|

시장보고서

상품코드

2065774

합법적 감청 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Lawful Interception - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

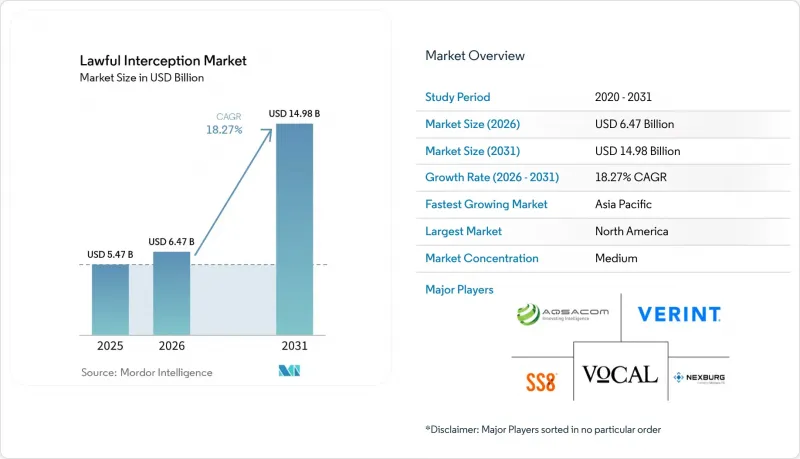

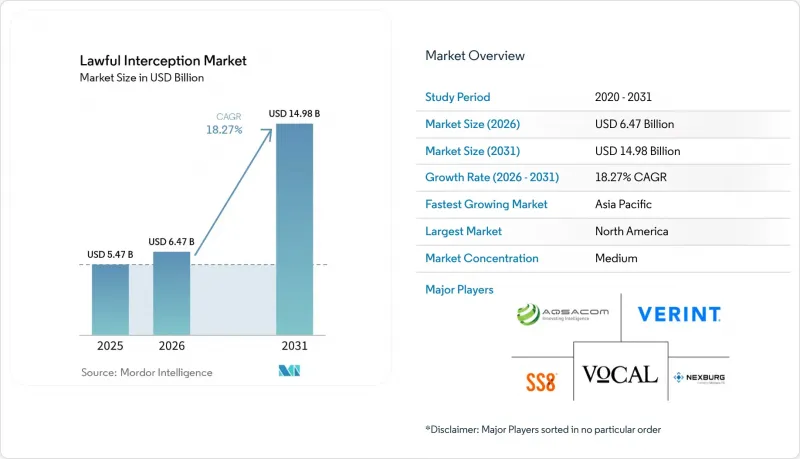

Mordor Intelligence에 의하면, 합법적 감청 시장 규모는 2025년 54억 7,000만 달러로 평가되었고, 2026년에는 64억 7,000만 달러로 추정되고, 2026-2031년 CAGR 18.27%로 성장을 지속할 전망이며, 2031년에는 149억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소별(솔루션 및 서비스), 네트워크별(고정 네트워크, 모바일 네트워크, IP 네트워크), 통신 채널별(음성 통신, 데이터 통신 등), 최종 사용자별(정부 및 법 집행 기관 등), 도입 형태별(온프레미스, 클라우드 및 호스팅형 LI-As-A-Service), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 합법적 감청 시장 동향 및 인사이트

가중되는 사이버 위협과 국가 안보상의 우려

지정학적 긴장과 국가 주도의 사이버 작전으로 인해 북미, 유럽, 아시아태평양 지역 전반에서 감청 예산이 증가하고 있습니다. 미국 국방부가 발표한 2024년 중국의 사이버 전쟁 태세에 대한 평가에서는 동시 다채널 감시가 가능한 첨단 감청 거점 구축이 시급하다는 점을 강조하고 있습니다. MITRE가 2024년 12월에 발표한, 곳곳에서 이루어지고 있는 기술적 감시에 관한 검토 보고서에서는 AI를 활용한 분석을 통해 원시 감청 데이터를 실용적인 정보로 변환할 수 있기 때문에 각 기관은 음성 감청에 그치지 않는 수준으로 시스템을 업그레이드해야 할 필요성에 직면해 있다고 주장하고 있습니다. 조직적인 위협 패턴을 신속하게 감지하는 것은 현재 5G 슬라이스, 위성 링크, 암호화 메시징에 걸친 실시간 상관 분석에 달려 있습니다. 따라서, 사일로화된 프로브가 아닌 통합된 분석 제품군을 제공하는 벤더들이 경쟁 우위를 점하고 있습니다. 특히 미국, 영국, 호주, 일본에서 시행되는 국가 차원의 조달 프로그램이 계속해서 기초적인 수요를 견인하고 있습니다.

규제상 의무 및 규정 준수 요건

세계 각국 정부는 통신 사업자 및 디지털 플랫폼에 대해 합법적인 접근 기능을 제공하도록 의무화하는 법적 체계를 강화하고 있습니다. EU의 2024년판 이중용도 수출관리 개정안에서는 감시 도구에 대한 실사 강화가 요구되고 있으며, 규정 준수 관련 문서를 잘 갖춘 공급업체가 유리한 입장에 서게 됩니다. 인도의 ‘통신법안’ 초안 및 2024년 5G 감청과 관련된 국가사이버조정센터(NCCC)의 사양서는 상세한 기술적 청사진을 규정하고 있으며, 현지 통신 사업자들을 검증된 3GPP 준수 솔루션으로 이끌고 있습니다. 금융기관들은 현재 도청 기록을 FinCEN의 국경 간 자금 추적 의무와 일치시켜야 하므로, 규정 준수 감시에 대한 기업 지출이 증가하고 있습니다. 규제 당국이 아키텍처 지침으로 3GPP TS 33.106/107을 참고하고 있기 때문에 표준화 위원회에 참여하고 있는 벤더들의 솔루션 도입이 가속화되고 있습니다.

개인정보 보호권을 둘러싼 반발과 데이터 보호법

시민의 자유를 요구하는 압력과 엄격한 데이터 보호법으로 인해, 특히 유럽과 북미에서는 광범위한 감시 도구의 도입이 억제되고 있습니다. 유럽 데이터보호위원회가 2025년 2월에 발표한 AI의 개인정보 보호 위험에 관한 지침에서는 알고리즘의 투명성과 데이터 최소화가 요구되고 있어, AI를 활용한 감청 시 종합적인 데이터 수집의 장벽이 높아지고 있습니다. 회원국마다 규정이 제각각이기 때문에 통신 사업자들은 서로 다른 규정 준수 업무 절차를 유지할 수밖에 없어 비용이 증가하고 있습니다. 옹호 단체들은 알고리즘의 편향성 및 대규모 감시와 관련된 소송을 계속하고 있으며, 공급업체들에게 선택적 타겟팅과 견고한 감시 대시보드의 도입을 촉구하고 있습니다. 이와 동시에, OTT 플랫폼에서 엔드투엔드 암호화가 기본 설정으로 적용됨에 따라 감청 범위가 제한되고 있으며, 이로 인해 예외적인 접근 의무에 관한 정책 논쟁이 격화되고 있습니다.

부문별 분석

2025년, 합법적인 감청 시장에서 솔루션의 점유율은 67.20%를 차지한 것으로 평가되었으며, 이는 중계 장치, 감청 액세스 포인트 및 분석 플랫폼에 대한 수요에 힘입은 결과입니다. 그러나 통신 사업자와 기업들이 통합, 규제 대응, 라이프사이클 지원을 외부에 위탁함에 따라, 서비스 부문은 연평균 성장률(CAGR) 18.62%로 확대될 것으로 전망됩니다. 3GPP 사양을 실용적인 도입 계획으로 구체화하는 컨설팅 업무는 특히 5G 슬라이싱으로 인해 아키텍처가 복잡해지고 있는 만큼 여전히 수요가 높습니다. 관리형 감청 서비스는 24시간 상주하는 보안 인력을 보유하지 않은 소규모 통신 사업자에게 매력적인 선택지입니다. 솔루션 분야 중에서는 감청 관리 소프트웨어가 가장 빠르게 성장하고 있습니다. 이는 암호화된 페이로드를 분석하는 AI 모듈이 분석의 가치를 높이고 있기 때문입니다. 복호화 엔진과 행동 분석 애드온은 코어 프로브를 보완하여 선제적인 이상 알림을 가능하게 합니다. 메디에이션 디바이스는 소프트웨어 정의형 대체 제품으로 인한 상품화 압력에 직면해 있지만, 레거시 회선 교환형 도메인에서는 여전히 중요한 역할을 수행하고 있습니다. 따라서 합법적인 감청 시장은 하드웨어 추상화와 클라우드 기반 오케스트레이션을 통합한 플랫폼으로 전환되고 있습니다.

규제의 급격한 변화로 인해 서비스의 가치는 더욱 높아지고 있습니다. 자문팀은 수출 관리 평가 및 개인정보 영향 감사를 통해 통신 사업자를 지원하며, 규정 준수 위험을 최소화합니다. 지속적 통합(CI) 지원을 통해 프로브 펌웨어가 분기별 3GPP 릴리스를 확실하게 준수하도록 보장됩니다. 교육 서비스를 통해 조사 담당자는 AI 대시보드를 효과적으로 활용할 수 있게 되어, 인사이트를 얻는 데 걸리는 평균 시간을 단축합니다. 멀티테넌트형 클라우드 도입이 확대되는 가운데, 각 벤더사는 패치 적용 및 검증을 자동화하는 DevSecOps 솔루션 제공을 확대되고 있습니다. 그 결과, 여전히 주류를 이루고 있는 솔루션과 전문 서비스 및 관리형 서비스를 통한 지속적인 수익원이 합법적 감청 시장에서 공급업체의 수익 구조를 점점 더 안정적으로 만들고 있습니다.

2025년, 모바일 인프라는 합법적 감청 시장 규모의 50.60%를 차지했으며, 이는 GSM, UMTS 및 LTE 감시 인프라가 확고히 자리 잡았음을 반영합니다. 그러나 VoIP, VoLTE 및 OTT 트래픽으로 인해 통신이 패킷 도메인으로 전환됨에 따라, IP 네트워크는 연평균 성장률(CAGR) 19.05%로 확대되고 있습니다. 패킷 지향화를 통해 풍부한 메타데이터가 확보됨에 따라, 당국은 협대역 음성 통신으로는 얻을 수 없었던 소셜 그래프와 행동 패턴을 파악할 수 있게 됩니다. 5G 독립형 환경에서의 네트워크 슬라이싱은 기존의 코어 프로브를 우회하는 가상 서브넷을 생성함으로써, 에지 측에 배치된 감청 기능에 대한 수요를 불러일으키고 있습니다. 사용자 플레인 프로브와 고처리량 패킷 브로커를 통합할 수 있는 벤더는 Tier 1 통신사들 사이에서 높은 인지도를 얻고 있습니다.

유선 네트워크 분야는 안정세를 유지하고 있지만, 구리선 회선의 폐지가 가속화됨에 따라 서서히 축소되고 있습니다. 하이브리드 VoLTE의 도입으로 인해 모바일과 IP의 경계가 모호해지면서, RAN, 코어, IMS 등 각 도메인에 걸친 통합적인 감청 오케스트레이션이 요구되고 있습니다. NEC가 SS8에 기반한 태평양 횡단 합법적 감청 규정 준수 인증을 획득한 것은 해저 회선에서 대양 횡단 패킷 감청에 필요한 요건을 여실히 보여주고 있습니다. 모바일 분야에서는 3G/4G 네트워크가 여전히 프로브 트래픽의 대부분을 차지하고 있지만, 5G 트래픽은 기하급수적으로 증가하고 있어, 벤더들은 패킷 손실 없이 100 Gbps의 캡처 속도를 실현해야 하는 압박을 받고 있습니다. 그 결과, 투자는 급증하는 암호화 트래픽에 대해서도 미래에 대비한 대응이 가능한, 확장 가능하고 가상화된 IP 감청 프레임워크로 전환되고 있습니다.

지역별 분석

북미는 2025년에도 합법적 감청 시장 규모의 38.85%를 계속 차지했으며, 이는 연방 정부의 자금 지원, 성숙한 통신 인프라, 그리고 세계 표준을 형성하는 벤더 생태계에 힘입은 결과입니다. 미국 정부 기관들은 ‘법 집행 기관 통신 지원법(CALEA)’의 규정을 지속적으로 세분화하고 있으며, 이에 따라 업그레이드된 프로브에 대한 국내 수요가 증가하고 있습니다. 캐나다의 5G 공급망 보안 심사는 지정학적 감시가 강화되는 가운데, 통신 사업자들이 도청 방지 규정 준수 인증을 취득해야 할 시급성을 높이고 있습니다. AI 조사 분야에서 지역적 리더십이 고급 분석 모듈의 도입을 가속화하여, 혁신과 조달이라는 선순환을 만들어내고 있습니다. 랜섬웨어 및 국가가 연루된 해킹 사건 증가로 인해 예산 배정이 유지되고 있으며, 플랫폼의 꾸준한 업데이트가 보장되고 있습니다.

아시아태평양은 2031년까지 19.36%라는 지역별 최고 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 5G의 급속한 확산에 따라 네트워크 슬라이스 및 엣지 클라우드를 위한 감청 메커니즘이 필요해졌으며, 이러한 요건은 인도의 NCCC 기술 프레임워크에 의해 규정되어 있습니다. 호주, 일본, 한국에서는 중요 인프라에 대해 엄격한 규제가 적용되고 있으며, 이것이 적극적인 시스템 업그레이드를 촉진하고 있습니다. 한편, 동남아시아의 통신 사업자들은 막대한 설비 투자를 피하기 위해 클라우드 호스팅 방식의 프로브를 도입하고 있으며, 이는 해당 지역의 디지털 전환 노력과도 부합합니다. 중국의 확대되는 사이버 전쟁 전략으로 인해 주변국들은 국내 감시 능력을 강화해야 하는 상황에 놓여 있으며, AI를 활용한 분석에 대한 수요가 증가하고 있습니다. 그러나 이 지역은 법 제도가 다르기 때문에 공급업체는 관할 구역별로 규정 준수 패키지를 맞춤화할 수밖에 없습니다.

유럽에서는 개인정보 보호와 보안상의 요구 사항이 복잡하게 얽혀 있습니다. 유럽연합 집행위원회의 고위급 그룹이 비협조적인 OTT 사업자에 대한 제재를 권고한 것은 통신의 추적 가능성을 중시하는 규제 방향을 여실히 보여주고 있습니다. 그러나 GDPR(EU 개인정보보호규정)의 의무에 따라 데이터 최소화 및 합법적인 목적으로의 제한이 부과됨에 따라 도입의 복잡성이 증가하고 있습니다. 회원국마다 규정이 제각각이기 때문에 통신 사업자는 서로 다른 LI 핸드오버 형식에 대응하기 위해 여러 개의 중계 게이트웨이를 동시에 운영해야 하는 경우가 종종 있습니다. 따라서 광범위한 법률 자료실을 보유한 유서 깊은 벤더는 경쟁 우위를 점하고 있습니다. 한편, 라틴아메리카와 중동 및 아프리카에서는 시장이 아직 발전 단계에 있지만, 장래성이 기대되고 있습니다. 이 지역의 통신 사업자들은 감청에 대한 투자와 진행 중인 인프라 구축 간의 균형을 맞추고, 막대한 현지 하드웨어 투자를 피하기 위해 종종 클라우드 서비스를 이용하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the lawful interception market size is expected to grow from USD 5.47 billion in 2025 to USD 6.47 billion in 2026 and is forecast to reach USD 14.98 billion by 2031 at 18.27% CAGR over 2026-2031.

This report is Segmented by Component (Solution and Services), Network (Fixed Networks, Mobile Networks, and IP Networks), Communication Channel (Voice Communication, Data Communication, and More), End-User (Government and Law-Enforcement Agencies, and More), Deployment Mode (On-Premise, and Cloud/Hosted LI-As-A-Service), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Lawful Interception Market Trends and Insights

Rising Cyber-Threats and National Security Concerns

Geopolitical tensions and state-sponsored cyber operations are elevating interception budgets across North America, Europe, and Asia-Pacific. The U.S. Department of Defense's 2024 assessment of China's cyber-warfare posture underscores the urgency for advanced listening posts capable of simultaneous multi-channel surveillance. MITRE's December 2024 review of ubiquitous technical surveillance argues that AI-enabled analytics convert raw intercepts into actionable intelligence, driving agencies to upgrade beyond voice taps. Rapid detection of coordinated threat patterns now hinges on real-time correlation across 5G slices, satellite links, and encrypted messaging. Vendors offering integrated analytics suites rather than siloed probes therefore gain competitive traction. National-level procurement programs, particularly in the United States, United Kingdom, Australia, and Japan, continue to drive baseline demand.

Regulatory Mandates and Compliance Requirements

Governments worldwide are tightening legal frameworks that oblige telecom operators and digital platforms to furnish lawful-access capabilities. The EU's 2024 dual-use export-control update demands enhanced due diligence for surveillance tools, favoring vendors with mature compliance documentation. India's draft Telecommunication Bill and its 2024 National Cyber Coordination Centre (NCCC) specifications for 5G interception codify detailed technical blueprints, steering local carriers toward tested 3GPP-conformant solutions. Financial institutions must now align interception records with FinCEN's cross-border funds tracing obligations, expanding enterprise spending on compliance monitoring. As regulators reference 3GPP TS 33.106/107 for architectural guidance, vendors embedded in standards committees enjoy accelerated adoption.

Privacy-Rights Backlash and Data-Protection Laws

Civil-liberties pressure and stringent data-protection statutes temper the adoption of expansive surveillance tools, particularly in Europe and North America. The European Data Protection Board's February 2025 guidance on AI privacy risks calls for algorithmic transparency and data minimisation, raising hurdles for blanket data collection in AI-enhanced interception. Fragmented Member-State rules compel carriers to maintain disparate compliance workflows, adding cost. Advocacy groups continue to litigate algorithmic bias and mass-surveillance claims, forcing vendors to introduce selective targeting and robust oversight dashboards. In parallel, end-to-end encryption defaults on OTT platforms limit interception scope, intensifying the policy debate on exceptional-access mandates.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of IP-Based and 5G Communications

- Shift Toward Cloud-Hosted Interception Platforms

- High Cost and Complexity of Multi-Network Build-Out

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 67.20% of the lawful interception market share in 2025, underpinned by demand for mediation devices, interception access points, and analytics platforms. However, the services segment is projected to rise at a 18.62% CAGR as carriers and enterprises outsource integration, regulatory mapping, and lifecycle support. Consulting engagements that translate 3GPP specifications into actionable deployment blueprints remain in high demand, especially as 5G slicing adds architectural nuance. Managed interception services appeal to smaller operators lacking round-the-clock security staff. Within solutions, interception-management software enjoys the highest velocity because AI modules that parse encrypted payloads drive analytic value. Decryption engines and behavioural-analysis add-ons complement core probes, enabling proactive anomaly alerts. Mediation devices face commoditisation pressure from software-defined alternatives, yet they retain importance for legacy circuit-switched domains. The lawful interception market thus tilts toward platforms that bundle hardware abstraction with cloud-ready orchestration.

Rapid regulatory churn further elevates service value. Advisory teams guide carriers through export-control assessments and privacy-impact audits, minimising compliance risk. Continuous-integration support ensures that probe firmware aligns with quarterly 3GPP releases. Training services equip investigators to exploit AI dashboards, shortening mean-time-to-insight. As multi-tenant cloud deployments proliferate, vendors expand DevSecOps offerings to automate patching and verification. Consequently, although solutions remain dominant, recurring-revenue streams from professional and managed services increasingly stabilise vendor revenue profiles in the lawful interception market.

Mobile infrastructure held 50.60% of the lawful interception market size in 2025, reflecting entrenched GSM, UMTS, and LTE monitoring foundations. Yet IP networks are advancing at a 19.05% CAGR because VoIP, VoLTE, and OTT traffic shift communications toward packet domains. Packet orientation unlocks metadata richness, allowing agencies to map social graphs and behavioural patterns unavailable in narrowband voice. Network slicing under 5G standalone creates virtual sub-nets that bypass legacy core probes, prompting demand for edge-resident intercept functions. Vendors able to merge user-plane probes with high-throughput packet brokers capture mindshare among tier-one carriers.

The fixed-network segment remains stable but slides slowly as copper retirements accelerate. Hybrid VoLTE deployments blur mobile and IP boundaries, forcing unified interception orchestration across RAN, core, and IMS domains. NEC's certification of trans-Pacific lawful-intercept compliance with SS8 illustrates cross-ocean packet-intercept requirements for submarine routes. Within the mobile category, 3G/4G networks still generate majority probe volumes, but 5G traffic grows exponentially, pushing vendors to engineer 100 Gbps capture rates without packet loss. Consequently, investment tilts toward scalable, virtualised IP-intercept frameworks that future-proof carriers against surging encrypted traffic.

Geography Analysis

North America retained 38.85% of the lawful interception market size in 2025, supported by federal funding, mature telecom infrastructure, and vendor ecosystems that shape global standards. U.S. agencies continue to refine Communications Assistance for Law Enforcement Act provisions, bolstering domestic demand for upgraded probes. Canada's 5G supply-chain security reviews add urgency for carriers to certify interception compliance amid geopolitical scrutiny. Regional leadership in AI research accelerates the adoption of advanced analytics modules, feeding virtuous cycles of innovation and procurement. Heightened ransomware and state-sponsored hacking incidents sustain budget allocations, ensuring steady platform refreshes.

Asia-Pacific is projected to post the fastest regional CAGR at 19.36% through 2031. Rapid 5G roll-outs require intercept mechanisms for network slices and edge clouds, tasks codified by India's NCCC technical framework. Australia, Japan, and South Korea apply stringent critical-infrastructure rules, spurring proactive system upgrades. Meanwhile, Southeast Asian operators embrace cloud-hosted probes to avoid heavy capex, aligning with regional digital-transformation agendas. China's expanding cyber-warfare doctrine is prompting neighbouring states to harden domestic surveillance capabilities, reinforcing demand for AI-driven analytics. The region, however, presents heterogeneous legal regimes, compelling vendors to tailor compliance packs per jurisdiction.

Europe exhibits a complex interplay of privacy safeguards and security imperatives. The European Commission's High-Level Group recommendation to sanction non-cooperative OTT providers spotlights a regulatory tilt toward traceable communications. Yet GDPR obligations mandate data minimisation and lawful-purpose constraints, increasing deployment complexity. Fragmented member-state regulations mean that carriers often must maintain parallel mediation gateways to accommodate differing LI handover formats. Established vendors with extensive legal libraries, therefore, gain a competitive advantage. Elsewhere, Latin America, the Middle East, and Africa remain nascent yet promising; operators there balance interception investments against ongoing infrastructure build-outs, often turning to cloud services that circumvent heavy local hardware outlays.

- Verint Systems Inc.

- SS8 Networks, Inc.

- Nexburg GmbH

- Trovicor GmbH

- BAE Systems plc

- Gamma Group

- Elbit Systems Ltd.

- IPS S.p.A.

- Aqsacom Inc.

- Vocal Technologies Ltd.

- Ericsson AB

- Nokia Corp.

- Huawei Technologies Co. Ltd.

- Cisco Systems, Inc.

- Rohde and Schwarz GmbH

- Group 2000

- NetQuest Corp.

- NICE Ltd.

- Thales Group

- Palantir Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising cyber-threats and national security concerns

- 4.2.2 Regulatory mandates and compliance requirements

- 4.2.3 Proliferation of Internet Protocol (IP)-based and 5G communications

- 4.2.4 Shift toward cloud-hosted interception platforms

- 4.2.5 Artificial Intelligence (AI)-driven real-time metadata analytics Return on Investment (ROI)

- 4.2.6 Digital-evidence admissibility frameworks

- 4.3 Market Restraints

- 4.3.1 Privacy-rights backlash and data-protection laws

- 4.3.2 High cost and complexity of multi-network build-out

- 4.3.3 Vendor lock-in limits interoperability

- 4.3.4 "Encryption-by-default" policies in Over-The-Top (OTT) apps

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape and Government Initiatives

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solution

- 5.1.1.1 Mediation devices

- 5.1.1.2 Interception access points

- 5.1.1.3 Interception management software

- 5.1.1.4 Decryption and analytics modules

- 5.1.2 Services

- 5.1.2.1 Consulting

- 5.1.2.2 Integration and deployment

- 5.1.2.3 Support and maintenance

- 5.1.1 Solution

- 5.2 By Network

- 5.2.1 Fixed networks

- 5.2.1.1 Public Switched Telephone Network (PSTN)

- 5.2.1.2 Broadband

- 5.2.2 Mobile networks

- 5.2.2.1 Global System for Mobile Communications (GSM)

- 5.2.2.2 General Packet Radio Service (GPRS)

- 5.2.2.3 3G/4G/LTE

- 5.2.2.4 5G and future Radio Access Network (RAN)

- 5.2.3 IP networks

- 5.2.3.1 Voice over Internet Protocol (VoIP)

- 5.2.3.2 Data-traffic monitoring

- 5.2.1 Fixed networks

- 5.3 By Communication Channel

- 5.3.1 Voice communication

- 5.3.2 Data communication

- 5.3.3 Social media and OTT messaging

- 5.4 By End-User

- 5.4.1 Government and Law-Enforcement Agencies

- 5.4.2 Intelligence agencies

- 5.4.3 Enterprises

- 5.5 By Deployment Mode

- 5.5.1 On-premise

- 5.5.2 Cloud/Hosted LI-as-a-Service

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Verint Systems Inc.

- 6.4.2 SS8 Networks, Inc.

- 6.4.3 Nexburg GmbH

- 6.4.4 Trovicor GmbH

- 6.4.5 BAE Systems plc

- 6.4.6 Gamma Group

- 6.4.7 Elbit Systems Ltd.

- 6.4.8 IPS S.p.A.

- 6.4.9 Aqsacom Inc.

- 6.4.10 Vocal Technologies Ltd.

- 6.4.11 Ericsson AB

- 6.4.12 Nokia Corp.

- 6.4.13 Huawei Technologies Co. Ltd.

- 6.4.14 Cisco Systems, Inc.

- 6.4.15 Rohde and Schwarz GmbH

- 6.4.16 Group 2000

- 6.4.17 NetQuest Corp.

- 6.4.18 NICE Ltd.

- 6.4.19 Thales Group

- 6.4.20 Palantir Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis