|

시장보고서

상품코드

2065518

AI 추론 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI Inference GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

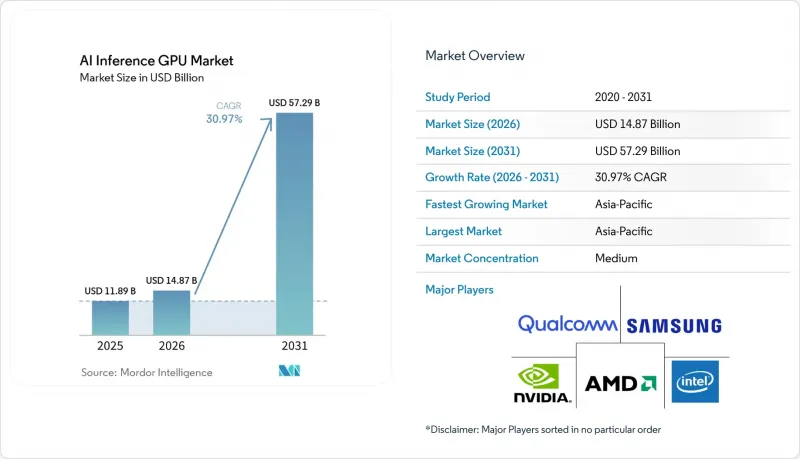

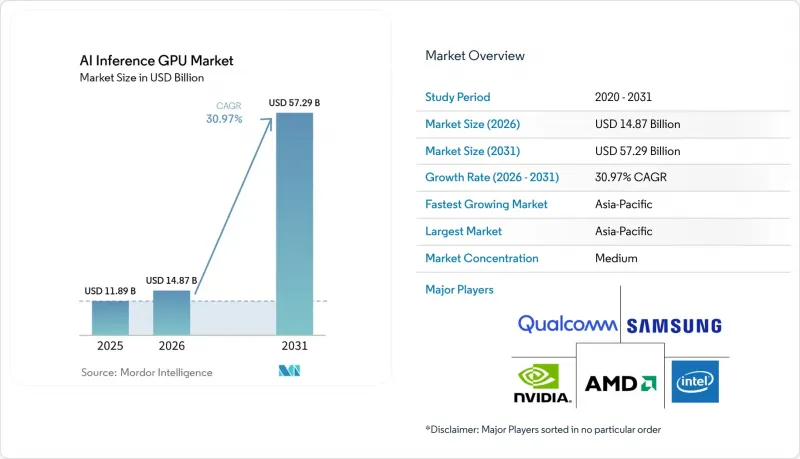

AI 추론 GPU 시장 규모는 2025년 118억 9,000만 달러로 평가되었고, 2026년 148억 7,000만 달러로 추정되고, 2031년까지 572억 9,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 30.97%를 나타낼 전망입니다.

본 보고서는 도입 형태별(클라우드/데이터센터, 엣지, 기타), 폼 팩터별(PCIe GPU, SXM/OAM GPU, 기타), 용도별(생성형 AI, 컴퓨터 비전, 추천 시스템, 자율 시스템, 기타), 지역별(북미, 유럽, 아시아태평양, 남미, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 AI 추론 GPU 시장 동향 및 인사이트

하이퍼스케일 데이터센터에서 생성형 AI 서비스 수요 급증

하이퍼스케일 클라우드에서는 훈련 시스템의 규모를 뛰어넘는 추론 클러스터가 제공되며, 이는 단일 대형 언어 모델이 수백만 명의 동시 사용자를 처리하고 있다는 현실을 반영하고 있습니다. Microsoft Azure는 2025년 하반기에 GitHub Copilot 및 Azure OpenAI 엔드포인트를 지원하기 위해 12만 개의 NVIDIA H200 NVL GPU를 추가했습니다. 이 엔드포인트들은 2025년 12월에 500억 건 이상의 API 호출을 처리했습니다. Oracle Cloud Infrastructure는 접합부 온도를 75°C 미만으로 유지하는 수냉식 랙 설계를 도입한 결과, GPU 추론 워크로드에서 99.95%의 가동률을 달성했다고 보고했습니다. AWS는 2026년 3월에 맞춤형 칩 ‘Inferentia 3’를 도입하여 Inferentia 2보다 3배 높은 처리량을 달성했으나, FP8 및 INT4 양자화를 활용하는 혼합 정밀도 워크로드에서는 NVIDIA Blackwell NVL이 여전히 우위를 점하고 있습니다. 메타는 2025년 400억 달러 규모의 자본 예산 중 180억 달러가 추론 인프라에 배정되었다고 밝히며, 용량을 임대하는 대신 자체적으로 보유하는 것의 전략적 우선순위를 강조했습니다. 대화형 AI의 지연 시간 목표가 2024년 500밀리초에서 2026년에는 200밀리초 미만으로 더욱 엄격해짐에 따라, 고대역폭 메모리와 저지연 상호 연결을 갖춘 GPU에 대한 수요는 계속해서 가속화되고 있습니다.

전자상거래 플랫폼에서 추천 엔진의 급속한 확산

실시간 개인화는 현재 10밀리초 미만의 지연 시간으로 작동하고 있으며, 소매업체들은 일괄 처리로 인한 지연 없이 스파스 임베딩 및 동적 특징량을 처리할 수 있는 추론용 GPU를 도입할 수밖에 없는 상황입니다. Amazon Personalize는 2025년에 판매자들이 CPU 기반 협업 필터링에서 GPU 가속형 딥러닝 모델로 전환함에 따라 추론 처리량을 향상시켰습니다. 알리바바 클라우드의 Hanguang 800 칩은 타오바오와 티몰의 추천 서비스 지연 시간을 35밀리초에서 12밀리초로 단축했으며, 2025년 ‘싱글스 데이’ 피크 기간 동안 쿼리 1건당 에너지 소비량을 60% 절감했습니다. Shopify는 2025년 9월 NVIDIA TensorRT-LLM을 통합하여 상품 검색 모델이 재고 변동에 5분 이내에 대응할 수 있도록 했으며, 시범 프로그램에 참여한 사업자의 전환율을 높였습니다. ByteDance에 따르면, TikTok Shop은 NVIDIA A100 및 H100 GPU에서 시간당 4억 건의 상품 노출을 처리하고 있으며, 적극적인 모델 프루닝을 통해 추론 비용은 총 상품 가치(GMV)의 0.02% 미만으로 억제되고 있습니다.

고성능 추론용 GPU의 높은 초기 투자 비용

NVIDIA H200 NVL 유닛의 정가는 4만 달러를 초과하여, 벤처 뎁트나 클라우드 크레딧을 보유하지 않은 중견 기업들에게는 큰 장벽이 되고 있습니다. Dell Technologies에 따르면, 고대역폭 메모리 및 수냉 시스템에 대한 요구 사항으로 인해 AI 최적화 서버의 평균 판매 가격이 전년 대비 35% 상승했다고 합니다. Supermicro사는 GPU 서버의 리드타임이 16주에 달하고 50%의 계약금이 필요하기 때문에 납기일이 2026년 하반기로 늦춰질 것이라고 보고했습니다. Equinix사의 데이터에 따르면, AI 추론용 랙은 평균 25kW를 소비하고 있으며, 이는 코로케이션 요금 인상 요인이 되고 있습니다. NVIDIA의 DGX Cloud 구독 서비스(GPU 시간당 5.50달러)도 대안이 될 수 있지만, 이용률이 60% 이상을 유지할 수 있는 경우에만 자체 보유하는 것이 비용 대비 효율이 더 높습니다.

부문별 분석

2025년, 하이퍼스케일러 각사가 하루 수십억 건의 API 호출을 처리하기 위해 자원을 집중한 결과, 클라우드 및 데이터센터로의 도입이 AI 추론 GPU 시장 점유율의 60.17%를 차지했습니다. 2025년 하반기 Microsoft Azure가 12만 대의 H200 NVL 유닛을 추가함에 따라, 한 달에 500억 건의 GitHub Copilot 호출이 가능해졌으며, 이는 조달 결정에 영향을 미치는 처리량 기준의 중요성이 부각되었음을 보여줍니다. 메타가 추론 인프라에 180억 달러를 배정했다는 사실은 훈련에서 서비스 제공으로의 전환을 더욱 여실히 보여주고 있습니다.

연평균 성장률(CAGR) 31.53%를 기록하며 진행 중인 엣지 확장은 지연 시간의 제약으로 인해 클라우드에서 왕복 처리가 불가능한 상황에서 그 기세를 더하고 있습니다. 테슬라의 ‘완전 자율 주행(Full-Self-Driving)’ 컴퓨터는 맞춤형 가속기에서 초당 2,300프레임의 카메라 이미지를 처리하며, 엣지 용도에 요구되는 결정론적 성능을 입증하고 있습니다. 산업용 자동화 분야에서도 제어 루프의 타이밍 요건을 충족하기 위해 온디바이스 추론이 선호되지만, 엄격한 전력 소비 제한으로 인해 GPU 선택지는 Jetson AGX Orin과 같이 60와트 미만의 모듈로 한정되어 있습니다. 따라서 AI 추론 GPU 시장은 전력 여유가 있는 하이퍼스케일 시설과 전력 제약이 있는 엣지 사이트 사이에서 양극화되고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 69.52%를 차지한 것으로 평가되었으며, 국가 주도의 AI 프로그램, 하이퍼스케일 기업과의 제휴, 그리고 적극적인 데이터센터 확장에 힘입어 2031년까지 연평균 성장률(CAGR) 31.92%를 기록하며 성장할 것으로 전망됩니다. 수출 규제로 인해 NVIDIA H100공급이 제한됨에 따라, 화웨이는 2025년에 5만 대 이상의 Ascend 910C 가속기를 출하했습니다. 릴라이언스 지오와 NVIDIA는 2025년 9월에 합작 회사를 설립하고, 2027년 중반까지 10만 대의 H100 GPU를 도입함으로써 인도 기업용 AI 서비스 추진의 기반을 마련했습니다. 싱가포르와 태국은 2026년에 새로운 수냉식 캠퍼스 건설을 승인했으며, 2027년에 GPU 임차인을 대상으로 개방될 800메가와트의 용량을 추가했습니다.

북미의 AI 추론 GPU 수요는 하이퍼스케일 클라우드 제공업체와, 데이터 주권 요건을 충족하기 위해 온프레미스 추론을 선호하는 규제 대상 기업들에 의해 주도되고 있습니다. AWS는 2025년 7월에 ‘Inferentia 3’를 출시했으며, TensorRT를 통한 최적화로 전환한 후 Stable Diffusion 파이프라인의 지연 시간이 40% 감소했다고 보고했습니다. JPMorgan Chase는 1만 대 이상의 NVIDIA H100 GPU를 갖춘 프라이빗 클라우드를 운영하고 있으며, 규정 준수가 중요한 워크로드에 있어 이 회사가 자사 소유의 인프라를 우선시하고 있음을 알 수 있습니다. 캐나다의 한 에너지 기업은 2026년 초에 실시간 유정 로그 분석을 위해 Groq 언어 처리 유닛의 시범 도입을 시작했으며, 이는 확정 지연형 실리콘에 대한 관심이 높아지고 있음을 보여줍니다.

유럽의 AI 법안에서는 문서화 및 투명성에 관한 의무가 추가됨에 따라 도입 주기가 길어지고 있습니다. 지멘스는 규정 준수가 가능함을 입증했습니다. 이 회사의 Gaudi 3 기반 Simatic AI 플랫폼은 의무화된 위험 평가 공개 요건을 충족하면서 반도체 팹의 가동 중단 시간을 18% 줄였습니다. 프랑스와 독일은 2028년 가동을 예정하고 있는 국가 주도의 추론 클라우드 프로그램에 20억 유로(21억 8,000만 달러)를 배정했으며, 규제 체계가 명확해지면 수요가 폭발적으로 증가할 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the aI inference GPU market size is projected to expand from USD 11.89 billion in 2025 and USD 14.87 billion in 2026 to USD 57.29 billion by 2031, registering a CAGR of 30.97% between 2026 and 2031.

This report is Segmented by Deployment Type (Cloud/Data Center, Edge, and More), Form Factor (PCIe GPUs, SXM/OAM GPUs, and More), Application (Generative AI, Computer Vision, Recommendation Systems, Autonomous Systems, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global AI Inference GPU Market Trends and Insights

Surging Demand for Generative AI Services in Hyperscale Data Centers

Hyperscale clouds are provisioning inference clusters that now exceed the scale of their training systems, reflecting the reality that a single large language model serves millions of concurrent users. Microsoft Azure added 120,000 NVIDIA H200 NVL GPUs in late 2025 to support GitHub Copilot and Azure OpenAI endpoints, which processed more than 50 billion API calls in December 2025. Oracle Cloud Infrastructure reported 99.95% uptime for GPU inference workloads after adopting liquid-cooled rack designs that keep junction temperatures below 75 °C. AWS introduced Inferentia 3 custom silicon in March 2026, delivering triple the throughput of Inferentia 2, yet NVIDIA Blackwell NVL remains ahead in mixed-precision workloads that exploit FP8 and INT4 quantization. Meta revealed that inference infrastructure consumed USD 18 billion of its USD 40 billion 2025 capital budget, underscoring the strategic priority of owning rather than leasing capacity. As latency targets for conversational AI tighten from 500 milliseconds in 2024 to less than 200 milliseconds in 2026, demand for GPUs with high-bandwidth memory and low-latency interconnects continues to accelerate.

Rapid Proliferation of Recommendation Engines in E-commerce Platforms

Real-time personalization now operates at sub-10-millisecond latency, forcing retailers to adopt inference GPUs that manage sparse embeddings and dynamic features without batch delays. Amazon Personalize increased inference throughput in 2025 as merchants migrated from CPU-based collaborative filtering to GPU-accelerated deep learning models. Alibaba Cloud's Hanguang 800 chip cut recommendation latency from 35 milliseconds to 12 milliseconds on Taobao and Tmall, reducing per-query energy consumption by 60% during the 2025 Singles' Day peak. Shopify integrated NVIDIA TensorRT-LLM in September 2025, enabling product-discovery models to adapt to inventory changes within 5 minutes and boosting conversion rates for pilot merchants. ByteDance stated that TikTok Shop processes 400 million product impressions per hour on NVIDIA A100 and H100 GPUs, with inference costs representing less than 0.02% of gross merchandise value due to aggressive model pruning.

High Up-Front Capital Cost of High-End Inference GPUs

List prices for NVIDIA H200 NVL units exceed USD 40,000, creating a significant barrier for mid-tier enterprises that lack venture debt or cloud credits. Dell Technologies stated that AI-optimized server average selling prices rose 35% year over year due to high-bandwidth memory and liquid-cooling requirements. Supermicro reported 16-week lead times for GPU servers and required 50% deposits, extending deliveries into late 2026. Equinix data shows AI inference racks consume 25 kilowatts on average, driving a premium in colocation charges. NVIDIA's DGX Cloud subscription at USD 5.50 per GPU-hour offers an alternative, but ownership remains cost-effective only when utilization stays above 60%.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Computer Vision across Industrial Automation Lines

- Growing Adoption of Conversational AI in Customer Support Operations

- Power and Cooling Constraints in Edge Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud and data-center installations held 60.17% of the AI inference GPU market share in 2025 as hyperscalers pooled resources to serve billions of daily API calls. Microsoft Azure's addition of 120,000 H200 NVL units in late 2025 enabled 50 billion GitHub Copilot calls in a single month, underscoring the throughput criteria that dominate procurement decisions. Meta's USD 18 billion allocation to inference infrastructure further illustrates the pivot from training to serving.

Edge deployments, advancing at 31.53% CAGR, gain traction where latency budgets deny round-trip cloud processing. Tesla's Full-Self-Driving computer processes 2,300 camera frames per second on custom accelerators, demonstrating the deterministic performance edge applications demand. Industrial automation similarly favors on-device inference to meet control-loop timing requirements, but strict power envelopes constrain GPU selection to sub-60-watt modules, such as the Jetson AGX Orin. The AI inference GPU market thus bifurcates between power-rich hyperscale facilities and constrained edge sites.

Geography Analysis

Asia-Pacific accounted for 69.52% of revenue in 2025 and is forecast to grow at a 31.92% CAGR through 2031, supported by sovereign AI programs, hyperscale partnerships, and aggressive data center expansion. Huawei shipped more than 50,000 Ascend 910C accelerators in 2025 after export restrictions limited NVIDIA H100 availability. Reliance Jio and NVIDIA formed a joint venture in September 2025 to install 100,000 H100 GPUs by mid-2027, anchoring India's push for enterprise AI services. Singapore and Thailand approved new liquid-cooled campuses in 2026, adding 800 megawatts of capacity that will open to GPU tenants in 2027.

The demand for AI inference GPUs in North America is driven by hyperscale cloud providers and regulated enterprises that prefer on-premises inference to meet data-sovereignty mandates. AWS released Inferentia 3 in July 2025 and reported 40% lower latency for Stable Diffusion pipelines after migrating to TensorRT optimization. JPMorgan Chase operates a private cloud with more than 10,000 NVIDIA H100 GPUs, underscoring the bank's preference for owned infrastructure for compliance-sensitive workloads. Canadian energy firms started pilot deployments of Groq language-processing units in early 2026 for real-time well-log interpretation, signaling rising interest in deterministic-latency silicon.

Europe's AI Act adds documentation and transparency obligations, lengthening deployment cycles. Siemens showed compliance is achievable; its Gaudi 3-based Simatic AI platform reduced semiconductor-fab downtime by 18% while meeting mandated risk-assessment disclosures. France and Germany earmarked EUR 2 billion (USD 2.18 billion) for sovereign inference cloud programs that will come online in 2028, indicating pent-up demand once regulatory clarity improves.

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Technologies, Inc.

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- Baidu, Inc.

- Microsoft Corporation

- Graphcore Ltd.

- Tenstorrent Inc.

- Mythic AI, Inc.

- Flex Logix Technologies, Inc.

- Imagination Technologies Ltd.

- Arm Holdings plc

- Cerebras Systems, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Generative AI Services in Hyperscale Data Centers

- 4.2.2 Rapid Proliferation of Recommendation Engines in E-commerce Platforms

- 4.2.3 Expansion of Computer Vision across Industrial Automation Lines

- 4.2.4 Growing Adoption of Conversational AI in Customer Support Operations

- 4.2.5 Emergence of Transformer-Pruning Optimized Inference GPUs

- 4.2.6 Availability of Open-Source Inference Compilers Lowering TCO

- 4.3 Market Restraints

- 4.3.1 High Up-Front Capital Cost of High-End Inference GPUs

- 4.3.2 Power and Cooling Constraints in Edge Deployments

- 4.3.3 Supply-Chain Volatility for Advanced Packaging Substrates

- 4.3.4 Rising Competition from RISC-V and Custom ASIC AI Accelerators

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Threat of Substitutes

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Bargaining Power of Suppliers

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud / Data Center

- 5.1.2 Edge

- 5.1.3 Embedded / On-Device

- 5.2 By Form Factor

- 5.2.1 PCIe GPUs

- 5.2.2 SXM / OAM GPUs

- 5.2.3 Embedded Modules

- 5.3 By Application

- 5.3.1 Generative AI

- 5.3.2 Computer Vision

- 5.3.3 Recommendation Systems

- 5.3.4 Autonomous Systems

- 5.3.5 NLP / Conversational AI

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 South Korea

- 5.4.3.4 India

- 5.4.3.5 Southeast Asia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies, Inc.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Huawei Technologies Co., Ltd.

- 6.4.7 Baidu, Inc.

- 6.4.8 Microsoft Corporation

- 6.4.9 Graphcore Ltd.

- 6.4.10 Tenstorrent Inc.

- 6.4.11 Mythic AI, Inc.

- 6.4.12 Flex Logix Technologies, Inc.

- 6.4.13 Imagination Technologies Ltd.

- 6.4.14 Arm Holdings plc

- 6.4.15 Cerebras Systems, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment