|

시장보고서

상품코드

2065782

유럽의 로봇 잔디깎기기계 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Robotic Lawn Mower - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

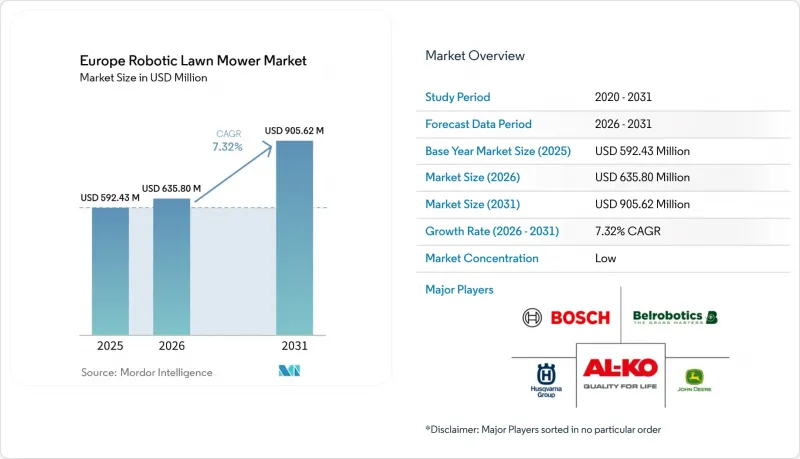

Mordor Intelligence에 의하면, 2026년 유럽 로봇 잔디깎기기계 시장 규모는 6억 3,580만 달러로 추정되고 있어 2025년 5억 9,243만 달러에서 확대해, 2031년에는 9억 562만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 7.32%로 성장할 것으로 전망됩니다.

본 보고서는 범위(단거리, 장거리, 기타), 배터리용량(20V 미만, 30V 이상, 기타), 판매 채널(소매점, 온라인, 기타), 용도(주거용 및 상업용), 최종 사용자(주택 소유자, 지자체, 기타), 연결 방식(경계선 방식, 시각 유도 방식, 기타) 및 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽 로봇 잔디깎이기계 시장 동향과 인사이트

시간을 절약해 주는 홈 오토메이션 기기에 대한 수요 증가

유럽의 주택 소유자들은 시간적 제약과 라이프스타일 선호도를 배경으로, 로봇 잔디깎기기계를 종합적인 스마트 홈 생태계에 통합하려는 추세가 강해지고 있습니다. 제조업체들이 기존의 홈 오토메이션 플랫폼과의 원활한 연동 기능을 개발하고, 음성 제어나 스마트폰을 통한 관리를 가능하게 함에 따라 이러한 추세는 더욱 가속화되고 있습니다. STIHL사의 ‘iMOW’ 시리즈는 스마트 홈 시스템과 음성 명령 기능을 통합하여, 통합된 자동화 경험을 원하는 소비자들 수요를 반영하고 있습니다. 이러한 통합은 기본적인 잔디 깎기에 그치지 않고, 기상 상황에 따른 일정 설정 및 유지보수 알림까지 포함하고 있습니다. 맞벌이 가구 증가와 같은 인구 동향의 변화로 인해, 주말에 잔디를 관리해야 하는 부담을 덜어주는 자율형 솔루션에 대한 수요가 높아지고 있습니다. 북유럽 시장의 스마트 홈 보급률은 로봇 잔디깎이기계 도입 동향과 직접적인 상관관계가 있으며, 기술에 대한 친숙도가 구매 결정의 요인이 되고 있음이 시사되고 있습니다.

배터리 구동 기기를 뒷받침하는 EU 그린딜의 인센티브

유럽연합(EU)의 규제 체계는 여러 정책 채널을 통해 배터리 구동식 로봇 잔디깎이기계에 구조적인 우위를 제공합니다. ‘넷 제로 산업법’은 청정 기술의 현지 생산을 우선시하는 반면, EU 규정 2023/1542에 근거한 새로운 배터리 규제는 화석 연료를 동력원으로 하는 대체품보다 전기 기기를 우대하는 지속가능성 요건을 규정하고 있습니다. 에코디자인 요건에 따라 제품 수명 주기 평가가 의무화되어 있으며, 높은 에너지 효율과 낮은 배출량 덕분에 로봇 잔디깎이기계는 본질적으로 유리한 입장에 있습니다. 가맹국들에서는 전동 원예 기기에 대한 세액 공제나 도시 지역에서의 가솔린식 공구 사용 제한 등, 이를 보완하기 위한 인센티브가 도입되어 있습니다. 이러한 규제의 기세는 기존 잔디깎이기계에 경쟁상의 불리함을 안겨주는 한편, 로봇 잔디깎이기계와 같은 대체 제품에게는 장기적인 시장 호재로 작용하고 있습니다. 또한, 새로운 체계에 따른 배터리 재활용 의무화는 지속 가능한 전력 시스템 분야의 혁신을 촉진하고, 순환 경제 추진에 투자하는 제조업체에 이익을 가져다주고 있습니다.

기존 잔디깎이기계에 비해 높은 초기 비용

가격에 대한 민감도는 여전히 로봇 잔디깎이기계 보급의 주요 걸림돌로 남아 있습니다. 특히, 가구 가처분 소득이 서유럽 수준에 미치지 못하는 동유럽 및 남유럽 시장에서는 이러한 경향이 두드러집니다. 고급형 경계선 불필요 모델은 3,000유로가 넘는 가격대에 속하며, 동급의 기존 잔디깎이기계보다 3-5배 비싼 가격입니다. 이러한 비용 차이는 대용량 시스템에서 가장 두드러지며, 첨단 GPS 내비게이션과 AI를 활용한 장애물 감지 기능이 가격을 크게 끌어올리고 있습니다. 합리적인 가격이라는 과제를 해결하기 위해 소비자 대상 대출 상품이나 리스 프로그램이 등장하고 있지만, 자동차나 가전 분야와 비교하면 그 보급은 여전히 제한적입니다. 총 소유 비용(TCO)을 계산할 때, 인건비 절감과 연료비를 고려하면 5-7년 기간 동안 로봇식 시스템이 더 유리한 경우가 많습니다. 그러나 소비자들은 대개 제품 수명 주기 전체에 걸친 경제성보다는 초기 구매 가격에 더 중점을 둡니다. 각 제조업체들은 시장 진입 장벽을 낮추기 위해 보급형 모델을 개발하고 있지만, 기능상의 제한으로 인해 요구 사항이 까다로운 사용자층에 대한 어필력이 제한될 가능성이 있습니다.

부문별 분석

2025년에는 중가형 로봇 잔디깎이기계가 44.10%라는 가장 높은 시장 점유율을 차지하고 있지만, 고가형 모델은 2031년까지 연평균 성장률(CAGR) 15.55%로 보급이 가속화되고 있습니다. 프리미엄 부문은 첨단 AI 내비게이션, 배터리 수명 연장, 종합적인 연결 기능 등 기술적 완성도가 높기 때문에 높은 가격 책정이 정당화됩니다. 저가형 모델은 가격에 민감한 소비자를 대상으로 하지만, 기능이 풍부한 대체 제품들로 인해 이익률이 압박받고 있습니다. 전문 조경 업체들은 비용 측면보다 신뢰성과 작업 범위의 폭이 더 중요시되는 상업용 분야에서 고급 시스템의 도입을 점점 더 늘리고 있습니다. 경계선 케이블이 필요 없는 기술로의 전환은 GPS를 통한 고정밀 위치 측정 및 장애물 감지 기능 덕분에 프리미엄 가격 책정이 가능한 하이엔드 부문에 이점을 가져다주고 있습니다. 허스크바나가 2025년에 13종의 새로운 경계선 케이블이 필요 없는 모델을 출시한 것은 이 회사가 프리미엄 시장 확대에 주력하고 있음을 보여줍니다.

이 제품 라인의 세분화는 얼리 어답터들이 기본 모델에서 기능이 풍부한 대체 제품으로 전환함에 따라 소비자의 요구가 점점 더 세분화되고 있음을 반영하고 있습니다. 중가대 제품은 프리미엄 가격을 지불하지 않고도 신뢰할 수 있는 자동화 기능을 원하는 교외 주택 소유주들에게 최적의 선택지가 되고 있으며, 이것이 해당 제품군이 시장에서 지배적인 위치를 차지하고 있는 이유를 설명해 줍니다. 고가 제품군의 성장 가속화는 고급 기능과 장기적인 신뢰성이라는 장점에 대한 가치 제안이 성공적으로 전달되고 있음을 시사합니다.

20-30V 모델은 2025년에 50.25%라는 가장 높은 시장 점유율을 차지하고 있지만, 30V를 초과하는 시스템은 2031년까지 연평균 성장률(CAGR) 13.2%를 기록하며 기술적 변화를 주도하고 있습니다. 고전압 시스템은 가동 시간 연장, 충전 시간 단축, 험한 지형에서의 수확 성능 향상을 가능하게 하여, 까다로운 사용자들 사이에서 도입이 확대되고 있습니다. 20V 미만 모델은 소형 잔디 관리 용도에 적합하지만, 더 고성능인 대체 제품들로부터의 경쟁 압박에 직면해 있습니다. 이러한 전압의 발전은 단위 중량당 성능이 뛰어난 대용량 리튬이온 시스템으로의 전환이라는 전동 공구 업계 전반의 동향과 맞물려 있습니다. STIHL의 배터리 제품 전략에 따르면, 2027년까지 매출의 35%를 배터리 구동 공구가 차지하도록 하는 것을 목표로 하고 있으며, 이는 해당 기업이 대용량 시스템에 주력하고 있음을 보여줍니다.

리튬 이온 배터리 생산에서 나타나는 규모의 경제 효과로 인해 고전압 시스템의 비용 프리미엄이 줄어들고 있으며, 이에 따라 시장의 전환이 가속화되고 있습니다. 또한, 용량별 세분화는 유럽 시장의 잔디 면적 분포를 반영하고 있으며, 교외의 광활한 부지에서는 가동 시간 연장이 점점 더 요구되고 있습니다. EU 규정 2023/1542에 따른 배터리 재활용 규제는 일회용 저전압 제품보다 지속 가능하고 대용량 시스템에 투자하는 제조업체를 우대하는 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the europe robotic lawn mower market size in 2026 is estimated at USD 635.8 million, growing from 2025 value of USD 592.43 million with 2031 projections showing USD 905.62 million, growing at 7.32% CAGR over 2026-2031.

This report is Segmented by Range (Low Range, High Range, and More), Battery Capacity (Less Than 20 V, More Than 30 V, and More), Sales Channel (Retailers, Online, and More), Application (Residential and Commercial), End-User (Homeowners, Municipalities, and More), Connectivity (Boundary-Wire, Vision-Guided, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Europe Robotic Lawn Mower Market Trends and Insights

Rising Demand for Time-Saving Home-Automation Devices

European homeowners increasingly integrate robotic lawn mowers into comprehensive smart home ecosystems, driven by time constraints and lifestyle preferences. The trend accelerates as manufacturers develop seamless connectivity with existing home automation platforms, enabling voice control and smartphone management. STIHL's iMOW series now integrates smart home systems and voice command capabilities, reflecting consumer demand for unified automation experiences. This integration extends beyond basic mowing to include weather-responsive scheduling and maintenance alerts. The demographic shift toward dual-income households amplifies demand for autonomous solutions that eliminate weekend lawn care obligations. Smart home penetration rates in Northern European markets correlate directly with robotic mower adoption patterns, suggesting that technology familiarity drives purchase decisions.

EU Green Deal Incentives Favoring Battery-Powered Equipment

The European Union's regulatory framework creates structural advantages for battery-powered robotic mowers through multiple policy channels. The Net Zero Industry Act prioritizes local manufacturing of clean technologies, while new battery regulations under EU 2023/1542 establish sustainability requirements that favor electric equipment over fossil fuel alternatives. Ecodesign requirements mandate product lifecycle assessments that inherently favor robotic mowers due to their energy efficiency and reduced emissions profiles. Member states are implementing complementary incentives, including tax credits for electric garden equipment and restrictions on gas-powered tools in urban areas. The regulatory momentum creates competitive disadvantages for conventional mowers while establishing long-term market tailwinds for robotic alternatives. Battery recycling mandates under the new framework also drive innovation in sustainable power systems, benefiting manufacturers investing in circular economy approaches.

High Upfront Cost Versus Conventional Mowers

Price sensitivity remains the primary barrier to robotic mower adoption, particularly in Eastern and Southern European markets where household disposable income lags Western European levels. Premium boundary wire-free models command prices exceeding EUR 3,000, representing 3-5 times the cost of equivalent conventional mowers. The cost differential is most pronounced for larger-capacity systems, where advanced GPS navigation and AI-powered obstacle detection drive significant price premiums. Consumer financing options and leasing programs are emerging to address affordability constraints, though adoption remains limited compared to the automotive or appliance sectors. The total cost of ownership calculation often favors robotic systems over 5-7 year periods when factoring labor savings and fuel costs. Yet, consumers typically focus on initial purchase price rather than lifecycle economics. Manufacturers are developing entry-level models to expand market accessibility, though feature limitations may constrain appeal among demanding users.

Other drivers and restraints analyzed in the detailed report include:

- Ageing Homeowner Population Boosting Demand for Low-Effort Lawn Care

- Construction of Smart-Homes with Integrated Turf-Management Hubs

- Theft-Vulnerability in Shared-Housing and Urban Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium-range robotic mowers hold the largest market share at 44.10% in 2025, while high-range models are experiencing accelerated adoption with a CAGR of 15.55% through 2031.The premium segment benefits from technological sophistication, including advanced AI navigation, extended battery life, and comprehensive connectivity features that justify higher price points. Low-range models serve price-sensitive consumers but face margin pressure from feature-rich alternatives. Professional landscapers increasingly specify high-end systems for commercial applications where reliability and coverage capacity outweigh cost considerations. The shift toward boundary wire-free technology benefits high-end segments where GPS precision and obstacle detection capabilities command premium pricing. Husqvarna's launch of 13 new boundary wire-free models in 2025 demonstrates the manufacturer's focus on premium market expansion.

The range segmentation reflects evolving consumer sophistication as early adopters graduate from basic models to feature-rich alternatives. Medium-range products occupy the sweet spot for suburban homeowners seeking reliable automation without premium pricing, explaining their dominant market position. High-range growth acceleration suggests successful value proposition communication around advanced features and long-term reliability benefits.

The 20 to 30V models hold the largest market share at 50.25% in 2025, while more-than-30V systems drive a technological transition with a CAGR of 13.2% through 2031. Higher-voltage systems enable extended runtime, faster charging, improved cutting performance on challenging terrain, driving adoption among demanding users. Less-than-20V models serve compact lawn applications but face competitive pressure from more capable alternatives. The voltage evolution parallels broader power tool industry trends toward higher-capacity lithium-ion systems that deliver superior performance per unit weight. STIHL's battery product strategy targets 35% of sales from battery-operated tools by 2027, indicating the manufacturer's commitment to higher-capacity systems.

Manufacturing economies of scale in lithium-ion production are reducing cost premiums for higher-voltage systems, accelerating market transition. The capacity segmentation also reflects lawn size distributions across European markets, where larger suburban properties increasingly demand extended runtime capabilities. Battery recycling regulations under EU 2023/1542 favor manufacturers investing in sustainable, higher-capacity systems over disposable, lower-voltage alternatives.

List of Companies Covered in this Report:

- Husqvarna Group

- Robert Bosch GmbH

- ANDREAS STIHL AG and Co. KG

- Deere and Company

- STIGA S.p.A.

- Positec Tool Corp. (WORX)

- Honda Motor Co., Ltd.

- AL-KO Gardentech

- Belrobotics

- Zucchetti Centro Sistemi (Ambrogio)

- Segway Inc.

- The Toro Company

- Stanley Black and Decker (Craftsman)

- WIPER S.R.L.

- Greenworks Tools

- MTD Products (Cub Cadet, Kress)

- Makita Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Time-Saving Home-Automation Devices

- 4.2.2 EU Green Deal Incentives Favouring Battery-Powered Equipment

- 4.2.3 Edge-Vision AI Enabling Boundary-Wire-Free Installation

- 4.2.4 Construction of Smart-Homes With Integrated Turf-Management Hubs

- 4.2.5 Ageing Homeowner Population Boosting Demand for Low-Effort Lawn Care

- 4.2.6 Shift to Subscription/Robot-as-a-Service Business Models

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost Versus Conventional Mowers

- 4.3.2 Theft-Vulnerability in Shared-Housing and Urban Settings

- 4.3.3 Limited Cutting Efficiency on Steep or Multi-Tier Lawns

- 4.3.4 Fragmented EU Safety Standards Delaying Pan-EU Launches

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Range

- 5.1.1 Low Range

- 5.1.2 Medium Range

- 5.1.3 High Range

- 5.2 By Battery Capacity

- 5.2.1 Less Than 20 V

- 5.2.2 20 to 30 V

- 5.2.3 More Than 30 V

- 5.3 By Sales Channel

- 5.3.1 Retailers

- 5.3.2 Specialty Stores

- 5.3.3 Online

- 5.4 By Application

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By End-User

- 5.5.1 Homeowners

- 5.5.2 Landscaping Companies

- 5.5.3 Sports Grounds and Parks

- 5.5.4 Municipalities

- 5.5.5 Golf Courses

- 5.5.6 Others

- 5.6 By Connectivity

- 5.6.1 Boundary-Wire

- 5.6.2 Smart-GPS / Wi-Fi

- 5.6.3 Vision-Guided (Camera/LiDAR)

- 5.7 By Country

- 5.7.1 Germany

- 5.7.2 United Kingdom

- 5.7.3 France

- 5.7.4 Italy

- 5.7.5 Spain

- 5.7.6 Sweden

- 5.7.7 Netherlands

- 5.7.8 Belgium

- 5.7.9 Austria

- 5.7.10 Switzerland

- 5.7.11 Poland

- 5.7.12 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Husqvarna Group

- 6.4.2 Robert Bosch GmbH

- 6.4.3 ANDREAS STIHL AG and Co. KG

- 6.4.4 Deere and Company

- 6.4.5 STIGA S.p.A.

- 6.4.6 Positec Tool Corp. (WORX)

- 6.4.7 Honda Motor Co., Ltd.

- 6.4.8 AL-KO Gardentech

- 6.4.9 Belrobotics

- 6.4.10 Zucchetti Centro Sistemi (Ambrogio)

- 6.4.11 Segway Inc.

- 6.4.12 The Toro Company

- 6.4.13 Stanley Black and Decker (Craftsman)

- 6.4.14 WIPER S.R.L.

- 6.4.15 Greenworks Tools

- 6.4.16 MTD Products (Cub Cadet, Kress)

- 6.4.17 Makita Corp.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment