|

시장보고서

상품코드

2065524

미국의 의료용 튜브 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Medical Tubing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

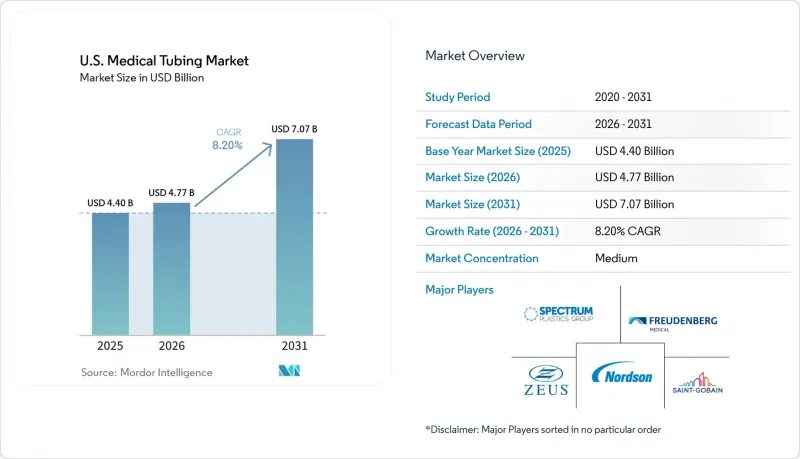

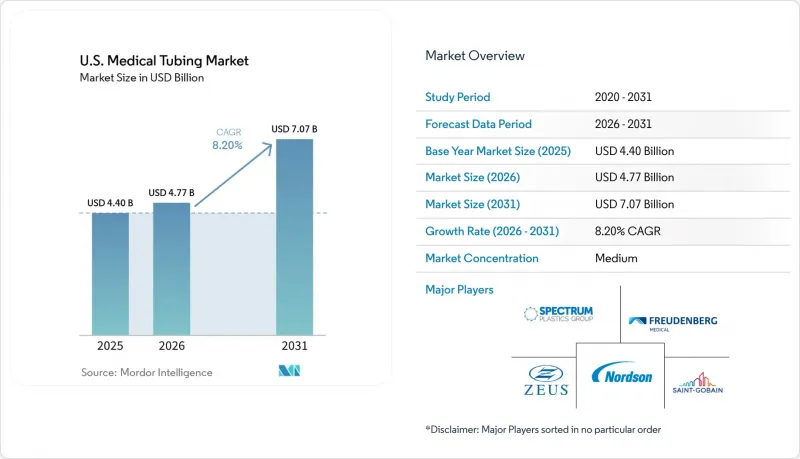

Mordor Intelligence에 의하면, 미국의 의료용 튜브 시장 규모는 2025년 44억 달러로 평가되었고, 2026년에는 47억 7,000만 달러로 추정되고, 2026-2031년 CAGR 8.20%로 성장을 지속할 전망이며, 2031년에는 70억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 소재별(플라스틱, 고무, 특수 폴리머), 구조별(싱글 루멘, 멀티 루멘, 공압출, 테이퍼 및 범프, 편조, 풍선, 열수축, 마이크로 압출 튜브), 용도별(10종), 최종 사용자별(5종), 제조 공정별(6종), 지역별(미국)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 의료용 튜브 시장 동향 및 분석

저침습 및 카테터를 이용한 시술 건수 증가

미국 의료용 튜브 시장은 개복 수술에서 카테터를 이용한 치료로 전환되는 추세를 원동력으로 삼아 눈부신 성장을 이루고 있습니다. 경카테터 대동맥판막 치환술(TAVR)의 연간 시술 건수는 10만 건을 넘어섰으며, 경카테터 승모판막 에지-투-에지 수복술의 연간 시술 건수도 1만 5,000건을 돌파했습니다. 이러한 구조적 심장 질환 치료 증가는 수요 양상을 완전히 바꿔놓고 있습니다. 왜냐하면 최신 카테터 시스템에는 더 엄격한 공차, 더 얇은 벽 두께, 다층 구조의 샤프트를 갖춘 정교한 설계가 요구되기 때문입니다. 이러한 기술의 발전으로 인해 고품질의 카테터 라이너, 보강 샤프트 및 다중 소재 튜브에 대한 수요가 증가하고 있습니다. 또한, 외래수술센터(ASC)의 확대로 조달 채널이 다양화되면서 더 많은 공급업체가 시장에 진입할 기회가 생기고 있습니다.

감염 관리 및 의료 현장에서 일회용 튜브에 대한 수요 증가

입원 환자, 외래 환자 및 시술 현장 전반에 걸쳐 감염 관리 요건이 강화됨에 따라 일회용 튜브에 대한 수요가 증가하고 있습니다. 사전 멸균 처리된 일회용 튜브 어셈블리는 위험 저감 프로토콜을 준수하며, 재처리 부담을 줄여줍니다. 이러한 변화로 인해 교체 빈도가 증가함에 따라, 투여 세트, 펌프용 튜브 및 멸균된 수액 어셈블리의 교체 주기가 빨라지고 있습니다. FDA가 업데이트한 품질 프레임워크는 의료기기 제조업체에 대한 위험 관리와 프로세스 관리를 중시함으로써 이러한 추세를 더욱 뒷받침하고 있습니다.

FDA에 의한 생체적합성 및 추출물 특성 평가에 따른 부담

미국의 의료용 튜브 시장에서 생체적합성 및 추출물에 대한 평가는 제품 개발자들에게 큰 과제가 되고 있습니다. FDA가 ISO 10993 규격을 준수함에 따라, 튜브, 특히 약물 전달, 투석 및 수액 주입에 사용되는 튜브에 대한 독성학적 심사 및 재료 평가가 더욱 엄격해졌습니다. 오랜 사용 실적이 있는 기존 PVC나 실리콘 시스템과 달리, 새로운 고분자 설계는 더욱 엄격한 심사를 받고 있습니다. 이로 인해 개발 기간이 길어질 뿐만 아니라, 시제품 단계에서 양산 단계로의 전환도 저해되고 있습니다. 또한, 연방관보(Federal Register)에 게재된 QMSR 관련 규정 제정으로 인해 설계 관리 및 문서화에 관한 추가 의무가 부과됨에 따라, 신규 튜브 설계가 규제 대상 생산에 도입되는 시기가 더욱 지연되고 있습니다.

부문별 분석

특수 폴리머는 미국 의료용 튜브 시장에서 가장 빠르게 성장하고 있는 소재 부문으로, 2026-2031년 연평균 성장률(CAGR) 10.18%를 나타낼 것으로 전망됩니다. 첨단 카테터 및 약물 전달 시스템의 설계에서는 범용 소재로는 일관되게 제공할 수 없는 특성이 점점 더 요구되고 있습니다. PEBA, PEEK, 열가소성 폴리우레탄 등의 소재는 보다 엄격한 치수 관리, 굴곡 내성의 향상, 뛰어난 화학적 안정성 덕분에 선호되고 있습니다. 이러한 변화는 튜브의 성능이 기기의 취급에 직접적인 영향을 미치는 혈관용, 신경혈관용 및 저침습적 용도에서 가장 두드러집니다.

2025년, 플라스틱 튜브는 미국 의료용 튜브 시장에서 38.12%의 점유율을 차지했으며, 이는 대량 생산되는 일회용 제품 및 정맥 내 투여 용도에서 플라스틱 튜브가 확고한 입지를 차지하고 있음을 반영합니다. PVC는 비용 효율성, 가공성, 그리고 광범위한 생체 적합성에 관한 실증 데이터를 바탕으로 여전히 큰 인기를 누리고 있습니다. 실리콘 및 라텍스 기반 제품이 주류를 이루는 고무 튜브는 연동 펌프 시스템, 호흡 회로 및 장기 배액 용도에서 필수적입니다.

2025년, 미국 의료용 튜브 시장에서 싱글 루멘 튜브는 40.25%를 차지했으며, 가장 큰 구조 유형이 되었습니다. 이러한 단순한 구조는 수액 세트나 카테터 샤프트와 같은 대량 생산 용도에 적합하며, 생산 효율성과 기존 압출 성형 플랫폼과의 호환성을 보장합니다. 이 구조는 병원이나 외래 진료 현장에서 널리 사용되고 있는 체액 관리 제품에 없어서는 안 될 요소입니다. 싱글 루멘 튜브는 폭넓은 수요와 지속적인 교체 수요 덕분에 여전히 시장을 독점하고 있습니다.

마이크로 압출 성형 및 마이크로 보어 튜브는 2026-2031년 연평균 성장률(CAGR) 10.75%를 기록했으며, 가장 빠르게 성장하고 있는 구조 부문입니다. 이러한 성장은 신경혈관 접근 및 로봇 보조 시스템 분야에서 카테터의 소형화에 힘입어 이루어지고 있으며, 카테터프로파일이 작아짐에 따라 내비게이션 성능과 치료 성과가 향상됩니다. 또한, 첨단 카테터 샤프트에 여러 기능이 통합됨에 따라 멀티루멘 및 공압출 튜브도 주목을 받고 있습니다. Zeus사는 2026년 1월, 최신 카테터 구조에 맞추어 설계된 ‘PFX 플랫폼’과 ‘PFX Flex Sub-Lite-Wall’을 출시하며 이러한 추세를 강조했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the u.S. medical tubing market size is expected to grow from USD 4.40 billion in 2025 to USD 4.77 billion in 2026 and is forecast to reach USD 7.07 billion by 2031 at 8.20% CAGR over 2026-2031.

This report is Segmented by Material (Plastic, Rubber, Specialty Polymers), Structure (Single-Lumen, Multi-Lumen, Co-Extruded, Tapered/Bump, Braided, Balloon, Heat-Shrink, Micro-Extruded Tubing), Application (10 Types), End User (5 Types), Manufacturing Process (6 Types), and Geography (United States). Market Forecasts are Provided in Terms of Value (USD).

U.S. Medical Tubing Market Trends and Insights

Rising Minimally Invasive and Catheter-Based Procedure Volumes

The United States medical tubing market is experiencing significant growth, driven by the transition from open surgeries to catheter-based interventions. Transcatheter aortic valve replacements have exceeded 100,000 annual procedures, while mitral transcatheter edge-to-edge repairs have surpassed 15,000 cases annually. This increase in structural heart procedures is reshaping demand, as modern catheter systems require advanced designs with tighter tolerances, thinner walls, and layered shaft constructions. These advancements are driving demand for premium catheter liners, reinforced shafts, and multi-material tubing. Additionally, the expansion of ambulatory surgical centers is diversifying procurement channels, creating opportunities for more suppliers to enter the market.

Higher Single-Use Tubing Demand from Infection Control and Care Settings

Rising infection control requirements across inpatient, outpatient, and procedural settings are boosting demand for single-use tubing. Pre-sterilized and disposable tubing assemblies align with risk reduction protocols and reduce the burden of reprocessing. This shift increases replacement frequency, accelerating the refresh cycle for administration sets, pump tubing, and sterile fluid-transfer assemblies. The FDA's updated quality framework further supports this trend by emphasizing risk management and process control for device manufacturers.

FDA Biocompatibility and Extractables Characterization Burden

In the U.S. medical tubing market, biocompatibility and extractables assessments pose significant challenges for product developers. The FDA's alignment with ISO 10993 standards has intensified the toxicological reviews and material assessments for tubing, especially those used in drug delivery, dialysis, and infusion. New polymer designs, lacking the extensive usage history of established PVC or silicone systems, face heightened scrutiny. This not only extends development timelines but also hampers the transition from prototype to commercial production. Furthermore, the Federal Register's rulemaking on QMSR introduces additional design-control and documentation mandates, further delaying the entry of new tubing designs into regulated production.

Other drivers and restraints analyzed in the detailed report include:

- Aging Chronic-Care Population Lifting Dialysis, Cardiovascular, and Home Care Tubing Demand

- Home Infusion and Ambulatory Care Migration Expanding Pump and Fluid-Transfer Tubing Demand

- Volatility in Medical-Grade Silicone, PVC, Fluoropolymer, and Specialty Material Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Specialty polymers are the fastest-growing material segment in the United States medical tubing market, with a projected CAGR of 10.18% from 2026 to 2031. Advanced catheter and drug delivery designs increasingly require properties that commodity materials cannot consistently provide. Materials like PEBA, PEEK, and thermoplastic polyurethane are preferred for tighter dimensional control, enhanced kink resistance, and superior chemical stability. This shift is most significant in vascular, neurovascular, and minimally invasive applications, where tubing performance directly impacts device handling.

In 2025, plastic tubing held a 38.12% share of the United States medical tubing market, reflecting its strong presence in high-volume disposable and IV administration applications. PVC remains popular due to its cost efficiency, processability, and extensive biocompatibility documentation. Rubber tubing, led by silicone and latex-based formats, is essential in peristaltic pump systems, respiratory circuits, and long-duration drainage applications.

Single-lumen tubing accounted for 40.25% of the United States medical tubing market in 2025, making it the largest structural format. Its simplicity suits bulk applications like IV sets and catheter shafts, ensuring production efficiency and compatibility with conventional extrusion platforms. This structure remains integral to fluid management products widely used in hospitals and ambulatory settings. Single-lumen tubing continues to dominate due to its broad demand and recurring replacement volumes.

Micro-extruded and microbore tubing is the fastest-growing structural segment, with a 10.75% CAGR from 2026 to 2031. This growth is driven by catheter miniaturization in neurovascular access and robotic-assisted systems, where smaller profiles enhance navigation and outcomes. Multi-lumen and co-extruded tubing are also gaining traction as advanced catheter shafts integrate multiple functionalities. Zeus highlighted this trend in January 2026 with the launch of the PFX platform and PFX Flex Sub-Lite-Wall, designed for modern catheter construction.

List of Companies Covered in this Report:

- Accu-Tube LLC

- Bentec Medical, LLC

- Compagnie de Saint-Gobain S.A.

- Duke Extrusion

- Freudenberg Medical, LLC

- Kent Elastomer Products, Inc.

- Medical Extrusion Technologies, Inc.

- MicroLumen, Inc.

- Micro-Tek Corporation

- NewAge Industries, Inc.

- Nordson

- One Medical Extrusion

- Polyzen, Inc.

- Putnam Plastics Corporation

- Raumedic

- Spectrum Plastics Group

- TE Connectivity Ltd.

- Teel Plastics, Inc.

- Tekni-Plex, Inc.

- Zeus Company LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Minimally Invasive and Catheter-Based Procedure Volumes

- 4.2.2 Higher Single-Use Tubing Demand from Infection Control and Care Standardization

- 4.2.3 Aging Chronic-Care Population Lifting Dialysis, Cardiovascular, and Urology Tubing Volumes

- 4.2.4 Home Infusion and Ambulatory Care Migration Expanding Pump and Transfer Tubing Demand

- 4.2.5 PFAS-Free Liner Substitution Cycle Creating Redesign-Driven Replacement Demand

- 4.2.6 Electrophysiology and Structural-Heart Device Scaling Increasing Microbore Reinforced Shaft Demand

- 4.3 Market Restraints

- 4.3.1 FDA Biocompatibility and Extractables Characterization Burden

- 4.3.2 Volatility in Medical-Grade Silicone, PVC, Fluoropolymer, and Specialty Resin Supply

- 4.3.3 PFAS Phase-Down Forces Revalidation of Catheter Liners and Process Windows

- 4.3.4 QMSR, Connector, and DEHP-Related Redesign Costs Slow Product Changeovers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Plastic

- 5.1.2 Rubber

- 5.1.3 Specialty Polymers

- 5.2 By Structure

- 5.2.1 Single-lumen Tubing

- 5.2.2 Multi-lumen Tubing

- 5.2.3 Co-extruded / Multi-layer Tubing

- 5.2.4 Tapered / Bump Tubing

- 5.2.5 Braided / Reinforced Tubing

- 5.2.6 Balloon Tubing

- 5.2.7 Heat-shrink Tubing

- 5.2.8 Micro-extruded / Microbore Tubing

- 5.3 By Application

- 5.3.1 Bulk Disposable Tubing

- 5.3.2 Catheters & Cannulae

- 5.3.3 Drug Delivery Systems

- 5.3.4 Dialysis & Renal Care Tubing

- 5.3.5 IV Infusion & Fluid Administration Tubing

- 5.3.6 Respiratory, Anesthesia & Gas Supply Tubing

- 5.3.7 Enteral Feeding & Gastrointestinal Tubing

- 5.3.8 Suction, Smoke Evacuation & Drainage Tubing

- 5.3.9 Biopharmaceutical Laboratory & Processing Tubing

- 5.3.10 Peristaltic Pump Tubing

- 5.4 By End User

- 5.4.1 Hospitals & Integrated Delivery Networks

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Physician Offices & Specialty Clinics

- 5.4.4 Home Care Setting

- 5.4.5 Medical Laboratories & Biopharmaceutical Facilities

- 5.5 By Manufacturing Process

- 5.5.1 Single-screw Extrusion

- 5.5.2 Twin-screw Extrusion

- 5.5.3 Micro-extrusion

- 5.5.4 Co-extrusion / Multi-layer Extrusion

- 5.5.5 Braiding, Coiling & Secondary Shaft Reinforcement

- 5.5.6 Heat-shrink & Reflow Processing

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Accu-Tube LLC

- 6.3.2 Bentec Medical, LLC

- 6.3.3 Compagnie de Saint-Gobain S.A.

- 6.3.4 Duke Extrusion

- 6.3.5 Freudenberg Medical, LLC

- 6.3.6 Kent Elastomer Products, Inc.

- 6.3.7 Medical Extrusion Technologies, Inc.

- 6.3.8 MicroLumen, Inc.

- 6.3.9 Micro-Tek Corporation

- 6.3.10 NewAge Industries, Inc.

- 6.3.11 Nordson Corporation

- 6.3.12 One Medical Extrusion

- 6.3.13 Polyzen, Inc.

- 6.3.14 Putnam Plastics Corporation

- 6.3.15 RAUMEDIC AG

- 6.3.16 Spectrum Plastics Group

- 6.3.17 TE Connectivity Ltd.

- 6.3.18 Teel Plastics, Inc.

- 6.3.19 Tekni-Plex, Inc.

- 6.3.20 Zeus Company LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment