|

시장보고서

상품코드

2065739

자동차용 레이더 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Automotive Radar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

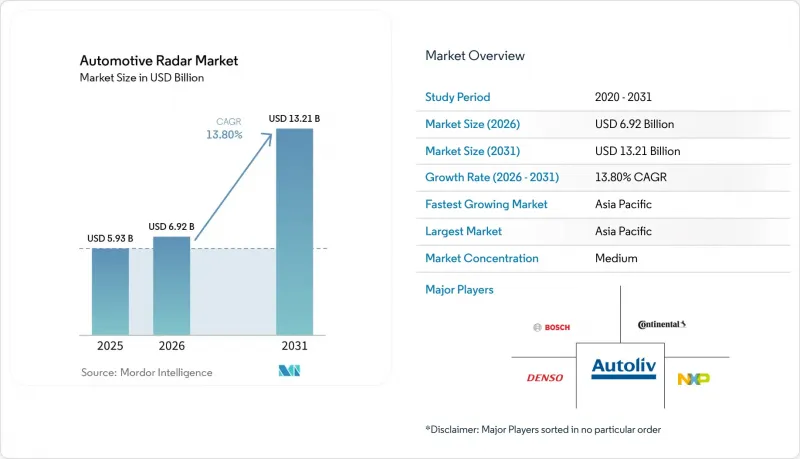

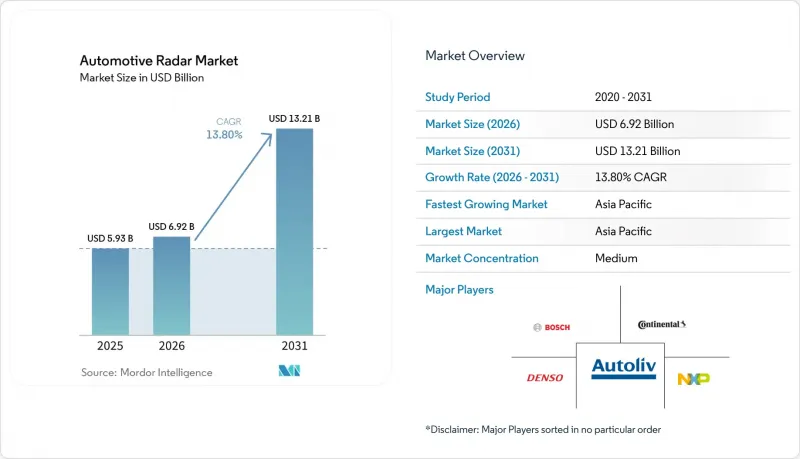

Mordor Intelligence에 의하면, 자동차용 레이더 시장 규모는 2025년 59억 3,000만 달러로 평가되었고, 2026년에는 69억 2,000만 달러로 추정되고, 2026-2031년 CAGR 13.8%로 성장을 지속할 전망이며, 2031년에는 132억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 감지 거리별(단거리, 중거리, 장거리), 주파수 대역별(24GHz, 77GHz, 기타), 용도별(어댑티브 크루즈 컨트롤, 자율주행 등), 차종별(승용차, 소형 상용차 등), 구동 방식별(내연기관 차량 등), 판매 채널별(OEM 순정 장비 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 자동차용 레이더 시장 동향 및 분석

엄격한 NCAP 및 UNECE 안전 기준

Euro NCAP의 2025년 평가 기준에 따르면, 차량 내 어린이 감지 및 전방 충돌 완화 기능이 의무화되어 있으며, 5성급 평가를 받기 위해서는 레이더 탑재가 필수입니다. 유럽연합 규정 2019/2206은 2024년 9월부터 모든 신형 차량으로 이 요건을 확대 적용하고 있으며, 이는 차량 조달 결정 및 보험료 산정에 직접적인 영향을 미치고 있습니다. 중국 공업정보화부는 2028년을 목표로 자동 긴급 제동 시스템의 의무화를 발표했으며, 국내 브랜드들이 센서를 선제적으로 탑재함에 따라 77GHz 대역에 대한 대량 수주가 예상됩니다. 유럽, 북미, 아시아·태평양 지역별 도입 속도의 차이로 인해 수요가 단계적으로 발생하고 있으며, 이에 따라 자동차용 레이더 시장은 주기적인 침체를 피할 수 있을 것으로 보입니다. 따라서 Tier 1 공급업체들은 OEM으로부터의 직접 인도를 기다리기보다는 규제 발효를 예상하여 전단 재고를 늘리고 있습니다.

77GHz 대역에서 비용 중심의 소형화 추세

24GHz에서 77GHz로 전환함에 따라 모듈의 실적가 약 60% 감소했으며, 감지 범위는 250m로 2배 확대되었습니다. 이를 통해 디자인상의 타협 없이 센서를 범퍼 페시아 뒤쪽에 숨길 수 있게 되었습니다. 텍사스 기기가 2025년 출시 예정인 AWR2944P는 하드웨어 가속기와 확장 메모리를 통합하여, 디스크리트 DSP와 마이크로컨트롤러를 하나의 다이에 집약하고 있습니다. NXP의 S32R47은 192개의 소자로 구성된 가상 어레이를 지원하며, 양산 수준의 비용으로 4D 포인트 클라우드를 구현합니다. 웨이퍼 스케일 집적, 실리콘 게르마늄 공정 및 칩렛 분할에 힘입어 평균 판매 가격은 2024년 85달러에서 2025년에는 72달러로 하락할 것으로 예상되며, 중국 팹의 생산량이 확대됨에 따라 2028년까지 55달러에 도달할 것으로 전망됩니다. 가격 하락으로 인해 보급형 트림에서도 프리미엄 레이더 기능을 이용할 수 있게 되면서, 센서 수 증가가 가속화되어 자동차용 레이더 시장 전체 수요를 견인하게 될 것입니다.

고비용의 다중 센서 융합 시스템

100 TOPS 이상의 인공지능 처리 능력을 갖춘 집중형 지각 스택은 대당 800-1,200달러의 비용 증가를 초래하며, 이는 대중차 브랜드가 쉽게 감당할 수 있는 금액이 아닙니다. 이러한 시스템의 기반이 되는 Nvidia Thor의 수냉식 컴퓨팅 모듈은 패키징 및 열 경로 설계 변경을 불가피하게 만들며, 특히 가격에 민감한 아시아태평양의 제품 등급에서 부품 원가(BOM)에 대한 부담을 가중시키고 있습니다. 중국공급업체는 유럽 및 미국의 동종 업체에 비해 40-50% 저렴한 가격으로 컴퓨팅 모듈을 생산하고 있지만, 단기적인 비용 부담으로 인해 보급형 모델의 레이더 옵션 기능이 제한되고 있으며, 당분간 판매 가능한 대수에도 상한선이 설정되어 있습니다. Tier 1 공급업체들은 개별 모듈을 판매할지, 아니면 센서 퓨전의 완전한 통합을 맡을지 선택해야 하는 상황에 직면해 있으며, 이러한 상충 관계는 이익률 유지와 자동차용 레이더 시장의 수익성에 영향을 미치고 있습니다. 향후 10년이 끝날 무렵에는 5nm 공정 노드와 치플렛 가속기를 통해 연산 비용이 절반으로 줄어들 것으로 예상되지만, 2026년부터 2028년에 걸친 기간 동안에는 여전히 대규모 도입의 걸림돌이 될 것입니다.

부문별 분석

단거리 레이더는 2025년 매출의 44.64%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 13.92%로 성장할 것으로 전망됩니다. 중거리 장치는 횡방향 교통 감지 및 교차로 감시를 지원하는 한편, 장거리 장치는 여전히 어댑티브 크루즈 컨트롤의 기반이 되고 있으나, 중국의 생산 능력 확대로 인한 가격 압박에 직면해 있습니다.

현재 코너 설치형 센서는 넓은 커버리지와 90m의 감지 거리를 모두 갖추고 있어, 하나의 센서로 주차, 사각지대 감지, 차선 변경 등의 각 작업을 처리할 수 있습니다. 60GHz 대역의 탑승자 감지 모듈은 새로운 초단거리 분야를 형성하고 있으며, Euro NCAP의 차량 내 안전 기준이 보급됨에 따라 급속히 확대될 전망입니다. 실리콘-게르마늄 기반 프런트엔드의 비용 절감 덕분에, 자동차 제조업체들은 트림 등급의 가격 목표를 벗어나지 않으면서도 4-6개의 단거리 유닛을 탑재할 수 있게 되었습니다. 주차, 사각지대 감지, 후방 횡단 차량 감지 기능에 걸친 수요의 통합으로 인해, 2031년까지 단거리 레이더의 안정적인 성장 궤도가 확보되어 있습니다.

77GHz 대역은 2025년 매출의 62.77%를 차지했으나, 2031년까지 79GHz 이미징 솔루션이 연평균 성장률(CAGR) 13.86%로 부상함에 따라 그 성장세는 둔화될 것입니다. 규제 당국은 24GHz 대역에 대한 신규 승인을 동결하고 있으며, 이로 인해 구형 장비는 점차 구식이 되어가고, 공급업체들의 77GHz 및 79GHz 대역에 대한 로드맵이 더욱 엄격해지고 있습니다.

Tier 1 공급업체는 딥러닝 가속 기능을 탑재한 77-81GHz 시스템 온 칩(SoC)을 발표하며, 기존 안테나 설계에서 더 높은 각도 분해능을 이끌어내고 있습니다. 프리미엄 차량 및 배터리 전기자동차(BEV) 플랫폼에서는 고해상도 포인트 클라우드 데이터를 구현하기 위해 4GHz의 스윕 대역폭을 확보하는 79GHz가 채택되고 있지만, 비용 절감을 위해 대중 시장용 모델에서는 여전히 77GHz가 사용되고 있습니다. 교통량이 많은 구간에서 주파수 공유로 인한 과제는 엔지니어링상의 부담을 가중시키고 있지만, 독자적인 간섭 제거 스택을 통해 성능은 Euro NCAP의 허용 범위 내에 유지되고 있습니다. 듀얼 밴드 로드맵을 통해 자동차 제조업체는 투자를 단계적으로 진행함으로써 77GHz 생산 라인의 잔존 금형 가치를 보호할 수 있습니다.

지역별 분석

아시아태평양은 2025년 자동차용 레이더 시장 매출의 38.48%를 차지했고, 2031년까지 연평균 성장률(CAGR) 14.53%를 기록할 전망이며, 이 지역은 가장 빠르게 성장하는 수요의 중심지로 자리매김하고 있습니다. 중국이 이러한 확장의 주도적인 역할을 하고 있습니다. Cheng-Tech 및 Huawei와 같은 국내 공급업체들은 2028년 자동 긴급 제동(AEB) 의무화에 대비하기 위해 77GHz 및 79GHz 모듈의 생산을 확대하고 있는 반면, OEM 업체들은 유럽 및 북미의 경쟁사들과 기능 면에서 대등한 경쟁력을 유지하기 위해 중급 트림에 6개 센서 세트를 기본 사양으로 탑재하고 있습니다. 일본과 한국에서는 고급차에 레이더가 널리 채택되고 있어, 덴소, 히타치 아스테모, 닛폰덴산 에레시스를 통해 모듈을 대량으로 수출하고 있지만, 국내 시장이 포화 상태에 가까워짐에 따라 성장세가 둔화되고 있습니다. 인도의 레이더 보급률은 2025년 기준 여전히 10% 미만이지만, 도로운송·고속도로부가 2027-2028년 자동 긴급 제동 시스템 도입 일정을 검토하고 있어, 예측 기간 후반에는 지역 출하량을 끌어올릴 잠재적인 성장 여지가 생겨나고 있습니다. 동남아시아 시장에서는 규제 시행이 지연되고 있지만, 태국, 인도네시아, 베트남에서는 사각지대 감지 시스템의 사후 장착에 대한 보험료 할인이 애프터마켓 수요를 촉진하고 있습니다. 호주 및 뉴질랜드에서는 장거리 고속도로의 안전 요건에 따라 장거리 주행에 대응할 수 있는 어댑티브 크루즈 컨트롤 모듈이 중요시되고 있기 때문에 레이더 탑재율은 서유럽과 비슷한 수준을 유지하고 있습니다. 아시아태평양 전체적으로 볼 때, 규모의 경제에 따른 이점이 평균 판매 가격 하락으로 이어지고 있어, 출하 대수가 증가하는 상황에서도 자동차용 레이더 시장은 이익률을 유지하고 있습니다.

2025년, 유럽은 전 세계 매출의 약 28%를 차지했습니다. 이는 5성급 평가를 목표로 하는 차량에 대해 전방 충돌, 사각지대, 차량 내 어린이 감지용 레이더의 탑재를 의무화하는 엄격한 Euro NCAP 평가 기준에 기반을 둔 것입니다. 프리미엄 브랜드들은 인식 정확도를 통해 차별화를 꾀하기 위해 79GHz 대역의 4D 이미징 솔루션을 도입하고 있지만, 양산 제조업체들은 여전히 규제 준수를 위해 비용이 최적화된 77GHz 대역의 코너 센서에 의존하고 있습니다. 콘티넨탈사의 누적 생산 대수 2억 대라는 이정표와 2025년 레이더 수주액 15억 유로(17억 달러)는 유럽이 1차 공급업체에게 설계 검증의 거점인 동시에 대량 생산의 기반으로서도 역할을 하고 있음을 보여줍니다. 동유럽의 위탁 조립 제조업체들은 물류 리스크를 억제하기 위해 니어쇼어링 전략을 채택한 독일, 프랑스, 이탈리아의 OEM 제조업체들 수요에 대응하기 위해 모듈 생산량을 확대되고 있습니다. 27개 회원국의 규제를 조화시킴으로써 수요의 균일성이 보장되고 있지만, 프랑크푸르트나 파리 등 교통량이 많은 구간에서는 79GHz 부근의 주파수 대역이 혼잡하여 간섭을 줄이기 위한 투자가 필요하게 되고, 이로 인해 시스템 전체의 비용이 상승하고 있습니다. 2026년에는 배터리식 전기차(BEV)의 등록 대수가 신차 판매량의 30%를 넘어설 것으로 예상되며, 유럽의 BEV 플랫폼에는 평균 5-6개의 센서가 탑재되기 때문에 내연기관 차량의 판매 대수가 감소하더라도 성장은 지속될 전망입니다. 따라서 유럽은 계속해서 소프트웨어 정의 레이더의 업데이트 및 무선 기술을 통한 성능 향상의 주요 시장으로 자리매김하고 있습니다.

북미는 2025년 매출의 약 24%를 차지했으며, 이러한 성장세는 미국 도로교통안전국(NHTSA)의 자동 긴급 제동(AEB) 의무화 및 제너럴 모터스의 ‘울트라 크루즈’와 포드의 ‘블루 크루즈’와 같은 핸즈프리 고속도로 주행 지원 시스템의 상용화에 힘입고 있습니다. 픽업 트럭이나 풀사이즈 SUV에는 트레일러 견인 지원 및 차선 중앙 유지 기능을 위해 3-4개의 장거리 센서가 탑재되어 있어, 소형 승용차에 비해 출하 대수는 적지만 차량 1대당 부품 가치를 높이고 있습니다. 캐나다는 미국의 규제를 따르고 있지만, 멕시코는 미국 수출용 레이더 탑재 차량의 수출 지향형 조립에 주력하고 있습니다. 남미, 중동 및 아프리카를 합친 2025년 매출액은 10% 미만에 그쳤습니다. 레이더 도입은 듀티 사이클 단축 및 보험료 절감을 통해 초기 하드웨어 비용을 상쇄할 수 있는 차량 함대 및 상용 부문에 집중되고 있습니다. 브라질과 사우디아라비아 정부의 안전 대책 프로그램 덕분에 2027년 이후에는 보급이 가속화될 가능성이 있지만, 규격의 불일치와 공급업체의 거점이 제한적이라는 점이 단기적인 판매량 증가를 억제하고 있습니다. 전반적으로, 지리적 분산 덕분에 자동차용 레이더 시장 규모는 지역별 정책 변동에 따른 영향을 완화하며, 성숙 시장과 신흥 시장 간의 성장 균형을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the automotive radar market size is expected to grow from USD 5.93 billion in 2025 to USD 6.92 billion in 2026 and is forecast to reach USD 13.21 billion by 2031 at a 13.8% CAGR over 2026-2031.

This report is Segmented by Range (Short-Range, Mid-Range, and Long-Range), Frequency Band (24 GHz, 77 GHz, and More), Application (Adaptive Cruise Control, Autonomous Driving, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Propulsion (Internal Combustion Vehicles, and More), Sales Channel (OEM-Fitted, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive Radar Market Trends and Insights

Stringent NCAP and UNECE Safety Mandates

Euro NCAP's 2025 protocol forces in-cabin child-presence detection and forward-collision mitigation, making radar mandatory for five-star ratings. The European Union Regulation 2019/2206 extends the requirement across all new vehicle types from September 2024, directly influencing fleet-procurement decisions and insurance pricing. China's Ministry of Industry and Information Technology has announced automatic emergency braking mandates for 2028, creating a pipeline of high-volume 77 GHz orders as domestic brands pre-load sensors. Differences in rollout cadence between Europe, North America and Asia-Pacific stage demand in sequential waves, helping the automotive radar market avoid cyclical slumps. Tier-1 suppliers are therefore stockpiling front-end inventory in anticipation of mandate triggers, rather than awaiting direct pull from original equipment manufacturers.

77 GHz Cost-Driven Miniaturisation Wave

Migrating from 24 GHz to 77 GHz has cut module footprints by around 60% and doubled detection range to 250 m, allowing sensors to hide behind bumper fascias without stylistic compromise. Texas Instruments' 2025 AWR2944P integrates a hardware accelerator and expanded memory, collapsing discrete DSPs and microcontrollers into one die. NXP's S32R47 adds support for 192-element virtual arrays that enable 4D point clouds at mass-market cost. Wafer-scale integration, silicon-germanium processes, and chiplet partitioning drive the average selling price from USD 85 in 2024 to USD 72 in 2025, with forecasts at USD 55 by 2028 as Chinese fabs ramp volume. Lower prices open premium radar functions to entry-level trims, accelerating sensor count and fueling overall automotive radar market demand.

High Multi-Sensor Fusion System Cost

Centralized perception stacks capable of 100+ TOPS artificial intelligence add USD 800-1,200 per vehicle, a premium mass-market brands cannot easily absorb. Liquid-cooled Nvidia Thor compute modules underpin these systems and force design changes in packaging and thermal paths, raising bill-of-material pressure, especially on price-sensitive Asia-Pacific trims. While Chinese suppliers produce compute at a 40-50% discount to Western peers, the near-term burden limits optional radar functions on entry-models and caps immediate addressable volume. Tier-1s must choose between selling standalone modules or taking on full sensor-fusion integration, a trade-off that impacts margin retention and automotive radar market profitability. By the decade's end, 5 nm nodes and chiplet accelerators promise to halve compute costs, but the 2026-2028 window remains a drag on mass uptake.

Other drivers and restraints analyzed in the detailed report include:

- Mass-Market Level-2+ Autonomy Adoption

- EV Architecture Headroom for Additional Sensors

- Spectrum Congestion at 79 GHz in Key Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Short-range radar captured 44.64% of 2025 revenue and is projected to advance at a 13.92% CAGR through 2031. Medium-range devices support cross-traffic detection and intersection monitoring, while long-range units remain the baseline for adaptive cruise control but face price pressure from expanding Chinese capacity.

Corner installations now combine wide-angle coverage with 90 m reach, enabling a single sensor to handle parking, blind-spot and lane-change tasks. Occupancy-monitoring modules at 60 GHz form a nascent ultra-short-range slice that will scale quickly as Euro NCAP in-cabin rules spread. Cost erosion in silicon-germanium front ends lets automakers deploy four to six short-range units without breaching trim-level price targets. Consolidated demand across parking, blind-spot and rear-cross-traffic functions secures a stable growth runway for short-range radar through 2031.

The 77 GHz band held 62.77% of 2025 revenue but its growth moderates as 79 GHz imaging solutions rise at a 13.86% CAGR through 2031. Regulators have frozen new 24 GHz approvals, pushing legacy units toward obsolescence and tightening supplier roadmaps around 77 GHz and 79 GHz.

Tier-1 suppliers unveiled 77-81 GHz system-on-chips that embed deep-learning acceleration, squeezing more angular resolution from established antenna designs. Premium and battery-electric platforms adopt 79 GHz to unlock 4 GHz sweep bandwidth for high-definition point clouds, yet mass-market models remain on 77 GHz for cost control. Spectrum-sharing challenges in dense corridors add engineering overhead, but proprietary interference-rejection stacks keep performance within Euro NCAP tolerance bands. The dual-band roadmap allows carmakers to stagger investment and protect residual tooling value in 77 GHz production lines.

Geography Analysis

Asia-Pacific generated 38.48% of 2025 revenue for the automotive radar market, and its 14.53% CAGR through 2031 positions the region as the fastest-growing demand center. China anchors this expansion: domestic suppliers such as Cheng-Tech and Huawei are scaling 77 GHz and 79 GHz module production to meet the 2028 automatic emergency-braking mandate, while original equipment manufacturers (OEMs) bundle six-sensor suites on mid-tier trims to hold feature parity with European and North American rivals. Japan and South Korea display high radar adoption in premium cars and export large volumes of modules through DENSO, Hitachi Astemo and Nidec Elesys, yet growth moderates as their domestic markets approach saturation. India's radar penetration remains below 10% in 2025, but the Ministry of Road Transport and Highways is evaluating a 2027-2028 automatic emergency-braking timeline, creating a latent runway that could lift regional shipments late in the forecast window. Southeast Asian markets lag in regulatory enforcement, although insurance rebates for blind-spot detection retrofits are stimulating aftermarket demand in Thailand, Indonesia and Vietnam. Australia and New Zealand maintain radar attach rates on par with Western Europe, driven by long-distance highway safety requirements that favor long-range adaptive-cruise modules. Collectively, Asia-Pacific's scale advantage reduces average selling prices, helping the automotive radar market defend margins even as unit counts accelerate.

Europe contributed roughly 28% of global revenue in 2025, underpinned by stringent Euro NCAP ratings that compel five-star contenders to fit forward-collision, blind-spot and in-cabin child-presence radar. Premium brands deploy 4D imaging solutions at 79 GHz to differentiate on perception accuracy, while volume manufacturers still rely on cost-optimized 77 GHz corner sensors for compliance. Continental's cumulative 200 million-unit production milestone and EUR 1.5 billion (USD 1.70 billion) in 2025 radar orders illustrate Europe's role as both design-validation hub and volume anchor for Tier-1 suppliers. Eastern European contract assemblers expand module output to serve German, French and Italian OEMs that embrace near-shoring strategies to contain logistics risk. Regulatory convergence across 27 member states guarantees homogeneous demand, yet spectrum congestion around 79 GHz in dense corridors such as Frankfurt and Paris requires interference-mitigation spending that raises total system cost. As battery-electric vehicle (BEV) registrations rise past 30% of new sales in 2026, European BEV platforms average five to six sensors, prolonging growth even as combustion volumes decline. Europe therefore remains the lead market for software-defined radar updates and over-the-air performance enhancements.

North America held approximately 24% of 2025 revenue, with momentum tied to National Highway Traffic Safety Administration automatic emergency-braking mandates and the commercialization of hands-free highway suites like General Motors Ultra Cruise and Ford BlueCruise. Pickup trucks and full-size SUVs integrate three to four long-range sensors for trailer-tow assistance and lane-centering, lifting per-vehicle dollar content despite lower unit shipments than compact passenger cars. Canada mirrors U.S. regulations, while Mexico focuses on export-oriented assembly of radar-equipped vehicles destined for the United States. South America, the Middle East and Africa together generated less than 10% of 2025 revenue; radar adoption concentrates in fleet and commercial segments where duty-cycle savings and lower insurance premiums offset initial hardware cost. Government safety programs in Brazil and Saudi Arabia may accelerate take-up after 2027, but fragmented standards and limited supplier footprints restrain near-term volumes. Overall, geographic diversification cushions the automotive radar market size from regional policy shocks and balances growth across mature and emerging economies.

- Robert Bosch GmbH

- Continental AG

- DENSO Corporation

- ZF Friedrichshafen AG

- Aptiv PLC

- Texas Instruments Inc.

- HELLA GmbH and Co. KGaA

- NXP Semiconductors N.V.

- Infineon Technologies AG

- Analog Devices Inc.

- Magna International Inc.

- Autoliv Inc.

- Veoneer Safety Systems

- Renesas Electronics Corp.

- STMicroelectronics N.V.

- Valeo SA

- Arbe Robotics Ltd.

- Vayyar Imaging Ltd.

- Indie Semiconductor

- Uhnder Inc.

- Smartmicro GmbH

- Smart Radar System Inc.

- Hitachi Astemo Ltd.

- Nidec Elesys Corp.

- Lunewave Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent NCAP And UNECE Safety Mandates

- 4.2.2 77 GHz Cost-Driven Miniaturisation Wave

- 4.2.3 Mass-Market Level-2+ Autonomy Adoption

- 4.2.4 EV Architecture Headroom For Additional Sensors

- 4.2.5 Emerging 4D Imaging Radar For Vision-Redundancy

- 4.2.6 Chiplet-Based Radar SOCs Enabling Retrofit Market

- 4.3 Market Restraints

- 4.3.1 High Multi-Sensor Fusion System Cost

- 4.3.2 Spectrum Congestion At 79 GHz In Key Regions

- 4.3.3 Thermal Bottlenecks In Legacy GigE Backbones

- 4.3.4 SiGe / GaAs Wafer Supply Constraints

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (Conventional vs 4D vs Imaging)

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Range

- 5.1.1 Short-Range Radar (SRR)

- 5.1.2 Medium-Range Radar (MRR)

- 5.1.3 Long-Range Radar (LRR)

- 5.2 By Frequency Band

- 5.2.1 24 GHz

- 5.2.2 77 GHz

- 5.2.3 79 GHz and above

- 5.3 By Application

- 5.3.1 Adaptive Cruise Control (ACC)

- 5.3.2 Automatic Emergency Braking (AEB)

- 5.3.3 Blind-Spot / Rear Cross-Traffic

- 5.3.4 Occupancy and Driver Monitoring

- 5.3.5 Autonomous Driving (L3+)

- 5.3.6 Parking Assistance and Automated Parking

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Heavy Commercial Vehicles

- 5.4.4 Robotaxis and AV Shuttles

- 5.5 By Propulsion

- 5.5.1 Internal-Combustion Vehicles

- 5.5.2 Battery-Electric Vehicles

- 5.5.3 Hybrid-Electric Vehicles

- 5.6 By Sales Channel

- 5.6.1 OEM-Fitted

- 5.6.2 Aftermarket Retrofits

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 France

- 5.7.3.3 United Kingdom

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 South Korea

- 5.7.4.4 India

- 5.7.4.5 Australia and New Zealand

- 5.7.4.6 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 DENSO Corporation

- 6.4.4 ZF Friedrichshafen AG

- 6.4.5 Aptiv PLC

- 6.4.6 Texas Instruments Inc.

- 6.4.7 HELLA GmbH and Co. KGaA

- 6.4.8 NXP Semiconductors N.V.

- 6.4.9 Infineon Technologies AG

- 6.4.10 Analog Devices Inc.

- 6.4.11 Magna International Inc.

- 6.4.12 Autoliv Inc.

- 6.4.13 Veoneer Safety Systems

- 6.4.14 Renesas Electronics Corp.

- 6.4.15 STMicroelectronics N.V.

- 6.4.16 Valeo SA

- 6.4.17 Arbe Robotics Ltd.

- 6.4.18 Vayyar Imaging Ltd.

- 6.4.19 Indie Semiconductor

- 6.4.20 Uhnder Inc.

- 6.4.21 Smartmicro GmbH

- 6.4.22 Smart Radar System Inc.

- 6.4.23 Hitachi Astemo Ltd.

- 6.4.24 Nidec Elesys Corp.

- 6.4.25 Lunewave Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment