|

시장보고서

상품코드

2065722

미국의 치과 치료 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Dental Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

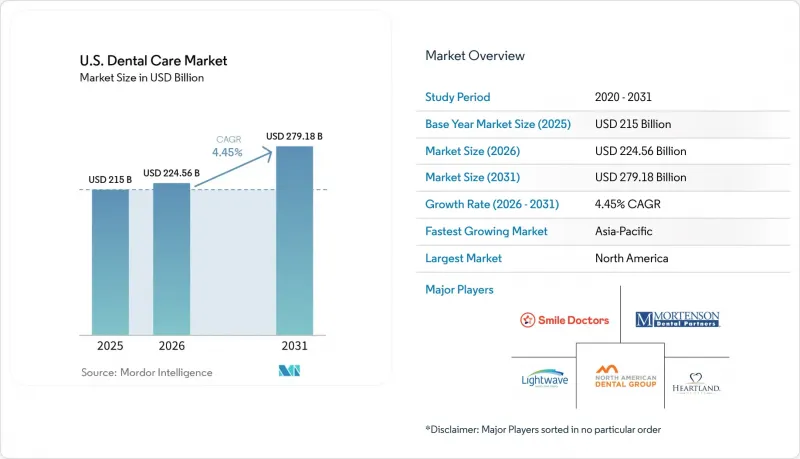

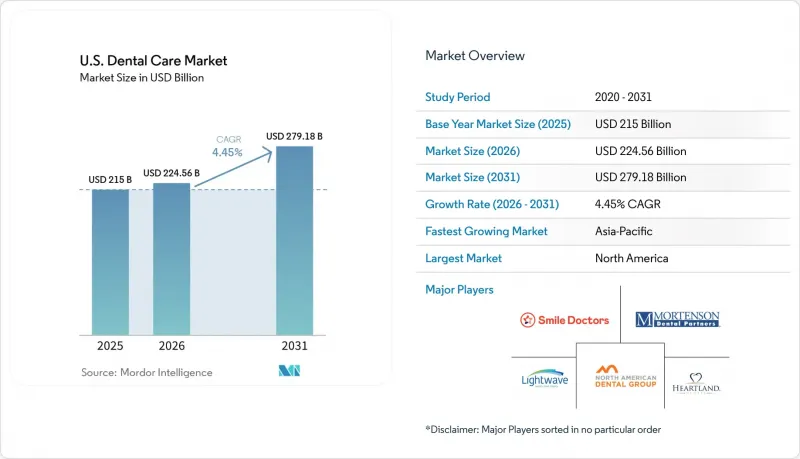

Mordor Intelligence에 의하면, 미국의 치과 치료 시장 규모는 2025년 2,150억 달러로 평가되었고, 2026년 2,245억 6,000만 달러로 추정되고, 2031년까지 2,791억 8,000만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 4.45%를 나타낼 전망입니다.

본 보고서는 서비스 유형별(비수술적 서비스, 수술적 서비스), 환자 연령대별(0-17세, 18-34세, 35-64세, 65세 이상) 및 진료 시설별(치과, 병원, 치과 서비스 기관, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 치과 의료 시장 동향 및 인사이트

메디케어 어드밴티지의 치과 혜택 확대가 고령자의 이용을 촉진

2025년, 메디케어 어드밴티지 가입자 수는 3,410만 명에 달했으며, 이는 메디케어 대상 인구의 54%를 차지하여 전년 대비 4% 증가한 수치입니다. 예측에 따르면, 이 비율은 2034년까지 64%까지 확대될 가능성이 있으며, 이는 고령자 대상 치과 보험 적용 범위가 계속해서 확대될 것임을 시사합니다. 2025년에는 메디케어 어드밴티지 플랜의 97% 이상이 치과 혜택을 포함하고 있었으며, 보충적인 치과 혜택도 널리 이용 가능했습니다. 스페셜 니즈 플랜 가입자 수가 71% 증가하면서 수복 치료, 치주 치료 및 전문 치료에 대한 수요를 견인한 결과, 고령 환자 1인당 수익이 증가했습니다.

성인 대상 메디케이드 치과 혜택 확대가 대상 인구를 늘리고 있습니다.

2024년 말까지 11개 주와 워싱턴 D.C.가 메디케이드 제도 하에서 성인을 대상으로 광범위한 치과 혜택을 제공하게 되었습니다. 이는 2020년의 4개 주에서 증가한 수치입니다. 최근 변경 사항에 따라 서비스 대상 범위가 확대되고, 연간 지급 한도액이 인상되었으며, 특정 성인층이 대상에 포함되었습니다. 이로 인해 환자 기반이 확대되어, 더 많은 저소득 성인들이 치과 진료를 받을 수 있게 되었습니다. 대규모 그룹이나 DSO(치과 서비스 조직)가 지원하는 진료소는 보수액 감소나 환자 수 증가에 대응하기 쉬운 입장에 있기 때문에 이러한 확장의 주요 수혜자가 되고 있습니다.

중요한 성장의 전환점에서 치과위생사 및 보조 인력의 부족이 진료 역량을 제약하고 있습니다.

미국의 치과 의료 시장은 치과 위생사 및 보조 인력의 부족으로 인해 보험 가입자 수요를 예약으로 전환하는 데 제약을 받고 있으며, 진료 능력에 한계를 겪고 있습니다. 2025년에는 치과의사의 74%가 치과위생사 채용에 극심한 어려움을 겪고 있다고 보고했으며, 57.2%의 자리가 공석인 상태였습니다. 연수 프로그램의 진료 공간 제한으로 인해 2037년까지 3만 명의 치과위생사가 부족할 것으로 예상되며, 이 문제가 더욱 심각해지고 있습니다. 이러한 인력 부족으로 인해 진료 역량이 11% 저하되어 대기 시간 증가, 일일 환자 진료 건수 감소, 치료 지연 등의 문제가 발생하고 있습니다. 급여, 업무량, 업무 범위 제한 등이 영향을 미치는 인재 유지를 둘러싼 과제는 이 문제를 해결하는 데 있어 여전히 중대한 장벽으로 남아 있습니다.

부문별 분석

2025년, 비수술적 서비스는 미국 치과 의료 시장 점유율의 55.46%를 차지했으며, 이는 모든 연령대에서 반복적으로 이루어지는 치아 세정 및 검진 등의 예방 치료가 주도하고 있습니다. 고용주가 제공하는 치과 보험은 예방 및 수복 치료에 대해 폭넓은 보장을 제공함으로써 이 부문을 뒷받침하고, 정기적인 이용을 안정적으로 유지하고 있습니다. 충전, 크라운, 브릿지 등의 수복 서비스 외에도, 미백이나 베니어와 같은 심미 치과 옵션도 수요와 수익 잠재력을 더욱 높여주고 있습니다.

외과적 시술 시장은 2026-2031년 연평균 성장률(CAGR) 6.15%를 나타낼 것으로 예측되며, 이는 서비스 유형 중 가장 높은 성장률입니다. 임플란트의 보급이 주요 촉진요인으로 작용하고 있으며, 고령 환자의 치아 결손 보철 수요와 젊은 층의 심미성을 중시하는 치료에 대한 수요 모두를 충족시키고 있습니다. 교정치과는 사춘기 환자층에 그치지 않고, 직장인 등 성인층으로까지 확대되고 있습니다. 한편, 근관 치료 및 치주질환 치료의 발전으로 청구 가능한 시술이 늘어나면서, 시장은 수익성이 높은 전문 시술로 전환되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the u.S. dental care market size is projected to expand from USD 215 billion in 2025 and USD 224.56 billion in 2026 to USD 279.18 billion by 2031, registering a CAGR of 4.45% between 2026 to 2031.

This report is Segmented by Service Type (Non-Surgical Services, Surgical Services), Patient Age Group (0-17 Years, 18-34 Years, 35-64 Years, 65 Years and Above), and Care Setting (Dental Clinics, Hospital, Dental Service Organization, Others). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Dental Care Market Trends and Insights

Medicare Advantage Dental Benefit Expansion Fueling Senior Utilization

In 2025, Medicare Advantage enrollment reached 34.1 million, representing 54% of the eligible Medicare population, a 4% increase from the previous year. Projections indicate this share could grow to 64% by 2034, signaling continued expansion of senior dental coverage. Over 97% of Medicare Advantage plans included dental benefits in 2025, with supplemental dental benefits also widely available. Special Needs Plans saw a 71% enrollment increase, driving demand for restorative, periodontal, and specialty procedures, resulting in higher revenue per senior patient.

Adult Medicaid Dental Benefit Expansion Broadening the Addressable Population

By the end of 2024, 11 states and Washington, D.C., offered extensive adult dental benefits under Medicaid, up from 4 states in 2020. Recent changes expanded service coverage, raised annual benefit limits, and targeted specific adult groups. This broadened the patient base, enabling more low-income adults to access dental care. Larger groups and DSO-backed practices are better positioned to manage lower reimbursements and higher volumes, making them key beneficiaries of this expansion.

Hygienist And Assistant Shortages Constraining Capacity At A Critical Growth Inflection

The U.S. dental care market faces capacity constraints as shortages of hygienists and assistants limit the conversion of insured demand into appointments. In 2025, 74% of dentists reported extreme difficulty in recruiting hygienists, with 57.2% of positions unfilled. A projected shortfall of 30,000 hygienists by 2037, driven by limited clinic space in training programs, further exacerbates the issue. These shortages have reduced practice capacity by 11%, increasing wait times, lowering visit throughput, and causing delays in treatment. Retention challenges, influenced by pay, workload, and scope-of-practice limits, remain a critical barrier to resolving this issue.

Other drivers and restraints analyzed in the detailed report include:

- DSO Consolidation And Specialty Rollout

- Cosmetic, Clear-Aligner, And Implant Demand Elevating Revenue Per Visit

- Out-Of-Pocket Burden And Annual Benefit Caps Suppressing Discretionary Demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, non-surgical services accounted for 55.46% of the U.S. dental care market share, driven by preventive care such as cleanings and exams, which are repeatable across all age groups. Employer-sponsored dental insurance supports this category by offering broad reimbursements for preventive and restorative procedures, stabilizing routine utilization. Restorative services like fillings, crowns, and bridges, along with cosmetic dentistry options such as whitening and veneers, further enhance demand and revenue potential.

Surgical services are projected to grow at a 6.15% CAGR from 2026 to 2031, the fastest among service types. Implant adoption is a key driver, addressing both aging patients' tooth replacement needs and younger adults' demand for appearance-driven treatments. Orthodontics is expanding beyond adolescents to working adults, while advancements in endodontics and periodontics are increasing billable interventions, shifting the market toward higher-revenue specialty procedures.

List of Companies Covered in this Report:

- 42 North Dental

- Affordable Care, LLC

- Benevis

- Dental Care Alliance

- Freedom Dental Health

- Great Expressions Dental Centers

- Heartland Dental

- InterDent

- Lightwave Dental Management LLC

- MAX Surgical Specialty Management

- MB2 Dental

- Mortenson Dental Partners

- North American Dental Group

- Parkview Dental Partners

- PDS Health

- Smile Brands

- Smile Doctors

- Sonrava Health

- Specialized Dental Partners

- The Aspen Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Medicare Advantage Dental Benefit Expansion

- 4.2.2 Adult Medicaid Dental Benefit Expansion and EHB Pathway

- 4.2.3 DSO Consolidation and Specialty Rollout

- 4.2.4 Cosmetic, Clear-Aligner, and Implant Demand

- 4.2.5 AI Diagnostics and Dental-Medical Integration

- 4.3 Market Restraints

- 4.3.1 Hygienist and Assistant Shortages

- 4.3.2 Out-of-Pocket Burden and Annual Benefit Caps

- 4.3.3 Low Medicaid Reimbursement and Administrative Friction

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining power of suppliers

- 4.7.2 Bargaining power of buyers

- 4.7.3 Threat of new entrants

- 4.7.4 Threat of substitutes

- 4.7.5 Intensity of competitive rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Non-surgical Services

- 5.1.1.1 Preventive Dentistry

- 5.1.1.2 Restorative Dentistry

- 5.1.1.3 Cosmetic Dentistry

- 5.1.2 Surgical Services

- 5.1.2.1 Implants & Oral Surgery

- 5.1.2.2 Orthodontics

- 5.1.2.3 Endodontics & Periodontics

- 5.1.1 Non-surgical Services

- 5.2 By Patient Age Group

- 5.2.1 0-17 years

- 5.2.2 18-34 years

- 5.2.3 35-64 years

- 5.2.4 65 years and above

- 5.3 By Care Setting

- 5.3.1 Dental Clinics

- 5.3.2 Hospital

- 5.3.3 Dental Service Organization

- 5.3.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 42 North Dental

- 6.3.2 Affordable Care, LLC

- 6.3.3 Benevis

- 6.3.4 Dental Care Alliance

- 6.3.5 Freedom Dental Health

- 6.3.6 Great Expressions Dental Centers

- 6.3.7 Heartland Dental

- 6.3.8 InterDent

- 6.3.9 Lightwave Dental Management LLC

- 6.3.10 MAX Surgical Specialty Management

- 6.3.11 MB2 Dental

- 6.3.12 Mortenson Dental Partners

- 6.3.13 North American Dental Group

- 6.3.14 Parkview Dental Partners

- 6.3.15 PDS Health

- 6.3.16 Smile Brands

- 6.3.17 Smile Doctors

- 6.3.18 Sonrava Health

- 6.3.19 Specialized Dental Partners

- 6.3.20 The Aspen Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment