|

시장보고서

상품코드

2065519

자동차용 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Automotive GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

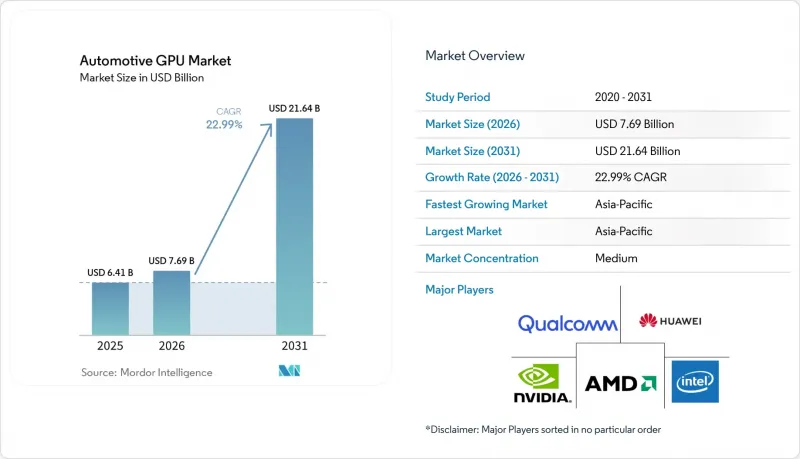

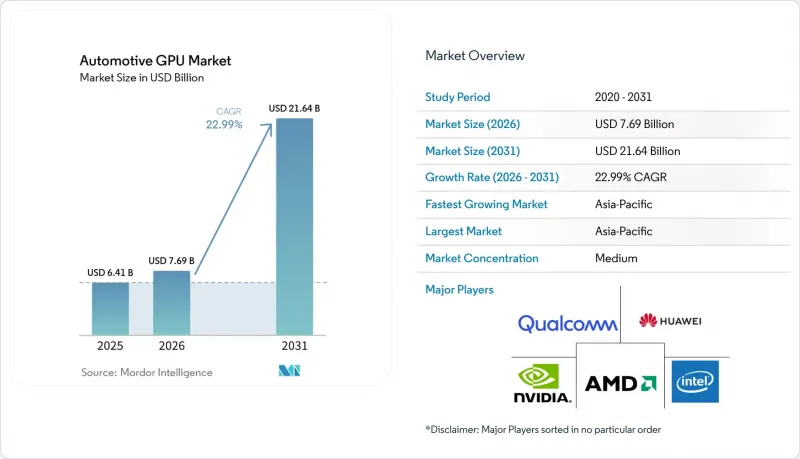

Mordor Intelligence에 의하면, 자동차용 GPU 시장 규모는 2025년 64억 1,000만 달러로 평가되었고, 2026년에는 76억 9,000만 달러로 추정되고, 2026-2031년 CAGR 22.99%로 성장을 지속할 전망이며, 2031년에는 216억 4,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 GPU 유형별(통합형 GPU 및 디스크리트 GPU), 용도별(인포테인먼트 시스템, 디지털 콕핏 및 계기판 등), 차종별(승용차 및 상용차), 지역별(북미, 유럽, 아시아태평양, 남미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 자동차용 GPU 시장 동향 및 인사이트

GPU 기반 ADAS의 도입 확대

Euro NCAP의 5성급 평가에서는 현재 핸즈프리 브레이크, 운전자 모니터링, 카메라의 이중화 기능이 평가 대상으로 포함되어 있으며, 이로 인해 비전 트랜스포머 및 센서 퓨전을 실행할 수 있는 프로그래밍 가능한 그래픽 코어에 대한 수요가 발생하고 있습니다. 모바일 퍼스트 아키텍처에 이어, 기능 안전 목표를 충족하면서 수백 테라플롭스의 성능을 발휘하는 NVIDIA DRIVE Hyperion과 같은 자동차용 칩이 등장하고 있습니다. 중국 도시 지역의 자율주행 내비게이션 프로그램에서는 이와 유사한 연산 능력을 활용해 다차선 로터리를 관리하고 있으며, 현지 OEM 업체들은 해당 기능을 무선(OTA)으로 활성화할 수 있도록 디스크리트 가속기를 핵심으로 한 2028년형 모델 설계를 진행 중입니다. 이러한 추세는 전 세계적인 현상이지만, 능동 안전 기능에 대한 보험료 할인이 하드웨어 비용을 상쇄할 수 있는 지역에서 보급이 가장 빠르게 진행되고 있습니다. 생산 규모가 확대됨에 따라 규모의 경제 효과로 인해 단가가 하락하고, 도입 곡선은 더욱 넓어집니다.

소프트웨어 정의 차량으로의 전환

수십 개의 전자제어 장치를 중앙 컴퓨팅 스택에 통합함으로써 배선 무게가 줄어들고, 무선 업데이트 관리가 용이해지며, 각 OEM 업체는 각 등급 간에 반도체 비용을 분산시킬 수 있습니다. NVIDIA DRIVE Thor는 CPU, GPU 및 고속 네트워크 기능을 단일 다이에 통합하여, 조종석 그래픽, 배터리 열 관리, 경로 계획 등을 동시에 실행할 수 있습니다. MediaTek의 3나노미터 ‘Dimensity Auto Cockpit’ 플랫폼 역시 동일한 설계 철학을 채택하고 있으며, NVIDIA Blackwell GPU와 음성 및 비전 용도 전용 신경망을 결합하고 있습니다. 그 비즈니스 논리는 설득력이 있습니다. 이 소프트웨어는 수익 창출 기회를 열어주고, 차량을 10년 동안 최신 상태로 유지하며, 잔존 가치를 지켜줍니다. ISO 26262 및 보다 최신의 ISO/SAE 21434 사이버 보안 규정 세트와 같은 규제 프레임워크는 지속적인 배포에 필요한 규정 준수 기반을 제공합니다.

첨단 노드 GPU 공급망의 변동

각 파운드리 업체들은 자동차용 생산량보다 데이터센터용 가속기 생산을 계속 우선시하고 있으며, 그 결과 자동차 프로그램의 리드타임이 길어지고 있습니다. 고대역폭 메모리 공급은 여전히 부족하며, 현물 가격이 2025년 초 이후 두 배로 치솟으면서 일부 OEM 업체들은 RAM 용량을 줄여 제품을 출하할 수밖에 없는 상황입니다. 성숙 노드의 부족이 문제를 더욱 심각하게 만들고 있는데, 이는 전원 관리 IC와 센서 인터페이스가 동일한 생산 능력 풀을 공유하고 있기 때문입니다. 일본, 인도, 미국 정부는 신규 제조 공장에 대한 지원을 실시하고 있지만, 건설 일정을 고려할 때 2027년 하반기까지는 상황이 개선될 것으로 보기는 어렵습니다. 그 전까지는 완충 재고를 확보하고 여러 공급업체로부터 조달하는 것(다중 조달)이 주요 위험 완화 방안이 됩니다.

부문별 분석

2025년, 자동차용 GPU 시장 점유율의 59.38%를 차지한 것은 집적 소자로, 15W 미만의 소비 전력 범위 내에서 인포테인먼트 클러스터 및 보급형 ADAS를 지원합니다. 이러한 단일 다이 구조는 부품 원가를 절감하고 열 설계를 간소화합니다. Arm Mali GPU와 소형 신경망을 결합한 NXP의 i.MX 95는 하이퍼바이저를 사용하지 않고도 ASIL-B 요건을 충족하며, 이러한 균형을 잘 보여주고 있습니다. 인도나 동남아시아 등 대량 생산 지역에서는 이러한 특성이 가격에 민감한 부문의 요구와 부합하고 있어, 2020년대 중반까지 계속해서 시장을 주도할 것으로 확실시되고 있습니다.

한편, 프리미엄 OEM 각사가 레벨 3 기능을 염두에 둔 미래 지향적인 설계를 추진하는 가운데, 디스크리트 가속기 시장은 연평균 성장률(CAGR) 23.68%로 확대될 것으로 전망됩니다. NVIDIA DRIVE Thor는 Gatik사와 이스즈 자동차의 레벨 4 트럭에 탑재되어 있으며, 중앙 집중형 노드를 통해 2 페타플롭스를 넘는 처리 능력을 집약하고 있습니다. MediaTek의 콕핏 플랫폼에는 NVIDIA의 GPU가 탑재되어 있어, 디스크리트 GPU와 통합형 GPU의 경계를 모호하게 만들며, 게임 및 시각화를 위한 고해상도 레이 트레이싱을 구현하고 있습니다. 따라서 자율주행 로드맵이 가장 적극적인 북미, 유럽, 중국에서는 디스크리트 보드로 인한 자동차용 GPU 시장 규모가 다른 지역에 비해 현저히 확대될 전망입니다.

지역별 분석

아시아태평양은 2025년 매출의 67.41%를 차지한 것으로 평가되었으며, 연평균 성장률(CAGR) 23.88%로 성장할 것으로 전망됩니다. 중국은 적극적인 전기차 보급과 국내 반도체 장려 정책을 통해 수요를 뒷받침하고 있습니다. Horizon Robotics가 전면 카메라형 ADAS 시장을 주도하는 한편, NVIDIA는 도시 지역용 자율주행 컴퓨팅 계약에서 큰 점유율을 차지하고 있습니다. 일본과 한국은 메모리와 파워 디바이스를 공급하며, 지역의 밸류체인을 뒷받침하고 있습니다. 한편, 인도의 반도체 미션은 2027년 이후 가동을 시작할 예정인 제조 라인과 첨단 패키징 라인에 자금을 지원하고 있습니다.

북미에서는 고급차의 출시와 레벨 2 이상의 기능이 급속히 보급되면서 시장이 확대되고 있습니다. 제너럴 모터스(GM)는 향후 모든 모델에 NVIDIA의 컴퓨팅 기술을 도입하기로 결정했으며, 검증 과정에서는 Omniverse에서 생성된 합성 데이터를 활용하고 있습니다. 고속도로에서의 핸즈프리 운전에 대한 규제 당국의 관심이 높아짐에 따라, 중급 트림 차량에서도 해당 기능이 도입되고 있습니다. 캐나다의 한랭지 시험장은 센서 퓨전 스택의 신뢰성을 높여, 간접적으로 디스크리트 가속기의 설계 채택 대수를 늘리고 있습니다.

유럽은 생산 대수 면에서는 아시아태평양 지역에 뒤처져 있지만, 기능 안전의 엄격성 면에서는 앞서고 있습니다. Euro NCAP의 2025년 평가 프로토콜에서는 자동 제동 및 운전자 모니터링 기능이 충돌 안전 성능과 동등한 수준으로 평가되고 있어, 소형차 시장에서 프로그래머블 GPU에 대한 수요를 가속화하고 있습니다. 독일, 프랑스, 영국은 폭스바겐 그룹, 스텔란티스, BMW, 메르세데스-벤츠의 소프트웨어 정의 플랫폼에 대한 투자를 통해 가치 창출에서 주도적인 역할을 수행하고 있습니다. 지역별 탄소 배출량 감축 목표가 전기차 판매를 촉진하며, GPU의 잠재 시장을 더욱 확대시키고 있습니다.

남미, 중동 및 아프리카는 여전히 수요 규모가 비교적 작은 지역입니다. 브라질의 인포테인먼트 시스템 업그레이드와 사우디아라비아로의 고급 전기차 수입이 국지적인 수요를 창출하고 있지만, 반도체 인프라 부족과 낮은 평균 판매 가격으로 인해 보급률은 여전히 저조한 상태입니다. 향후에는 통합형 GPU를 포함한 KD 키트(KD kit)의 현지 조립을 통해 출하 대수가 증가할 가능성이 있지만, 총비용이 낮아지기 전까지는 디스크리트 가속기의 보급은 틈새 시장에 그칠 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the automotive gPU market size is expected to grow from USD 6.41 billion in 2025 to USD 7.69 billion in 2026 and is forecast to reach USD 21.64 billion by 2031 at a 22.99% CAGR over 2026-2031.

This report is Segmented by GPU Type (Integrated GPUs and Discrete GPUs), Application (Infotainment Systems, Digital Cockpit/Instrument Cluster, and More), Vehicle Type (Passenger Vehicles and Commercial Vehicles), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive GPU Market Trends and Insights

Increasing GPU-Accelerated ADAS Adoption

Euro NCAP five-star scoring now rewards hands-free braking, driver monitoring, and camera redundancy, creating a pull for programmable graphics cores capable of running vision transformers and sensor fusion. Mobile-first architectures have given way to automotive-grade chips such as NVIDIA DRIVE Hyperion that deliver several hundred teraFLOPS while meeting functional-safety targets. Chinese urban navigation-on-autopilot programs use similar compute to manage multilane roundabouts, and regional OEMs are designing 2028 models around discrete accelerators so that features can be enabled over the air. The trend is global, yet penetration is fastest where insurance discounts for active safety offset the cost of the hardware. As volume scales, economies of scale reduce unit pricing and further widen the adoption curve.

Shift Toward Software-Defined Vehicles

Consolidating dozens of electronic control units into a central compute stack lowers wiring mass, eases over-the-air update management, and lets OEMs amortize silicon across trim levels. NVIDIA DRIVE Thor integrates CPU, GPU, and accelerated networking on a single die so that cockpit graphics, battery thermal control, and path planning can run concurrently. MediaTek's 3-nanometer Dimensity Auto Cockpit platform follows a similar blueprint, pairing an NVIDIA Blackwell GPU with a dedicated neural engine for voice and vision applications. The commercial logic is compelling: software unlocks monetizable options and keeps vehicles current for a decade, protecting residual value. Regulatory frameworks such as ISO 26262 and the newer ISO/SAE 21434 cybersecurity rule set supply the compliance backbone needed for continuous deployment.

Supply Chain Volatility for Advanced Node GPUs

Foundries continue to prioritize data-center accelerators over automotive volumes, leaving vehicle programs exposed to longer lead times. High-bandwidth memory remains in tight supply, and spot prices have doubled since early 2025, prompting some OEMs to ship with reduced RAM footprints. Mature-node shortages compound the issue as power-management ICs and sensor interfaces share the same capacity pool. Governments in Japan, India, and the United States are subsidizing new fabrication plants, but build-out timelines mean relief is unlikely before late 2027. Until then, buffer inventories and multi-sourcing remain the main mitigation levers.

Other drivers and restraints analyzed in the detailed report include:

- Demand for High-Resolution Digital Cockpits

- Automakers' Partnerships with Semiconductor Suppliers

- Thermal Management Challenges in Automotive Environments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated devices accounted for 59.38% of the Automotive GPU market share in 2025, serving infotainment clusters and entry-level ADAS within power envelopes below 15 W. Their single-die construction reduces bill-of-materials costs and simplifies thermal design. NXP's i.MX 95, which mates an Arm Mali GPU with a small neural engine, exemplifies this balance by meeting ASIL-B targets without a hypervisor. In volume regions such as India and Southeast Asia, these attributes align with price-sensitive segments, ensuring continued dominance through the middle of the decade.

Discrete accelerators, however, are forecast to grow at a 23.68% CAGR as premium OEMs future-proof designs for Level 3 features. NVIDIA DRIVE Thor powers Gatik and Isuzu's Level 4 trucks, aggregating over 2 petaFLOPS in a centralized node. MediaTek's cockpit platform embeds an NVIDIA GPU, blurring the line between discrete and integrated GPUs and enabling high-fidelity ray tracing for gaming and visualization. The Automotive GPU market size attributed to discrete boards will thus expand disproportionately in North America, Europe, and China, where autonomy roadmaps are most aggressive.

Geography Analysis

Asia-Pacific captured 67.41% of 2025 revenue and is projected to expand at a 23.88% CAGR. China anchors demand through aggressive electric vehicle penetration and domestic chip incentives; Horizon Robotics leads the front-camera ADAS market while NVIDIA holds a significant share of urban autopilot compute contracts. Japan and South Korea supply memory and power devices, sustaining the regional value chain, whereas India's semiconductor mission funds fabrication and advanced packaging lines that will come online from 2027 onward.

North America pairs premium vehicle launches with strong Level 2+ uptake. General Motors is committed to NVIDIA compute across upcoming models and relies on synthetic data generated with Omniverse for validation. Regulatory focus on hands-free highway driving stimulates adoption even in mid-tier trims. Canada's cold-climate testing grounds add credibility to sensor-fusion stacks, indirectly boosting design-win volume for discrete accelerators.

Europe trails Asia-Pacific in volume yet leads in functional-safety rigor. Euro NCAP's 2025 assessment protocols place automated braking and driver monitoring on par with crashworthiness, accelerating demand for programmable GPUs in compact cars. Germany, France, and the United Kingdom dominate value contribution through software-defined platform investments by Volkswagen Group, Stellantis, BMW, and Mercedes-Benz. Regional carbon-emission targets reinforce electric vehicle sales, further enlarging the addressable GPU pool.

South America, the Middle East, and Africa remain relatively small demand regions. Brazil's infotainment upgrades and Saudi Arabia's premium electric imports create pockets of demand, but limited semiconductor infrastructure and lower average selling prices keep penetration modest. Over time, localized assembly of knock-down kits that include integrated GPUs may boost shipments, yet discrete-accelerator uptake will remain niche until total cost declines.

- Nvidia Corporation

- Qualcomm Technologies, Inc.

- Intel Corporation

- Advanced Micro Devices, Inc.

- Imagination Technologies Limited

- Arm Ltd.

- Mobileye Global Inc.

- MediaTek Inc.

- Huawei Technologies Co., Ltd.

- VeriSilicon Holdings Co., Ltd.

- Socionext Inc.

- Cadence Design Systems, Inc.

- ROHM Co., Ltd.

- Vivante Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing GPU-Accelerated ADAS Adoption

- 4.2.2 Shift Toward Software-Defined Vehicles

- 4.2.3 Demand for High-Resolution Digital Cockpits

- 4.2.4 Automakers' Partnerships with Semiconductor Suppliers

- 4.2.5 Rise of Zonal Architectures Enabling Centralized Computing

- 4.2.6 Emergence of Open-Source GPU Compute Frameworks

- 4.3 Market Restraints

- 4.3.1 Thermal Management Challenges in Automotive Environments

- 4.3.2 Supply Chain Volatility for Advanced Node GPUs

- 4.3.3 Cost Sensitivity in Mass-Market Vehicle Segments

- 4.3.4 Certification Lag for Safety-Critical GPU Software

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Threat of Substitutes

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By GPU Type

- 5.1.1 Integrated GPUs

- 5.1.2 Discrete GPUs

- 5.2 By Application

- 5.2.1 Infotainment Systems

- 5.2.2 Digital Cockpit / Instrument Cluster

- 5.2.3 ADAS and Autonomous Driving

- 5.3 By Vehicle Type

- 5.3.1 Passenger Vehicles

- 5.3.2 Commercial Vehicles

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 South Korea

- 5.4.3.4 India

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nvidia Corporation

- 6.4.2 Qualcomm Technologies, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Advanced Micro Devices, Inc.

- 6.4.5 Imagination Technologies Limited

- 6.4.6 Arm Ltd.

- 6.4.7 Mobileye Global Inc.

- 6.4.8 MediaTek Inc.

- 6.4.9 Huawei Technologies Co., Ltd.

- 6.4.10 VeriSilicon Holdings Co., Ltd.

- 6.4.11 Socionext Inc.

- 6.4.12 Cadence Design Systems, Inc.

- 6.4.13 ROHM Co., Ltd.

- 6.4.14 Vivante Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment