|

시장보고서

상품코드

2065760

암배아항원(CEA) 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Carcinoembryonic Antigen (CEA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

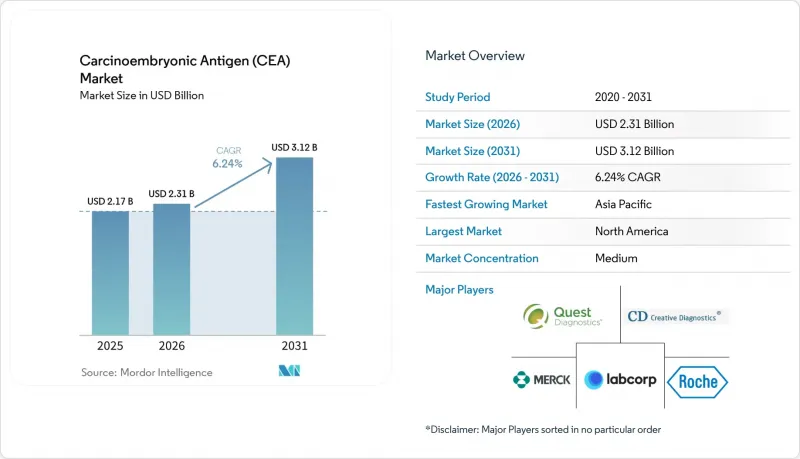

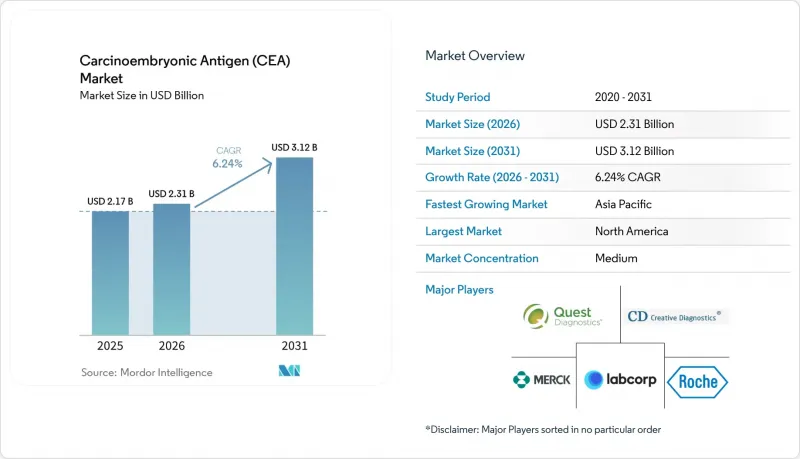

Mordor Intelligence에 의하면, 암배아항원(CEA) 시장 규모는 2025년 21억 7,000만 달러에서 2026년에는 23억 1,000만 달러로 확대되어 2031년까지 31억 2,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 6.24%로 성장할 전망입니다.

본 보고서는 제품별(분석 키트, 분석 장비/기기, 소모품 및 시약), 용도별(대장암, 췌장암, 폐암, 유방암 등), 최종 사용자별(병원 및 외과 센터, 진단실험실, 학술·연구 기관, 기타), 지역별(북미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 암배아항원(CEA) 시장 동향 및 분석

전 세계 대장암 유병률 증가

대장암 발병률 증가는 CEA 시장의 구조적 성장을 이끄는 원동력이 되고 있습니다. 중국에서만 2022년에 약 480만 건의 신규 암 사례가 보고되었으며, 그중 대장암이 주요 원인 중 하나입니다. 서유럽식 식생활로의 전환, 고령화, 그리고 검진 기술의 발전으로 인해 아시아태평양 및 북미 전역에서 대상 환자층이 확대되고 있습니다. 현재 헬스케어 시스템에서는 CEA 측정이 정기적인 모니터링에 포함되어 있으며, 태국의 ‘FIT+CEA’ 2단계 프로그램과 같이 환자를 대장내시경 검사 과정으로 유도하는 사례가 나타나고 있습니다. 임상의들은 간 전이 진단에 있어 80%의 민감도를 보이는 CEA를 높이 평가하고 있으며, 이로 인해 경과 관찰에서 CEA의 역할이 더욱 중요해지고 있습니다. 선별 검사에 참여하는 비율이 높아짐에 따라 검사 건수, 나아가 소모품 수요도 비례하여 증가합니다. 이러한 추세로 인해, 경쟁 유전체 분석 도구의 도입이 가속화되더라도 기본 성장세는 유지될 것입니다.

저침습적 바이오마커를 기반으로 한 모니터링으로의 전환

의사들은 진단 정확도를 유지하면서도 검사 부담을 줄여주는 혈액 검사를 점점 더 선호하고 있습니다. 2024년 FDA의 승인을 받은 83%의 민감도로 대장암을 검출하는 ‘Shield’ 검사는 이러한 비침습적 추세를 상징합니다. 현재, 모세혈관을 이용한 미량 채혈 장치는 정맥 채혈과 동등한 정확도를 실현하고 있어, 채혈 대기 시간 없이 외래에서 빈번한 검사가 가능해졌습니다. 수술 후 경과 관찰 프로토콜에서는 영상 진단 대신 CEA의 연속 측정이 점점 더 많이 채택되고 있어, 환자의 방사선 피폭량과 비용이 줄어들고 있습니다. 후속 검사로 대장내시경 검사 대신 손가락 끝에서 채혈만으로 충분해지면, 환자의 검사 준수율이 현저히 향상되며, CEA 추이를 분석하는 AI 알고리즘이 임상적 신뢰성을 한층 더 높이고 있습니다. 이러한 요인들이 복합적으로 작용하여 조기 개입을 위한 임상적 기회가 확대되고 있으며, 시약에 대한 지속적인 수요가 증가하고 있습니다.

CEA의 낮은 특이도가 위양성을 초래합니다.

널리 보급되어 있음에도 불구하고, CEA는 흡연자, 당뇨병 환자 및 양성 용종을 가진 환자에서 비악성적인 수치 상승이 관찰되며, 5.1-10 ng/mL 범위 내에서는 위양성률이 99.5%에 달합니다(KAMJE.ORG). 정기적인 경과 관찰 결과, 대장암 생존자의 거의 절반이 재발과 무관한 산발적인 CEA 수치 상승을 보이고 있으며, 이로 인해 불필요한 영상 검사와 환자의 불안을 초래하고 있습니다.

따라서 검사 기관에서는 지속적인 상승이 확인될 때까지 임상적 조치를 미루는 ‘리플렉스 검사’ 알고리즘을 채택하고 있지만, 이로 인해 검사 결과 보고까지 걸리는 시간이 길어지고 비용도 증가합니다. 이러한 낮은 특이도로 인해 CEA는 집단 검진에서의 유용성이 제한되며, 그 주요 가치는 치료 경과 모니터링에 국한됩니다. 현재, 조사는 오양성 결과를 줄이기 위해 CEA와 ctDNA, 단백질체학 시그니처를 결합한 다중 분석물 모델로 방향을 잡고 있습니다.

부문별 분석

2025년, 분석 키트는 45.62%의 시장 점유율을 차지하며, 다양한 검사 환경에서 CEA 검사의 표준화에 중심적인 역할을 하고 있음을 반영하고 있습니다. 이 분석 키트가 시장을 독점하고 있는 이유는 그 포괄성에 있으며, 다양한 헬스케어 현장에서 재현성과 규제 준수를 보장하는 완벽한 검사 솔루션을 제공하고 있기 때문입니다. 한편, 소모품 및 시약 부문은 검사 건수 증가와 소모품 특유의 지속적인 수익 모델에 힘입어 2031년까지 연평균 성장률(CAGR) 7.21%를 기록하며 성장할 것으로 전망됩니다. 분석 장비 및 기기는 가장 규모가 작은 부문이지만, 고처리량 CEA 검사의 기술적 기반을 제공하고 있으며, BD와 같은 기업들은 획기적인 분광 기술과 실시간 이미징 기술을 탑재한 ‘FACS Discover A8 Cell Analyzer’와 같은 첨단 플랫폼을 출시하고 있습니다.

자동화 및 고처리량 검사로의 전환에 따라 제품 수요 패턴이 재편되고 있는 가운데, 지멘스 헬스인이어스는 검사 워크플로우를 강화하고 수작업 개입의 필요성을 줄이기 위해 검사실 자동화 분야에서 인간 중심의 엔지니어링에 주력하고 있습니다. 포인트 오브 케어 검사 플랫폼은 업계에 혁신을 가져오는 존재로 부상하고 있으며, 2025년 1월 바이오메륨이 스핀칩 다이아그노스틱스를 인수함에 따라 전혈 검체에서 10분 만에 결과를 도출할 수 있는 면역 측정 기술이 도입되었습니다. 이러한 기술의 발전으로 인해, 분석 키트, 장비, 소모품 간의 기존의 경계를 모호하게 만드는 새로운 제품 카테고리가 등장하고 있습니다. 통합 플랫폼은 사용자의 개입을 최소화하면서도 종합적인 검사 솔루션을 제공하기 때문입니다.

지역별 분석

2025년 북미의 매출 점유율은 41.86%에 달했으며, 이는 동반진단의 긴밀한 통합, 폭넓은 보험 적용, 그리고 견고한 종양학 인프라를 뒷받침하고 있습니다. 미국에서는 절제술을 받은 대장암 환자의 CEA 모니터링에 대한 메디케어의 보험 급여가 효과를 거두고 있는 반면, FDA는 혁신적인 검사법을 신속하게 승인함으로써 기술 갱신 주기를 유지하고 있습니다. 민간 보험사 간의 통합으로 인해 검사 기관은 가격 면에서 압박을 받고 있지만, 검사 건수 증가로 인해 총매출액은 안정적인 수준을 유지하고 있습니다. 캐나다와 멕시코는 전국적인 선별 검사 확대와 국경을 초월한 참조 검사 기관과의 협력을 통해 추가적인 성장에 기여하고 있습니다.

아시아태평양은 6.82%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있으며, 2031년까지 CEA 시장에 상당한 절대적 가치를 더하게 될 것입니다. 중국에서는 혈액 유래 바이오마커를 활용한 다중 암 선별 검사의 시범 사업에 자금이 투입되고 있으며, 각 성의 프로그램에서는 집중 조달을 통해 검사 키트를 일괄 구매하고 있습니다. 일본에서는 2년마다 실시하는 내시경 검사와 바이오마커 모니터링을 결합한 검사 체계를 통해 검사 키트 소비량이 지속적으로 증가하고 있습니다. 인도의 AI 기반 종양 진단 생태계에서는 합리적인 가격의 멀티플렉스 검사와 클라우드 분석을 결합하여 지방 지역의 접근성을 높이는 동시에 시약 수요를 끌어올리고 있습니다.

유럽에서는 선별 검사가 아닌 감시 목적으로 CEA를 권장하는 조화로운 의료기술 평가 과정을 통해 안정적인 한 자릿수 성장이 나타나고 있습니다. 각국의 보건 당국은 구매 수량에 따른 할인을 협상함으로써 공급업체들이 가치 기반 계약으로 전환하도록 유도하고 있습니다. 남미, 중동 및 아프리카는 여전히 개발도상국이지만, 장래성은 높다고 할 수 있습니다. 암 등록 제도의 개선과 기부금을 통한 선별 검사 시범 사업을 통해 CEA 검사 의뢰 건수는 점차 증가할 것으로 보입니다. 전반적으로, 지역 간 불균형이 세계 CEA 시장의 균형을 유지하고 있으며, 고성장 신흥 시장이 성숙 지역의 가격 하락을 상쇄하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the carcinoembryonic antigen (CEA) market size is expected to increase from USD 2.17 billion in 2025 to USD 2.31 billion in 2026 and reach USD 3.12 billion by 2031, growing at a CAGR of 6.24% over 2026-2031.

This report is Segmented by Product (Assay Kits, Analyzers/Instruments, Consumables & Reagents), Application (Colorectal Cancer, Pancreatic Cancer, Lung Cancer, Breast Cancer, and More), End User (Hospitals & Surgical Centers, Diagnostic Laboratories, Academic & Research Institutes, Others), and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Carcinoembryonic Antigen (CEA) Market Trends and Insights

Escalating Global Colorectal Cancer Prevalence

Rising colorectal cancer incidence is a structural growth catalyst for the CEA market. China alone reported about 4.8 million new cancer cases in 2022, with colorectal malignancies among the top contributors Lifestyle shifts toward Western diets, ageing populations, and improved detection are enlarging the addressable patient pool across Asia-Pacific and North America. Healthcare systems now embed CEA measurement into routine surveillance, as seen in Thailand's two-step FIT-plus-CEA program that feeds patients into colonoscopy pathways . Clinicians value CEA for its 80% sensitivity in identifying liver metastases, reinforcing its role in longitudinal monitoring . As screening participation rises, test volumes-and thus consumable pull-through-scale proportionally. This dynamic sustains baseline growth even when adoption of competing genomic tools accelerates.

Shift Toward Minimally-Invasive Biomarker-Based Monitoring

Physicians show mounting preference for blood-based assays that lower procedural burden while sustaining diagnostic accuracy. The FDA approval of the Shield test in 2024, which detects colorectal cancer with 83% sensitivity, exemplifies this non-invasive trend . Capillary-blood micro-collection devices now match venous-draw accuracy, enabling frequent outpatient testing without phlebotomy queues. Post-operative surveillance protocols increasingly replace imaging with serial CEA measurement, reducing patient exposure to radiation and cost. Patient adherence improves materially when follow-up requires a finger-stick rather than a colonoscopy, and AI algorithms that analyze CEA trajectories are further elevating clinical confidence. These factors collectively widen the clinical window for early intervention and reinforce recurring reagent demand.

Limited Specificity of CEA Leading to False Positives

Despite ubiquity, CEA suffers non-malignant elevation in smokers, diabetics, and patients with benign polyps, producing false-positive rates as high as 99.5% within the 5.1-10 ng/mL band [KAMJE.ORG]. In routine surveillance, nearly half of colorectal cancer survivors record sporadic CEA spikes unrelated to relapse, driving unnecessary imaging and patient anxiety.

Laboratories therefore adopt reflex testing algorithms that delay clinical action until sequential rises are confirmed, but this lengthens turnaround and raises cost. The specificity shortfall limits CEA utility in population screening, confining its core value to treatment monitoring. Research now orients toward multi-analyte models that blend CEA with ctDNA or proteomic signatures to mitigate erroneous positives.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in High-Sensitivity Multiplex Immunoassays

- Expanding Government-Funded Cancer Screening Programs in Asia-Pacific

- Competition from Emerging Genomic & Proteomic Biomarkers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Assay kits commanded 45.62% market share in 2025, reflecting their central role in standardizing CEA testing across diverse laboratory environments. The dominance of assay kits stems from their comprehensive nature, providing complete testing solutions that ensure reproducibility and regulatory compliance across different healthcare settings. However, the consumables and reagents segment is projected to grow at 7.21% CAGR through 2031, driven by increasing test volumes and the recurring revenue model inherent in consumables. Analyzers and instruments represent the smallest segment but provide the technological foundation for high-throughput CEA testing, with companies like BD launching advanced platforms such as the FACSDiscover A8 Cell Analyzer featuring breakthrough spectral and real-time imaging technologies.

The shift toward automation and high-throughput testing is reshaping product demand patterns, with Siemens Healthineers focusing on human-centered engineering in laboratory automation to enhance diagnostic workflows and reduce manual intervention requirements . Point-of-care testing platforms are emerging as a disruptive force, with bioMerieux's acquisition of SpinChip Diagnostics in January 2025 bringing immunoassay technology that delivers results from whole blood samples in 10 minutes. This technological evolution is creating new product categories that blur traditional boundaries between assay kits, instruments, and consumables, as integrated platforms offer complete testing solutions with minimal user intervention.

Geography Analysis

North America's 41.86% revenue share in 2025 underscores deep integration of companion diagnostics, generous insurance coverage, and robust oncology infrastructures. The United States benefits from Medicare reimbursement for CEA monitoring in resected colorectal cancer, while the FDA fast-tracks innovative assays, sustaining technology refresh cycles . Consolidation among private payers pressures laboratories on pricing, yet elevated test volumes keep aggregate revenues stable. Canada and Mexico contribute incremental growth through national screening roll-outs and cross-border reference-lab collaborations.

Asia-Pacific delivers the fastest 6.82% CAGR and will add sizeable absolute value to the CEA market by 2031. China funds multi-cancer screening pilots incorporating blood-based biomarkers, with provincial programs purchasing bulk assay lots under centralized tenders. Japan's biennial endoscopy plus biomarker monitoring regimen drives sustained kit consumption. India's AI-augmented oncology diagnostics ecosystem blends affordable multiplex assays with cloud analytics, widening rural access and lifting reagent demand.

Europe shows steady single-digit growth via harmonized health-technology assessment pathways that endorse CEA for surveillance rather than screening. National Health Services negotiate volume-based discounts, nudging vendors toward value-based contracting. South America and the Middle East & Africa remain nascent but promising: improving cancer registries and donor-funded screening pilots will gradually pull CEA test orders upward. Collectively, regional heterogeneity balances the global CEA market, with high-growth emerging markets offsetting mature-region price erosion.

- Abbott Laboratories

- Roche

- Thermo Fisher Scientific

- Siemens Healthineers

- Danaher

- Beckton Dickinson

- bioMerieux

- DiaSorin

- Merck

- Bio-Rad Laboratories

- Tosoh

- Fujirebio Diagnostics (H.U. Group)

- Sysmex

- Randox Laboratories

- Quanterix Corporation

- Creative Diagnostics

- LabCorp

- Quest Diagnostics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating global colorectal cancer prevalence

- 4.2.2 Shift toward minimally-invasive biomarker-based monitoring

- 4.2.3 Technological advances in high-sensitivity multiplex immunoassays

- 4.2.4 Expanding government-funded cancer screening programs in Asia-Pacific

- 4.2.5 Rising demand for companion diagnostics in biologics trials

- 4.3 Market Restraints

- 4.3.1 Limited specificity of CEA leading to false positives

- 4.3.2 Competition from emerging genomic & proteomic biomarkers

- 4.3.3 Pricing pressure from assay commoditization

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product (Value)

- 5.1.1 Assay Kits

- 5.1.2 Analyzers / Instruments

- 5.1.3 Consumables & Reagents

- 5.2 By Application (Value)

- 5.2.1 Colorectal Cancer

- 5.2.2 Pancreatic Cancer

- 5.2.3 Lung Cancer

- 5.2.4 Breast Cancer

- 5.2.5 Liver Cancer

- 5.2.6 Others

- 5.3 By End User (Value)

- 5.3.1 Hospitals & Surgical Centers

- 5.3.2 Diagnostic Laboratories

- 5.3.3 Academic & Research Institutes

- 5.3.4 Others

- 5.4 By Geography (Value)

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 F. Hoffmann-La Roche Ltd

- 6.3.3 Thermo Fisher Scientific Inc.

- 6.3.4 Siemens Healthineers AG

- 6.3.5 Danaher Corporation (Beckman Coulter)

- 6.3.6 Becton, Dickinson and Company

- 6.3.7 bioMerieux SA

- 6.3.8 DiaSorin S.p.A.

- 6.3.9 Merck KGaA

- 6.3.10 Bio-Rad Laboratories, Inc.

- 6.3.11 Tosoh Corporation

- 6.3.12 Fujirebio Diagnostics (H.U. Group)

- 6.3.13 Sysmex Corporation

- 6.3.14 Randox Laboratories Ltd.

- 6.3.15 Quanterix Corporation

- 6.3.16 Creative Diagnostics

- 6.3.17 LabCorp

- 6.3.18 Quest Diagnostics Incorporated

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment