|

시장보고서

상품코드

2065589

하이브리드 근무 하드웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Hybrid Work Hardware - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

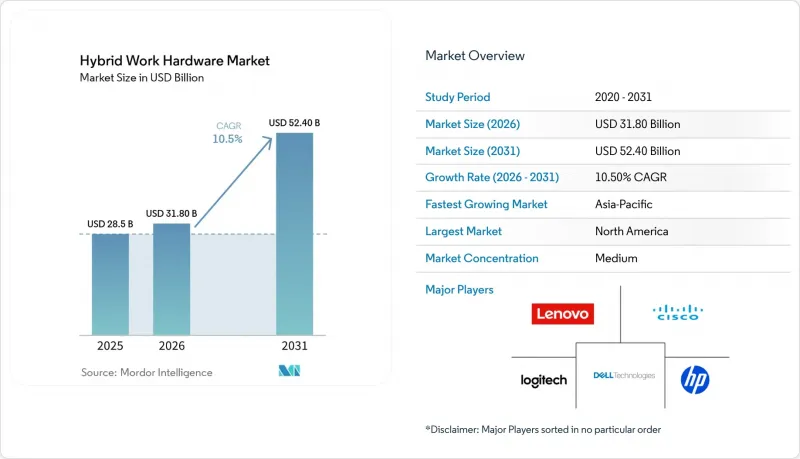

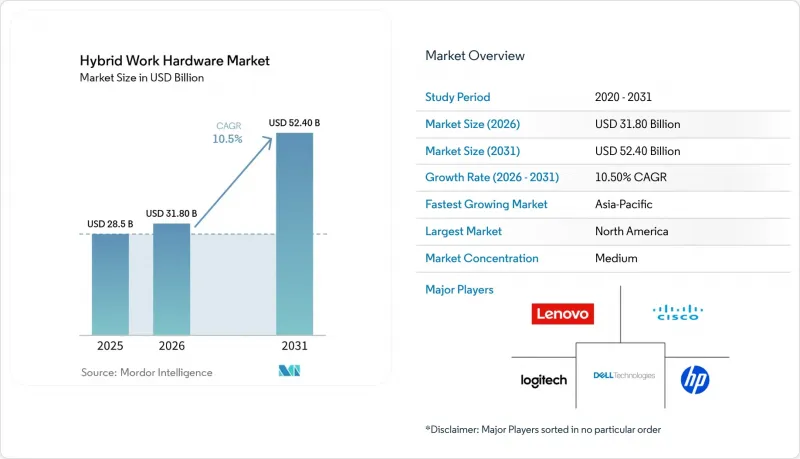

Mordor Intelligence에 의하면, 하이브리드 근무 하드웨어 시장 규모는 2025년 285억 달러에서 2026년에는 318억 달러로 확대되어 2031년까지 524억 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 10.50%로 성장할 전망입니다.

본 보고서는 제품 유형(컴퓨팅 기기, 주변기기 및 액세서리, 협업 하드웨어 등), 조직 규모(대기업, 중소기업), 최종 사용 산업(IT 및 통신, BFSI 등), 유통 채널(오프라인, 온라인) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 하이브리드 근무 하드웨어 시장 동향과 인사이트

‘Bring Your Own Meeting(BYOM)’ 정책의 보급

BYOM(Bring Your Own Meeting) 정책에 따라, 직원들은 별도의 코덱이 필요 없는 USB 스피커폰이나 자동 프레임 조정 카메라에 개인 노트북을 연결할 수 있으므로, 복잡한 IT 프로비저닝 과정을 생략할 수 있고 하드웨어 교체 주기가 단축됩니다. Owl Labs의 보고서에 따르면, 2025년 하이브리드 근무자의 63%가 익숙한 데스크톱 인터페이스를 재현한 BYOM 환경을 선호할 것으로 나타났습니다. 이러한 추세는 기업들이 고정형 장비를 소프트웨어에 의존하지 않는 사운드바로 교체함에 따라, 회의실 시스템 시장에서 예상되는 연평균 성장률(CAGR) 12.8%와도 일치합니다. 삼성, 시스코, 로지텍은 2026년 2월, 이러한 추세에 대응하여 제로 터치 도입을 약속하는 사전 통합형 번들을 발표했습니다. 이는 개방성을 희생하여 관리의 간소화를 도모하는 생태계 전략입니다. 모듈식 BYOM을 도입한 조직은 하드웨어가 라이선스 조건과 분리된 상태를 유지하기 때문에 SaaS 계약 재협상 시 여전히 유리한 입지를 확보할 수 있으며, 2028년부터 2030년까지의 갱신 기간 동안에도 선택의 폭을 유지할 수 있습니다.

팬데믹 이후 화상 회의 도입의 급증

웹캠의 보급률은 2024년까지 정점에 달했지만, 1차 도입된 단말기의 수명이 다하고, 사용자들이 4K 광학 시스템, 신경망 기반 노이즈 억제, 엣지 기반 분석 기능을 요구함에 따라 지출은 계속되고 있습니다. 2026년 1월에 출시된 로지텍의 ‘Rally AI’ 카메라에는 스피커 추적 기능을 로컬에서 실행하는 전용 프로세서가 내장되어 있어, 클라우드와의 왕복 지연 시간을 줄여주는 동시에 의료 및 금융 분야의 데이터 주권 요건을 충족합니다. 대학 강당 개보수 비용은 1실당 8,000-1만 5,000달러로, 교육 분야의 두 자릿수 연평균 성장률(CAGR)을 뒷받침하고 있습니다. 천장에 설치된 어레이 덕분에 시차가 있는 지역의 학생들을 위해 비동기 재생이 가능해집니다. Crestron사의 ‘Collab Compute’와 같은 어플라이언스형 제품은 연산 처리, 터치 조작, 라이선싱을 하나의 SKU에 통합하여 부품 명세서(BOM)의 복잡성을 줄이고 도입을 가속화합니다. CRESTRON.COM.

협업 기기에서 제기되는 사이버 보안 및 데이터 개인정보 보호에 대한 우려

상시 가동 상태인 카메라와 마이크는 악의적인 공격자가 펌웨어에 악성 코드를 심거나 중간자 공격을 통해 악용할 수 있는 공격 대상 영역을 확대시킵니다. AVIXA의 2024년 조사에 따르면, IT 리더의 58%는 공급업체가 ISO 27001 인증을 획득한 제조 공정과 안전한 부트 체인을 입증할 때까지 하드웨어 도입을 연기하고 있었습니다. 현재 기업들은 Trusted Platform Modules(TPM) 및 자동 패치 적용 유틸리티를 사양으로 채택하고 있으며, 엔드포인트 1대당 100-200달러의 추가 비용이 발생하지만, 연간 매출의 4%에 해당하는 GDPR(EU 개인정보보호규정) 위반 벌금을 피할 수 있게 되었습니다. 이러한 추세로 인해 CVE 정보를 공개하고 버그 보상 프로그램에 자금을 지원하는 기존 브랜드들이 유리한 입지를 차지하는 반면, 공급망이 불투명한 화이트박스 시장 신규 진출기업들은 불리한 입장에 놓여 있습니다.

부문별 분석

2025년 하이브리드 근무 하드웨어 시장에서 32.25%의 점유율을 차지하는 컴퓨팅 기기가 시장 규모 1위를 차지하고 있지만, 화상 회의 시스템은 2031년까지 연평균 성장률(CAGR) 12.8%를 기록하며 더욱 급속한 성장이 예상됩니다. 컴퓨팅 엔드포인트의 상품화가 진행되고 있으며, 부품 사양이 균일화됨에 따라 2025년에는 비즈니스용 노트북의 평균 가격이 8% 하락했습니다. 주변 기기가 그 격차를 메우고 있으며, Jabra PanaCast 기기에 내장된 DSP가 클라우드 지연을 줄여주는 사례가 대표적입니다. 한편, Wi-Fi 6E 라우터와 같은 네트워크 및 연결 하드웨어는 멀티스트림 회의에서 대역폭의 대칭성을 보장합니다. 협업 보드나 인터랙티브 화이트보드는 교육 및 의료 분야에서 점차 보급되고 있으며, 터치 조작을 통한 주석 기능을 통해 원격지에 있는 구성원들을 회의실 기반의 업무 흐름에 통합할 수 있게 되었습니다. 인체공학에 기반한 조명 키트 등 부수적인 카테고리의 성장 속도는 완만하지만, 하이브리드 근무를 위한 종합적인 패키지를 완성하는 데 기여하고 있습니다.

예측 기간 동안 기업들은 노트북 교체에 쓰던 자금을 회의실 현대화에 할당할 것으로 보입니다. 이러한 변화는 BYOM(Bring Your Own Meeting)에 의해 가속화되고 있는데, 이는 직원 1인당 여러 대의 노트북을 준비하는 것보다 하나의 스마트바만으로 팀 전체를 지원할 수 있기 때문입니다. 따라서 하이브리드 근무 하드웨어 시장 점유율은 공유 공간 인프라로 재분배될 전망입니다. 특히, Crestron의 ‘Collab Compute’와 같이, 벤더들이 연산, 제어, 연결 기능을 단일 SKU로 통합하는 추세가 확산되고 있기 때문입니다. 통합형 회의실 솔루션은 더 높은 수익률을 가져오기 때문에 벤더는 신경망 가속기를 탑재하기 위한 예산을 확보할 수 있으며, 그 결과 후발 경쟁사들에 대한 기술적 진입 장벽이 효과적으로 높아집니다.

하이브리드 근무 하드웨어 시장 규모는 전 세계적으로 계약, 대량 구매 할인 및 사내 AV 팀을 활용하는 대기업에 집중되어 있으며, 2025년에는 전체 시장의 68.46%를 차지할 것으로 전망됩니다. 한편, 자원이 제한적인 중소기업은 연평균 성장률(CAGR) 12.24%를 기록하며, 2031년까지 그 격차를 서서히 좁혀갈 것으로 예측됩니다. 이러한 변화의 원인은 전문 통합 업체가 필요 없는 USB 기반 바에 있으며, 이를 통해 사무실 관리자가 1시간 이내에 엔드포인트를 설치할 수 있게 되었습니다. 또한, 자금 조달 모델 역시 HP, Dell, Lenovo와의 경쟁 조건을 평등하게 하고 있으며, 이들 기업은 현재 노트북, 모니터, 주변기기를 월정액 구독 방식으로 제공하고 있어 중소기업의 현금 흐름 실정에 부합하고 있습니다.

대기업들은 계속해서 프리미엄 시장을 주도하며, 하드웨어, SaaS 라이선스 및 5년짜리 관리형 서비스 계약의 번들 패키지에 대해 협상을 진행할 것입니다. 그러나 많은 대기업들이 소비자 대상 전자상거래를 본뜬 유연한 조달 방식을 도입하기 시작하면서, 중소기업이 누리고 있는 것과 마찬가지로 SKU 단위의 투명한 가격 책정과 익일 배송을 요구하고 있습니다. BYOM(Bring Your Own Mobile)이 보급됨에 따라 지원 부담은 중앙 집중식 IT 부서에서 직원들에게로 옮겨가고 있으며, 대기업이 그동안 누려왔던 인력 측면의 우위는 약화되고 있습니다. 다만, 제로 트러스트의 기기 정책과 같은 거버넌스 요건에 관해서는 여전히 충분한 자원을 보유한 조직이 유리한 입장에 있습니다.

지역별 분석

2025년, 하이브리드 근무 하드웨어 시장 매출액 중 북미가 36.46%를 차지했습니다. 이는 포춘 500대 기업의 장비 교체 주기와 재택근무 장비에 대한 세액 공제에 힘입은 결과입니다. 이 지역은 잘 구축된 광섬유 백본과 광범위한 Wi-Fi 6E 구축의 혜택을 받고 있어, 풀 해상도의 4K 스트리밍 시 화질이 저하되는 경우가 거의 없습니다. 주 및 지방 자치단체의 보조금을 통해 공공 부문 종사자를 위한 장비에 대한 지원이 더욱 확대되고 있으며, 이에 따른 수요는 기업 본사 이외의 분야로도 확대되고 있습니다. 그러나 ‘캘리포니아주 개인정보 보호법’과 같은 사이버 보안 규제로 인해 규정 준수 비용이 증가하고 있어, 구매자들은 취약점 공개 프로그램이 문서화되어 있는 평판이 좋은 브랜드를 선택하는 경향이 있습니다.

아시아태평양은 세계 최고 수준인 연평균 성장률(CAGR) 12.62%의 성장 궤도에 올라 있습니다. 싱가포르, 인도, 일본에서 정부 주도로 5G 네트워크가 확대됨에 따라 지연이라는 병목 현상이 해소되어, 실시간으로 다수가 참여하는 화이트보드 이용이 가능해졌습니다. 인도의 전자기기 대상 ‘생산 연계형 인센티브(PLI)’ 제도는 로지텍과 예링크로부터의 수탁 생산을 유치하고 있으며, 이를 통해 수입 관세가 인하되고 물류 리드타임이 단축되고 있습니다. 인구 동향으로 인한 노동력 부족에 직면한 일본의 고용주들은 도시 외 지역의 인재 풀을 활용하기 위해 하이브리드 근무 모델을 도입하고 있습니다. 이러한 변화로 인해, 미국 홈 오피스의 주류를 이루고 있는 대형 디스플레이가 아닌, 아파트에서도 사용하기 편리한 소형 회의용 바에 대한 수요가 증가하고 있습니다. 동시에, 현지 브랜드들은 언어 현지화와 문화에 맞춘 UI 설계를 활용하여 서유럽의 기존 기업들을 앞지르고 있습니다.

유럽의 성장세가 둔화되고 있는 것은 환경 규제로 인해 규정 준수 비용이 증가하고 있기 때문입니다. 2025년 11월, 카드뮴계 양자점에 대한 RoHS 규제 적용 예외 조치가 종료됨에 따라, 각 공급업체들은 디스플레이 1대당 50-100달러를 재인증 시험에 투자할 수밖에 없게 되었습니다. 중동의 바이어들은 각국의 데이터 주권법에 대응하기 위해 하드웨어 암호화 드라이브로의 전환을 추진하고 있으며, 이러한 추세는 킹스턴이 2025년 11월에 발표한 지역별 스토리지 보고서에서도 지적된 바 있습니다. 아프리카에서는 광대역 환경이 아직 미비하여 시장은 여전히 발전 단계에 있지만, 남아프리카공화국과 케냐에서 진행된 시범 프로그램을 통해 태양광 발전 방식의 회의용 키트가 5 Mbps 미만의 회선에서도 작동한다는 사실이 입증되었으며, 인프라가 정비되면 잠재적인 성장 여지가 있음을 시사하고 있습니다. 남미에서의 보급 상황은 환율 변동에 따라 달라집니다. 브라질에서는 하이브리드 근무 방식의 추진 정책이 호황기에 수요를 자극하는 반면, 아르헨티나에서는 수입 규제로 인해 재생 제품의 암시장 유통 경로가 생겨나고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the hybrid work hardware market size is expected to increase from USD 28.50 billion in 2025 to USD 31.80 billion in 2026 and reach USD 52.40 billion by 2031, growing at a CAGR of 10.50% over 2026-2031.

This report is Segmented by Product Type (Computing Devices, Peripherals and Accessories, Collaboration Hardware, and More), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunication, BFSI, and More), Distribution Channel (Offline, and Online), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Hybrid Work Hardware Market Trends and Insights

Proliferation of Bring Your Own Meeting Policies

BYOM policies shorten hardware refresh cycles because employees can connect personal laptops to USB speakerphones and auto-framing cameras without proprietary codecs, bypassing complex IT provisioning. Owl Labs reported that 63% of hybrid workers in 2025 favored BYOM layouts that mirror familiar desktop interfaces. The preference aligns with the 12.8% CAGR expected for conference-room systems as firms replace fixed boxes with software-agnostic soundbars. Samsung, Cisco, and Logitech countered the trend in February 2026 by unveiling pre-integrated bundles that promise zero-touch deployment, an ecosystem play that trades openness for administrative simplicity. Organizations embracing modular BYOM still gain leverage when renegotiating SaaS contracts because hardware remains decoupled from licensing terms, preserving optionality in the 2028-2030 refresh window.

Surge in Video Conferencing Adoption Post Pandemic

Although webcam penetration peaked by 2024, spending persists as first-wave endpoints reach end of life and users demand 4K optics, neural noise suppression, and edge-based analytics. Logitech's Rally AI cameras, launched in January 2026, embed dedicated processors that execute speaker tracking locally, mitigating cloud round-trip latency and satisfying data-sovereignty mandates in healthcare and finance. University lecture-hall retrofits costing USD 8,000-15,000 per room underpin education's double-digit CAGR, with ceiling-mounted arrays enabling asynchronous playback for students in distant time zones. Appliance-style offerings, like Crestron's Collab Compute, package compute, touch control, and licensing into one SKU, reducing bill-of-materials complexity and accelerating deployment CRESTRON.COM.

Cybersecurity and Data Privacy Concerns in Collaborative Devices

Always-on cameras and microphones expand the attack surface that malicious actors exploit through firmware implants and man-in-the-middle attacks. AVIXA's 2024 survey indicated 58% of IT leaders delayed hardware rollouts until vendors proved ISO 27001-certified manufacturing and secure boot chains. Enterprises now specify Trusted Platform Modules and auto-patch utilities, adding USD 100-200 per endpoint yet averting potential GDPR fines equal to 4% of annual turnover. The trend elevates incumbent brands that publish CVE disclosures and fund bug-bounty programs, while penalizing white-box entrants with opaque supply chains.

Other drivers and restraints analyzed in the detailed report include:

- Upgrades to Conference Rooms for Hybrid Collaboration

- Rising Demand for AI-Powered Meeting Equity Features

- Budget Constraints for Small and Medium Businesses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid Work Hardware market size leadership in 2025 rested with computing devices, which held a 32.25% share, yet video conferencing systems are poised for faster expansion at a 12.8% CAGR through 2031. Computing endpoints have commoditized, with average business-laptop prices dropping 8% in 2025 as component spec sheets homogenized. Peripherals bridge the gap, exemplified by Jabra PanaCast's on-device DSPs that reduce cloud latency, while networking and connectivity hardware, such as Wi-Fi 6E routers, ensure bandwidth symmetry for multi-stream meetings. Collaboration boards and interactive whiteboards are ascending in education and healthcare, where touch-enabled annotation brings remote cohorts into room-based workflows. Ancillary categories like ergonomic lighting kits grow more slowly but round out holistic hybrid-work bundles.

Across the forecast horizon, enterprises will redirect capital from refreshed notebooks toward conference-room modernization, a shift accelerated by BYOM, as one smart bar can serve an entire team rather than multiple laptops per employee. Hybrid Work Hardware market share is therefore poised to rebalance toward shared-space infrastructure, especially as vendors collapse compute, control, and connectivity into single SKUs such as Crestron's Collab Compute. The greater margin resident in integrated room solutions grants vendors budget to embed neural accelerators, effectively raising the technology bar for late-comer competitors.

The hybrid Work Hardware market size is skewed toward large enterprises, with 68.46% in 2025, leveraging global contracts, bulk discounts, and in-house AV teams. Small and medium-sized enterprises, while resource-constrained, are projected to post a 12.24% CAGR, gradually narrowing the gap through 2031. The inflection stems from USB-based bars that require no specialist integrators, allowing office managers to install endpoints in under an hour. Financing models also level the playing field with HP, Dell, and Lenovo, which are now pricing laptops, monitors, and peripherals as monthly subscriptions, aligning with SMB cash-flow realities.

Large enterprises will continue controlling the premium tier, negotiating bundles of hardware, SaaS licenses, and five-year managed-services addenda. However, many have begun adopting flexible procurement practices that mirror consumer e-commerce, demanding transparent SKU-level pricing and next-day delivery, similar to what SMBs enjoy. As BYOM proliferates, the support burden falls from centralized IT to employees, reducing the staffing advantage historically enjoyed by large firms, although governance requirements such as zero-trust device posture still favor well-resourced organizations.

Geography Analysis

North America accounted for 36.46% of the Hybrid Work Hardware market revenue in 2025, underpinned by Fortune 500 refresh cycles and tax deductions for home-office equipment. The region benefits from mature fiber backbones and pervasive Wi-Fi 6E rollouts, ensuring that full-resolution 4K streams rarely downgrade. State and provincial grants further subsidize equipment for public-sector employees, broadening addressable demand beyond corporate headquarters. Yet cybersecurity regulations, such as the California Privacy Rights Act, increase compliance costs, nudging buyers toward established brands with documented vulnerability disclosure programs.

Asia-Pacific is on course for a 12.62% CAGR, the fastest worldwide. Government-funded 5G expansion in Singapore, India, and Japan removes latency bottlenecks and supports real-time, multi-participant whiteboarding. India's Production-Linked Incentive scheme for electronics attracts contract manufacturing from Logitech and Yealink, lowering import duties and shortening logistical lead times. Japanese employers, facing demographic labor shortages, embrace hybrid work models to tap non-urban talent pools; this shift drives high demand for compact, apartment-friendly conferencing bars rather than large-format displays prevalent in U.S. home offices. Simultaneously, local brands leverage linguistic localization and culturally specific UI cues to edge out Western incumbents.

Europe's growth lags because environmental mandates increase compliance costs. The November 2025 sunset of the RoHS exemption for cadmium-based quantum dots forced vendors to invest USD 50-100 per display in re-qualification testing. Middle Eastern buyers shift toward hardware-encrypted drives to meet national data-sovereignty laws, a behavior Kingston flagged in its November 2025 regional storage report. Africa remains nascent due to patchy broadband, yet pilot programs in South Africa and Kenya prove that solar-powered conference kits can function on sub-5 Mbps links, hinting at latent upside once infrastructure matures. South American adoption fluctuates with currency volatility; Brazil's hybrid-work incentives spur demand in bull cycles, whereas import restrictions in Argentina create gray-market channels for refurbished gear.

- Logitech International S.A.

- Cisco Systems, Inc.

- HP Inc.

- Lenovo Group Limited

- Dell Technologies Inc.

- Microsoft Corporation

- Apple Inc.

- Crestron Electronics, Inc.

- Barco NV

- GN Audio A/S (Jabra)

- AVer Information Inc.

- AVerMedia Technologies, Inc.

- Konftel AB

- Vaddio (Legrand AV Inc.)

- Shure Incorporated

- EPOS Audio A/S

- Bose Corporation

- DTEN, Inc.

- Yealink Network Technology Co., Ltd.

- Maxhub (Guangzhou Shiyuan Electronic Technology Company Limited)

- ClearOne Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Bring Your Own Meeting (BYOM) Policies Among Enterprises

- 4.2.2 Surge in Video Conferencing Adoption Post Pandemic

- 4.2.3 Upgrades to Conference Rooms for Hybrid Collaboration

- 4.2.4 Expansion of High-Speed Broadband and 5G Networks

- 4.2.5 Rising Demand for AI-Powered Meeting Equity Features

- 4.2.6 Tax Incentives for Remote Work Equipment in Select Countries

- 4.3 Market Restraints

- 4.3.1 Cybersecurity and Data Privacy Concerns in Collaborative Devices

- 4.3.2 Budget Constraints for Small and Medium Businesses

- 4.3.3 Environmental Regulations Limiting Use of Certain Display Materials

- 4.3.4 Component Shortages in Audio Chipsets Affecting Lead Times

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Industry Attractiveness - Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Computing Devices

- 5.1.2 Peripherals and Accessories

- 5.1.3 Collaboration Hardware

- 5.1.4 Video Conferencing and Meeting Room Systems

- 5.1.5 Networking and Connectivity Hardware

- 5.1.6 Other Product Types

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-Sized Enterprises

- 5.3 By End-user Industry

- 5.3.1 IT and Telecommunication

- 5.3.2 BFSI

- 5.3.3 Healthcare and Lifesciences

- 5.3.4 Retail and Consumer Goods

- 5.3.5 Education

- 5.3.6 Government and Public Sector

- 5.3.7 Manufacturing

- 5.3.8 Media and Entertainment

- 5.3.9 Other Industry Verticals

- 5.4 By Distribution Channel

- 5.4.1 Offline

- 5.4.2 Online

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Logitech International S.A.

- 6.4.2 Cisco Systems, Inc.

- 6.4.3 HP Inc.

- 6.4.4 Lenovo Group Limited

- 6.4.5 Dell Technologies Inc.

- 6.4.6 Microsoft Corporation

- 6.4.7 Apple Inc.

- 6.4.8 Crestron Electronics, Inc.

- 6.4.9 Barco NV

- 6.4.10 GN Audio A/S (Jabra)

- 6.4.11 AVer Information Inc.

- 6.4.12 AVerMedia Technologies, Inc.

- 6.4.13 Konftel AB

- 6.4.14 Vaddio (Legrand AV Inc.)

- 6.4.15 Shure Incorporated

- 6.4.16 EPOS Audio A/S

- 6.4.17 Bose Corporation

- 6.4.18 DTEN, Inc.

- 6.4.19 Yealink Network Technology Co., Ltd.

- 6.4.20 Maxhub (Guangzhou Shiyuan Electronic Technology Company Limited)

- 6.4.21 ClearOne Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment