|

시장보고서

상품코드

2065526

미국의 스마트 헬스케어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)US Smart Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

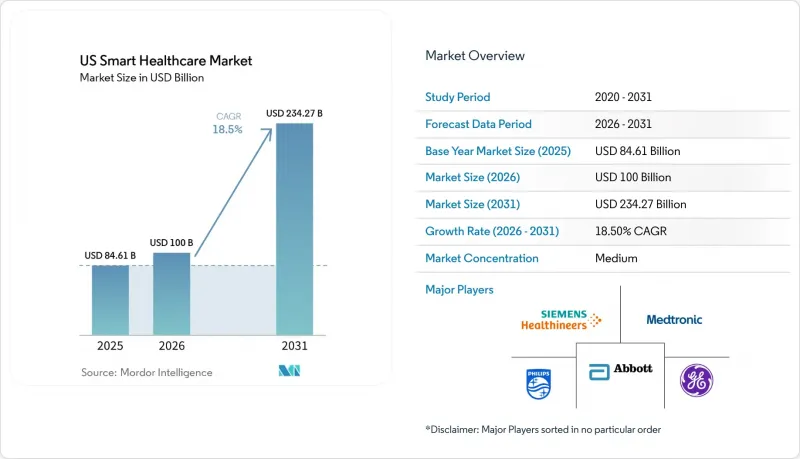

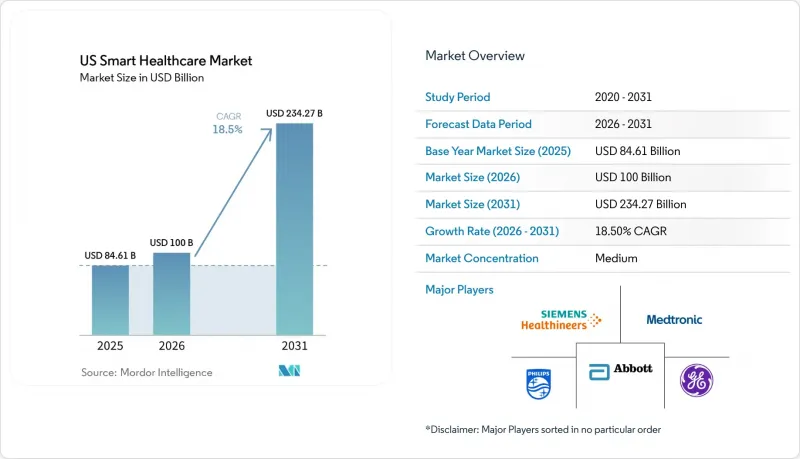

Mordor Intelligence에 의하면, 미국의 스마트 헬스케어 시장 규모는 2025년에 846억 1,000만 달러로 평가되었고, 2026년에 1,000억 달러로 추정되고, 2031년까지 2,342억 7,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 18.5%로 성장할 전망입니다.

본 보고서는 구성 요소별(하드웨어, 소프트웨어, 서비스), 기술별(AI, IoT, 클라우드, 원격의료, 웨어러블), 제품별(웨어러블, 모니터링, 전자건강기록(EHR), m헬스, 원격진료), 도입 형태별(웹 기반, SaaS, 하이브리드), 용도별(원격 환자 모니터링, 만성 질환, 피트니스, 복약 관리, 진단, 고령자), 최종 사용자별(병원, 재택 간호, 보험사, 제약 기업, 외래수술센터(ASC), 환자), 연결 방식별(유선, 무선)로 분류되어 있습니다. 금액은 달러(USD)로 표시되어 있습니다.

미국의 스마트 헬스케어 시장 동향 및 인사이트

FHIR API 및 상호운용성 지원에 관한 지출

미국의 스마트 헬스케어 시장에서 상호운용성에 대한 투자는 장기적인 IT 목표에서 시급한 업무상 우선 과제로 전환되고 있습니다. 연방 규제가 효과적인 디지털 연결을 요구하는 가운데, 의료 서비스 제공업체와 보험사는 사전 승인, 환자 접근, 데이터 교환을 위한 업무 흐름을 현대화해야 한다는 압박에 점점 더 직면하고 있습니다. 컴플라이언스 비용은 초기 단계에 그치지 않고, 미들웨어, 테스트, 워크플로우 재설계, 버전 업그레이드 등이 필요합니다. 병원 및 보험 기관의 레거시 시스템은 최신 인터페이스와의 통합에 어려움을 겪고 있으며, 그 결과 통합 서비스, 워크플로우 자동화 및 플랫폼 업그레이드에 대한 지속적인 투자가 촉진되고 있습니다. 이로 인해 상호운용성 공급업체들에게 지속적인 수익 사이클이 형성되고 있습니다.

만성 질환으로 인한 RPM 및 가상 진료 수요

미국의 스마트 헬스케어 시장에서 원격 모니터링에 대한 수요는 기기 혁신보다는 만성 질환 관리의 경제성에 의해 주도되고 있습니다. 2026년 의사 보수 일정표에 따라 CPT 코드 99445 및 99470이 도입되어, 모니터링 기간이 더 짧은 경우나 에피소드형 진료 상황에서도 청구가 가능해졌습니다. 이번 변경으로 인해 기존의 장기 프로그램 외에도 더 많은 환자가 등록할 수 있게 되었습니다. 고혈압이나 당뇨병 등의 질환의 경우, 지급액이 측정 가능한 치료 성과와 연동되어 있기 때문에 의료 제공업체는 환자를 적극적으로 추적할 유인을 얻게 됩니다. 벤더 입장에서는 에피소드형 치료, 퇴원 후 관리, 그리고 복약 순응도 모니터링과 같은 업무 흐름에서 새로운 비즈니스 기회가 창출되고 있습니다.

사이버 보안 침해 위험과 시정 조치의 부담

사이버 보안은 미국의 스마트 헬스케어 시장에서 여전히 중대한 과제로 남아 있습니다. 2024년에 발생한 체인지 헬스케어(Change Healthcare)에 대한 랜섬웨어 공격은 1억 9,000만 건의 기록에 영향을 미쳤으며, 3분기까지 24억 5,700만 달러의 비용을 초래함으로써 시스템적 위험을 여실히 드러냈습니다. 2026년, HHS OCR은 4건의 랜섬웨어 사건에 대해 총 116만 5,000달러의 HIPAA 합의금을 부과하며 단속을 강화할 것임을 시사했습니다. 의료 서비스 제공업체와 보험사는 보안 강화, 감사, 복구 계획에 예산을 할당하고 있어 모니터링 장비, 분석 도구, 케어 플랫폼에 대한 투자가 뒤처지고 있습니다. 또한, 사이버 위험으로 인해 구매자들은 재택 간호 및 원격 모니터링 분야에서 엔드포인트 확장에 신중한 태도를 보이고 있습니다.

부문별 분석

2025년, 미국의 스마트 헬스케어 시장에서 하드웨어는 46.21%를 차지했습니다. 이는 병원, 진단센터, 가정 내 커넥티드 기기에 대한 투자가 주도한 결과입니다. 하드웨어는 원격 모니터링 및 원격 진단에 필수적이지만, 프로그램의 규모가 확대됨에 따라 그 장기적인 가치는 감소하고 있으며, 연결성과 규정 준수를 보장하는 소프트웨어 및 서비스로 초점이 이동하고 있습니다.

서비스 분야는 2031년까지 연평균 21.2%의 성장률을 보일 것으로 예상되며, 각 구성 요소 중 가장 높은 성장률을 보이고 있습니다. 구독형 모니터링, 도입 지원, 플랫폼 관리를 통해 일회성 기기 판매가 지속적인 수익으로 전환되고 있습니다. 하드웨어, 소프트웨어, 관리형 서비스를 결합한 번들형 솔루션은 단일 디바이스를 대체할 수 있는 확장 가능한 대안을 제공합니다.

2025년 기준으로 기술별 분석에 따르면, IoT는 미국 스마트 헬스케어 시장 점유율의 40.45%를 차지했으며, 환자 모니터링, 자산 추적, 워크플로우 자동화 분야에서 핵심적인 데이터 계층으로 기능하고 있습니다. 그 구조적 중요성은 일관된 데이터 수집을 가능하게 하고, 다른 인텔리전스 계층을 뒷받침한다는 점에 있습니다.

인공지능(AI)은 2031년까지 연평균 성장률(CAGR) 22.8%로 성장할 것으로 예상되며, 가장 빠르게 성장하는 기술 분야가 될 전망입니다. AI 도구는 병원 업무 흐름에 점점 더 통합되면서 의료진의 번아웃을 완화하고 문서 작성 효율을 높이고 있습니다. 이로 인해 기업 내 도입이 가속화되고 있으며, 연결된 인프라의 가치가 높아지고 있습니다.

2025년, 스마트 웨어러블 기기는 임상 모니터링 및 일반 소비자의 건강 관리에 활용된 것을 배경으로 38.3%의 점유율을 기록하며 미국 스마트 헬스케어 시장을 주도했습니다. 지속적인 데이터 수집과 다양한 치료 경로를 지원하는 능력을 바탕으로, 환자 모니터링 및 환자 참여 분야에서 핵심적인 역할을 수행하고 있습니다.

원격의료 플랫폼은 2031년까지 연평균 성장률(CAGR) 23.5%를 나타낼 것으로 예측되며, 이는 각 제품군 중 가장 높은 성장률입니다. 대면, 온라인, 비동기 방식 등 어떤 형태로든 진료를 제공할 수 있는 유연성 덕분에, 원격의료는 단순한 편의성 향상을 위한 도구에서 만성 질환 관리 및 진료 조정 모델의 중요한 구성 요소로 그 위상을 높여가고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the uS smart healthcare market size is projected to be USD 84.61 billion in 2025, USD 100 billion in 2026, and reach USD 234.27 billion by 2031, growing at a CAGR of 18.5% from 2026 to 2031.

This report is Segmented by Component (Hardware, Software, Services), Technology (AI, Iot, Cloud, Telehealth, Wearables), Product (Wearables, Monitoring, EHR, Mhealth, Telemedicine), Deployment (Web-Based, Saas, Hybrid), Application (RPM, Chronic Disease, Fitness, Medication, Diagnosis, Elderly), End User (Hospitals, Home Care, Payers, Pharma, Ascs, Patients), Connectivity (Wired, Wireless). Value (USD).

US Smart Healthcare Market Trends and Insights

FHIR API and Interoperability Compliance Spending

Interoperability spending has shifted from a long-term IT goal to an immediate operational priority in the United States smart healthcare market. Providers and payers face increasing pressure to modernize workflows for prior authorization, patient access, and data exchange as federal regulations demand effective digital connections. Compliance costs extend beyond initial milestones, requiring middleware, testing, workflow redesigns, and version upgrades. Legacy systems in hospitals and payer organizations struggle to integrate modern interfaces, driving ongoing investments in integration services, workflow automation, and platform upgrades. This creates a sustained revenue cycle for interoperability vendors.

Chronic-Disease-Led RPM and Virtual Care Demand

Remote monitoring demand in the United States smart healthcare market is driven by chronic care economics rather than device innovation. The 2026 Physician Fee Schedule introduced CPT codes 99445 and 99470, expanding billing eligibility to shorter monitoring windows and episodic care settings. This change allows more patients to enroll outside traditional long-term programs. Providers are incentivized to track patients proactively, as payments are tied to measurable outcomes for conditions like hypertension and diabetes. Vendors now have opportunities in episodic, post-discharge, and near-adherence monitoring workflows.

Cybersecurity Breach Exposure and Remediation Burden

Cybersecurity remains a critical challenge in the United States smart healthcare market. The 2024 Change Healthcare ransomware attack highlighted systemic risks, affecting 190 million records and resulting in USD 2.457 billion in costs through Q3. In 2026, HHS OCR imposed USD 1,165,000 in HIPAA settlements across four ransomware cases, reflecting stricter enforcement. Providers and payers are diverting budgets to security upgrades, audits, and recovery planning, delaying investments in monitoring devices, analytics tools, and care platforms. Cyber risks also make buyers cautious about expanding endpoints in home care and remote monitoring.

Other drivers and restraints analyzed in the detailed report include:

- Care-Team Productivity and Ambient Clinical AI Adoption

- Home-Based Care and Hospital-at-Home Digital Stack Expansion

- Legacy Integration and Budget Pressure in Community Providers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, hardware accounted for 46.21% of the United States smart healthcare market, driven by investments in connected devices across hospitals, diagnostic centers, and homes. While hardware is essential for remote monitoring and diagnostics, its long-term value declines as programs scale, shifting focus to software and services that ensure connectivity and compliance.

Services are projected to grow at 21.2% through 2031, the fastest among components. Subscription monitoring, implementation support, and platform administration are transforming one-time device sales into recurring revenue. Bundled solutions combining hardware, software, and managed services offer a scalable alternative to standalone devices.

IoT held 40.45% of the United States smart healthcare market share by technology in 2025, serving as the core data layer for patient monitoring, asset tracking, and workflow automation. Its structural importance lies in enabling consistent data capture, which supports other intelligence layers.

Artificial Intelligence is expected to grow at a 22.8% CAGR through 2031, making it the fastest-growing technology segment. AI tools are increasingly integrated into hospital workflows, reducing clinician burnout and improving documentation, which accelerates enterprise adoption and enhances the value of connected infrastructure.

Smart Wearable Devices led the United States smart healthcare market in 2025 with a 38.3% share, driven by their use in clinical monitoring and consumer health engagement. Their ability to support continuous data collection and multiple care pathways ensures their central role in patient monitoring and engagement.

Telemedicine Platforms are forecast to grow at a 23.5% CAGR through 2031, the fastest among products. The flexibility to deliver care in-person, virtually, or asynchronously has elevated telemedicine from a convenience tool to a critical component of chronic care and care coordination models.

List of Companies Covered in this Report:

- Abbott Laboratories

- American Well

- Athenahealth

- Baxter

- Doximity, Inc.

- eClinicalWorks

- Epic Systems

- GE Healthcare

- iRhythm Technologies

- Koninklijke Philips

- Masimo

- Medical Information Technology, Inc. (MEDITECH)

- Medtronic

- NextGen Healthcare

- Omnicell

- Oracle

- Resmed

- Siemens Healthineers

- Teladoc Health

- Veradigm Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 FHIR API and Interoperability Compliance Spending

- 4.2.2 Chronic-Disease-Led RPM and Virtual Care Demand

- 4.2.3 Care-Team Productivity and Ambient Clinical AI Adoption

- 4.2.4 Home-Based Care and Hospital-At-Home Digital Stack Expansion

- 4.2.5 CMS ACCESS Model Outcome-Aligned Reimbursement

- 4.2.6 TEFCA, QHIN, and Patient-Directed Data Mobility Acceleration

- 4.3 Market Restraints

- 4.3.1 Cybersecurity Breach Exposure and Remediation Burden

- 4.3.2 Legacy Integration and Budget Pressure in Community Providers

- 4.3.3 Rural Broadband and Digital-Literacy Access Gaps

- 4.3.4 Consent Fragmentation in Behavioral and Substance-Use Data Exchange

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of new entrants

- 4.7.2 Bargaining power of suppliers

- 4.7.3 Bargaining power of buyers

- 4.7.4 Threat of substitutes

- 4.7.5 Industry rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software and Platforms

- 5.1.3 Services

- 5.2 By Technology

- 5.2.1 Artificial Intelligence (AI)

- 5.2.2 Internet of Things (IoT)

- 5.2.3 Big Data Analytics

- 5.2.4 Cloud Computing

- 5.2.5 Blockchain

- 5.2.6 Telehealth Technologies

- 5.2.7 Wearable Technologies

- 5.3 By Product

- 5.3.1 Smart Wearable Devices

- 5.3.2 Smart Monitoring Devices

- 5.3.3 Electronic Health Records (EHR)

- 5.3.4 mHealth Applications

- 5.3.5 Telemedicine Platforms

- 5.3.6 Smart Pills & Connected Devices

- 5.4 By Deployment Model

- 5.4.1 On-premise

- 5.4.2 Web-based or Hosted

- 5.4.3 Cloud-based or SaaS

- 5.4.4 Hybrid

- 5.5 By Application

- 5.5.1 Remote Patient Monitoring

- 5.5.2 Chronic Disease Management

- 5.5.3 Fitness & Wellness

- 5.5.4 Clinical Workflow Management

- 5.5.5 Medication Management

- 5.5.6 Diagnosis & Treatment

- 5.5.7 Elderly Care

- 5.6 By End User

- 5.6.1 Hospitals & Clinics

- 5.6.2 Home Healthcare Settings

- 5.6.3 Diagnostic Centers

- 5.6.4 Healthcare Payers

- 5.6.5 Pharmaceutical & Biotechnology Companies

- 5.6.6 Ambulatory Surgical Centers

- 5.6.7 Patients/Consumers

- 5.7 By Connectivity

- 5.7.1 Wired

- 5.7.2 Wireless

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott

- 6.3.2 American Well Corporation

- 6.3.3 athenahealth, Inc.

- 6.3.4 Baxter International Inc.

- 6.3.5 Doximity, Inc.

- 6.3.6 eClinicalWorks, LLC

- 6.3.7 Epic Systems Corporation

- 6.3.8 GE HealthCare

- 6.3.9 iRhythm Technologies, Inc.

- 6.3.10 Koninklijke Philips N.V.

- 6.3.11 Masimo Corporation

- 6.3.12 Medical Information Technology, Inc. (MEDITECH)

- 6.3.13 Medtronic plc

- 6.3.14 NextGen Healthcare, Inc.

- 6.3.15 Omnicell, Inc.

- 6.3.16 Oracle

- 6.3.17 ResMed Inc.

- 6.3.18 Siemens Healthineers AG

- 6.3.19 Teladoc Health, Inc.

- 6.3.20 Veradigm Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment