|

시장보고서

상품코드

2066370

클라우드 고성능 컴퓨팅(HPC) 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cloud High Performance Computing (HPC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

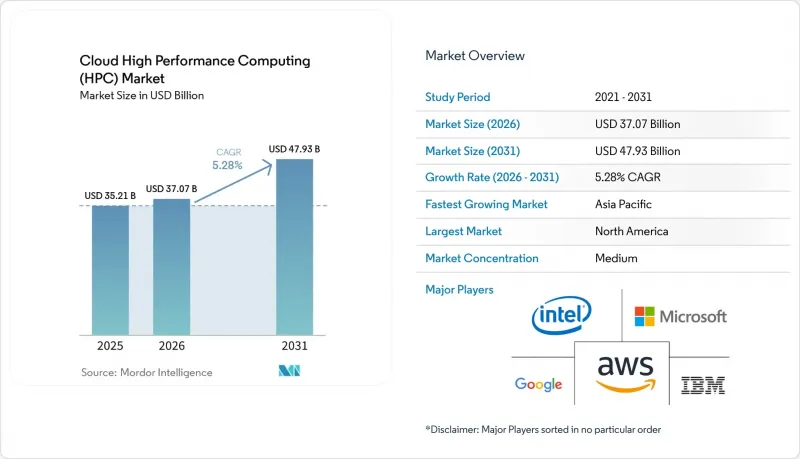

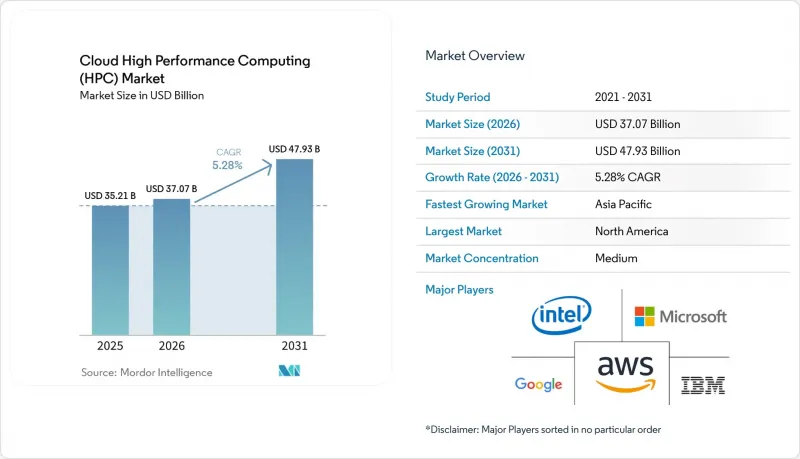

Mordor Intelligence에 의하면, 클라우드 고성능 컴퓨팅 시장 규모는 2025년에 352억 1,000만 달러로 평가되었고 2026년 370억 7,000만 달러에서 2031년까지 479억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.28%를 나타낼 전망입니다.

본 보고서는 구성 요소(하드웨어, 소프트웨어, 서비스), 배포 모델(퍼블릭 클라우드 등), 서비스 모델(Infrastructure As A Service 등), 산업 분야(항공우주 및 방위 등), 조직 규모(대기업, 중소기업) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 클라우드 고성능 컴퓨팅(HPC) 시장 동향과 인사이트

클라우드 HPC에서 AI 및 생성형 워크로드의 급증

현재 인공지능(AI) 훈련은 클라우드 HPC의 총 사이클 수의 40%를 차지하고 있으며, 이는 2022년의 15%에서 크게 증가한 수치입니다. 이러한 급증은 트랜스포머 기반 언어 모델과 비전 모델이 막대한 계산 자원을 필요로 하는 특성을 반영한 것입니다. 대규모 배치 크기, 분산형 데이터 병렬 알고리즘 및 미세 조정된 하이퍼파라미터 탐색을 위해서는 한 번에 수천 대의 GPU를 며칠 동안 지속적으로 사용해야 하지만, 이러한 요구 사항은 On-Premise의 고정 용량과는 양립할 수 없습니다. 따라서 클라우드 플랫폼에서는 모델 훈련을 위해 즉시 가동하고, 검증 완료 즉시 중지할 수 있는 탄력적인 클러스터를 제공함으로써 유휴 자본을 최소화하고 있습니다. 2024년, 아마존 웹 서비스(AWS)는 확장 가능한 AI 지원 미디어 렌더링을 위한 ‘Deadline Cloud’를 출시하며, 워크로드에 특화된 서비스의 완성도를 보여주었습니다. 방위 기관과 제약 기업도 비슷한 경향을 보이고 있으며, 언어 기반 분자 설계나 자율주행차의 인식 파이프라인에 클라우드 슈퍼컴퓨팅을 활용함으로써 연구개발 주기를 단축하고, 인사이트를 얻기까지 걸리는 시간을 단축하고 있습니다.

고대역폭 상호 연결 및 가속기의 급속한 확대

NVIDIA Quantum-2 InfiniBand나 새롭게 등장한 800기가비트 이더넷 링크와 같은 차세대 패브릭은 현재 마이크로초 수준의 지연 시간을 실현하고 있어, 밀접하게 결합된 메시지 전달형 용도이 성능 저하를 크게 초래하지 않고 클라우드 환경에서 실행될 수 있게 되었습니다. NVIDIA 기반의 Grace Hopper 슈퍼칩이나 인텔의 데이터센터용 GPU인 Ponte Vecchio로 대표되는 GPU의 발전 덕분에, 노드당 처리량이 향상되는 동시에 에너지 효율도 개선되고 있습니다. 각 하이퍼스케일러 기업들은 연산, 메모리, 네트워크 흐름 간의 균형을 맞추기 위해 맞춤형 ASIC 통합을 점점 더 확대하고 있으며, 이를 통해 상용 클라우드와 국립 연구소의 슈퍼컴퓨터 사이에 기존에 존재하던 격차를 효과적으로 해소하고 있습니다. 이러한 기술적 도약은 고밀도 및 저지연 노드 간 상호 연결에 의존하는 기상 예측, 충돌 시뮬레이션, 지진파 이미징 솔루션에 있어 매우 중요합니다.

클라우드 아웃바운드 전송 및 데이터 마이그레이션 비용의 급등

멀티페타바이트 규모의 시뮬레이션에서는 데이터 전송 비용이 컴퓨팅 비용의 200%를 초과하는 경우도 있어, 온디맨드 리소스를 통해 실현된 비용 절감 효과가 상쇄되어 버립니다. 유전체 분석 파이프라인, 지진파 이미징, 고밀도 몬테카를로 워크로드의 경우, 중간 파일이 오브젝트 스토리지, 데이터베이스, 하류 분석 플랫폼 사이를 반복적으로 오가기 때문에 반복할 때마다 데이터 전송 비용이 급증합니다. 각 하이퍼스케일러 기업들은 할인 요금 조사용 채널이나 오프라인 전송 어플라이언스를 도입하고 있지만, 근본적인 비용 측면의 과제는 여전히 남아 있습니다. 따라서 조직에서는 데이터의 왕복 횟수를 최소화하는 아키텍처를 선택하거나, 인-시추 분석을 도입하거나, 시뮬레이션 노드 근처에 후처리 환경을 배치하는 방안 등을 검토하고 있지만, 이러한 해결책들은 모두 운영상의 새로운 복잡성을 수반합니다.

부문별 분석

하드웨어는 2025년 매출의 44.12%를 차지하고 있으며, 이는 GPU, 고대역폭 메모리, NVMe 지원 스토리지 어레이를 탑재한 데이터센터 랙의 자본 집약적 특성을 여실히 보여주고 있습니다. NVIDIA는 클라우드 제공업체가 자사의 가장 빠르게 성장하는 상업 채널임을 확인했으며, 이는 가속기 및 상호 연결 스위치에 대한 지속적인 투자를 뒷받침하는 것입니다. 플릿 운영자들이 테라플롭당 전력 소비 감소를 추구하는 가운데, 각 벤더들은 노드 밀도, 에너지 효율, 그리고 열적으로 최적화된 폼 팩터를 차별화의 핵심 요소로 삼고 있습니다.

한편, 소프트웨어 분야는 가장 높은 성장세를 보이고 있으며, 2031년까지의 연평균 성장률(CAGR)은 8.42%로 예측됩니다. 이는 리소스 할당을 실시간으로 조정하는 스케줄러, AI를 활용한 성능 프로파일러, 그리고 멀티클라우드 및 하이브리드 환경을 아우르는 워크플로우 관리자에 의해 주도되고 있습니다. 소프트웨어 분야의 클라우드 고성능 컴퓨팅(HPC) 시장 확대는 실제 사용 시간에 따라 비용을 조정하는 구독형 라이선싱 모델에 힘입어, 이에 따라 예산이 자본 지출에서 운영비로 전환되고 있습니다.

퍼블릭 클라우드는 2025년에 67.95%의 시장 점유율을 차지해, 미디어 렌더링, 컴퓨터 지원 엔지니어링, 생명과학 분야의 검색에서 두드러지는 탄력적인 프로젝트 기반의 시뮬레이션 집중 처리 플랫폼으로서의 역할을 계속하고 있습니다. 각 프로바이더는 세분화된 과금 미터 제공, 긴급성이 낮은 작업에 대한 스팟 풀 활용, 데이터 소재지 관련 법규 준수를 위한 리저널 존 유지를 통해 워크로드를 확보하고 있습니다.

프라이빗 클라우드는 규모는 작지만, 규제가 엄격한 업계에서 결정론적인 지연 시간과 주권적인 제어를 중시하는 가운데 연평균 성장률(CAGR) 7.52%를 나타낼 것으로 전망됩니다. 기업들은 하이퍼스케일 데이터센터의 탄력성을 모방하면서도 에어갭 방식의 보안을 유지하는 컨버지드 HPC 어플라이언스를 기반으로 사내 클라우드를 구축하고 있습니다. 하이브리드 오케스트레이터는 이러한 환경을 통합하고, 비용 곡선과 큐의 깊이를 기반으로 작업을 할당하는 단일 작업 제출 포털을 사용자에게 제공합니다.

지역별 분석

북미는 2025년에도 39.94%의 점유율을 유지했습니다. 이는 고밀도 하이퍼스케일 인프라와 클라우드 우선 아키텍처를 정당화하는 연방 정부 주도의 엑사스케일 이니셔티브에 힘입은 것입니다. 방위 및 우주 기관의 지속적인 개선 자금이 첨단 시뮬레이션에 대한 꾸준한 수요를 뒷받침하고 있으며, 반도체 설계, 자율 시스템, 디지털 미디어로 구성된 활기찬 상업 생태계가 이 지역의 리더십을 공고히 하고 있습니다. 데이터 수출 및 암호화에 관한 규제가 명확해짐에 따라, 규제가 엄격한 업계에서 클라우드 HPC 도입이 더욱 가속화되고 있습니다.

아시아태평양은 각국 정부가 국가 주도의 AI 및 반도체 설계 역량 구축에 수십억을 투자하고 있어, 연평균 성장률(CAGR) 8.77%라는 가장 높은 미래 성장률을 기록하고 있습니다. 중국은 첨단 가속기 수출 규제에도 불구하고, 국산 GPU 대체품 및 양자·고전 하이브리드 센터에 대한 투자를 통해 클라우드 HPC 예산을 증액하고 있습니다. 일본은 HPC 로드맵을 ‘사회 5.0’과 연계하여, 스마트 제조를 위한 엣지에서 클라우드로의 통합을 추진하고 있습니다. 한편, 인도의 ‘디지털 공공 인프라’ 이니셔티브는 지역 방언을 활용한 대규모 언어 모델링에 대한 수요를 창출하고 있습니다. 지역 통신 사업자들은 하이퍼스케일러와 제휴하여 국내에 가용성 구역을 호스팅함으로써, 데이터의 지역성에 대한 우려를 완화하고 더 광범위한 시장 진출을 촉진하고 있습니다.

유럽은 EU 역내 페타스케일 시스템에 공동 투자하는 ‘유럽 고성능 컴퓨팅 공동 사업(EHPC)’의 지원을 받아, 견조하면서도 보다 신중한 궤도를 밟고 있습니다. 독일의 자동차 제조업체는 공장 내 클러스터의 용량 한계에 도달했을 때, 공기역학 시뮬레이션을 클라우드 인스턴스로 오프로드하고 있으며, 북유럽의 재생에너지 사업자는 풍부한 수력발전을 활용한 저탄소 데이터센터를 운영하고 있습니다. GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정) 준수가 하이브리드형 도입 방식을 촉진하고 있으며, 기밀성이 높은 텔레메트리 데이터는 On-Premise에서 보관하는 한편, 대규모 실험 설계 실행에는 클라우드의 확장성을 활용하고 있습니다. 각국의 디지털 전략과 탄소 중립 목표가 맞물려 조달 모델에 영향을 미치며, 친환경 인증을 받은 클라우드 리전의 도입을 촉진하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the cloud high performance computing market size was valued at USD 35.21 billion in 2025 and estimated to grow from USD 37.07 billion in 2026 to reach USD 47.93 billion by 2031, at a CAGR of 5.28% during the forecast period (2026-2031).

This report is Segmented by Component (Hardware, Software, and Services), Deployment Model (Public Cloud, and More), Service Model (Infrastructure As A Service, and More), Industrial Application (Aerospace and Defense, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Cloud High Performance Computing (HPC) Market Trends and Insights

Surging AI and Generative Workloads in Cloud HPC

Artificial intelligence training now consumes 40% of total cloud HPC cycles, up from 15% in 2022, a leap that reflects the compute-hungry nature of transformer-based language and vision models. Large batch sizes, distributed data-parallel algorithms, and fine-tuned hyper-parameter searches require thousands of GPUs for days at a time, conditions that correlate poorly with fixed on-premises capacity. Cloud platforms, therefore, supply elastic clusters that can be spun up for model training and spun down once validation is complete, minimizing idle capital. In 2024, Amazon Web Services released Deadline Cloud for scalable AI-assisted media rendering, signaling the depth of workload-tailored offerings. Defense and pharmaceutical organizations follow a similar pattern, utilizing cloud supercomputing for language-driven molecular design and autonomous vehicle perception pipelines, thereby shortening R&D loops and compressing time-to-insight.

Rapid Expansion of High-Bandwidth Interconnects and Accelerators

Next-generation fabrics, such as NVIDIA Quantum-2 InfiniBand and emerging 800-Gigabit Ethernet links, now deliver microsecond-level latency, enabling tightly coupled message-passing applications to run in the cloud without significant performance penalties. GPU advances, led by NVIDIA-based Grace Hopper superchips and Intel's Ponte Vecchio data-center GPUs, increase per-node throughput while improving energy efficiency.Hyperscalers are increasingly integrating custom ASICs to balance compute, memory, and network flows, effectively bridging the historical gaps between commercial clouds and national lab supercomputers. These technical leaps are pivotal for weather prediction, crash simulation, and seismic imaging solutions that rely on dense, low-latency node interconnects.

Elevated Cloud Egress and Data-Movement Costs

For multi-petabyte simulations, outbound data charges can eclipse compute fees by 200%, eroding the savings realized from on-demand resources. Genomics pipelines, seismic imaging, and high-density Monte Carlo workloads repeatedly shuttle intermediate files between object stores, databases, and downstream analytics platforms, amplifying the egress bill with each iteration. While hyperscalers have introduced reduced-tariff research channels and offline transfer appliances, the foundational economics remain challenging. Organizations therefore weigh architecture choices that minimize data round-trips, adopt in-situ analytics, or colocate post-processing near the simulation nodes, yet each workaround carries new operational complexity.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Hybrid and Multicloud HPC Strategies

- Increasing Availability of HPC-Optimized Cloud Instances

- Talent Shortage in Cloud-Native HPC Operations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware contributed 44.12% of 2025 revenue, underscoring the capital-intensive nature of datacenter racks loaded with GPUs, high-bandwidth memory, and NVMe-backed storage arrays. NVIDIA confirmed that cloud providers form its fastest-growing commercial channel, a testament to ongoing spending on accelerators and interconnect switches. Vendors anchor differentiation around node density, energy efficiency, and thermally optimized form factors, as fleet operators chase lower watts per teraflop.

Software, however, posts the highest momentum, with an expected 8.42% CAGR through 2031, driven by schedulers that tune allocations in real-time, AI-assisted performance profilers, and workflow managers that span multicloud and hybrid estates. The expansion of the Cloud High Performance Computing market size on the software side also benefits from subscription licensing models that align costs with active use minutes, shifting budgets from capital to operating expenses.

The public cloud garnered 67.95% share in 2025 and remains the backbone for elastic, project-based simulation bursts that characterize media rendering, computer-aided engineering, and life sciences searches. Providers win workloads by exposing granular billing meters, utilizing spot pools for non-urgent jobs, and maintaining regional zones to comply with data-residency laws.

Private cloud, while smaller, is projected to log a 7.52% CAGR as regulated verticals emphasize deterministic latency and sovereign control. Enterprises craft internal clouds atop converged HPC appliances that mimic the elasticity of hyperscale data centers while maintaining air-gapped security. Hybrid orchestrators integrate these estates, presenting users with a single submission portal that assigns jobs based on cost curves and queue depth.

Geography Analysis

North America retained 39.94% share in 2025, supported by dense hyperscale footprints and federally backed exascale initiatives that validate cloud-first architectures. Continuous improvement funds from defense and space agencies feed sustained demand for advanced simulation, while a vibrant commercial ecosystem of semiconductor design, autonomous systems, and digital media consolidates regional leadership. Regulatory clarity regarding data export and encryption further accelerates cloud HPC adoption in heavily controlled industries.

The Asia-Pacific region records the highest forward growth at a 8.77% CAGR as governments earmark billions for sovereign AI and semiconductor design capacity. China increases cloud HPC budgets despite export constraints on advanced accelerators by investing in homegrown GPU alternatives and quantum-classical hybrid centers. Japan aligns HPC roadmaps with Society 5.0, pushing edge-to-cloud integration for smart manufacturing, while India's Digital Public Infrastructure initiative creates demand for large-scale language modeling in regional dialects. Regional telcos partner with hyperscalers to host in-country availability zones, alleviating data-locality concerns and facilitating broader market entry.

Europe commands a strong though more measured trajectory, aided by the European High-Performance Computing Joint Undertaking that co-finances petascale systems within EU borders. Automotive OEMs in Germany offload aerodynamic simulations to cloud instances when factory clusters max out, and renewable energy operators in the Nordics harness low-carbon datacenters driven by abundant hydro power. GDPR compliance stimulates hybrid adoption patterns, keeping sensitive telemetry on-premises but using cloud scale for large design-of-experiments runs. National digital strategies and carbon-neutral targets jointly influence procurement models, nudging adoption toward green-certified cloud regions.

- Amazon Web Services Inc.

- Microsoft Corporation

- Google LLC

- International Business Machines Corporation

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Lenovo Group Limited

- NEC Corporation

- Fujitsu Limited

- Sugon Information Industry Co. Ltd.

- Atos SE

- Dassault Systemes SE

- Oracle Corporation

- Huawei Technologies Co., Ltd.

- Alibaba Group Holding Limited (Alibaba Cloud)

- Rescale Inc.

- Penguin Computing Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging AI and Generative Workloads in Cloud HPC

- 4.2.2 Rapid Expansion of High-Bandwidth Interconnects and Accelerators

- 4.2.3 Growing Adoption of Hybrid and Multicloud HPC Strategies

- 4.2.4 Increasing Availability of HPC-Optimized Cloud Instances

- 4.2.5 Demand for Sustainability-Focused HPC Infrastructure

- 4.2.6 Government-Funded Exascale and Sovereign AI Initiatives

- 4.3 Market Restraints

- 4.3.1 Elevated Cloud Egress and Data-Movement Costs

- 4.3.2 Talent Shortage in Cloud-Native HPC Operations

- 4.3.3 Export Controls on Advanced Accelerators

- 4.3.4 Latency-Sensitive Workloads Still Favor On-Premises Clusters

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Servers

- 5.1.1.2 Storage

- 5.1.1.3 Networking Devices

- 5.1.1.4 Accelerators (GPUs/TPUs)

- 5.1.2 Software

- 5.1.3 Services

- 5.1.1 Hardware

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By Service Model

- 5.3.1 Infrastructure as a Service (IaaS)

- 5.3.2 Platform as a Service (PaaS)

- 5.3.3 Software as a Service (SaaS)

- 5.3.4 Managed HPC Services

- 5.4 By Industrial Application

- 5.4.1 Aerospace and Defence

- 5.4.2 Energy and Utilities

- 5.4.3 Banking, Financial Services and Insurance

- 5.4.4 Media and Entertainment

- 5.4.5 Manufacturing

- 5.4.6 Life Science and Healthcare

- 5.4.7 Academic and Research

- 5.4.8 Government

- 5.4.9 Other Industrial Applications

- 5.5 By Organization Size

- 5.5.1 Large Enterprises

- 5.5.2 Small and Medium Enterprises

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Google LLC

- 6.4.4 International Business Machines Corporation

- 6.4.5 Hewlett Packard Enterprise Company

- 6.4.6 Dell Technologies Inc.

- 6.4.7 NVIDIA Corporation

- 6.4.8 Advanced Micro Devices Inc.

- 6.4.9 Intel Corporation

- 6.4.10 Lenovo Group Limited

- 6.4.11 NEC Corporation

- 6.4.12 Fujitsu Limited

- 6.4.13 Sugon Information Industry Co. Ltd.

- 6.4.14 Atos SE

- 6.4.15 Dassault Systemes SE

- 6.4.16 Oracle Corporation

- 6.4.17 Huawei Technologies Co., Ltd.

- 6.4.18 Alibaba Group Holding Limited (Alibaba Cloud)

- 6.4.19 Rescale Inc.

- 6.4.20 Penguin Computing Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment