|

시장보고서

상품코드

2065620

사료용 아답토젠 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Feed Adaptogens - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

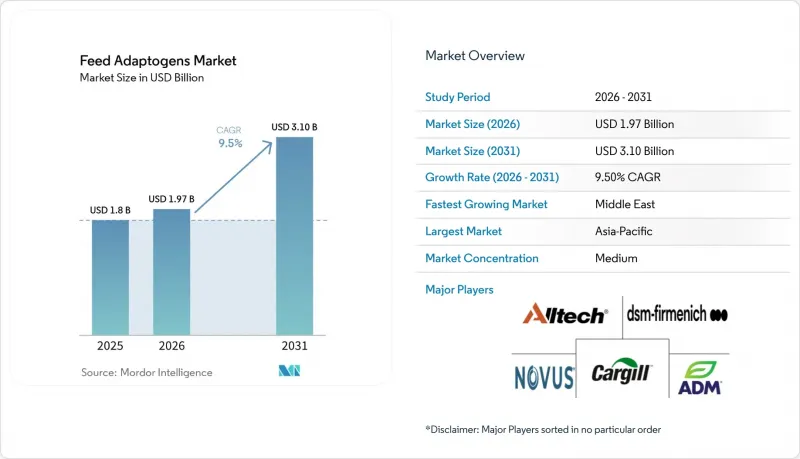

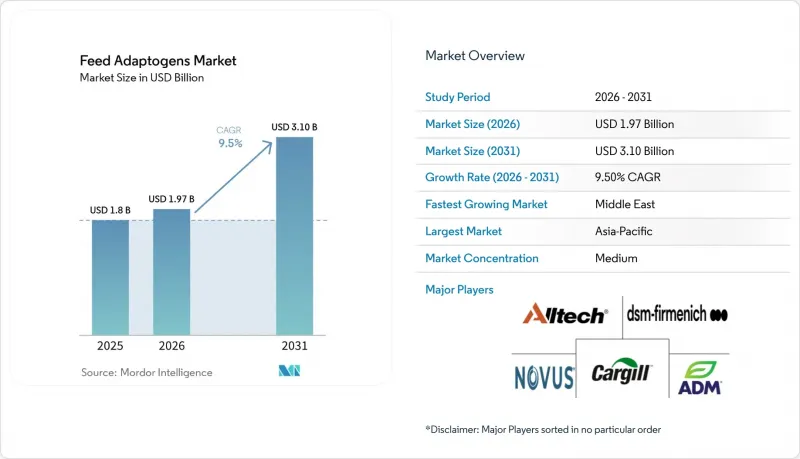

Mordor Intelligence에 의하면, 사료용 아답토젠 시장 규모는 2025년 18억 달러에서 2026년에는 19억 7,000만 달러로 확대되어 2031년까지 31억 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 9.50%로 성장할 전망입니다.

본 보고서는 원료별(허브계 아답토젠, 버섯계 아답토젠), 형태별(분말, 액체, 캡슐·비즈렛), 가축별(가금류, 돼지, 반추동물, 수산 양식, 반려동물), 기능별(스트레스 완화, 면역 강화, 사료 전환율 향상), 지역별(북미, 남미, 유럽, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 사료용 아답토젠 시장 동향 및 인사이트

성장 촉진제로서의 항생제 사용 금지

항생제를 이용한 성장 촉진제 사용 금지는 사료용 아답토젠 시장에 있어 가장 확실한 구조적 뒷받침이 되고 있습니다. 이는 몇몇 주요 축산 경제권에서 가장 널리 정착되어 있고 비용이 저렴한 성장 촉진 수단이 배제되었기 때문입니다. 미국은 의학적으로 중요한 항균제의 생산과 사용을 중단했고, 중국은 항생제를 이용한 성장 촉진제를 폐지했으며, 캐나다는 항균제 라벨에서 성장 촉진 관련 표기를 삭제함에 따라, 공급처가 비항생제 사료 솔루션으로 전환되었습니다. 또한, 사료용 아답토젠 시장은 항생제 사용이 여전히 유연하게 허용되는 중소득 생산국들의 수출 압력으로부터도 혜택을 보고 있습니다. 이는 수출업체가 수출 대상 시장의 구매자 요건을 준수해야 할 필요성이 커지고 있기 때문입니다.

천연 및 허브 유래 축산 제품에 대한 수요 증가

사료용 아답토젠 시장은 항생제 사용량이 적고 투입물의 투명성이 높은 생산 시스템에서 생산된 육류, 우유, 계란, 수산물을 찾는 구매자들로부터 지지를 얻고 있습니다. 식품 소매업체, 레스토랑 체인, 수입업체들은 공급업체에 항생제를 사용하지 않은 생산 사실을 입증할 것을 요구하고 있으며, 이로 인해 사료 선정은 단순한 농장 차원의 선호 사항으로 취급되지 않고 조달 감사의 대상이 되고 있습니다. 니트라에 위치한 슬로바키아 농업대학교 연구진이 2026년에 발표한 리뷰에 따르면, 식물 유래 사료 첨가물은 가금류, 돼지, 반추동물에서 사료 전환율, 장 건강 및 항산화 상태를 개선하는 것으로 밝혀졌습니다. 이로 인해 일상적인 항생제 사용에서 벗어나려는 생산 시스템에서 허브계 아답토젠의 상업적 가치가 더욱 높아지고 있습니다. 이러한 변화는 북미와 유럽연합(EU)에 그치지 않고, 브라질, 인도, 태국의 수출 지향형 생산자들이 국내 정책만으로는 요구되는 것보다 더 빨리 천연 사료 프로그램을 도입하고 있기 때문에 더 광범위한 영향을 미치고 있습니다. 그 결과, 사료용 아답토젠 시장은 규제가 엄격한 지역뿐만 아니라, 고품질 수출 경로에 대한 접근이 보다 친환경적인 생산을 강조하거나 추적 가능한 사료 관리 관행을 실천하는 데 달려 있는 지역에서도 확대되고 있습니다.

식물성 사료 첨가물에 대한 규제상의 장벽과 복잡한 승인 절차

규제는 여전히 사료용 아답토젠 시장에서 가장 뚜렷한 제약 요인 중 하나입니다. 이는 식물 유래 첨가물이 기존의 많은 사료 원료보다 더 까다로운 승인 절차를 거쳐야 하기 때문입니다. 규정(EC) 제1831/2003호에 따라, 유럽식품안전청(EFSA)은 제품이 심사 단계로 넘어가기 전에 대상 종의 안전성, 소비자의 안전성, 사용자의 안전성 및 환경 안전성을 포괄하는 완전한 자료를 제출할 것을 요구하고 있습니다. 유럽식품안전청(EFSA)은 완전한 신청 서류가 제출되어야 비로소 과학적 평가가 시작된다고 밝혔으며, 추가 자료 요청으로 인해 심사 절차가 최소 기간을 초과하여 길어질 가능성이 있습니다. 이로 인해 상품화가 지연되고, 규정 준수 비용이 증가하게 됩니다. 2025년에 발표된 로즈마리, 라벤더, 페퍼민트, 와일드타임 팅크제에 관한 의견서는 이 과정이 얼마나 상세하게 진행되는지를 보여주고 있으며, 품종별 함유 상한치, 메틸오이게놀에 대한 규제, 그리고 위험 분석 및 중요 관리점(HACCP)에 기반한 품질 요건 등이 포함되어 있습니다.

부문별 분석

2025년에는 허브계 아답토젠이 61.2%라는 최대 시장 점유율을 차지했으며, 이미 확립된 가금류 및 돼지용 사료 프로그램에 적합하기 때문에 사료용 아답토젠 시장에서 확고한 선두 자리를 유지했습니다. 오레가노, 타임, 강황, 아슈와간다, 황기 유래의 에센셜 오일 블렌드, 팅크, 건조 추출물을 활용한 상업적 이용은 오랫동안 정착되어 왔기 때문에 구매자들은 이러한 제품의 취급 방법, 배합 비율 및 기능적 역할에 대해 더 자세히 이해하고 있습니다. 이러한 확고한 기반은 조달망의 확충과, 새로운 기능성 카테고리에 비해 허브 원료에 대한 광범위한 효능 연구 결과가 문서화되어 있다는 점에 힘입어 더욱 공고해지고 있습니다.

버섯 유래 아답토겐을 대상으로 하는 사료용 아답토겐 시장은 2031년까지 연평균 성장률(CAGR) 9.8%로 확대될 것으로 예상되며, 현재 예측 기간 동안 가장 빠르게 성장하는 원료 부문이 될 전망입니다. 사료용 아답토젠 업계에서는 영지(Ganoderma lucidum), 멧버섯(Hericium erinaceus), 동충하초(Cordyceps militaris), 팽이버섯(Agaricus bisporus) 등의 버섯 유래 원료가 가금류 및 반추동물의 사료 분야에서 더욱 견고한 연구 기반을 구축하고 있어, 이에 대한 관심이 높아지고 있습니다. 또한, 사용 후 버섯 배지나 관리된 재배 모델은 일부 야생 채취 식물에 비해 순환형 생산 목표와 더 부합하기 때문에 지속가능성 측면에서도 이 부문이 지지를 받고 있습니다.

2025년에는 분말이 52.3%로 가장 큰 시장 점유율을 차지했습니다. 이는 이 방식이 상업적인 가금류 및 돼지 사육에 사용되는 주류 사료 제조 시스템과 얼마나 밀접하게 부합하는지를 반영하고 있습니다. 드라이 프리믹스나 펠렛 사료의 생산 라인은 이미 분말을 효율적으로 처리할 수 있도록 설계되어 있으므로, 전환 비용을 절감할 수 있고 기존 공정에 쉽게 통합할 수 있습니다. 또한, 많은 식물 추출물과 버섯 다당류는 적절하게 조제되어 있다면 컨디셔닝 및 펠릿화 온도를 견딜 수 있으므로, 분말은 대규모 분쇄 공정에서도 우수한 성능을 발휘합니다.

액상 형태의 사료용 아답토젠 시장 규모는 2031년까지 연평균 성장률(CAGR) 8.5%로 확대될 것으로 예상되며, 집약형 사육 시스템의 확대에 따라 액상 제품이 가장 빠르게 성장하는 부문이 될 전망입니다. 육계나 산란계 사육 현장에서 액체 투여는 매력적인 방법입니다. 이는 음수 시스템을 활용함으로써 균일한 급여가 가능해지며, 열 스트레스나 질병의 위협이 발생했을 때 일반적인 사료 생산 주기보다 훨씬 신속하게 대응할 수 있기 때문입니다. 수용성 아슈와간다 추출물이나 에센셜 오일 에멀전은 농장 관리자가 새로운 사료 배치를 기다릴 필요 없이 투여량을 신속하게 조정할 수 있게 해주기 때문에 이러한 환경에서 그 중요성이 점점 더 커지고 있습니다.

지역별 분석

아시아태평양은 2025년에 35.4%라는 가장 높은 지역 시장 점유율을 차지하며, 사료용 아답토젠 시장의 중심적인 위치를 유지하고 있습니다. 이는 해당 지역이 막대한 가축 사육 규모와 허브 원료에 관한 깊은 전통을 모두 갖추고 있기 때문입니다. 중국은 여전히 주요 견인 역할을 하고 있습니다. 해당 국가에서 항생제 성장 촉진제 사용이 금지됨에 따라, 세계 최대 규모의 축산 시스템 중 하나가 대체 사료 수단으로 전환되었기 때문입니다. 인도는 확대되고 있는 사료 부문과, 현재 산업 규모로 제품 개발을 뒷받침하는 확립된 아유르베다 수의학 실천을 통해 제2의 성장 기반이 되고 있습니다. 일본과 호주는 전체 규모로는 작지만, 양국 모두 고급 수산 사료 분야의 혁신과 생물안전성을 중시하는 배합 기준에 영향을 미치고 있습니다. 따라서 아시아태평양 지역의 사료용 아답토젠 시장은 규모와 품질의 향상이라는 두 가지 요인에 힘입어 성장하고 있으며, 동남아시아의 가금류 및 새우 양식 시스템에서도 사료 사양의 고도화가 진행되고 있습니다.

중동은 가장 빠르게 성장하는 지역 부문이며, 식량 안보 정책이 가축 및 수산 양식의 집약화를 촉진함에 따라 사료용 아답토젠 시장은 2031년까지 연평균 성장률(CAGR) 8.9%로 확대될 것으로 전망됩니다. 사우디아라비아, 아랍에미리트, 튀르키예에서는 정부 주도의 개발 프로그램과 장기 공급 계약을 활용하여, 많은 신흥 지역보다 더 신속하게 가금류 및 수산물 생산에 최신 사료 첨가제를 도입하고 있습니다. 이를 통해 규격 채택 주기가 단축되었으며, 체계적인 조달을 통해 국제적인 공급업체들에게 보다 명확한 시장 진입 기회가 제공되고 있습니다. 아프리카는 여전히 규모가 가장 작은 지역 부문이지만, 남아프리카공화국, 이집트, 나이지리아 각국 정부가 도시 지역의 동물성 단백질 수요 증가에 대응해 가축 생산성 향상에 힘쓰고 있어 장기적인 기회를 내포하고 있습니다.

북미와 유럽은 규제, 대규모 통합형 축산 시스템, 그리고 보다 친환경적인 축산 모델을 선호하는 구매자들의 기호에 힘입어 차세대 주요 수요 시장을 형성하고 있습니다. 미국은 가금류 및 돼지 산업이 이미 대규모 상업 네트워크를 통해 운영되고 있으며, 검증된 비항생제 첨가제를 신속하게 도입할 수 있기 때문에 북미 수요를 주도하고 있습니다. 사료용 아답토젠 시장에서 유럽은 다른 어느 지역보다 규제가 엄격한 상황이 계속되고 있습니다. 이는 식물 유래 첨가물이 엄격한 승인 절차를 거쳐야 하기 때문이며, 이로 인해 제품 출시 시기는 늦어지지만 승인된 제품에 대한 신뢰도는 높아집니다. 독일, 프랑스, 영국이 유럽의 주요 수요 거점으로 자리 잡고 있으며, 이들 국가에서는 소매업체의 조달 기준과 지속가능성 관련 요건이 첨가제 선정에 영향을 미치고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the feed adaptogens market size is projected to increase from USD 1.80 billion in 2025 to USD 1.97 billion in 2026 and reach USD 3.10 billion by 2031, growing at a CAGR of 9.50% over 2026-2031.

This report is Segmented by Source (Herbal Adaptogens, and Mushroom Adaptogens), by Form (Powder, Liquid, and Encapsulated and Beadlet), by Livestock (Poultry, Swine, Ruminants, Aquaculture, and Pets ), by Function (Stress Mitigation, Immune Enhancement, and Feed Conversion), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Feed Adaptogens Market Trends and Insights

Ban on Antibiotics as Growth Promoters

The ban on antibiotic growth promoters has become the clearest structural support for the feed adaptogens market, as it removed the most established, low-cost growth tool from several major livestock economies. The United States ended the production and use of medically important antimicrobials, China eliminated antibiotic growth promoters, and Canada removed growth-promotion claims from antimicrobial labels, thereby shifting procurement toward non-antibiotic feed solutions. The feed adaptogens market is also benefiting from export pressure in middle-income producer countries, where antibiotic use remains more flexible, as exporters increasingly need to comply with buyer requirements in destination markets.

Rising Demand for Natural and Herbal Livestock Products

The feed adaptogens market is gaining support from buyers seeking meat, milk, eggs, and seafood from systems with lower antibiotic use and greater input transparency. Food retailers, restaurant chains, and importers are asking suppliers to document antibiotic-free production, which brings feed decisions into procurement audits rather than leaving them as farm-level preferences. A 2026 review published by researchers of the Slovak University of Agriculture in Nitra found that phytogenic feed additives improved feed conversion ratio, intestinal integrity, and antioxidant status across poultry, swine, and ruminants, strengthening the commercial case for herbal adaptogens in production systems seeking to move away from routine antibiotic support. This change matters beyond North America and the European Union because export-oriented producers in Brazil, India, and Thailand are adopting natural feed programs earlier than local policy alone would require. As a result, the feed adaptogens market is expanding not only in regions with strict regulation but also in those where access to premium export channels depends on cleaner production claims and traceable feed practices.

Regulatory Barriers and Complex Approval Processes for Botanical Feed Additives

Regulation remains one of the clearest limits on the feed adaptogens market because botanical additives face a more detailed approval process than many conventional feed inputs. Under Regulation (EC) No. 1831/2003, the European Food Safety Authority requires complete dossiers that cover target species safety, consumer safety, user safety, and environmental safety before a product can move through review. The European Food Safety Authority states that scientific assessment begins only after a complete submission, and additional data requests can lengthen the process beyond the minimum review window, which delays commercialization and increases compliance expense. Its 2025 opinions on rosemary, lavender, peppermint, and wild thyme tinctures show how specific this process can become, including species-based inclusion limits, methyleugenol controls, and hazard analysis and critical control point quality expectations.

Other drivers and restraints analyzed in the detailed report include:

- Heat-Stress Management in Commercial Livestock

- Rapid Growth of Global Aquaculture Sector

- Mycotoxin Contamination Risk in Botanical Raw Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Herbal adaptogens held the largest market share at 61.2% in 2025, keeping them firmly ahead in the feed adaptogens market because they already fit established poultry and swine feed programs. Commercial use has been built over many years around essential oil blends, tinctures, and dry extracts from oregano, thyme, turmeric, ashwagandha, and astragalus, so buyers are more familiar with their handling, inclusion rates, and performance role. This established base is reinforced by sourcing depth and by the wider set of documented efficacy studies available for herbal materials than for newer functional categories.

The feed adaptogens market for mushroom adaptogens is projected to expand at a 9.8% CAGR through 2031, making them the fastest-growing source segment in the current forecast period. The feed adaptogens industry is giving mushroom-derived inputs more attention because species such as Ganoderma lucidum, Hericium erinaceus, Cordyceps militaris, and Agaricus bisporus now have a stronger research base across poultry and ruminant diets. Sustainability also supports this segment, as spent mushroom substrate and controlled cultivation models better align with circular production goals than some wild-harvested botanicals.

Powder accounted for the largest market share at 52.3% in 2025, reflecting how closely this format aligns with the dominant feed manufacturing systems used in commercial poultry and swine production. Dry premixes and pelleted feed lines are already designed to handle powders efficiently, which lowers changeover costs and keeps the format easy to integrate into existing routines. Powder also performs well in large-scale milling because many botanical extracts and mushroom polysaccharides can tolerate conditioning and pelleting temperatures when properly prepared.

The feed adaptogens market size for liquid formats is projected to grow at an 8.5% CAGR through 2031, making liquid the fastest-growing segment as intensive housing systems expand. Liquid delivery is attractive in broiler and layer operations because drinking water systems allow uniform dosing and a much faster response during heat stress events or disease pressure than a normal feed production cycle can provide. Water-soluble ashwagandha extracts and essential oil emulsions are becoming more relevant in these settings because farm managers can change dose levels quickly without waiting for a new feed batch.

Geography Analysis

Asia-Pacific held the largest regional market share at 35.4% in 2025, keeping it at the center of the feed adaptogens market, as the region combines large livestock volumes with deep herbal raw material traditions. China remains the main anchor because its ban on antibiotic growth promoters shifted one of the world's largest animal production systems toward alternative feed tools. India adds a second growth base through its expanding compound feed sector and through established Ayurvedic veterinary practice that now supports more industrial-scale product development. Japan and Australia are smaller in total volume, but both influence premium aquafeed innovation and biosecurity-led formulation standards. The feed adaptogens market in Asia-Pacific is therefore driven by both scale and quality progression, with Southeast Asian poultry and shrimp systems also upgrading feed specifications.

The Middle East is the fastest regional segment, with the feed adaptogens market projected to expand at an 8.9% CAGR through 2031 as food security policies drive livestock and aquaculture intensification. Saudi Arabia, the United Arab Emirates, and Turkey are using state-backed development programs and long-term supply arrangements to bring modern feed additives into poultry and fish production faster than many emerging regions. That shortens the standard adoption cycle and provides international suppliers with clearer entry points through organized procurement. Africa remains the smallest regional segment, but it offers a longer-term opportunity, as governments in South Africa, Egypt, and Nigeria work to boost livestock productivity amid rising urban demand for animal protein.

North America and Europe formed the next major demand bloc, supported by regulation, large integrated livestock systems, and buyer preference for cleaner animal production models. The United States leads North American demand because its poultry and swine industries already operate through large commercial networks that can quickly absorb validated non-antibiotic additives. Europe remains more regulated than any other region in the feed adaptogens market, since botanical additives must pass a strict authorization process that slows launches but raises confidence in approved products. Germany, France, and the United Kingdom are the main European demand centers, where retailer sourcing standards and sustainability requirements influence additive selection.

- Cargill, Incorporated

- DSM-Firmenich AG

- Archer Daniels Midland Company

- Alltech, Inc.

- Kemin Industries, Inc.

- Trouw Nutrition International B.V. (Nutreco N.V.)

- Novus International, Inc.

- Phytobiotics Futterzusatzstoffe GmbH

- EW Nutrition GmbH

- Nutrex N.V.

- Ayurvet Limited

- Indian Herbs Specialities Private Limited

- Natural Remedies Private Limited

- Zinpro Corporation

- Phytoline GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ban on antibiotics as growth promoters

- 4.2.2 Rising demand for natural and herbal livestock products

- 4.2.3 Heat-stress management in commercial livestock

- 4.2.4 Rapid growth of global aquaculture sector

- 4.2.5 Feed-cost optimization through adaptogen supplementation

- 4.2.6 Adoption of precision livestock farming practices

- 4.3 Market Restraints

- 4.3.1 Regulatory barriers and complex approval processes for botanical feed additives

- 4.3.2 Mycotoxin contamination risk in botanical raw materials

- 4.3.3 Volatile scalability of herbal adaptogen production

- 4.3.4 Limited supply and price volatility of botanical raw materials

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Source

- 5.1.1 Herbal Adaptogens

- 5.1.2 Mushroom Adaptogens

- 5.2 By Form

- 5.2.1 Powder

- 5.2.2 Liquid

- 5.2.3 Encapsulated and Beadlet

- 5.3 By Livestock Species

- 5.3.1 Poultry

- 5.3.2 Swine

- 5.3.3 Ruminants

- 5.3.4 Aquaculture

- 5.3.5 Pets

- 5.4 By Function

- 5.4.1 Stress Mitigation

- 5.4.2 Immune Enhancement

- 5.4.3 Feed Conversion Improvement

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Cargill, Incorporated

- 6.4.2 DSM-Firmenich AG

- 6.4.3 Archer Daniels Midland Company

- 6.4.4 Alltech, Inc.

- 6.4.5 Kemin Industries, Inc.

- 6.4.6 Trouw Nutrition International B.V. (Nutreco N.V.)

- 6.4.7 Novus International, Inc.

- 6.4.8 Phytobiotics Futterzusatzstoffe GmbH

- 6.4.9 EW Nutrition GmbH

- 6.4.10 Nutrex N.V.

- 6.4.11 Ayurvet Limited

- 6.4.12 Indian Herbs Specialities Private Limited

- 6.4.13 Natural Remedies Private Limited

- 6.4.14 Zinpro Corporation

- 6.4.15 Phytoline GmbH