|

시장보고서

상품코드

2065530

학습 경험 플랫폼(LXP) : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Learning Experience Platform (LXP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

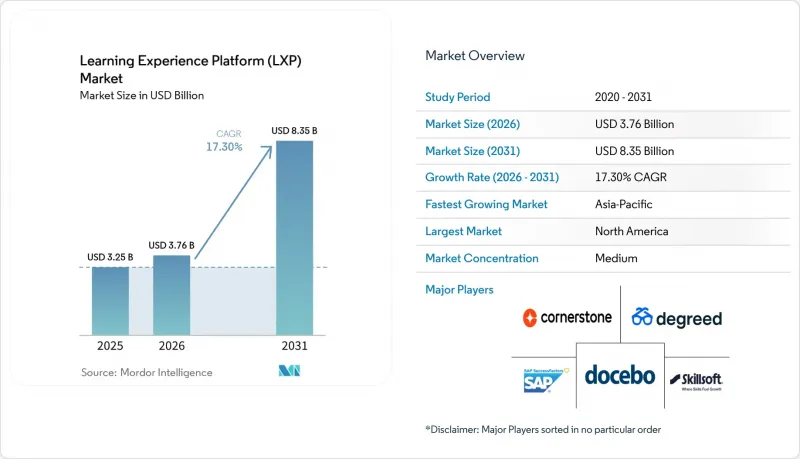

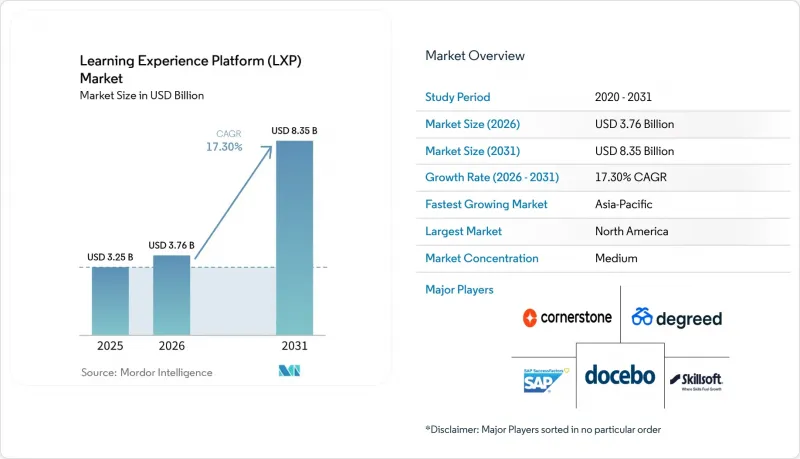

Mordor Intelligence에 의하면, 학습 경험 플랫폼(LXP) 시장 규모는 2025년 32억 5,000만 달러로 평가되었습니다. 2026년에는 37억 6,000만 달러로 확대되어 2031년까지 83억 5,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 17.30%로 성장할 전망입니다.

본 보고서는 구성 요소(플랫폼(학습 컨텐츠 통합 플랫폼 등), 서비스), 배포 방식(클라우드 기반, On-Premise형, 하이브리드형), 기업 규모(대기업, 중소기업), 최종 사용자 산업(기업, 교육 기관, 정부·비영리 단체 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 학습 경험 플랫폼(LXP) 시장 동향 및 인사이트

원격·하이브리드형 인재 육성으로의 급속한 전환

학습 경험 플랫폼(LXP) 시장은 하이브리드 근무 방식이 정착됨에 따라 계속해서 혜택을 보고 있습니다. 이는 조직이 현재 완전 원격 근무, 하이브리드 근무, 그리고 현장 근무 직원을 동시에 교육하고 있기 때문입니다. 2025년에는 원격 근무가 가능한 미국 근로자의 대다수가 하이브리드 형태로 근무하고 있으며, 이는 유연성이 일시적인 것이 아니라 구조적인 것이 되었음을 보여줍니다. 이러한 환경 속에서 학습 경험 플랫폼의 도입이 가속화되고 있습니다. 비동기형 컨텐츠, 모바일 접속, AI를 활용한 학습 경로 제안, 일관된 사용자 경험을 통해 조직은 서로 다른 근무 환경에서도 동등한 학습 성과를 제공할 수 있게 되기 때문입니다. 또한, 이러한 변화에 따라 학습자의 자율성에 대한 기대도 높아지고 있습니다. 근무 방식을 스스로 선택하는 직원들은 학습 방법이나 시기에 대해서도 마찬가지로 자율성을 추구하는 경향이 강해지고 있기 때문입니다. 유연한 플랫폼 아키텍처를 기반으로 하면서도 획일적인 학습 순서를 강요하는 기업의 경우, 도입 초기 단계에서 참여도가 떨어지는 경향이 나타납니다. 따라서 플랫폼 설계와 컨텐츠 전략은 둘 다 똑같이 중요합니다.

AI를 활용한 맞춤형 학습 경로의 필요성

학습 경험 플랫폼(LXP) 시장은 단순한 컨텐츠 추천에서 AI를 활용한 역량 격차 해소로 전환되는 추세에 힘입어 성장하고 있습니다. Docebo는 2026년 ‘AI 준비도 격차 보고서’에서 AI 도입 및 활용 능력이 기업 교육 담당 리더에게 가장 큰 과제로 대두되고 있는 반면, 많은 조직에서는 여전히 역할의 변화에 대응하지 못하는 정적인 학습 모델을 사용하고 있다고 지적했습니다. 따라서 개인화의 질이 구매의 주요 판단 기준이 되고 있습니다. 왜냐하면 직책이나 부서와 같은 미약한 신호를 바탕으로 구축된 플랫폼은 학습자가 무시해 버릴 만한 추천을 제시하기 쉽기 때문입니다. TalentLMS는 2026년 보고서에서 인사 담당자의 73%가 디지털 역량 강화를 최우선 과제로 꼽고 있다고 밝혔습니다. 이는 일반적인 카탈로그를 제시하는 것이 아니라, 특정 역량을 매핑하고, 추천하며, 검증할 수 있는 시스템에 대한 수요를 뒷받침하는 것입니다. 따라서, 독자적인 스킬 그래프를 풍부하게 보유한 벤더는 학습 경험 플랫폼 시장에서 우위를 점하게 됩니다. 왜냐하면, 시스템에 학습자의 활동 데이터가 축적됨에 따라 추천 내용을 지속적으로 개선할 수 있기 때문입니다.

도입 및 컨텐츠 큐레이션 비용의 고가

첫해 도입 비용이 높다는 점은 특히 대기업의 예산 규모를 초과하는 조직의 경우, 학습 경험 플랫폼 시장에 있어 여전히 실질적인 장벽으로 작용하고 있습니다. 구매자들은 구독료가 총 지출의 일부에 불과하다는 사실을 종종 깨닫게 됩니다. 왜냐하면 도입, 기술 프레임워크 설계, 컨텐츠 라이선싱 및 배포 지원은 플랫폼 기본 요금에 포함되어 있지 않기 때문입니다. 가동을 시작한 후에도 부담은 계속됩니다. 여러 소스로 구성된 학습 환경에서는 오래된 컨텐츠를 삭제하고, 학습 경로의 품질을 유지하며, 변화하는 역할의 요구 사항에 맞추어 라이브러리를 업데이트하기 위해 지속적인 편집 작업이 필요하기 때문입니다. 이러한 압박감은 중소기업, 전담 인력을 상시 큐레이션 업무에 배정할 수 없는 학습 팀 인력이 제한된 조직에서 더욱 크게 느껴집니다. 각 벤더사는 번들로 제공되는 컨텐츠와 AI를 활용한 큐레이션을 통해 일부 과제를 완화하고 있지만, 고품질의 최신 학습 경험을 유지하기 위한 비용 문제가 여전히 광범위한 도입을 가로막고 있습니다.

부문별 분석

2025년에는 플랫폼 솔루션이 매출의 61.26%를 차지했는데, 이는 학습 경험 플랫폼(LXP) 시장에서 기업 구매 담당자들이 여전히 단일 기능 도구보다 통합형 제품군을 선호하고 있음을 보여줍니다. 이 카테고리에서는 AI를 활용한 맞춤형 학습 모듈, 스킬 인텔리전스 계층, 컨텐츠 통합, 그리고 학습 활동과 직원의 성과를 연계할 수 있는 분석 도구에 대한 수요가 주를 이루고 있습니다. 학습 분석 플랫폼이 주목을 받고 있는 이유는 경영진의 구매 담당자들이 단순한 수료 현황 대시보드 이상의 것을 원하며, 역량 향상에 대한 검증 가능한 증거를 점점 더 요구하고 있기 때문입니다. 또한, 컨텐츠 통합 플랫폼은 기존의 컨텐츠 관계를 완전히 대체하도록 강요하지 않으면서도 기업이 학습 경험 플랫폼 시장에 진출할 수 있는 현실적인 수단을 제공하기 때문에 여전히 중요한 위치를 차지하고 있습니다.

서비스 분야는 2031년까지 연평균 성장률(CAGR) 18.37%를 나타낼 것으로 예측되며, 시장에서 가장 빠르게 확대되고 있는 분야입니다. 이러한 경향은 구매자의 우선순위가 단순한 소프트웨어 도입에서 활용, 거버넌스, 그리고 측정 가능한 도입 현황으로 이동하고 있음을 반영합니다. 아데코 그룹은 2026년 보고서에서 직원의 역량을 파악하기 위한 데이터 인사이트에 적극적으로 투자하고 있는 기업이 고작 33%에 불과하다고 지적했으며, 이는 도입 지원 및 역량 아키텍처 서비스에 대한 수요가 크다는 것을 시사합니다. 실제로 이는 스킬 프레임워크, 매니지드 애널리틱스, 러닝 오퍼레이션에 관한 컨설팅이 일회성 구축 업무가 아니라 지속적인 수익원이 되고 있음을 의미합니다. 그 결과, LXP 시장에서는 제품의 기능과 운영 지원을 결합하여, 비즈니스 리더가 플랫폼을 쉽게 활용하고 상황을 파악할 수 있도록 하는 벤더들이 높은 평가를 받고 있습니다.

2025년에는 클라우드 기반 도입이 매출의 76.24%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 21.49%를 유지하며 주요하고 가장 빠르게 성장하는 모델로 자리매김했습니다. 학습 경험 플랫폼 시장의 이 분야는 클라우드 네이티브 시스템이 On-Premise 환경보다 더 신속하게 AI 모델 업데이트, 커넥터 출시, 스킬 그래프 개선을 반영할 수 있기 때문에 지속적인 배포의 이점을 누리고 있습니다. 이러한 속도가 중요한 이유는 추론의 품질이 최신 데이터, 빈번한 모델 업데이트, 그리고 다른 엔터프라이즈 시스템과의 폭넓은 상호 운용성에 달려 있기 때문입니다. 아시아태평양과 남미의 성장 시장도 ‘클라우드 우선’ 아키텍처로 직접 전환하고 있으며, 이로 인해 학습 경험 플랫폼(LXP) 시장에서 클라우드의 장기적인 우위가 더욱 공고해지고 있습니다.

On-Premise 배포는 주권 관련 규제나 격리된 네트워크로 인해 직원의 학습 기록을 클라우드에 저장하는 것이 제한되는 환경에서는 여전히 일정한 위치를 차지하고 있습니다. 방위 관련 기업, 기밀을 다루는 정부 기관 및 특정 산업 분야에서는 규정 준수상의 제약이 풀 클라우드 서비스가 제공하는 유연성의 이점을 상쇄하기 때문에 이 모델이 여전히 선호되고 있습니다. 따라서 하이브리드 방식이 현실적인 중간 방안으로 부상하고 있습니다. 특히 유럽의 금융 서비스 업계에서는 기밀 데이터를 로컬 인프라에 보관하면서, 클라우드 모듈을 통해 개인 맞춤화 및 고도화된 분석을 처리할 수 있습니다. 이러한 혼합 아키텍처 덕분에 LXP 시장은 AI 기능이나 보안 요건을 전면적으로 타협하지 않으면서도, 엄격한 규제가 적용되는 분야에서도 확대될 수 있게 됩니다.

지역별 분석

2025년, 북미는 매출의 42.36%를 차지하며 학습 경험 플랫폼(LXP) 시장에서 가장 큰 점유율을 기록했습니다. 미국은 대기업이 밀집해 있는 기반, 성숙한 HRIS 생태계, 그리고 성과를 추적할 수 있는 인재 개발에 대한 높은 투자 의지를 모두 갖추고 있어 여전히 주요 견인차 역할을 하고 있습니다. 캐나다에서도 금융 서비스 및 정부 기관에서 수요가 높은 것으로 나타납니다. 이러한 분야에서는 클라우드 보안 인증이 공급업체 선정에 있어 점점 더 중요한 요소로 대두되고 있습니다. 멕시코에서는 다국적 제조 기업과 기술 서비스 기업들이 더욱 복잡해지는 국경을 초월한 사업 운영을 위해 확장성이 뛰어난 스페인어 교육 인프라에 투자하고 있어, 시장이 급속히 성장하고 있습니다. 남미에서는 도입이 아직 초기 단계에 있지만, 브라질과 아르헨티나에서는 학습 경험 플랫폼 시장에서 모바일 우선이며 다국어를 지원하는 클라우드 도입에 대한 꾸준한 수요가 발생하고 있습니다.

유럽은 학습 경험 플랫폼 시장에서 높은 부가가치를 지닌 반면, 규정 준수 요건이 까다로운 지역입니다. 독일과 영국은 여전히 최대의 국내 시장이며, 독일 수요는 제조업의 디지털화와 직업 훈련 및 견습 제도와 관련된 인력의 재교육 수요에 힘입어 유지되고 있습니다. 프랑스에서는 직업 훈련 시장 규모가 320억 유로를 넘어섰습니다. 이는 2025년의 평균 유로/달러 환율 1.10을 적용하면 352억 달러에 해당합니다. 또한, Qualiopi의 요건에 따라 벤더 선정 시 컨텐츠 거버넌스 및 감사 추적 기능이 더욱 중요시되고 있습니다. Unow는 2026년 3월, 500명 이상의 인사 및 교육 담당자를 대상으로 실시한 설문조사 결과를 통해 학습 형태의 균형이 점차 안정화되고 있다고 보고했습니다. 이는 원격 학습만을 통한 성장에서 의도적인 혼합형 학습의 최적화로 전환되고 있음을 시사합니다. 스페인과 이탈리아에서는 중견 시장에서 비즈니스 기회가 확대되고 있는 반면, 제재와 관련된 제약으로 인해 러시아의 역할은 계속해서 축소되고 있으며, 지역 내 비중은 DACH 지역, 프랑스, 영국으로 이동하고 있습니다. 사우디아라비아와 아랍에미리트(UAE)가 주도하는 중동에서는 국가 차원의 기술 향상 계획이 급속히 진전되고 있는 반면, 아프리카는 여전히 초기 단계에 머물러 있으며, 수요는 남아프리카공화국의 금융 서비스 업계와 나이지리아의 확대되는 기술 인력에 집중되어 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 18.11%를 기록하며 성장할 것으로 예상되며, LXP 시장에서 가장 빠르게 성장하는 지역이 될 것입니다. 인도는 여전히 심각한 기술 인력 부족 문제에 더해, 응용 AI 역량, 안전 수칙, 규정 준수 관련 교육에 대한 기업 수요가 지속적으로 증가하고 있다는 점에서 두드러집니다. Workera는 2026년 보고서에서 AI 에이전트를 이해하고 활용하기 위해 필요한 핵심 역량을 갖춘 기업 직원이 고작 13%에 불과하다고 지적했으며, 이는 현재의 역량 수준이 얼마나 제한적인지를 보여줍니다. 중국의 도입 경로는 노동력 정책과 데이터 현지화 규제에 의해 형성되어 있으며, 이러한 정책들은 국내 AI 학습 제공업체를 우대하고 국제 플랫폼의 확장을 제한하고 있습니다. 일본, 호주, 뉴질랜드는 여전히 성숙한 중규모 시장으로, 사용자 1인당 구매력이 높고 인재 계획에 대한 관심도 높기 때문에 스킬 인텔리전스 기능에 대한 수요가 지속되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the learning experience platform (LXP) market size is expected to increase from USD 3.25 billion in 2025 to USD 3.76 billion in 2026 and reach USD 8.35 billion by 2031, growing at a CAGR of 17.30% over 2026-2031.

This report is Segmented by Component (Platform [Learning Content Aggregation Platform, and More], and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Corporate, Academic, Government and Non-Profit, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Learning Experience Platform (LXP) Market Trends and Insights

Rapid Shift to Remote and Hybrid Workforce Learning

The learning experience platform (LXP) market continues to benefit from the normalization of hybrid work because organizations now train fully remote, hybrid, and on-site employees at the same time. In 2025, most remote-capable US workers were operating in hybrid arrangements, indicating that flexibility had become structural rather than temporary. In this environment, learning experience platform deployments are gaining traction because asynchronous content, mobile access, AI-curated pathways, and consistent user experience help organizations deliver the same learning outcome across different work settings. This shift also raises expectations around learner control, since employees who choose how they work increasingly expect similar control over how and when they learn. Companies that place rigid learning sequences on top of flexible platform architecture often see weaker engagement early in rollout, which makes platform design and content strategy equally important.

Need For AI-Driven Personalized Learning Paths

The learning experience platform (LXP) market is also being driven forward by the shift from simple content recommendations to AI-driven skill-gap closure. Docebo stated in its 2026 AI Readiness Gap Report that AI adoption and fluency had become the main pressure point for enterprise learning leaders, while many organizations were still using static learning models that could not keep pace with role change. That makes personalization quality a central buying criterion, because platforms built on weak signals, such as job title or department, often produce recommendations that learners ignore. TalentLMS reported in 2026 that 73% of HR managers saw expanded digital skills as their main priority, which supports demand for systems that can map, recommend, and validate specific capabilities rather than present generic catalogs. Vendors with greater proprietary skills graphs therefore hold an advantage in the learning experience platform market because they can keep improving recommendations as more learner activity enters the system.

High Implementation And Content-Curation Costs

High first-year activation costs remain a real barrier for the learning experience platform market, especially outside large-enterprise budgets. Buyers often find that subscription pricing is only one part of the total outlay because implementation, skills-framework design, content licensing, and rollout support sit outside the core platform fee. The burden continues after go-live because multi-source learning environments require ongoing editorial work to retire outdated content, maintain pathway quality, and keep libraries aligned with changing role needs. That pressure is felt more sharply by SMEs and by organizations with lean learning teams that cannot dedicate staff to full-time curation. Vendors are reducing some friction with bundled content and AI-assisted curation, but the economics of maintaining high-quality, current learning experiences still slow broader adoption.

Other drivers and restraints analyzed in the detailed report include:

- Upskilling For Enterprise Digital-Transformation Goals

- Integrations With HRIS and Productivity Suites

- Data-Privacy and Security Concerns in Regulated Sectors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform solutions held 61.26% of revenue in 2025, which shows that enterprise buyers still favor integrated suites over point tools in the learning experience platform (LXP) market. Within this category, demand has centered on AI-driven personalized learning modules, skills intelligence layers, content aggregation, and analytics tools that can connect learning activity to workforce performance. Learning analytics platforms have gained traction because executive buyers want more than completion dashboards and increasingly ask for auditable evidence of capability improvement. Content aggregation platforms also remain relevant because they give enterprises a practical route into the learning experience platform market without forcing a full replacement of existing content relationships.

Services are projected to grow at an 18.37% CAGR through 2031, which makes them the fastest-expanding component in the market. That pattern reflects a shift in buyer priorities from software deployment alone toward activation, governance, and measurable adoption. The Adecco Group reported in 2026 that only 33% of companies were actively investing in data insights to understand workforce skills capabilities, which points to a large need for implementation support and skills architecture services. In practice, this means consulting around skills frameworks, managed analytics, and learning operations has become a recurring revenue stream rather than a one-time setup function. As a result, the LXP market is rewarding vendors that can combine product capability with operational support that makes the platform usable and visible to business leaders.

Cloud-based deployment accounted for 76.24% of revenue in 2025 and remained both the leading and the fastest-growing model, with a 21.49% CAGR through 2031. This part of the learning experience platform market benefits from continuous delivery because cloud-native systems can push AI-model updates, connector releases, and skills-graph improvements faster than on-premises installations. That speed matters because inference quality depends on current data, frequent model refresh, and broad interoperability with other enterprise systems. Growth markets in Asia-Pacific and South America are also moving directly to cloud-first architectures, which strengthens the long-term lead of cloud in the learning experience platform (LXP) market.

On-premises deployment still holds a place in environments where sovereignty rules or isolated networks limit cloud storage of employee learning records. Defense contractors, classified government entities, and certain industrial operations continue to favor this model because compliance limits outweigh the flexibility benefits of full cloud delivery. Hybrid deployment is therefore emerging as a practical middle path, especially in European financial services where sensitive data can stay on local infrastructure while cloud modules handle personalization and advanced analytics. This blended architecture allows the LXP market to expand in tightly governed sectors without forcing a full compromise on AI capability or security requirements.

Geography Analysis

North America held 42.36% of revenue in 2025, which gave the region the largest share of the learning experience platform (LXP) market. The United States remains the main anchor because it combines a dense base of large enterprises, mature HRIS ecosystems, and high willingness to spend on trackable workforce development. Canada also shows strong demand in financial services and government, where cloud security certifications increasingly shape vendor selection. Mexico is emerging faster as multinational manufacturers and technology-services firms invest in scalable Spanish-language training infrastructure for more complex cross-border operations. South America remains earlier in adoption, but Brazil and Argentina are creating steady demand for mobile-first and multi-language cloud deployments within the learning experience platform market.

Europe represents a high-value but compliance-heavy part of the learning experience platform market. Germany and the United Kingdom remain the largest national markets, with German demand supported by manufacturing digitization and workforce reskilling needs tied to vocational and apprenticeship pathways. In France, the professional training market exceeded EUR 32 billion, which equals USD 35.2 billion at the 2025 average EUR/USD rate of 1.10, and Qualiopi requirements have made content governance and audit-trail capability more important in vendor screening. Unow reported in 2026 that a March survey of more than 500 HR and training professionals showed learning modality balance was stabilizing, which indicates a shift from remote-only growth toward deliberate blended optimization. Spain and Italy are building mid-market opportunity, while sanctions-related constraints continue to reduce Russia's role and shift regional weight toward the DACH cluster, France, and the United Kingdom. The Middle East, led by Saudi Arabia and the UAE, is advancing quickly on national upskilling agendas, while Africa remains earlier stage with demand centered on South Africa's financial services base and Nigeria's expanding technology workforce.

Asia-Pacific is projected to grow at an 18.11% CAGR through 2031, which makes it the fastest-growing regional block in the LXP market. India stands out because skill shortages remain acute and enterprise demand for applied AI capability, safety behavior, and compliance-linked learning continues to rise. Workera reported in 2026 that only 13% of enterprise employees possessed the critical skills needed to understand and work with AI agents, which shows how limited the current skills baseline remains. China's adoption path is shaped by workforce policy and data-localization rules, which favor domestic AI-learning providers and limit the reach of international platforms. Japan, Australia, and New Zealand remain mature mid-sized markets where high per-seat purchasing power and strong interest in workforce planning support ongoing demand for skills-intelligence features.

- Cornerstone OnDemand, Inc.

- Docebo Inc.

- SAP SuccessFactors (SAP SE)

- Skillsoft Corporation (SumTotal)

- Degreed, Inc.

- Valamis Group Oy

- Fuse Universal Ltd.

- Absorb Software Inc.

- Learn Amp Ltd.

- Schoox, Inc.

- D2L Corporation (formerly Desire2Learn)

- LinkedIn Corporation

- Udemy, Inc.

- 360Learning SA

- Thrive Learning Ltd.

- Learning Pool Ltd.

- Litmos

- Axonify Inc.

- Emerald Works Limited (Mind Tools)

- Mind Tools (Emerald Works)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Shift to Remote and Hybrid Workforce Learning

- 4.2.2 Need For Ai-driven Personalized Learning Paths

- 4.2.3 Integrations With HRIS and Productivity Suites

- 4.2.4 Upskilling For Enterprise Digital-Transformation Goals

- 4.2.5 Skills-ontology Linkage to Talent Marketplaces

- 4.2.6 Xapi-enabled LRS Analytics Proving ROI

- 4.3 Market Restraints

- 4.3.1 High Implementation and Content-Curation Costs

- 4.3.2 Data-Privacy/Security Concerns in Regulated Sectors

- 4.3.3 Proprietary Skills Taxonomies Create Vendor Lock-in

- 4.3.4 Legacy-LMS Integration Drains IT Bandwidth

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform

- 5.1.1.1 Learning Experience Platforms

- 5.1.1.2 AI-driven Personalized Learning Platforms

- 5.1.1.3 Skills Intelligence Platforms

- 5.1.1.4 Learning Content Aggregation Platforms

- 5.1.1.5 Learning Analytics and Engagement Platforms

- 5.1.2 Services

- 5.1.1 Platform

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based LXP

- 5.2.2 On-Premises LXP

- 5.2.3 Hybrid LXP

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-user Industry

- 5.4.1 Corporate

- 5.4.2 Academic (K-12, Higher Ed)

- 5.4.3 Government and Non-profit

- 5.4.4 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cornerstone OnDemand, Inc.

- 6.4.2 Docebo Inc.

- 6.4.3 SAP SuccessFactors (SAP SE)

- 6.4.4 Skillsoft Corporation (SumTotal)

- 6.4.5 Degreed, Inc.

- 6.4.6 Valamis Group Oy

- 6.4.7 Fuse Universal Ltd.

- 6.4.8 Absorb Software Inc.

- 6.4.9 Learn Amp Ltd.

- 6.4.10 Schoox, Inc.

- 6.4.11 D2L Corporation (formerly Desire2Learn)

- 6.4.12 LinkedIn Corporation

- 6.4.13 Udemy, Inc.

- 6.4.14 360Learning SA

- 6.4.15 Thrive Learning Ltd.

- 6.4.16 Learning Pool Ltd.

- 6.4.17 Litmos

- 6.4.18 Axonify Inc.

- 6.4.19 Emerald Works Limited (Mind Tools)

- 6.4.20 Mind Tools (Emerald Works)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment