|

시장보고서

상품코드

2065604

미국의 안면 주사제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Facial Injectables - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

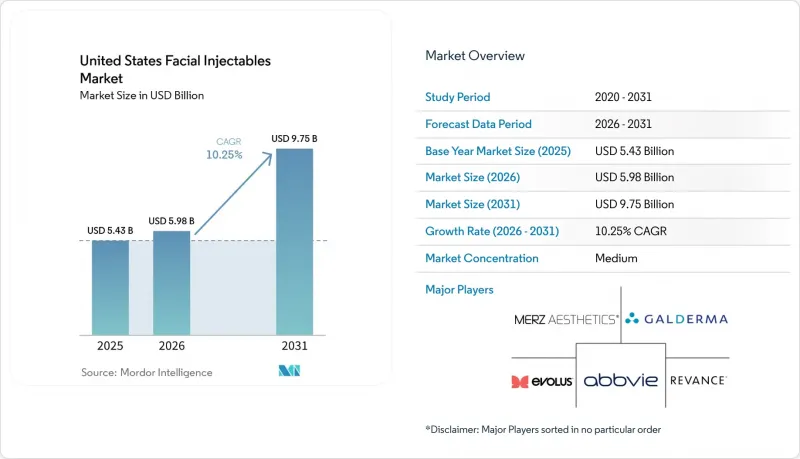

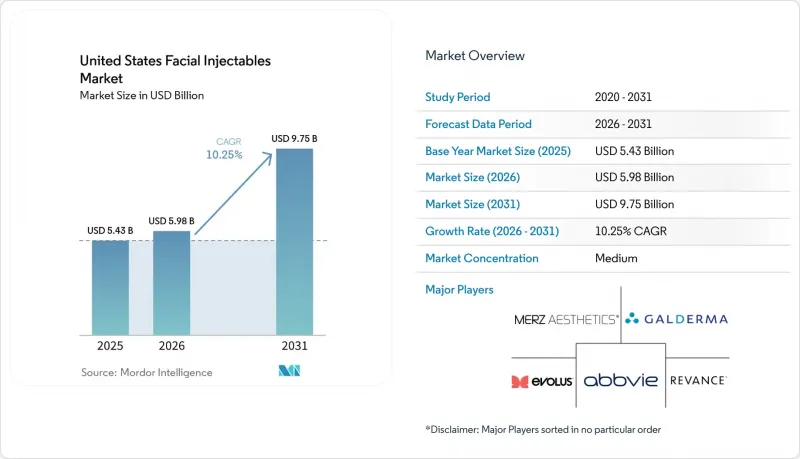

Mordor Intelligence에 의하면, 미국 안면 주사제 시장 규모는 2025년 54억 3,000만 달러, 2026년 59억 8,000만 달러에서 2031년까지 97억 5,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 10.25%를 나타낼 전망입니다.

본 보고서는 제품 유형(보툴리눔툭신(보톡스), 히알루론산 필러, 하이드록시아파타이트 필러 등), 용도(얼굴 주름 개선, 입술 볼륨 증대, 중안면 볼륨 증대, 턱선 형성, 흉터 개선, 기타), 최종 사용자(피부과 클리닉, 외과 센터, 메디컬 스파, 병원/외래수술센터(ASC))별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국 안면 주사제 시장 동향 및 분석

저침습적 안면 미용 시술에 대한 선호도 증가

외과적 안면 시술에서 주사제 시술로의 전환은 미국 안면 주사제 시장에서 환자들이 미용 관리를 접근하는 방식에 지속적인 변화가 일어나고 있음을 반영합니다. 2024년에는 미용 목적의 저침습 시술 총 건수가 2,820만 건을 넘어섰으며, 신경 조절제 주사만 해도 988만 건에 달했습니다. 이는 이러한 치료법이 폭넓은 환자층에게 얼마나 친숙해졌는지를 보여줍니다. 회복 기간이 짧고, 결과가 예측 가능하며, 치료 효과를 단계적으로 조절할 수 있다는 점에서 정기적인 유지 관리에 있어서는 주사제가 외과 수술보다 여전히 매력적인 선택지로 남아 있습니다. 시술 건수가 많다는 점은 소비자들이 얼굴의 노화를 더욱 적극적으로 주시하도록 유도하고 있으며, 신경 쓰이는 부분을 발견한 후 치료를 예약하기까지 걸리는 기간을 단축시키고 있습니다. ‘메디컬 스파’라는 채널은 지금까지 피부과나 성형외과를 방문해 본 적이 없는 소비자들에게도 이 카테고리를 친숙하게 느끼게 함으로써, 이러한 경향을 더욱 강화하고 있습니다.

청소년을 대상으로 한 예방적 주사 요법

Z세대와 젊은 밀레니얼 세대를 대상으로 한 예방적 치료는 미국 안면 주사제 시장 수요 연령대 구성을 변화시키고 있습니다. 『Aesthetic Surgery Journal』지에 게재된 2025년 동료 심사를 거친 분석에 따르면, 평가 대상 환자의 연령대가 10년씩 늘어날 때마다 첫 시술의 평균 연령이 8.8세 낮아지는 것으로 밝혀졌으며, 이는 일시적인 유행이 아니라 명확한 세대 변화를 시사하고 있습니다. 이는 상업적으로도 중요한 의미를 지닙니다. 왜냐하면 치료 시작 시기가 빠를수록 환자의 평생 재구매 주기가 길어지기 때문입니다. 또한, 치료 결과가 일관적이라면 20대에 형성된 브랜드 충성도는 오랫동안 지속되므로, 브랜드 간 경쟁 환경도 변화하게 됩니다. 이 계층과 조기에 접점을 형성한 의료기관이나 브랜드는 환자가 시간이 지남에 따라 새로운 치료 부위를 추가해 나갈수록 수요를 유지하는 데 유리한 입장에 설 수 있습니다.

높은 본인 부담금으로 인한 재치료의 부담

미국의 안면 주사제 시장은 치료비의 압도적 다수가 본인 부담인 탓에 여전히 환자의 지출에 크게 좌우되고 있습니다. 보톡스 등 신경독소 치료의 1회 시술 비용은 보통 300-600달러이지만, 히알루론산 필러 치료는 제품 선택이나 시술자의 경력에 따라 다르지만, 부위당 보통 600-2,000달러가 시세입니다. 얼굴의 여러 부위를 관리하는 환자나, 동일한 치료 주기 내에서 보톡스와 필러를 병행하는 환자의 경우, 이러한 비용은 급격히 증가합니다. 이 부담은 해당 카테고리가 더 젊고 가격에 민감한 소비자층으로 확대됨에 따라 특히 중요해집니다. 이러한 소비자층에게 있어 미용에 쓰는 예산은 일상적인 가계비와 직접적으로 경쟁하는 요소입니다. 회원제 모델이나 치료 계획, 그 밖의 고객 유지 도구를 활용하지 않는 시술자는 내원 지연, 시술 빈도 감소, 그리고 고객 이탈의 위험이 높아집니다.

부문별 분석

2025년, 보툴리눔툭신(보톡스)는 미국 안면 주사제 시장 점유율의 56.31%를 차지하며, 이 부문에서 신규 환자를 유치하는 주요 통로로서의 입지를 공고히 하고 있습니다. 이러한 우위는 미간 주름, 눈썹 리프팅, 교근 축소, 다한증 등 폭넓은 적용 분야뿐만 아니라, 안정적인 연간 수요를 뒷받침하는 재시술 패턴에서 비롯됩니다. 미국의 안면 주사제 업계는 이 분야에 대한 높은 인지도 덕분에 혜택을 보고 있습니다. 많은 초진 환자들이 보다 개인 맞춤형 필러 치료로 넘어가기 전에, 먼저 보툴리눔툭신(보톡스) 치료부터 시작하기 때문입니다. ‘DAXXIFY’는 임상 효과의 지속 기간 중앙값이 24주라는 특징 덕분에 경쟁 우위를 한층 더 강화하고 있습니다. 이에 따라 가치에 대한 논의는 단순한 시술 빈도에서 1회 내원당 유효성으로 전환되고 있습니다.

하이드록시아파타이트 계열 필러와 PLLA 바이오자극제는 재생의학 분야에서 그 입지를 넓혀가고 있습니다. 이 분야에서는 환자들이 단순히 단기적인 볼륨 증가뿐만 아니라, 구조적인 지지력과 콜라겐 생성을 촉진하는 효과를 원하는 경우가 많기 때문입니다. 멜츠 에스테틱스는 2026년 4월, 데콜테 부위에 대한 ‘RADIESSE’의 FDA 승인을 획득했습니다. 이로써 해당 브랜드의 적응증은 4가지로 확대되며, 얼굴과 신체 모두를 아우르는 재생의료 분야에서의 입지가 강화될 것입니다. PMMA 및 콜라겐 기반 필러는 여드름 흉터 교정이나 만성적인 볼륨 부족 개선 등 용도는 제한적이지만, 지속적인 효과를 발휘하고 있습니다. 히알루론산(HA) 필러는 적응증 확대, 피부 질 개선 치료에 대한 관심 증가, 그리고 GLP-1 치료를 받고 있는 환자를 대상으로 한 적극적인 연구 개발에 힘입어, 2026년부터 2031년까지 연평균 성장률(CAGR) 11.38%를 기록하며 가장 빠르게 성장하는 제품 부문으로 자리매김하고 있습니다. 미국의 안면용 필러 업계에서는 FDA 승인 절차가 여전히 중요한 진입 장벽으로 작용하고 있으며, 이로 인해 신규 진출기업들의 경쟁이 치열해지는 상황에서도 기존 브랜드들은 시장 점유율을 계속 지켜내고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the united states facial injectables market size is projected to expand from USD 5.43 billion in 2025 and USD 5.98 billion in 2026 to USD 9.75 billion by 2031, registering a CAGR of 10.25% between 2026 to 2031.

This report is Segmented by Product Type (Botulinum Toxin, HA Fillers, Calcium Hydroxylapatite Fillers, and More), Application (Facial Line Correction, Lip Augmentation, Midface Augmentation, Jawline Contouring, Scar Correction, Others), and End User (Dermatology Clinics, Surgery Centers, Medical Spas, Hospitals/ASCs). The Market Forecasts are Provided in Terms of Value (USD).

United States Facial Injectables Market Trends and Insights

Growing Preference for Minimally Invasive Facial Aesthetics

The shift away from surgical facial procedures toward injectables reflects a durable change in how patients approach aesthetic care in the United States facial injectables market. Total cosmetic minimally invasive procedures exceeded 28.2 million in 2024, and neuromodulator injections alone reached 9.88 million, which shows how familiar these treatments have become for a broad patient base. Short recovery time, predictable outcomes, and the ability to adjust treatment gradually continue to make injectables more appealing than surgery for repeat maintenance. High procedure volume also teaches consumers to monitor facial aging more actively, which shortens the gap between noticing a concern and booking treatment. The medspa channel strengthens this pattern because it brings the category closer to consumers who may never have engaged a dermatologist or plastic surgeon before.

Preventative Injectables Among Younger Adults

Preventive treatment among Gen Z and younger millennials is changing the age profile of demand across the United States facial injectables market. A 2025 peer-reviewed analysis in the Aesthetic Surgery Journal found that the average age of first injection declines by 8.8 years with each successive decade of patients evaluated, which points to a strong cohort shift rather than a passing preference. This matters commercially because earlier treatment starts create a longer repeat-purchase cycle over the life of the patient. It also changes brand competition, because loyalty formed in the 20s can persist for many years if treatment outcomes remain consistent. Providers and brands that connect with this group early are better positioned to retain demand as these patients add new treatment areas over time.

High Out-of-Pocket Repeat-Treatment Burden

The United States facial injectables market remains heavily exposed to patient spending because treatments are overwhelmingly self-pay. Neurotoxin sessions usually range from USD 300 to USD 600, while HA filler treatments typically range from USD 600 to USD 2,000 per area depending on product choice and injector profile. These costs build quickly for patients who maintain several facial areas or combine toxins with fillers in the same treatment cycle. That burden is especially important as the category expands into younger and more price-sensitive consumers, whose aesthetic budgets compete directly with routine household expenses. Providers that do not use membership models, treatment plans, or other retention tools face a greater risk of delayed visits, reduced frequency, and higher churn.

Other drivers and restraints analyzed in the detailed report include:

- Broader Male-Patient Adoption

- Longer-Duration Toxins and Regenerative Fillers

- Counterfeit and Unapproved Online Injectables

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Botulinum toxin held 56.31% of United States facial injectables market share in 2025, which confirms its position as the main entry point for new patients in the category. Its lead reflects broad use across glabellar lines, brow lifting, masseter reduction, and hyperhidrosis, along with repeat treatment patterns that support stable annual demand. The United States facial injectables industry also benefits from the category's familiarity, because many first-time patients begin with toxin before moving into more customized filler protocols. DAXXIFY adds another competitive layer by offering a median clinical duration of 24 weeks, which shifts the value discussion from simple session frequency toward efficacy per visit.

Calcium hydroxylapatite fillers and PLLA biostimulators are gaining momentum in regenerative treatment settings, where patients often want structural support and collagen stimulation rather than short-term volumization alone. Merz Aesthetics receives FDA approval in April 2026 for RADIESSE in the decollete area, which expands the brand to four indications and strengthens its regenerative positioning across face and body. PMMA and collagen-based fillers continue to serve narrower but durable uses such as acne scar correction and chronic volume deficit management. HA fillers are the fastest-growing product segment at 11.38% CAGR from 2026 to 2031, supported by broader indication expansion, rising interest in skin-quality treatment, and active R&D directed at GLP-1-treated patients. FDA approval pathways remain a meaningful entry barrier in the United States facial injectables industry, which helps established brands defend share even as new entrants intensify competition.

List of Companies Covered in this Report:

- AbbVie (Allergan Aesthetics)

- Bloomage Biotechnology

- Croma-Pharma

- Crown Laboratories

- Daewoong Pharmaceutical

- Evolus

- Galderma

- Hugel

- Hugel America

- Ipsen

- Laboratoires Expanscience

- Medytox

- Merz Pharma

- Prollenium Medical Technologies

- Revance

- Sinclair Pharma

- Suneva Medical

- Teoxane Laboratories

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Preference for Minimally Invasive Facial Aesthetics

- 4.2.2 Preventative Injectables Among Younger Adults

- 4.2.3 Broader Male-Patient Adoption

- 4.2.4 Longer-Duration Toxins and Regenerative Fillers

- 4.2.5 GLP-1-Related Facial Volume-Loss Correction Demand

- 4.2.6 Skin-Quality Injectables Expanding Treatment Occasions

- 4.3 Market Restraints

- 4.3.1 High Out-Of-Pocket Repeat-Treatment Burden

- 4.3.2 Counterfeit and Unapproved Online Injectables

- 4.3.3 Tighter Injector-Supervision and Delegation Rules

- 4.3.4 Adverse-Event and Liability Sensitivity in High-Volume Settings

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Botulinum Toxin

- 5.1.2 Hyaluronic Acid Fillers

- 5.1.3 Calcium Hydroxylapatite Fillers

- 5.1.4 Poly-L-lactic Acid Biostimulators

- 5.1.5 PMMA / Collagen Hybrid Fillers

- 5.1.6 Other Facial Soft Tissue Fillers

- 5.2 By Application

- 5.2.1 Facial line correction

- 5.2.2 Lip augmentation and perioral rejuvenation

- 5.2.3 Midface and cheek augmentation

- 5.2.4 Chin and jawline contouring

- 5.2.5 Acne scar and atrophic scar correction

- 5.2.6 Lipoatrophy and volume restoration

- 5.2.7 Other Applications

- 5.3 By End User

- 5.3.1 Dermatology clinics

- 5.3.2 Plastic surgery and cosmetic surgery centers

- 5.3.3 Medical spas

- 5.3.4 Hospitals and ambulatory surgery centers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 AbbVie (Allergan Aesthetics)

- 6.3.2 Bloomage Biotechnology

- 6.3.3 Croma-Pharma

- 6.3.4 Crown Laboratories

- 6.3.5 Daewoong Pharmaceutical

- 6.3.6 Evolus

- 6.3.7 Galderma

- 6.3.8 Hugel

- 6.3.9 Hugel America

- 6.3.10 Ipsen

- 6.3.11 Laboratoires VIVACY

- 6.3.12 Medytox

- 6.3.13 Merz Aesthetics

- 6.3.14 Prollenium Medical Technologies

- 6.3.15 Revance

- 6.3.16 Sinclair Pharma

- 6.3.17 Suneva Medical

- 6.3.18 Teoxane Laboratories

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment