|

시장보고서

상품코드

2065609

대퇴골두 인공 관절 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Femoral Head Prostheses - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

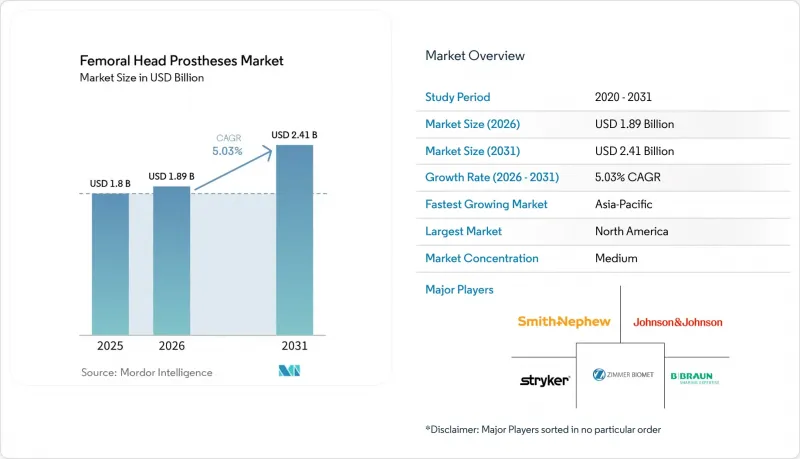

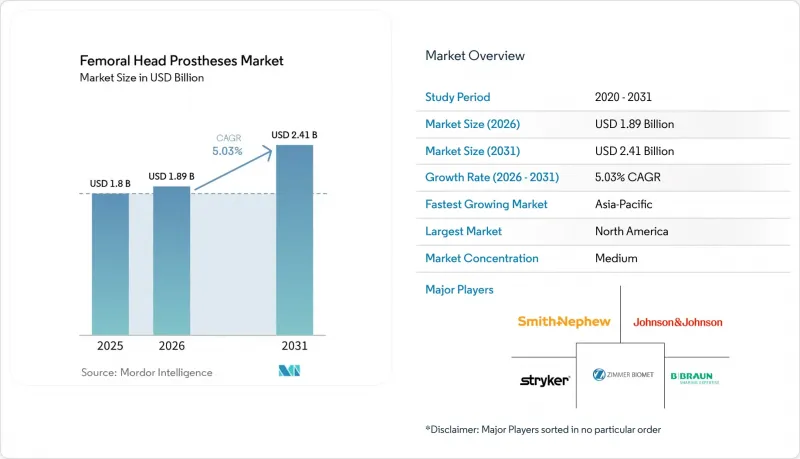

Mordor Intelligence에 의하면, 대퇴골두 인공 관절 시장 규모는 2025년 18억 달러로 평가되었고, 2026년에는 18억 9,000만 달러로 추정되고, 2031년까지 24억 1,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 5.03%로 성장할 전망입니다.

본 보고서는 제품 유형별(바이폴라, 유니폴라 및 엔도세팔릭, 모듈러), 재질별(CoCr 합금, 스테인리스 스틸, 세라믹, 지르코늄 산화물), 고정 방법별(시멘트 고정, 시멘트리스, 하이브리드), 수술 방법별(반관절 치환술-FNF, 괴사, 인공 고관절 전치환술, 재치환술), 최종 사용자별(병원, ASC, 전문 의료 센터), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 예상치는 금액(달러)으로 표시되어 있습니다.

세계의 대퇴골두 인공관절 시장 동향 및 인사이트

고령화 사회에서 발생하는 전위성 대퇴골 경부 골절의 부담 증가

대퇴골두 인공관절 시장은 자금 조달의 변동에도 불구하고 골절 발생률이 꾸준히 증가하고 있어, 전 세계 고령화 인구를 배경으로 계속해서 견조한 지지를 얻고 있습니다. 2025년 분석에 따르면, 2024년 전 세계 연령 조정 유병률은 10만 명당 1,834.14로, 1990년 수준보다 14.2% 증가한 것으로 나타났습니다. 이 조사에 따르면, 인구 고령화와 증가를 배경으로 2036년까지 전 세계에서 1,680만 건의 고관절 골절이 발생할 것으로 예측되고 있습니다. 미국에서는 현재 연간 25만 명 이상이 고관절 골절을 앓고 있으며, 2050년까지 50만 명에 달할 것으로 예상에 따라 골절 관련 임플란트에 대한 수요는 계속해서 견조한 추세를 보일 전망입니다. T

불안정 골절에 대한 고정술보다 인공관절 치환술이 선호되는 경향

대퇴골두 인공관절 시장은 불안정 골절에 대한 인공관절 치환술로의 명확한 전환에 힘입어 성장하고 있습니다. 2025년에 실시된, 2만 9,980명의 환자를 대상으로 한 20건의 체계적 문헌고찰에 따르면, 전체 인공 고관절 치환술(THA)은 수술 시간이 20분 더 걸리는 경우, 반 인공 고관절 치환술에 비해 재수술 위험을 33% 감소시키고, 수술 후 조기 기능 회복을 촉진하는 것으로 나타났습니다. 반관절 치환술은 수술 시간이 짧고 마취에 노출되는 시간도 적기 때문에 운동 기능이 제한된 고령 환자에게는 여전히 유용합니다. 75세 이상으로 허약도가 높고 동반 질환이 많은 환자들에게는 양극형 임플란트의 사용이 증가하고 있습니다. 2023년 이탈리아에서 대퇴골 경부 골절 치료 중 부분 관절 치환술이 44.5%를 차지했으며, 시장에서 부분 관절 치환술이 선택적인 역할을 하고 있음을 알 수 있습니다.

건강 상태가 양호한 고령자를 대상으로 한 인공 고관절 전치환술(THA)과 듀얼 모빌리티형 치환술

건강 상태가 양호한 고령 환자들 사이에서 인공 고관절 전치환술(THA)이나 듀얼 모빌리티형 임플란트를 선택하는 경향이 강해지고 있으며, 이것이 대퇴골두 보철물 시장 수요를 견인하고 있습니다. 2025년에 실시된 체계적 문헌고찰 및 메타분석에 따르면, 특정 노년기 대퇴골 경부 골절 사례에서 듀얼 모빌리티형 인공 고관절 치환술(THA)이 양극형 반관절 치환술에 비해 우수한 기능적 예후를 보였으며, 장기적인 합병증도 적은 것으로 밝혀졌습니다. 이러한 추세는 60세에서 79세 사이의 활동적인 환자층에서 가장 두드러지며, 이 같은 환자들은 인지 기능이 양호하고, 장수화를 염두에 두고 재치환술의 위험을 최소화하는 것을 우선시하고 있습니다. 현재 외과의사들은 잠재적인 연골 마모나 향후 인공관절 치환술로 전환함에 따른 문제를 완화하기 위해, 이러한 환자의 고관절에 대한 시술을 더욱 적극적으로 시행하고 있습니다.

부문별 분석

2025년, 양극형 대퇴골두 인공관절은 시장 점유율의 62.10%를 차지했으며, 전위성 대퇴골경부 골절 치료 분야에서 주도적인 위치를 유지했습니다. 수술 시간 단축 및 고관절 마모 감소와 같은 임상적 이점으로 인해, 고령 환자에게 이상적인 선택지가 되고 있습니다. 단극형 및 내두개형 기기는 비용 효율성을 중시하는 시장에서 여전히 중요한 위치를 차지하고 있지만, 2031년까지 연평균 성장률(CAGR) 6.90%를 나타낼 것으로 예측되는 모듈형 구성 요소는 수술 중 유연성과 재이식 수술의 복잡성에 대응할 수 있는 능력 덕분에 지지를 넓혀가고 있습니다.

2025년 소재별 시장 점유율에서 코발트-크롬 합금이 48.85%를 차지했으며, 이는 비용 대비 효과와 외과의사들이 이 소재에 익숙하다는 점이 주된 요인으로 꼽힙니다. 스테인리스 스틸은 장기적인 성능이 뛰어난 소재로의 전환에 따라 시장 점유율이 계속해서 하락하고 있습니다. 세라믹은 2031년까지 연평균 성장률(CAGR) 7.20%를 기록하며 성장할 것으로 예상되며, 특히 젊고 활동적인 환자들 사이에서 마모나 재수술 위험이 낮다는 점 때문에 인기가 높아지고 있습니다. 시장은 실적이 입증되고 일관된 제조 기준을 갖춘 소재로 점차 전환되고 있습니다.

지역별 분석

2025년, 북미는 프리미엄 임플란트 수요와 임상적 채택을 배경으로 대퇴골두 인공관절 시장 점유율의 41.95%를 차지했습니다. 미국은 고관절 골절 발생률이 높고, 인공관절 치환술에 대한 확립된 보험 급여 제도, 그리고 검증된 임플란트를 외과의사들이 빠르게 도입함에 따라 이러한 추세를 주도했습니다. 미국에서 대퇴골 경부 골절의 연령 조정 사망률은 2002년 10만 명당 39.6명에서 2023년에는 10만 명당 22.4명으로 감소했습니다. 치료 성과가 향상됨에 따라 재식술 관리, 재료 선택 및 임플란트의 수명에 대한 관심이 높아지고 있습니다. 캐나다와 멕시코의 점유율은 비교적 낮았지만, 멕시코는 가격에 민감한 미국 환자들을 대상으로 한 의료 관광의 혜택을 누리고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.30%로 성장할 것으로 예상되며, 대퇴골두 인공관절 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 중국, 일본, 한국의 고령화 추세에 더해, 인도와 동남아시아에서의 수술 체계 확충이 성장을 견인하고 있습니다. 해당 지역에는 아직 충족되지 않은 수요가 존재하기 때문에 진단, 외상 환자 의뢰, 수술 체계에서 약간의 개선만 보여도 수술 건수를 대폭 늘릴 수 있습니다. 중국에서는 임플란트 분류 기준이 엄격해지면서 공급업체의 품질은 향상되고 있지만, 신규 진출기업 시장 진입이 지연될 가능성이 있습니다.

유럽은 성숙한 인공관절 치환술의 진료 경로, 널리 보급된 시멘트 고정 방식의 골절 치료, 그리고 탄탄한 등록제도에 힘입어 대퇴골두 인공관절의 주요 시장으로 자리매김하고 있습니다. 서유럽에서는 검증된 임플란트 플랫폼이 선호되는 반면, 동유럽에서는 비용을 중시하는 시멘트 고정 방식의 외과적 시술 분야에서 성장 가능성이 있습니다. 남미에서는 브라질이 시장을 독점하고 있으며, 공급업체들은 대규모 유통망을 통해 가격을 중시하는 수요에 초점을 맞추었습니다. 중동 및 아프리카 시장 점유율은 작지만, GCC 국가들의 전문 정형외과 센터에 대한 투자가 고부가가치 사례에 대한 기회를 창출하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the femoral head prostheses market size is expected to increase from USD 1.8 billion in 2025 to USD 1.89 billion in 2026 and reach USD 2.41 billion by 2031, growing at a CAGR of 5.03% over 2026-2031.

This report is Segmented by Product Type (Bipolar, Unipolar/Endocephalic, Modular), Material (CoCr Alloy, Stainless Steel, Ceramic, Oxidized Zirconium), Fixation (Cemented, Cementless, Hybrid), Procedure (Hemiarthroplasty-FNF, Necrosis, THA, Revision), End User (Hospitals, Ascs, Specialty Centers), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts in Value (USD).

Global Femoral Head Prostheses Market Trends and Insights

Rising Displaced Femoral Neck Fracture Burden In Aging Population

The femoral head prostheses market continues to find strong support from the aging global population, as the incidence of fractures rises steadily despite funding fluctuations. A 2025 analysis highlighted a global age-standardized prevalence rate of 1,834.14 per 100,000 in 2024, reflecting a 14.2% increase from 1990 levels. The study projected 16.8 million global hip fracture cases by 2036, driven by population aging and growth. In the United States, hip fractures currently affect over 250,000 individuals annually, with projections reaching 500,000 by 2050, ensuring consistent demand for fracture-related implants. T

Arthroplasty Preference Over Fixation For Unstable Fractures

The femoral head prostheses market benefits from a clear shift toward arthroplasty for unstable fractures. A 2025 review of 20 systematic studies involving 29,980 patients showed that Total Hip Arthroplasty (THA) reduced revision risk by 33% and improved early functionality compared to hemiarthroplasty, despite a 20-minute longer surgery. Hemiarthroplasty remains relevant for older patients with limited mobility due to shorter operation times and reduced anesthesia exposure. Bipolar implants are increasingly used in patients over 75 with higher frailty and comorbidities. In 2023, partial arthroplasty accounted for 44.5% of femoral neck fracture treatments in Italy, reflecting a selective role for hemiarthroplasty within the market.

Total Hip Arthroplasty And Dual-Mobility Substitution In Fitter Elderly

Healthier elderly patients are increasingly choosing Total Hip Arthroplasty (THA) and dual-mobility constructs, driving demand in the femoral head prostheses market. A 2025 systematic review and meta-analysis highlighted that dual-mobility THA demonstrated superior functional outcomes and fewer long-term complications compared to bipolar hemiarthroplasty in select geriatric femoral neck fracture cases. This trend is most evident among active patients aged 60 to 79, who are cognitively intact and prioritize minimizing revision risks over their extended lifespan. Surgeons are now more proactive in addressing the acetabulum in these patients to mitigate potential cartilage wear or future conversion challenges.

Other drivers and restraints analyzed in the detailed report include:

- Cemented Stem Adoption In Osteoporotic Fracture Care

- Faster-Recovery Surgical Workflows And Muscle-Sparing Approaches

- Tender-Driven Pricing Pressure And Bundled Trauma Episode Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, bipolar femoral head prostheses held 62.10% of the market share, maintaining their leadership in displaced femoral neck fracture care. Their clinical advantages, including shorter procedures and reduced acetabular wear, make them ideal for elderly patients. Unipolar and endocephalic devices remain relevant in cost-sensitive markets, while modular components, projected to grow at 6.90% CAGR through 2031, gain traction for their intraoperative flexibility and ability to address revision complexities.

Cobalt-chromium alloy accounted for 48.85% of the market share by material in 2025, driven by its cost-effectiveness and surgeon familiarity. Stainless steel continues to decline in favor of materials with better long-term performance. Ceramic, forecasted to grow at 7.20% CAGR through 2031, is gaining popularity for its lower wear and revision risks, particularly among younger, active patients. The market is shifting towards proven materials with validated outcomes and consistent manufacturing standards.

Geography Analysis

In 2025, North America held a 41.95% share of the femoral head prostheses market, driven by premium implant demand and clinical adoption. The United States led this trend due to a high incidence of hip fractures, established arthroplasty reimbursements, and rapid surgeon adoption of validated implants. Age-adjusted mortality from femoral neck fractures in the United States declined from 39.6 per 100,000 in 2002 to 22.4 per 100,000 in 2023. Improved outcomes have increased the focus on revision management, material choice, and survivorship. Canada and Mexico contributed smaller shares, with Mexico benefiting from medical tourism by price-sensitive United States patients.

Asia-Pacific is projected to grow at a CAGR of 8.30% through 2031, making it the fastest-growing region in the femoral head prostheses market. Aging populations in China, Japan, and South Korea, along with expanding surgical capacity in India and Southeast Asia, are driving growth. The region's unmet needs mean even modest improvements in diagnosis, trauma referrals, and operating capacity can significantly boost procedure volumes. In China, stricter implant classifications are improving supplier quality but may delay market entry for new players.

Europe remains a key market for femoral head prostheses, supported by mature arthroplasty pathways, widespread cemented fracture care, and strong registry systems. Western Europe favors validated implant platforms, while Eastern Europe offers growth potential in cost-sensitive cemented trauma procedures. In South America, Brazil dominates the market, with suppliers focusing on price-conscious demand through scaled distribution. The Middle East and Africa contribute a smaller share, but GCC investments in specialized orthopedic centers are creating opportunities for high-value cases.

- AK Medical Holdings Limited

- B. Braun

- Beznoska, s.r.o.

- Corin Group Limited

- Enovis Corporation

- Exactech

- implantcast GmbH

- Johnson & Johnson MedTech (DePuy Synthes)

- Mathys Ltd Bettlach

- Medacta Group SA

- Meril Life Science

- MicroPort

- Ortho Development Corporation

- Peter Brehm GmbH

- Smiths Group

- Stryker

- Surgival Co., S.A.U.

- United Orthopedic Corporation

- Waldemar Link

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Displaced Femoral Neck Fracture Burden in Aging Populations

- 4.2.2 Arthroplasty Preference Over Fixation for Unstable Fractures

- 4.2.3 Cemented Stem Adoption in Osteoporotic Fracture Care

- 4.2.4 Faster-Recovery Surgical Workflows and Muscle-Sparing Approaches

- 4.2.5 Registry-Led Shift Toward Validated Stem and Head Platforms

- 4.2.6 SKU Renewal from MDR Recertification Favoring Scaled Suppliers

- 4.3 Market Restraints

- 4.3.1 Total Hip Arthroplasty and Dual-Mobility Substitution in Fitter Elderly Patients

- 4.3.2 Tender-Driven Pricing Pressure and Bundled Trauma Episode Economics

- 4.3.3 MDR Recertification Cost and Portfolio Rationalization

- 4.3.4 Medico-Legal Overhang on Taper and Head-Related Failures

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Bipolar Femoral Head Prostheses

- 5.1.2 Unipolar / Endocephalic Femoral Head Prostheses

- 5.1.3 Modular Femoral Head Components

- 5.2 By Material

- 5.2.1 Cobalt-Chromium Alloy

- 5.2.2 Stainless Steel

- 5.2.3 Ceramic

- 5.2.4 Oxidized Zirconium and Advanced Bearing Surfaces

- 5.3 By Fixation Compatibility

- 5.3.1 Cemented-Compatible Systems

- 5.3.2 Cementless-Compatible Systems

- 5.3.3 Hybrid / Convertible Systems

- 5.4 By Procedure Type

- 5.4.1 Hemiarthroplasty for Displaced Femoral Neck Fracture

- 5.4.2 Hemiarthroplasty for Femoral Head Necrosis

- 5.4.3 Total Hip Arthroplasty

- 5.4.4 Revision Hip Arthroplasty and Hemi-to-Total Conversion

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Ambulatory Surgical Centers

- 5.5.3 Specialty Orthopedic Centers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AK Medical Holdings Limited

- 6.3.2 B. Braun Melsungen AG

- 6.3.3 Beznoska, s.r.o.

- 6.3.4 Corin Group Limited

- 6.3.5 Enovis Corporation

- 6.3.6 Exactech, Inc.

- 6.3.7 implantcast GmbH

- 6.3.8 Johnson & Johnson MedTech (DePuy Synthes)

- 6.3.9 Mathys Ltd Bettlach

- 6.3.10 Medacta Group SA

- 6.3.11 Meril Life Sciences Pvt. Ltd.

- 6.3.12 MicroPort Scientific Corporation

- 6.3.13 Ortho Development Corporation

- 6.3.14 Peter Brehm GmbH

- 6.3.15 Smith & Nephew plc

- 6.3.16 Stryker Corporation

- 6.3.17 Surgival Co., S.A.U.

- 6.3.18 United Orthopedic Corporation

- 6.3.19 Waldemar Link GmbH & Co. KG

- 6.3.20 Zimmer Biomet Holdings, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment