|

시장보고서

상품코드

2065529

IT 및 통신 분야 인재 관리 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Talent Management In IT And Telecom - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

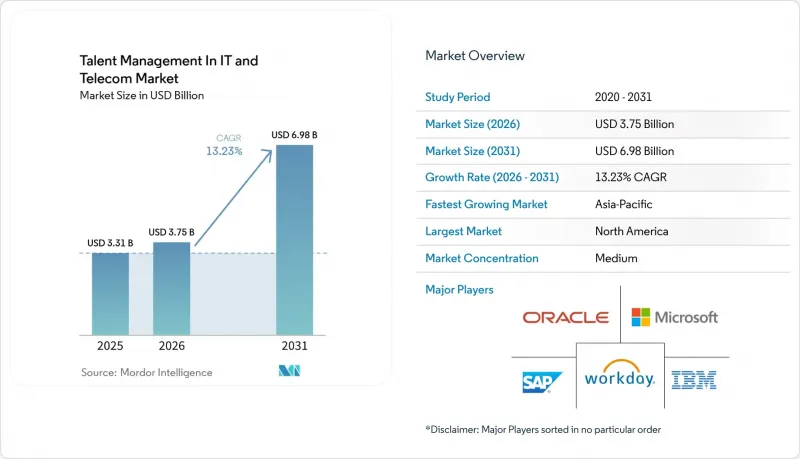

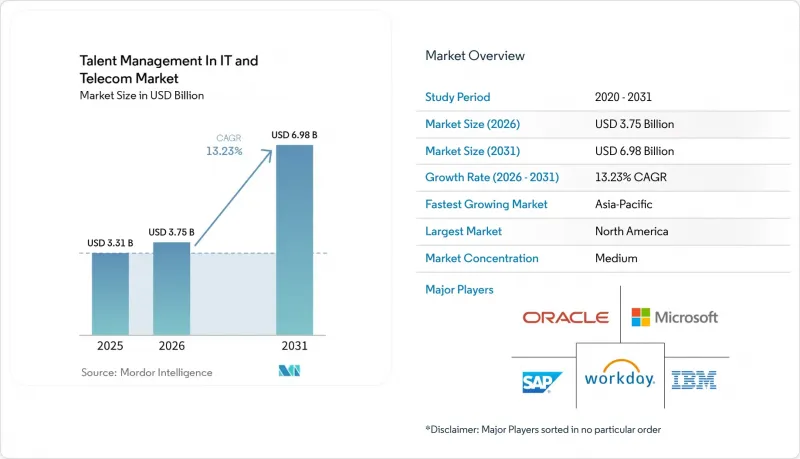

Mordor Intelligence에 의하면, IT 및 통신 분야 인재 관리 시장 규모는 2025년에 33억 1,000만 달러로 평가되었습니다. 2026년 37억 5,000만 달러에서 2031년까지 69억 8,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 13.23%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어, 서비스), 배포 방식(On-Premise, 클라우드), 기업 규모(대기업, 중소기업), 용도(직원 참여 및 경력 개발, 학습 및 역량 개발, 후계자 계획, 채용 및 인재 확보 등), 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 IT 및 통신 분야 인재 관리 시장 동향 및 인사이트

기술직 대상 AI 탑재 채용 봇 도입이 가속화되고 있습니다.

IT 및 통신 분야 인재 관리 시장에서 자율형 채용은 결정적인 운영 모델로 자리 잡고 있습니다. 이는 고용주가 기술 인력을 보다 신속하게 선발해야 할 뿐만 아니라, 채용 담당자의 부담을 줄여야 하기 때문입니다. Oracle과 에이트폴드 AI의 신제품 출시는 각 벤더들이 현재 에이전트 기반 면접 및 자동화된 채용 업무를 단순한 선택적 부가 기능이 아닌 핵심 기능으로 자리매김하고 있음을 보여줍니다. 통신 업계의 채용 과정에서 이는 특히 현장 엔지니어링, 클라우드, 사이버 보안 분야의 직무에서 중요합니다. 이러한 분야에서는 채용 지연이 서비스 제공이나 인프라 구축 프로그램의 지연으로 이어질 가능성이 있기 때문입니다. IT 및 통신 분야 인재 관리에서는 소싱, 면접, 기술 데이터를 보다 광범위한 인재 관리 시스템과 연동시키는 플랫폼이 점차 우위를 점하고 있습니다. 여전히 서로 연동되지 않은 채용 담당자용 도구에 의존하고 있는 벤더들은 자율형 에이전트가 채용 프로세스의 더 큰 부분을 담당하게 됨에 따라 채용 프로세스에서 배제될 위험이 높아지고 있습니다.

클라우드 전환의 물결이 SaaS 인사 관리 제품군을 뒷받침하고 있습니다.

클라우드 전환을 통해 IT 및 통신 분야 인재 관리를 강화하고 있습니다. 이는 구매자가 변동하는 직원 수나 프로젝트 구성에 대응할 수 있는 단일 인재 관리 시스템을 원하기 때문입니다. SAP의 SuccessFactors 2026년 상반기 릴리스에서는 AWS와의 양방향 및 제로 카피 데이터 공유 기능이 추가되어, SAP Cloud ERP, SAP Fieldglass, SAP SuccessFactors에 걸친 계획 연동이 실현되었습니다. 이는 연동된 클라우드 아키텍처로의 전환 추세를 반영한 것입니다. Workday의 2026년 봄 릴리스에서는 Databricks, Google Cloud, Snowflake 등의 플랫폼과의 양방향 액세스를 실현하는 개방형 표준을 채택한 ‘Workday Data Lake’도 도입되었습니다. IT 및 통신 업계에서 채용 및 인사 이동이 급격히 변화하는 상황에서는 인력, 재무 및 업무 계획 간의 일관성을 유지해야 하므로, 이러한 움직임은 중요합니다. 따라서 클라우드 아키텍처는 단순한 호스팅 옵션에 그치지 않고, IT 및 통신 분야 인재 관리 측면에서 인재의定着과 업무 운영을 좌우하는 중요한 요소가 되고 있습니다.

기존 HRIS 스택과의 통합에 따른 복잡성

통합의 복잡성은 IT 및 통신 분야 인재 관리, 특히 여러 국가에 걸친 인사 체제를 갖춘 대형 통신 사업자에게 있어 여전히 가장 뚜렷한 단기적 걸림돌로 작용하고 있습니다. 많은 통신 그룹에서는 수년에 걸친 합병을 통해 구축된 PeopleSoft, On-Premise형 SAP HCM, 그리고 맞춤형 급여 계산 시스템이 혼재되어 운영되고 있어, 필드 매핑이나 워크플로우의 통합이 어려워지고 있습니다. 이 문제는 단순히 기술적인 문제만은 아닙니다. 각 통합 프로젝트에서는 직무 아키텍처, 보상 항목, 현지 규정 준수 규칙에 대해서도 합의를 도출해야 하기 때문입니다. 데이터가 급여 계산, 성과 평가, 인재 관리 등 각 시스템에 분산된 상태로는 인재 분석 결과가 실무상의 인력 배치 의사 결정에 활용되기까지 너무 오랜 시간이 걸리게 됩니다. 각 벤더사는 보다 개방적인 데이터 레이어와 기성 커넥터를 제공함으로써 이에 대응하고 있지만, 레거시 시스템이 주류를 이루는 IT 및 통신 분야 인재 관리 분야에서는 여전히 가치를 실현하기까지의 기간이 길어지고 있습니다.

부문별 분석

2025년, IT 및 통신 분야 인재 관리 시장 중 소프트웨어가 68.26%를 차지했으며, 플랫폼 부문이 구매자의 지출에서 여전히 중심을 차지했습니다. 이러한 우위가 유지된 이유는 고용주가 채용, 분석, 규정 준수, 워크플로우 자동화를 개별 도구로 분산시키지 않고, 단일 상용 계약 하에 통합하고자 했기 때문입니다. IT 및 통신 분야 인재 관리 시장에서 소프트웨어는 SaaS를 통한 제공 방식의 이점도 누리고 있습니다. 이는 공급업체가 고객 측의 하드웨어를 변경하지 않고도 새로운 AI 기능을 출시할 수 있기 때문입니다. 이로 인해 IT 및 통신 분야 인재 관리에서 소프트웨어가 계속해서 중심적인 위치를 차지하고 있으며, 특히 기능의 충실도와 마찬가지로 표준화가 중요시되는 주요 고객사에서 이러한 경향이 두드러집니다.

AI가 주도하는 인사 환경에서 도입, 변경 관리, 지원 업무가 점점 더 어려워짐에 따라, 서비스 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 14.36%로 성장할 것으로 전망됩니다. 새로운 역량 프레임워크나 사내 인사 이동 관리 시스템은 모두 현지 프로세스나 기존 데이터에 맞추어 설정해야 하기 때문에 이에 대한 서비스 수요가 증가하고 있습니다. 정기적인 릴리스 주기 또한 이러한 수요를 더욱 부추기고 있으며, Cornerstone이나 Workday와 같은 벤더들은 사용자 정의 워크플로우에 영향을 미칠 수 있는 잦은 업데이트를 지속적으로 제공합니다. 즉, IT 및 통신 분야 인재 관리는 통합 전문가나 매니지드 서비스 파트너에게 지속적인 업무를 창출해 주고 있는 것입니다.

2025년 기준으로 IT 및 통신 분야 인재 관리 시장 규모 중 클라우드가 74.24%의 점유율을 차지했으며, 2031년까지 연평균 성장률(CAGR) 14.21%를 나타낼 것으로 예측됩니다. IT 및 통신 분야 인재 관리 시장에서 분산된 엔지니어링 팀이 지역이나 부서를 넘나들며 실시간 데이터 접근을 필요로 하기 때문에 클라우드는 여전히 선호되는 모델로 자리 잡고 있습니다. 또한, 클라우드 도입을 통해 AI의 신속한 배포, 규정 준수 업데이트의 용이화, 그리고 기업이 새로운 사업 부문이나 계약 업체를 추가할 때 발생하는 마찰을 줄일 수 있습니다. SAP와 Workday는 모두 2026년에 클라우드 기반 데이터 공유 및 계획 수립 기능을 확대하고 있으며, 이는 ‘커넥티드 워크포스’ 아키텍처로의 전환을 뒷받침하고 있습니다.

직원 데이터를 국경 내에 보관해야 하거나, 엄격하게 관리되는 운영 환경 내에서만 유지해야 하는 경우에는 On-Premise형 시스템이 여전히 중요하게 여겨지고 있습니다. 따라서, 국내 데이터 규제가 적용되는 걸프 연안 국가 시장에서는 클라우드 도입으로 인해 로컬 호스팅이 완전히 대체되지는 않을 것입니다. 그럼에도 불구하고, IT 및 통신 분야 인재 관리 시장의 지출 추세는 계획, 채용, 역량 관련 데이터를 단일 환경에서 통합할 수 있는 클라우드 플랫폼을 지속적으로 선호하고 있습니다. 분석의 심도를 저해하지 않으면서 지역별 호스팅을 지원할 수 있는 벤더는 다음 주기에서 가장 견고한 입지를 다질 가능성이 높을 것입니다.

지역별 분석

2025년, 북미는 IT 및 통신 분야 인재 관리 시장 점유율의 42.36%를 차지하며, 이 지역은 계속해서 1위를 유지했습니다. 이 지역은 하이퍼스케일러의 집중, 성숙한 HR 테크 생태계, 그리고 AI를 활용한 인재 관리 도구의 기업 도입이 급속히 진행되고 있다는 장점을 가지고 있습니다. 미국에서는 캘리포니아주의 AI 도입 관련 규제와 일리노이주에서 고용 과정에서 차별적인 AI 사용에 대한 민권상 책임이 구매자들을 감사 가능하고 거버넌스 조치가 완료된 플랫폼으로 이끌고 있습니다. 또한, 포춘 500대 기업의 65% 이상이 Workday를 도입하고 있다는 이 회사의 위상 덕분에, 북미의 도입 기업들은 대규모 플랫폼 구축 및 생태계를 통한 지원을 가장 먼저 활용할 수 있게 되었습니다. 이러한 요인들이 복합적으로 작용하여, 대기업 수요와 규정 준수를 중시하는 제품 개발이라는 두 가지 측면에서 IT 및 통신 분야 인재 관리 시장은 북미에서 가장 견조한 상태를 유지하고 있습니다.

유럽은 엄격한 데이터 거버넌스와 대규모 통신 및 IT 서비스 인프라에 힘입어, IT 및 통신 분야 인재 관리 시장에서 여전히 주요 수익원으로 자리 잡고 있습니다. GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정)에 따라, 구매 기업은 각국에 흩어져 있는 도구를 개별적으로 관리하는 대신, 분산된 인사 데이터를 감사 가능한 플랫폼으로 통합하도록 권장받고 있습니다. 20만 명의 직원을 두고 있으며, 국내 인사 기술상을 수상한 도이치 텔레콤의 ‘성장 허브’는 이 지역에서 사내 이동 및 역량 관리 플랫폼이 시범 운영 단계를 벗어났음을 보여줍니다. 2026년 8월로 다가온 EU AI법 준수 기한에 따라, 거버넌스, 문서화, AI 관리 기준이 더욱 명확한 시스템으로의 도입이 가속화되고 있습니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 14.95%를 나타낼 것으로 예측되며, IT 및 통신 분야 인재 관리 부문에서 가장 빠르게 성장하는 지역 블록이 될 전망입니다. 이러한 성장의 요인은 디지털 인프라의 확대, 젊은 층의 노동력, 그리고 인도, 베트남, 인도네시아, 필리핀에서 제2급(Tier-2) 기술 허브의 부상에 있습니다. 이러한 지역에서는 보다 체계적인 인재 관리 프로세스가 요구되고 있습니다. 인도의 통신 부문 기술 위원회(Telecom Sector Skill Council)는 연간 15만 명의 훈련을 이수한 통신 종사자의 취업을 목표로 하고 있으며, 에릭슨의 교육 파트너십은 100개 교육 기관에 이르고 있습니다. 이는 현재 진행 중인 노동력 개발의 규모를 여실히 보여주고 있습니다. 남미에서는 여전히 가격에 대한 민감도가 높아, 중소규모 IT 기업에서 분석 기능이 풍부한 소프트웨어 제품군의 도입이 제한되고 있습니다. 한편, 걸프 연안 국가들에서는 각국의 고용 의무와 현지 데이터 규제를 충족하기 위해 정부 규제를 준수하는 플랫폼에 대한 투자가 진행되고 있습니다. 그 결과, IT 및 통신 분야 인재 관리는 아시아태평양에서는 급속한 구조적 성장이 예상되는 반면, 중동 및 아프리카에서는 규정 준수를 중심으로 한 선택적 수요가 나타나고, 남미 지역에서는 보다 완만한 도입 곡선을 보일 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the talent management in IT and telecom market size was valued at USD 3.31 billion in 2025 and estimated to grow from USD 3.75 billion in 2026 to reach USD 6.98 billion by 2031, at a CAGR of 13.23% during the forecast period (2026-2031).

This report is Segmented by Component (Software, and Services), Deployment Mode (On-Premise, and Cloud), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Engagement and Career Development, Learning and Development, Succession Planning, Recruitment and Talent Acquisition, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Talent Management In IT And Telecom Market Trends and Insights

Accelerated Adoption Of AI-Powered Recruiter Bots For Tech Roles

Autonomous recruiting is becoming a defining operating model in the talent management in IT and telecom market, because employers need to screen technical talent faster and with less recruiter effort. Product launches from Oracle and Eightfold AI show that vendors now position agentic interviewing and automated hiring actions as core functions rather than optional add-ons. In telecom hiring, this matters most for field engineering, cloud, and cybersecurity roles, where delays can slow service delivery and infrastructure programs. In the talent management in IT and telecom market, the advantage is shifting toward platforms that connect sourcing, interviewing, and skills data with the wider workforce stack. Vendors that still rely on disconnected recruiter tools face a higher risk of being bypassed as autonomous agents take over larger parts of the hiring flow.

Cloud Migration Wave Boosting SaaS Talent Suites

Cloud migration is strengthening talent management in the IT and telecom markets because buyers want a single workforce system that can keep pace with changing headcounts and project mixes. SAP's SuccessFactors 1H 2026 release added bi-directional, zero-copy data sharing with AWS and linked planning across SAP Cloud ERP, SAP Fieldglass, and SAP SuccessFactors, reflecting this push toward a connected cloud architecture. Workday's spring 2026 release also introduced Workday Data Lake using open standards for bi-directional access with platforms such as Databricks, Google Cloud, and Snowflake. These moves matter in IT and telecom, because workforce, finance, and delivery planning need to stay aligned when hiring or redeployment changes quickly. That makes cloud architecture not just a hosting choice but also a retention and operating lever within talent management in the IT and telecom markets.

Integration Complexity With Legacy HRIS Stacks

Integration complexity remains the clearest near-term brake on the talent management in IT and telecom market, especially for large operators with multi-country HR estates. Many telecom groups still run a mix of PeopleSoft, SAP HCM on-premises, and custom payroll engines built through years of mergers, which makes field mapping and workflow harmonization difficult. The problem is not only technical, because each integration project also forces agreement on job architecture, compensation fields, and local compliance rules. When data stays split across payroll, performance, and headcount systems, workforce analytics arrive too late to guide live staffing decisions. Vendors are responding with more open data layers and prebuilt connectors, but the talent management in IT and telecom market still sees longer time-to-value where legacy stacks dominate.

Other drivers and restraints analyzed in the detailed report include:

- Remote and Hybrid Work Models Scaling Digital Performance Management

- Compliance-Driven Demand For Unified HR Data Security Controls

- High Subscription Cost Of Analytics-Rich Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 68.26% of the talent management market in the IT and telecom market in 2025, keeping the platform layer at the center of buyer spending. That lead persisted because employers wanted to bring recruiting, analytics, compliance, and workflow automation under one commercial relationship rather than across separate tools. In the talent management market for IT and telecom, software also benefits from SaaS delivery, as vendors can release new AI capabilities without customer-side hardware changes. That keeps software central to talent management in the IT and telecom markets, especially in large accounts where standardization matters as much as feature depth.

Services are projected to grow at a 14.36% CAGR from 2026 to 2031, as implementation, change management, and support work become harder in AI-led HR environments. The need for services is rising because every new skills framework or internal mobility layer has to be configured around local processes and legacy data. Regular release cycles add to this demand, with vendors like Cornerstone and Workday continuing to ship frequent updates that can affect custom workflows. That means talent management in the IT and telecom markets continues to create recurring work for integration specialists and managed service partners.

Cloud held 74.24% share of the talent management in IT and telecom market size in 2025 and is projected to grow at 14.21% CAGR through 2031. In the talent management in IT and telecom market, cloud remains the preferred model because distributed engineering teams need live data access across regions and functions. Cloud deployment also supports faster AI rollout, easier compliance updates, and lower friction when companies add new business units or contractors. SAP and Workday both expanded cloud data-sharing and planning capabilities in 2026, which supports this shift toward connected workforce architectures.

On-premises systems still matter where workforce data must stay inside national boundaries or within tightly controlled operator environments. That is why cloud adoption does not fully displace local hosting in Gulf markets governed by in-country data rules. Even so, the direction of spend in the talent management in IT and telecom market continues to favor cloud platforms that can combine planning, hiring, and skills data in one environment. Vendors that can support regional hosting without losing analytical depth are likely to hold the strongest position over the next cycle.

Geography Analysis

North America captured 42.36% of the talent management in IT and telecom market share in 2025, which kept the region in the lead. The region benefits from the concentration of hyperscalers, a mature HR-tech ecosystem, and faster enterprise adoption of AI-enabled workforce tools. In the United States, California's AI hiring rules and Illinois civil rights liability for discriminatory AI use in employment are pushing buyers toward auditable and governance-ready platforms. Workday's position with more than 65% of the Fortune 500 also gives North American buyers early access to scaled platform rollouts and ecosystem support. That combination keeps the talent management in IT and telecom market strongest in North America for both large-enterprise demand and compliance-led product development.

Europe remains a major revenue center in the talent management in IT and telecom market, supported by strict data governance and a large telecom and IT services base. GDPR has encouraged buyers to consolidate fragmented HR data into auditable platforms instead of managing scattered tools across countries. Deutsche Telekom's growth hub, which serves 200,000 employees and won a national HR Tech award, shows that internal mobility and skills platforms have moved beyond pilot status in the region. The EU AI Act compliance deadline in August 2026 is now accelerating procurement toward systems with clearer governance, documentation, and AI management standards.

Asia-Pacific is forecast to grow at 14.95% CAGR from 2026 to 2031, making it the fastest-growing regional block in the talent management in IT and telecom market. Growth comes from expanding digital infrastructure, younger labor pools, and the rise of Tier-2 tech hubs in India, Vietnam, Indonesia, and the Philippines that need more formal talent processes. India's Telecom Sector Skill Council is targeting placement of 150,000 trained telecom workers annually, while Ericsson's training partnership spans 100 institutes, which shows the scale of workforce development now underway. South America remains more price sensitive, which limits adoption of analytics-rich suites among smaller IT employers, while Gulf markets are investing in sovereign-compliant platforms to meet national employment mandates and local data rules. This leaves the talent management in IT and telecom market with fast structural upside in Asia-Pacific, selective compliance-led demand in the Middle East and Africa, and a more measured adoption curve in South America.

- SAP SE

- Oracle Corporation

- Workday, Inc.

- Microsoft Corporation

- IBM Corporation

- ADP, Inc.

- Ceridian HCM Holding Inc.

- UKG Inc.

- Cornerstone OnDemand Inc.

- ServiceNow Inc.

- Zoho Corporation

- BambooHR LLC

- PeopleFluent (LTG plc)

- Infor, Inc.

- iCIMS, Inc.

- Eightfold AI Inc.

- SumTotal Systems, LLC

- Amdocs Limited

- Tata Consultancy Services Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Adoption of AI-Powered Recruiter Bots for Tech Roles

- 4.2.2 Cloud Migration Wave Boosting Saas Talent Suites

- 4.2.3 Remote and Hybrid Work Models Scaling Digital Performance Management

- 4.2.4 Compliance-driven Demand for Unified HR Data Security Controls

- 4.2.5 Skills Taxonomies Linked To 5G and Network Virtualization Roadmaps

- 4.2.6 Growth of Internal Talent Marketplaces in Tier-2 Asian Tech Hubs

- 4.3 Market Restraints

- 4.3.1 Integration Complexity With Legacy HRIS Stacks

- 4.3.2 High Subscription Cost of Analytics-rich Platforms

- 4.3.3 Talent-data Sovereignty Rules in the Middle East and Africa

- 4.3.4 Algorithmic Bias Concerns Slowing AI Recruitment Tools

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Support and Maintenance Services

- 5.2 By Deployment Mode

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.3 By End-Use Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By Application

- 5.4.1 Performance Management

- 5.4.2 Learning and Development

- 5.4.3 Succession Planning

- 5.4.4 Compensation Management

- 5.4.5 Recruitment and Talent Acquisition

- 5.4.6 Workforce Planning

- 5.4.7 Employee Engagement and Career Development

- 5.4.8 Other Talent Management Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Workday, Inc.

- 6.4.4 Microsoft Corporation

- 6.4.5 IBM Corporation

- 6.4.6 ADP, Inc.

- 6.4.7 Ceridian HCM Holding Inc.

- 6.4.8 UKG Inc.

- 6.4.9 Cornerstone OnDemand Inc.

- 6.4.10 ServiceNow Inc.

- 6.4.11 Zoho Corporation

- 6.4.12 BambooHR LLC

- 6.4.13 PeopleFluent (LTG plc)

- 6.4.14 Infor, Inc.

- 6.4.15 iCIMS, Inc.

- 6.4.16 Eightfold AI Inc.

- 6.4.17 SumTotal Systems, LLC

- 6.4.18 Amdocs Limited

- 6.4.19 Tata Consultancy Services Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment