|

시장보고서

상품코드

2065776

클라우드 보안 태세 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cloud Security Posture Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

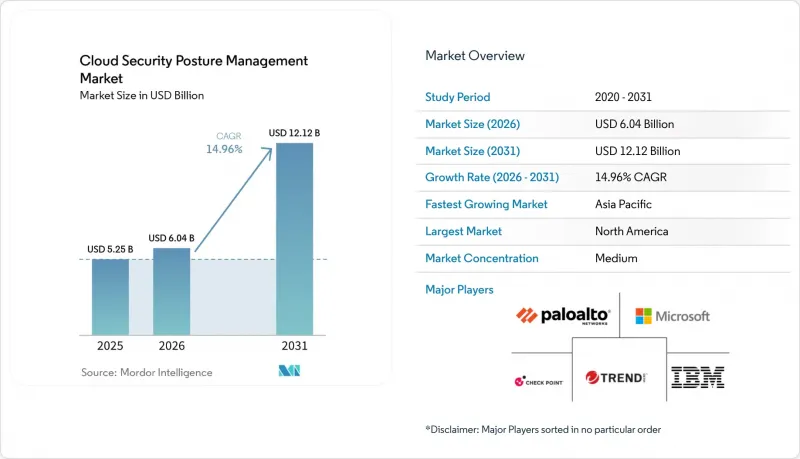

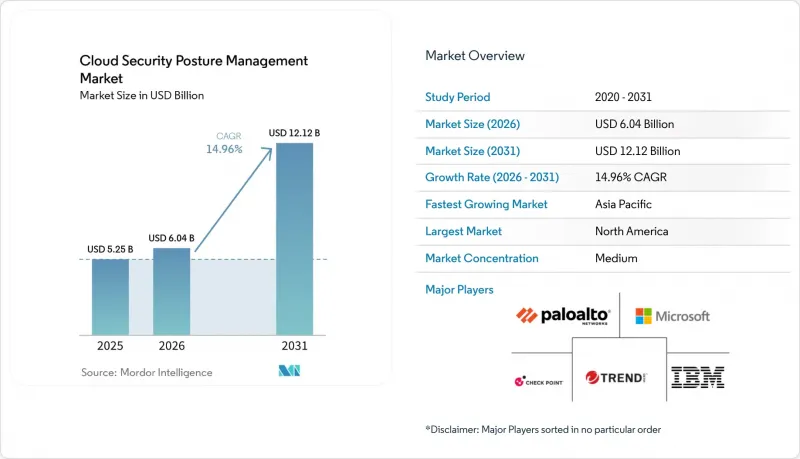

Mordor Intelligence에 의하면, 클라우드 보안 태세 시장 규모는 2025년 52억 5,000만 달러, 2026년 60억 4,000만 달러에서 2031년까지 121억 2,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 14.96%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소(솔루션 및 서비스), 클라우드 모델(Infrastructure As A Service(IaaS), Platform As A Service(PaaS) 등), 배포 모드(퍼블릭 클라우드, 프라이빗 클라우드 등), 조직 규모(대기업 및 중소기업), 산업 분야(은행, 금융서비스 및 보험(BFSI), 헬스케어, 제조업 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 클라우드 보안 태세 관리(CSPM) 시장 동향 및 인사이트

CSPM의 클라우드 네이티브 애플리케이션 보호 플랫폼(CNAPP) 생태계로의 통합

클라우드 보안 태세 관리는 독립형 대시보드에서 통합된 CNAPP 제품군의 핵심 모듈로 빠르게 전환되고 있습니다. 이러한 변화로 인해 보안 팀은 중복되는 콘솔과 정책을 개별적으로 관리해야 하는 번거로움에서 벗어날 수 있습니다. Aqua Security가 컨테이너 및 워크로드 제어와 함께 포지션 분석 기능을 제공하기로 한 결정은 단일 정책 평면을 통해 빌드 단계부터 실행 단계에 이르기까지의 설정 오류를 추적할 수 있게 되었음을 보여줍니다. 이러한 진화가 클라우드 보안 태세 관리 시장의 성장을 주도하고 있습니다. 통합 플랫폼을 도입한 조직에서는 경보가 자산의 맥락이나 악용 경로와 연계된 상태로 전달되기 때문에 문제 해결까지 걸리는 평균 소요 시간(MTTR)이 대폭 단축되었다고 보고되고 있습니다. 또한, 동일한 콘솔을 통해 개발 파이프라인에 가드레일을 구축함으로써, 프로덕션 환경의 리소스에 도달하기 전에 설정의 편차를 억제하고 있습니다. ID 거버넌스 모듈과의 통합을 통해 클라우드 계정 내 권한 침식을 가시화하고, 숨겨진 공격 표면을 더욱 줄입니다. 이러한 변화들이 복합적으로 작용하여 DevOps와 SecOps 간의 피드백 루프가 강화되고, 단일 기능 제품 공급업체로 전환하는 데 드는 비용이 증가합니다.

AI를 활용한 자동 복구 엔진의 부상

현재, 인공지능(AI) 도구는 구성 그래프를 분석하여 비즈니스에 미치는 영향도를 기준으로 감지 결과를 순위별로 분류하고, Infrastructure-as-Code의 풀 리퀘스트를 통해 수정 작업을 수행합니다. 조기 도입 기업들에 따르면, 자동 생성된 시정 조치 덕분에 도입 후 90일 만에 처리되지 않은 클라우드 알림의 누적 건수가 절반으로 줄어드는 경우가 많다고 합니다. 결정론적 정책 엔진은 일반적인 모범 사례 조언이 아닌, 정확한 JSON 및 YAML 수정안을 제시함으로써 인적 오류를 줄여줍니다. 이러한 접근 방식은 전 세계 클라우드 보안 분야의 기술 격차를 해소하는 동시에, 수석 분석가들이 위협 감지에 집중할 수 있도록 해줍니다. 인터넷 서비스 제공업체에게 있어 시정 조치의 이행 정도는 명확한 차별화 요소가 됩니다. 왜냐하면 고객은 플랫폼이 무엇을 감지하는지뿐만 아니라, 수동 승인 절차를 거치지 않고 얼마나 신속하게 조치를 취할 수 있는지를 평가하기 때문입니다. 분석 레이어와 자동화 워크플로우를 모두 갖춘 벤더는 테넌트의 데이터량이 증가함에 따라 정확도가 향상되는 독자적인 머신러닝 모델을 통해 고객 유지율을 더욱 높일 수 있습니다.

SecOps 팀의 경보 피로와 기술 부족

리스크를 가시화한다는 측면에서 클라우드 보안 태세 관리가 성공을 거둔 결과, 많은 보안 운영 센터(SOC)가 이에 대응하느라 분주한 상황입니다. 기업들은 하루에 수천 건에 달하는 포스처 경보를 수신하는 경우가 많지만, 이를 선별할 분석가를 충분히 신속하게 채용하지 못하고 있습니다. 포티넷의 현장 데이터에 따르면, 대규모 팀조차도 매일 감지된 결과 중 극히 일부만 조사했으며, 설정 오류가 방치된 채로 남아 있으며, 이에 따라 도구에 대한 신뢰가 떨어지고 있습니다. 자동화를 통해 부담의 일부는 줄어들지만, CI/CD 파이프라인에 정책 조정 및 수정을 반영하기 위해서는 여전히 높은 수준의 전문 지식이 필요합니다. 그 결과, 매니지드 서비스 이용이 확대되고 있지만, 그 비용은 이미 사이버 보안 예산이 빠듯한 중소기업에게 큰 부담이 되고 있습니다.

부문별 분석

2025년, 솔루션 분야는 클라우드 보안 태세 관리(CSPM) 시장에서 66.45%의 점유율을 유지하고 있으며, 감지 및 보고 기능이 여전히 대다수의 구매자에게 있어 진입점 역할을 하고 있음이 확인되었습니다. 그러나 기업들이 경보를 영구적인 정책 변경으로 이어가는 데 따르는 운영상의 복잡성에 직면하고 있는 가운데, 서비스 분야는 2031년까지 연평균 성장률(CAGR) 15.12%로 확대되고 있습니다. 매니지드 서비스 파트너는 지속적인 튜닝, 맞춤형 규칙 설계, 연중무휴 24시간 트리아지 등의 서비스를 제공하고 있지만, 많은 팀에는 이를 수행할 내부 리소스가 부족합니다. 서비스 계약의 급증은 합병이나 규정 준수 인증에 앞서 이루어지는 포지션 평가에 대한 수요가 증가하고 있음을 반영하고 있으며, 컨설팅 기업들은 이 틈새 시장을 빠르게 수익화하고 있습니다. 따라서 플랫폼 공급업체들은 수익 유출을 막기 위해 서비스 제휴를 강화하거나 사내 자문팀을 구성하고 있습니다.

기술 격차의 확대는 특히 전임 클라우드 보안 아키텍트를 고용할 여력이 없는 중견 기업에서 서비스 이용을 더욱 촉진하고 있습니다. 시간 단위 과금이 아닌 성과 기반의 가격 책정으로 패키지화된 서비스를 제공하는 업체는 위험 감소라는 목표와 직결되기 때문에 지지를 얻고 있습니다. 예측 기간 동안 AI 기반 시정 조치를 위한 통합 서비스가 가장 빠른 성장세를 보일 것으로 전망됩니다. 이는 결정론적 정책 엔진이 운영 환경에서 의도파관 않은 구성 변경을 방지하기 위해 신중한 거버넌스가 필요하기 때문입니다.

2025년, 클라우드 보안 태세 관리(CSPM) 시장에서 IaaS(Infrastructure as a Service) 환경이 48.92%의 점유율을 차지하며, 가상 머신과 컨테이너 워크로드가 기존부터 지배적인 위치를 차지하고 있음이 드러났습니다. 그러나 SaaS 리소스는 15.2%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 이는 각 사업 부문이 기존의 경계를 벗어나 기밀 데이터를 저장하는 생산성 제품군, CRM 플랫폼, 협업 도구를 계속해서 도입하고 있기 때문입니다. SaaS 보안 태세 관리 모듈은 테넌트 수준 설정, 미사용 API 토큰, 과도한 공유 링크를 스캔함으로써 이러한 격차를 해소합니다. 이러한 기능을 도입한 기업들은 방치된 계정이나 타사 통합 기능이 비활성화되었을 때 위험이 급격히 감소한다는 사실을 확인하고 있습니다.

또한, 서버리스 및 관리형 데이터베이스 서비스의 보급에 따라 Platform as a Service(PaaS)도 주요 검토 대상으로 떠오르고 있습니다. 이 분야에서 보안 체계 관리를 위해서는 일시적인 기능이나 상황에 따른 최소 권한의 개념을 이해해야 합니다. 이는 상시 가동되는 서버를 전제로 하는 기존의 스크레이퍼로는 충분히 해결하지 못하고 있는 과제입니다. IaaS, PaaS, SaaS 모두에 걸쳐 일관된 정책 언어를 제공하는 벤더는 세 가지 별개의 툴 스택으로 인한 운영 부담을 줄여줌으로써 경영진의 지지를 얻고 있습니다. 이러한 변화로 인해, 클라우드 보안 태세 관리가 모든 클라우드 제공 모델을 아우르는 보편적인 제어 계층이라는 인식이 확고해졌습니다.

지역별 분석

북미는 클라우드 도입 성숙도가 높고, 보안 업체가 밀집해 있으며, 정부 기관 및 계약업체에 문서화된 구성 기준선을 유지할 것을 의무화하는 FedRAMP와 같은 엄격한 프레임워크 덕분에 2025년에도 매출 점유율 35.02%를 유지했습니다. 연방 정부의 제로 트러스트 프로그램에 대한 지속적인 투자가 플랫폼에 대한 지출을 뒷받침하는 한편, 건전한 벤처 생태계가 AI 기반 자동 수정 기능을 도입하는 혁신적인 스타트업에 자금을 지원하고 있습니다. 캐나다 기업들은 미국의 보안 기준을 점점 더 적극적으로 준수하고 있으며, 이로 인해 국경을 초월한 관리형 서비스 계약이 가능해지면서 해당 지역의 매출을 끌어올리고 있습니다.

아시아태평양은 각국 정부가 데이터 현지화 정책을 법제화하고, 현지 클라우드 데이터센터 건설에 대해 세제상의 우대 조치를 시행하고 있는 만큼, 15.55%라는 지역 내 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 일본, 인도, 호주의 대규모 국가 디지털화 프로젝트에서는 조달 지침에 클라우드 보안 체계에 대한 보고가 포함되어 있어, 사실상 정부가 지원하는 워크로드에 해당 도구를 도입하는 것이 의무화되어 있습니다. 한편, 2024년에 제정된 말레이시아 사이버보안법에서는 중요 분야의 사업자에 대한 지속적인 감시를 의무화하고 있으며, 이로 인해 벤더들의 동남아시아 시장 진출이 가속화되면서 현지 시스템 통합사업자들에게 채널 개척의 기회가 생기고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정)과 알고리즘에 의한 의사결정의 투명성을 요구하는 새로 채택된 인공지능 규제를 중심으로 한 복잡한 규정 준수 환경이 나타나고 있습니다. 따라서 기업들은 필요에 따라 여러 관할 구역에 걸친 감사 추적을 생성할 수 있는 보안 현황 대시보드를 요구하고 있습니다. 독일과 프랑스는 국내에서 데이터를 처리하도록 요구하는 ‘주권 클라우드 이니셔티브’를 주도하고 있으며, 서비스 제공업체들은 EU 전용 호스팅 구역을 개설해야 하는 압박을 받고 있습니다. 이와 동시에, 영국의 브렉시트 이후 규제 차이로 인해 듀얼 컴플라이언스 매핑에 대한 수요가 증가하고 있으며, 유연한 정책 엔진을 갖춘 플랫폼이 유리해지고 있습니다. 라틴아메리카와 중동 및 아프리카는 여전히 개발도상국이지만, 하이퍼스케일러의 지역 진출로 인해 현지 기업들이 최신 API를 이용할 수 있게 되는 등 매력적인 성장 지역으로 부상하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the cloud security posture management market size is projected to expand from USD 5.25 billion in 2025 and USD 6.04 billion in 2026 to USD 12.12 billion by 2031, registering a CAGR of 14.96% between 2026 to 2031.

This report is Segmented by Component (Solutions, and Services), Cloud Model (Infrastructure As A Service (IaaS), Platform As A Service (PaaS), and More), Deployment Mode (Public Cloud, Private Cloud, and More), Organization Size (Large Enterprises, and SMEs), Industry Vertical (BFSI, Healthcare, Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Cloud Security Posture Management Market Trends and Insights

Integration of CSPM into Cloud-Native Application Protection Platform (CNAPP) ecosystems

cloud security posture management is rapidly shifting from a standalone dashboard to a foundational module inside unified CNAPP suites, a change that relieves security teams from juggling overlapping consoles and policies. Aqua Security's decision to ship posture analytics alongside container and workload controls shows how a single policy plane can now trace misconfigurations from build to runtime This evolution is driving growth in the cloud security posture management market,Organizations deploying converged platforms report materially lower mean-time-to-remediate because alerts arrive already correlated with asset context and exploit pathways. The same console also pushes guardrails back into developer pipelines, which curbs drift before it reaches production resources. Integrations with identity governance modules further reduce hidden attack surfaces by exposing privilege creep inside cloud accounts. Collectively, these changes tighten the feedback loop between DevOps and SecOps and raise the switching costs for point-product providers.

Rise of AI-assisted auto-remediation engines

Artificial-intelligence tooling now reads configuration graphs, ranks findings by business impact, and triggers fixes through Infrastructure-as-Code pull requests. Early adopters note that auto-generated remediation often cuts the backlog of open cloud alerts in half during the first 90 days of use. Deterministic policy engines reduce human error by proposing precise JSON or YAML changes instead of generalized best-practice advice. The approach counters the global cloud-security skills gap and frees senior analysts to focus on threat hunting, For providers, remediation depth becomes a clear differentiator because customers evaluate not just what the platform detects but how quickly it can act without manual approval loops. Vendors that own both the analytics layer and the automation workflow gain further stickiness through proprietary machine-learning models that improve with tenant data volume.

Alert fatigue and skills shortage in SecOps teams

The very success of cloud security posture management in surfacing risk has overwhelmed many security operations centers. Enterprises often receive thousands of posture alerts per day and cannot hire analysts fast enough to triage them. Fortinet field data show that even large teams investigate only a fraction of daily findings, leaving misconfigurations unaddressed and eroding trust in the tooling. Automation alleviates part of the burden, yet significant expertise remains necessary to tune policies and integrate fixes into CI/CD pipelines. As a result, managed-service options grow in popularity, but their cost pressures smaller businesses already coping with tight cybersecurity budgets.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of zero-trust and shared-responsibility audits

- Regulatory push for real-time cloud-configuration reporting

- Tool overlap with CWPP and CIEM creating budget friction

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions segment retained 66.45% share of the Cloud Security Posture Management market in 2025, confirming that detection and reporting remain the entry point for most buyers. Yet the Services category is expanding at 15.12% CAGR through 2031 as enterprises confront the operational complexity of turning alerts into lasting policy change. Managed-service partners offer continuous tuning, custom rule engineering, and 24X7 triage, activities that many teams lack the internal bandwidth to perform. The surge in service contracts also reflects growing demand for posture assessments prior to mergers or compliance certifications, a niche that consulting firms are quick to monetize. Platform vendors therefore boost service alliances or build in-house advisory teams to prevent revenue leakage.

The widening skills gap further fuels service uptake, particularly among mid-market organizations that cannot afford full-time cloud-security architects. Providers that deliver packaged offerings with outcome-based pricing-rather than hourly billing-gain traction because they map directly to risk-reduction goals. Over the forecast horizon, integration services for AI-driven remediation should see the fastest growth, given that deterministic policy engines require careful governance to avoid unintended configuration changes in production environments.

Infrastructure as a Service environments held 48.92% share of the Cloud Security Posture Management market in 2025, underscoring the historical dominance of virtual-machine and container workloads. However, SaaS resources will log the highest 15.2% CAGR because business units continue to adopt productivity suites, CRM platforms, and collaboration tools that store sensitive data outside the traditional perimeter. SaaS Security Posture Management modules plug this gap by scanning tenant-level settings, unused API tokens, and excessive sharing links. Enterprises adopting these capabilities note rapid risk reduction when orphaned accounts and third-party integrations are disabled.

Platform as a Service also enters mainstream consideration as serverless and managed database services proliferate. Here, posture management must understand ephemeral functions and context-aware least privilege, tasks poorly addressed by legacy scrapers that assume persistent servers. Vendors that expose consistent policy languages across IaaS, PaaS, and SaaS win executive support by curbing the operational burden of three separate tooling stacks. The shift cements the perception of cloud security posture management as a universal control layer spanning the full spectrum of cloud-delivery models.

Geography Analysis

North America retained 35.02% revenue share in 2025 owing to mature cloud adoption, a dense concentration of security vendors, and stringent frameworks such as FedRAMP that push agencies and contractors to maintain documented configuration baselines. Continued federal investment in zero-trust programs sustains platform spending, while a healthy venture ecosystem funds disruptive start-ups that introduce AI-native remediation features. Canadian enterprises increasingly align with U.S. security standards, enabling cross-border managed-service deals that lift regional revenue.

Asia-Pacific will deliver the fastest regional CAGR at 15.55% as governments legislate data-localization practices and provide tax incentives for local cloud datacenter builds. Large-scale national digitization projects in Japan, India, and Australia embed cloud-security posture reporting in procurement guidelines, effectively mandating tool deployment in state-backed workloads. Meanwhile, the Malaysian Cyber Security Act of 2024 requires continuous monitoring for critical-sector operators, accelerating vendor entry into Southeast Asian markets and creating channel opportunities for local systems integrators.

Europe exhibits a complex compliance landscape anchored by GDPR and newly adopted artificial-intelligence regulations that demand transparency in algorithmic decision-making. Enterprises thus seek posture dashboards that can produce multi-jurisdiction audit trails on demand. Germany and France spearhead sovereign-cloud initiatives that call for in-country data processing, prompting providers to launch EU-only hosting zones. In parallel, the United Kingdom's post-Brexit regulatory divergence drives demand for dual compliance mappings, which favors platforms with flexible policy engines. Latin America, the Middle East, and Africa remain nascent but attractive expansion territories as hyperscaler region launches bring modern APIs within reach of local businesses.

- Palo Alto Networks

- Check Point Software Technologies

- Microsoft

- Trend Micro

- IBM

- Fortinet

- McAfee

- AWS

- Oracle

- Qualys

- Wiz

- Orca Security

- Lacework

- Aqua Security

- Tenable

- Cisco Systems

- VMware

- CrowdStrike

- Zscaler

- Rapid7

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Integration of CSPM into Cloud Native Application Protection Platform (CNAPP) platforms

- 4.2.2 Rise of AI-assisted auto-remediation engines

- 4.2.3 Expansion of zero-trust and shared-responsibility audits

- 4.2.4 Regulatory push for real-time cloud-config reporting

- 4.2.5 Multi-cloud sprawl in mid-market enterprises

- 4.2.6 Insurance-driven security scorecard requirements

- 4.3 Market Restraints

- 4.3.1 Alert-fatigue and skills shortage in SecOps teams

- 4.3.2 Tool overlap with CWPP / CIEM creating budget friction

- 4.3.3 Limited API depth for some SaaS/PaaS providers

- 4.3.4 Data-residency barriers in sovereign-cloud projects

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Compliance Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Cloud Model

- 5.2.1 Infrastructure as a Service (IaaS)

- 5.2.2 Platform as a Service (PaaS)

- 5.2.3 Software as a Service (SaaS)

- 5.3 By Deployment Mode

- 5.3.1 Public Cloud

- 5.3.2 Private Cloud

- 5.3.3 Hybrid Cloud

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By Industry Vertical

- 5.5.1 Banking Finance Services and Insurances (BFSI)

- 5.5.2 Healthcare

- 5.5.3 Retail and E-commerce

- 5.5.4 IT and Telecommunication

- 5.5.5 Government and Public Sector

- 5.5.6 Education

- 5.5.7 Manufacturing

- 5.5.8 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Palo Alto Networks

- 6.4.2 Check Point Software Technologies

- 6.4.3 Microsoft

- 6.4.4 Trend Micro

- 6.4.5 IBM

- 6.4.6 Fortinet

- 6.4.7 McAfee

- 6.4.8 AWS

- 6.4.9 Oracle

- 6.4.10 Qualys

- 6.4.11 Wiz

- 6.4.12 Orca Security

- 6.4.13 Lacework

- 6.4.14 Aqua Security

- 6.4.15 Tenable

- 6.4.16 Cisco Systems

- 6.4.17 VMware

- 6.4.18 CrowdStrike

- 6.4.19 Zscaler

- 6.4.20 Rapid7

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis