6,345만 달러에서 2031년까지 9억 239만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 27.92%를 나타낼 전망입니다.

본 보고서는 스케줄링 워크플로우(환자 예약, 진료팀 등), AI 기능(예측 AI, 대화형 AI, 규칙 기반 등), 도입 모델(클라우드 기반, On-Premise형, 하이브리드형), 최종 사용자(병원, 진료소, 외래수술센터(ASC) 등), 전문 분야(1차 진료, 행동 의학 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 인공지능(AI) 기반 의료용 스케줄링 소프트웨어 시장 동향 및 인사이트

AI를 활용한 노쇼 예측 및 예약 슬롯 회복

이 시장은 예약 무단 취소가 수익 손실, 의료진의 시간 낭비, 직원들의 업무 부담 증가로 이어진다는 단순한 사실 덕분에 혜택을 보고 있습니다. 현재 예측 모델은 예약 내역, 환자의 행동, 진료 패턴을 활용하여 예약 시간이 유실되기 전에 취소나 무단 취소 위험이 높은 예약을 파악하고 있습니다. 이 점은 중요합니다. 왜냐하면 의료 제공업체들은 단순히 알림 기능을 개선하는 것뿐만 아니라, 여유 시간이 발생하기 전에 그 수용 능력을 회복할 방법을 모색하고 있기 때문입니다. Luma Health사는 2026년 4월, 자사의 플랫폼이 이미 의료 기관 고객사를 대상으로 250만 시간의 인력 절감 및 35만 건 이상의 진료 관련 후속 관리 지원을 달성했다고 발표했습니다. 이는 자동화된 프레임 회수 및 후속 조치 워크플로의 비즈니스적 효과를 입증하는 것입니다. 인공지능(AI) 기반 의료용 스케줄링 소프트웨어 시장에서 이 기능 세트는 외래 환자 수가 많고 빈 시간대 하나당 비용이 높은 경우에 특히 가치가 있습니다. 또한, 이는 사업 확장을 위한 자연스러운 길을 열어줍니다. 왜냐하면, 우선 진료율 향상 측면에서 그 가치를 입증한 공급업체는 그 후 대기 명단 관리, 의료 서비스 격차 해소, 나아가 더 광범위한 접근 관리로 사업을 확대할 수 있기 때문입니다.

연중무휴 24시간 운영되는 대화형 자가 예약 서비스에 대한 수요

의료 예약 소프트웨어 분야의 AI 시장은 진료 시간이나 전화 대기 줄에 구애받지 않는 연중무휴 24시간 디지털 접근에 대한 환자들 수요에 힘입어 성장하고 있습니다. 음성 및 채팅 에이전트를 통해 환자들은 쉬운 말로 예약, 취소, 일정 변경을 할 수 있게 되었으며, 이로 인해 접수 팀의 업무 부담이 줄어들고 응답 시간이 단축되었습니다. Zocdoc은 2025년 5월, 예약 관련 전화를 자율적으로 처리하는 ‘Zo by Zocdoc’을 출시하며, 대화형 예약이 더 이상 시험적인 기능이 아니라 주류 접근 도구로 자리매김하고 있음을 보여주었습니다. athenahealth 역시 2026년 2월, 미국인 5명 중 1명이 이용하는 의료 제공업체 네트워크 전반에 걸쳐 ‘대기 목록 예약’ 및 ‘강화된 환자 자율 예약’ 기능을 포함한 에이전트형 환자 커뮤니케이션 도구를 도입하며, 이와 유사한 방향성을 추진했습니다. 유럽에서도 이와 유사한 수요 추세가 나타나고 있으며, samedi사는 현지 규정 준수 요건을 충족하면서 의료기관의 예약 관리 시스템에 직접 연동되는 AI 기능과 ‘KI-Telefonassistent’를 제공합니다. 그 결과, 의료 예약 소프트웨어 시장에서 AI는 환자의 편의성과 직원의 효율성을 동시에 향상시키는 ‘상시 이용 가능한 접근 모델’로 점차 발전하고 있습니다.

환자 데이터의 개인정보 보호와 AI 거버넌스의 부담

의료 기관들이 규정 준수 관련 부담에 대해 명확한 내부 거버넌스 절차가 아직 마련되지 않았다고 인식하고 있는 경우, 시장 도입 속도는 여전히 더딘 상태입니다. 현재의 예약 시스템은 예약 사유, 보험 정보, 소통 내역 및 기타 데이터를 다루고 있으며, AI가 도입될 경우 엄격한 개인정보 보호 심사가 필요할 수 있습니다. 그로 인해, 특히 제한된 법무 자원 속에서 감독 체계, 문서화, 안전한 운영 관리를 입증해야 하는 중견 벤더의 경우, 기업의 구매 주기에 주저함이 나타나고 있습니다. 그 결과, 의료 기관들이 자동화 자체를 거부하는 것은 아니며, 계약 체결 전에 훈련 데이터, 사람에 의한 검토, 감사 기록, 사고 대응에 대해 더 많은 질문을 던지고 있는 것입니다. 의료 예약 관리 소프트웨어 분야의 AI 시장에서는 이러한 추세로 인해, 조달 시 보다 종합적인 규정 준수 대책 패키지를 제시할 수 있는 대형 벤더나 평판이 좋은 플랫폼 파트너가 유리한 입장에 서는 경향이 있습니다. 또한, 법무, 보안, 임상 각 팀이 모두 동일한 도입 계획을 승인해야 하는 환경에서는 판매 주기가 길어지는 요인이 되기도 합니다.

부문별 분석

2025년, 인공지능(AI) 기반 의료용 스케줄링 소프트웨어 시장 점유율 중 41.31%를 환자 예약 관리가 차지했으며, 환자 접근의 최전선에 위치하고 가장 광범위한 의료 기관 환경에 대응하고 있기 때문에 가장 큰 워크플로우 부문으로 자리매김했습니다. 인공지능(AI) 기반 의료용 스케줄링 소프트웨어 시장은 EHR 네이티브 모듈, 환자용 예약 도구, 컨택 센터 자동화 플랫폼 등 가장 다양한 공급업체 구성을 통해 혜택을 누리고 있습니다. 의료 기관의 경우, 전화 문의 건수 감소, 내원율 향상, 예약 완료 속도 향상과 같은 가치가 명확하게 드러나기 때문에 대부분의 경우 이 부분부터 도입을 시작합니다. 또한, 이 부문은 데이터 측면에서 자연스러운 우위를 가지고 있습니다. 예약 내역, 알림, 취소, 재예약 등의 이벤트가 안정적인 기록을 생성하여 AI 모델이 이를 최적화에 활용할 수 있기 때문입니다. 따라서 시장이 더욱 전문적인 업무 흐름으로 확대되고 있는 상황에서도, 환자 예약 관리는 여전히 주요 수익원으로 자리 잡고 있습니다.

케어 팀의 일정 관리 시장은 2031년까지 연평균 성장률(CAGR) 29.38%를 나타낼 것으로 예측되며, 이는 직원의 가용성, 자격, 업무 부담을 환자 수요와 조화시키는 도구에 대한 수요가 증가하고 있음을 반영합니다. QGenda는 이 분야를 단순한 스케줄링 문제로만 보지 않고 인재 관리의 문제로도 간주하고 있으며, QGenda가 의뢰한 2025년 Forrester의 ‘Total Economic Impact’ 조사에 따르면, 해당사의 통합 케어 팀 스케줄링 플랫폼을 이용하는 의료 시스템 고객사에서 430%의 ROI가 보고되었습니다. 또한, QGenda는 2026년 5월에 Workday HCM과의 공인 통합을 도입하여, 스케줄링 결정과 인사 시스템 간의 연동을 강화했습니다. 또한, 의료 제공업체들이 더욱 복잡해진 서비스 전반에 걸쳐 진료실, 장비, 인력을 조율하려는 가운데, 시술 및 자원 일정 관리도 주목을 받고 있습니다. LeanTaaS는 2025년 6월, 진료소 예약부터 수술실 배정에 이르기까지 최적화 범위를 확대하여 연간 400만 건의 수술을 지원하는 엔드투엔드 수술 조정 플랫폼인 ‘iQueue for Surgical Clinics’를 출시했습니다. 액세스 센터 및 옴니채널을 통한 일정 관리 역시 추가적인 성장 요인으로 작용하고 있습니다. 이는 의료 시스템이 전화, 포털, 디지털 아웃리치를 아우르는 단일 운영 모델을 필요로 하기 때문입니다. 의료 일정 관리 소프트웨어 업계의 AI 분야에서 단순한 예약 접수를 넘어선 워크플로우의 확대는 공급업체들이 운영의 중추적인 역할을 점점 더 수행해 나가고 있음을 보여줍니다.

예측 스케줄링은 2025년 전체 시장의 38.24%를 차지하며, 의료 스케줄링 소프트웨어 분야의 AI 시장을 주도했습니다. 그 가치는 수익 회복 및 기존 예약 슬롯의 효율적 활용과 밀접한 관련이 있기 때문입니다. 이 모델은 예약에 무단 불참할 가능성이 높은 환자를 파악하고, 대상에 맞춘 연락을 지원하며, 알림의 효율성을 높여주기 때문에 의료기관은 그 유용성을 즉시 파악할 수 있습니다. 이 기능은 광범위한 오케스트레이션 도구에 비해 워크플로우를 재설계할 필요가 거의 없기 때문에 대부분의 경우 최초의 운영 사례로 활용됩니다. 또한, 1차 진료부터 환자 수가 많은 외래 진료에 이르기까지, 예약 무단 취소가 명백한 비용 손실로 이어지는 다양한 전문 분야에 적합합니다. 예측형 스케줄링이 주도적인 위치를 차지하고 있다는 사실은 도입 초기 단계에서 구매자들이 여전히 측정 가능한 운영 성과를 가져다주는 이용 사례를 선호하고 있음을 보여줍니다.

의료 일정 관리 소프트웨어 시장에서 AI가 문제 예측에서 자동 수정으로 전환됨에 따라, 수용 능력 최적화와 대기 목록 자동화가 2031년까지 연평균 성장률(CAGR) 29.52%로 성장을 주도하고 있습니다. 이 차이는 중요합니다. 왜냐하면, 수동으로 전화를 걸거나 스프레드시트를 관리하지 않고도 취소된 예약을 채울 수 있다면, 의료기관은 더 큰 가치를 얻을 수 있기 때문입니다. Luma Health는 2026년 봄 출시를 통해 운영용 AI를 확장했습니다. 이를 통해 시스템은 수신된 팩스 문서에서 치료의 공백을 파악하고, 직원의 개입 없이 일정 관리 워크플로를 시작할 수 있게 되었습니다. 또한, LeanTaaS는 2026년 2월, 용량 최적화 관리 부문에서 2년 연속 ‘Best in KLAS’에 선정되었습니다. 이는 이 기능에 대한 구매자의 신뢰가 실적이 입증된 소수공급업체에 집중되고 있음을 보여줍니다. 대화형 AI를 통한 예약, 규칙 기반의 추천 엔진, 트리아지 중심 도구는 최종 예약이 확정되기 전의 다양한 접점을 처리하기 위해 여전히 중요합니다. 이러한 기능들이 결합되면서, 의료 예약 소프트웨어 시장에서 AI는 단순한 예측에 그치지 않고, 환자의 접근성을 확보하기 위한 보다 종합적인 ‘의사결정 및 실행’ 단계로 확대되고 있습니다. 따라서 의료 예약 소프트웨어 업계에서 AI는 분석 기능뿐만 아니라 운영 측면에서도 점점 더 중요해지고 있습니다.

지역별 분석

2025년, 북미는 인공지능(AI) 기반 의료용 스케줄링 소프트웨어 시장 점유율에서 47.24%를 차지하며, 지역별로는 가장 큰 기여를 한 지역이 되었습니다. 이는 의료 기관의 디지털화, 높은 관리 비용, 그리고 이미 자리 잡은 공급업체의 존재가 모두 상업적 도입을 가속화하고 있기 때문입니다. 이 지역은 의료 시스템의 밀집된 기반, 여러 거점을 보유한 의료기관 그룹, 전자건강기록(EHR)의 도입, 그리고 이미 복잡한 기업 환경을 대상으로 판매를 진행하고 있는 환자 접근성 솔루션 공급업체의 존재와 같은 이점을 갖추고 있습니다. 또한, 콜센터의 업무 부담, 예약 누락, 운영 인건비 등이 이미 면밀하게 추적되고 있기 때문에 AI를 활용한 예약 관리의 비즈니스 사례를 정량화하기 쉬운 지역이기도 합니다. 따라서 북미의 의료 일정 관리 소프트웨어 분야에서 AI는 이 카테고리의 존재를 입증하는 것보다, 어떤 도입 모델이나 통합 수준이 가장 효과적으로 확장될 수 있는지를 입증하는 데 중점을 두고 있습니다. 이러한 성숙한 수요 기반 덕분에, 성장률이 초기 단계에 있는 지역보다 낮을지라도 이 지역은 공급업체의 수익에서 계속해서 핵심적인 위치를 차지할 것입니다.

유럽에서는 공적 의료 제도, 개인정보 보호에 대한 기대, 조달 절차 등이 도입 결정에 더 직접적인 영향을 미치기 때문에 다양한 도입 양상이 나타납니다. 그럼에도 불구하고, 규제 명확화 및 상호운용성 확보를 위한 노력 덕분에 규정 준수를 충족하는 도입 환경이 점차 갖춰지고 있으며, 해당 지역은 발전하고 있습니다. 프랑스는 이러한 변화에서 두드러진 역할을 하고 있으며, 2025년에 발표된 ‘Segur du numerique vague 2 LGC’ 프레임워크에서는 스케줄링 통합을 표준화하기 쉽게 하는 상호운용성 요건이 규정되어 있습니다. 독일 역시 samedi 등공급업체를 통해 기여하고 있습니다. 이 회사는 현지 데이터 관련 요건을 준수하면서, 의료 제공업체의 업무 흐름과 연동되는 AI 기반 일정 관리 및 전화 비서 기능을 제공합니다. 유럽의 의료 일정 관리 소프트웨어 시장에서 AI의 보급 현황은 북미에 비해 여전히 편차가 나타나고 있지만, 공공 부문의 현대화와 민간 진료소의 디지털화가 맞물리면서 해당 시장의 기회는 확대되고 있습니다. 의료 제공업체가 규정 준수 요건과 의뢰 환자 대응, 대기 시간 단축, 외래 환자 관리 측면에서 명확한 이점을 연계할 수 있는 지역에서는 도입이 가장 활발하게 진행될 것으로 전망됩니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 30.83%로 가장 빠르게 성장하고 있는 지역이며, 의료 디지털화 수준이 아직 낮은 상태에서 빠르게 따라잡고 있는 이 지역에서 인공지능(AI) 기반 의료용 스케줄링 소프트웨어가 급속히 확대되고 있음을 보여줍니다. 막대한 환자 수, 의료기관 이용의 격차, 그리고 정부 주도의 디지털 헬스 프로그램이 예약 절차를 개선하고 수작업으로 인한 병목 현상을 완화할 수 있는 도구에 대한 수요를 창출하고 있습니다. 또한, 이 지역에서는 병원, 진료소 및 원격의료 현장에서의 업무 흐름 자동화를 목표로 하는 국내외 기술 공급업체들의 기반도 확대되고 있습니다. 따라서 아시아태평양은 향후 수익 성장뿐만 아니라, 북미에서 볼 수 있는 것보다 ‘모바일 우선’이며 비용 효율성을 중시하는 새로운 도입 모델 측면에서도 중요한 시장으로 자리매김하고 있습니다. 남미, 중동 및 아프리카는 여전히 초기 단계에 있는 지역이지만, 병원의 현대화와 민간 의료기관의 디지털화가 지속적으로 확대됨에 따라 장기적인 기회를 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the aI in medical scheduling software market size was valued at USD 205.95 million in 2025 and is estimated to grow from USD 263.45 million in 2026 to reach USD 902.39 million by 2031, at a CAGR of 27.92% during the forecast period (2026-2031).

This report is Segmented by Scheduling Workflow (Patient Appointment, Care Team, and More), AI Capability (Predictive, Conversational AI, Rules-Based, and More), Deployment Model (Cloud-Based, On-Premises, Hybrid), End User (Hospitals, Clinics, Ascs, and More), Specialty (Primary Care, Behavioral Health, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global AI In Medical Scheduling Software Market Trends and Insights

AI-Led No-Show Prediction and Slot Recovery

The market is benefiting from the simple fact that missed appointments translate into lost revenue, idle clinician time, and more work for staff. Predictive models now use booking history, patient behavior, and care patterns to identify appointments with higher cancellation or no-show risk before the slot is lost. This matters because providers do not only want better reminders, they want a way to recover capacity before it goes unused. Luma Health stated in April 2026 that its platform had already helped health system clients save 2.5 million staff hours and manage more than 350,000 care-related next steps, which supports the commercial case for automated slot recovery and follow-up workflows. In the AI in medical scheduling software market, this feature set is especially valuable where high outpatient volumes make each unfilled slot more costly. It also creates a natural path for expansion because vendors that first prove value on attendance can later extend into waitlists, care gap closure, and broader access management.

24/7 Conversational Self-Scheduling Demand

The AI in medical scheduling software market is also being lifted by patient demand for round-the-clock digital access that does not depend on office hours or call queues. Voice and chat agents now let patients book, cancel, or reschedule in plain language, which reduces the load on front-desk teams and improves response time. Zocdoc launched Zo by Zocdoc in May 2025 to handle inbound scheduling calls autonomously, showing that conversational booking is being positioned as a mainstream access tool rather than a pilot feature. athenahealth pushed the same direction in February 2026 with agentic patient communication tools that included Waitlist Scheduling and Enhanced Patient Self-Scheduling across a provider network that serves 1 in 5 Americans. The same demand pattern is visible in Europe, where samedi offers AI features and a KI-Telefonassistent that connect directly to provider scheduling environments under local compliance expectations. As a result, the AI in medical scheduling software market is moving closer to an always-available access model where patient convenience and staff efficiency improve at the same time.

Patient Data Privacy and AI Governance Burden

The market still faces slower adoption where providers believe the compliance burden is not yet matched by clear internal governance processes. Scheduling systems now handle appointment reasons, insurance information, communication history, and other data that can trigger strict privacy reviews when AI is involved. That creates hesitation in enterprise buying cycles, especially for mid-market vendors that need to prove oversight, documentation, and safe operating controls with limited legal resources. The effect is not that providers reject automation, but that they ask more questions about training data, human review, audit trails, and incident response before signing contracts. In the AI in medical scheduling software market, this tends to favor larger vendors and established platform partners that can present a fuller compliance package during procurement. It also lengthens sales cycles in settings where legal, security, and clinical teams all need to approve the same deployment.

Other drivers and restraints analyzed in the detailed report include:

- EHR-Connected Workflow Automation Adoption

- Prior-Authorization-Aware Booking Workflows

- Fragmented EHR and Departmental Integration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Patient appointment scheduling held 41.31% of the AI in medical scheduling software market share in 2025, making it the largest workflow segment because it sits at the front end of patient access and serves the broadest range of provider settings. This part of the AI in medical scheduling software market benefits from the widest vendor mix, including EHR-native modules, patient-facing booking tools, and contact-center automation platforms. Providers often begin here because the value is easier to see through fewer calls, better attendance, and faster booking completion. The segment also has a natural data advantage because appointment history, reminders, cancellations, and rebooking events create a steady record that AI models can use for optimization. That is why patient appointment scheduling remains the main revenue anchor even as the market expands into more specialized workflows.

Care team scheduling is projected to grow at a 29.38% CAGR through 2031, reflecting stronger demand for tools that align staff availability, credentials, and workload with patient demand. QGenda has framed this area as a workforce management problem as much as a scheduling problem, and a 2025 Forrester Total Economic Impact study commissioned by QGenda reported 430% ROI for health system clients using its unified care team scheduling platform. QGenda also introduced a certified integration with Workday HCM in May 2026, which strengthens the link between scheduling decisions and HR systems. Procedure and resource scheduling is also gaining traction as providers try to coordinate rooms, equipment, and staff across more complex service lines. LeanTaaS launched iQueue for Surgical Clinics in June 2025 as an end-to-end surgical coordination platform that extends optimization from clinic booking into operating room allocation and supports 4 million surgeries annually. Access-center and omnichannel scheduling adds another layer of growth because health systems want a single operating model across phone, portal, and digital outreach. In the AI in medical scheduling software industry, workflow expansion beyond simple appointment booking is a sign that vendors are moving closer to operational command-center roles.

Predictive scheduling accounted for 38.24% of the 2025 market and led the AI in medical scheduling software market because its value is closely tied to revenue recovery and better use of existing appointment supply. Providers understand the model quickly because it helps identify likely no-shows, supports targeted outreach, and makes reminder efforts more efficient. This capability is often the first production use case because it requires less workflow redesign than broader orchestration tools. It also fits a wide range of specialties, from primary care to high-volume outpatient services, where missed appointments carry a clear cost. The leading position of predictive scheduling shows that buyers still prefer use cases with measurable operational outcomes at the start of adoption.

Capacity optimization and waitlist automation leads growth with a 29.52% CAGR through 2031, as the AI in medical scheduling software market shifts from predicting problems to automatically correcting them. That distinction matters because providers gain more value when cancellations are backfilled without manual calls or spreadsheet management. Luma Health's Spring 2026 release expanded its Operational AI so the system could identify care gaps from incoming fax documents and trigger scheduling workflows without staff intervention. LeanTaaS was named Best in KLAS for Capacity Optimization Management for the second straight year in February 2026, which signals that buyer trust in this capability is consolidating around a smaller group of validated vendors. Conversational AI scheduling, rules-based recommendation engines, and triage-led tools remain important because they address different access points before the final booking happens. Together these functions are broadening the AI in medical scheduling software market from prediction alone into a fuller decision-and-action layer for patient access. The AI in medical scheduling software industry is therefore becoming more operational, not only more analytical.

Geography Analysis

North America held 47.24% of the AI in medical scheduling software market share in 2025, which made it the largest regional contributor because provider digitization, high administrative cost, and established vendor presence all support faster commercial adoption. The region benefits from a dense base of health systems, multi-site provider groups, EHR adoption, and patient access vendors that already sell into complex enterprise environments. It is also the geography where the business case for AI scheduling is often easiest to quantify, since call-center burden, appointment leakage, and operational labor costs are already closely tracked. The AI in medical scheduling software market in North America is therefore less about proving the category exists and more about proving which deployment model and integration depth can scale best. That mature demand base should keep the region central to vendor revenue even if its growth rate is lower than earlier-stage regions.

Europe presents a different adoption pattern because public health systems, privacy expectations, and procurement pathways shape rollout decisions more directly. Even so, the region is moving forward as regulatory clarity and interoperability efforts improve the environment for compliant deployment. France has taken a visible role in this shift, and the Segur du numerique vague 2 LGC framework published in 2025 set interoperability requirements that make scheduling integrations easier to standardize. Germany is also contributing through vendors such as samedi, which offers AI-enabled scheduling and telephone assistant capabilities that connect to provider workflows under local data expectations. The AI in medical scheduling software market in Europe is still more uneven than in North America, but the mix of public sector modernization and private practice digitization is widening the addressable opportunity. Adoption is likely to remain strongest where providers can connect compliance requirements with clear gains in referral handling, wait-time reduction, and outpatient coordination.

Asia-Pacific is the fastest-growing region with a 30.83% CAGR through 2031, showing that the AI in medical scheduling software market is expanding quickly where healthcare digitization is still catching up from a lower base. Large patient populations, uneven provider access, and government-backed digital health programs are creating room for tools that improve appointment flow and reduce manual bottlenecks. The region also has a growing base of local and international technology vendors targeting workflow automation in hospitals, clinics, and virtual care settings. That makes Asia-Pacific important not only for future revenue growth, but also for new deployment models that may be more mobile-first and cost-sensitive than those seen in North America. South America and the Middle East and Africa remain earlier-stage regions, yet they add long-term opportunity as hospital modernization and private provider digitization continue to spread.

- AdvancedMD

- athenahealth

- eClinicalWorks

- Epic Systems

- Hyro

- Kyruus Health

- LeanTaaS

- Luma Health

- NexHealth

- NextGen Healthcare

- Notable

- Oracle Health

- Petal

- Phreesia

- QGenda

- Qventus

- Relatient

- Veradigm

- WellSky

- Zocdoc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Led No-Show Prediction and Slot Recovery

- 4.2.2 24/7 Conversational Self-Scheduling Demand

- 4.2.3 Provider Burnout and Staffing Shortages

- 4.2.4 EHR-Connected Workflow Automation Adoption

- 4.2.5 Prior-Authorization-Aware Booking Workflows

- 4.2.6 Contact-Center Voice AI Economics

- 4.3 Market Restraints

- 4.3.1 Patient Data Privacy and AI Governance Burden

- 4.3.2 Fragmented EHR And Departmental Integration

- 4.3.3 Clinical Change-Management Resistance

- 4.3.4 Real-Time Data Quality and Schedule-Rule Complexity

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Scheduling Workflow

- 5.1.1 Patient Appointment Scheduling

- 5.1.2 Care Team Scheduling

- 5.1.3 Procedure and Resource Scheduling

- 5.1.4 Access-Center and Omnichannel Scheduling

- 5.2 By AI Capability

- 5.2.1 Predictive Scheduling

- 5.2.2 Conversational AI Scheduling

- 5.2.3 Rules-Based and Recommendation Scheduling

- 5.2.4 Capacity Optimization and Waitlist Automation

- 5.2.5 Triage-Led and Intent-Aware Scheduling

- 5.3 By Deployment Model

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By End User

- 5.4.1 Hospitals and Health Systems

- 5.4.2 Clinics and Physician Groups

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Diagnostic and Imaging Centers

- 5.4.5 Other End Users

- 5.5 By Specialty

- 5.5.1 Primary Care

- 5.5.2 Behavioral and Mental Health

- 5.5.3 Cardiology

- 5.5.4 Orthopedics

- 5.5.5 Oncology

- 5.5.6 Dental

- 5.5.7 Other Specialities

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 AdvancedMD

- 6.3.2 athenahealth

- 6.3.3 eClinicalWorks

- 6.3.4 Epic Systems Corporation

- 6.3.5 Hyro

- 6.3.6 Kyruus Health

- 6.3.7 LeanTaaS

- 6.3.8 Luma Health

- 6.3.9 NexHealth

- 6.3.10 NextGen Healthcare

- 6.3.11 Notable

- 6.3.12 Oracle Health

- 6.3.13 Petal

- 6.3.14 Phreesia

- 6.3.15 QGenda

- 6.3.16 Qventus

- 6.3.17 Relatient

- 6.3.18 Veradigm LLC

- 6.3.19 WellSky

- 6.3.20 Zocdoc

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment