|

시장보고서

상품코드

2066390

미국의 종자 처리 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

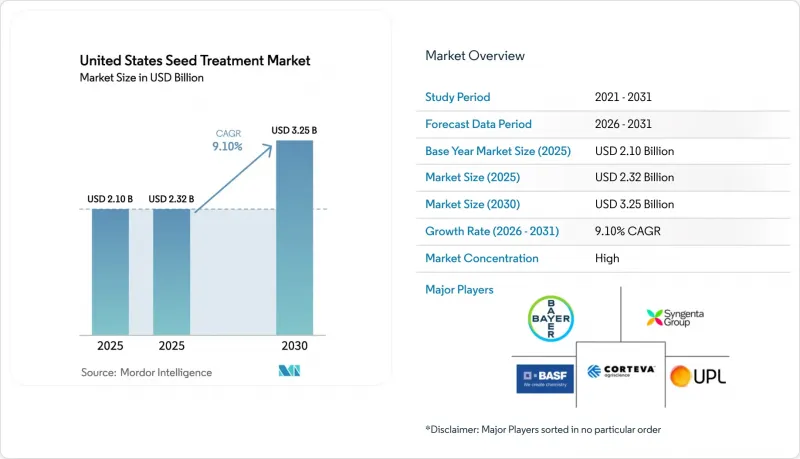

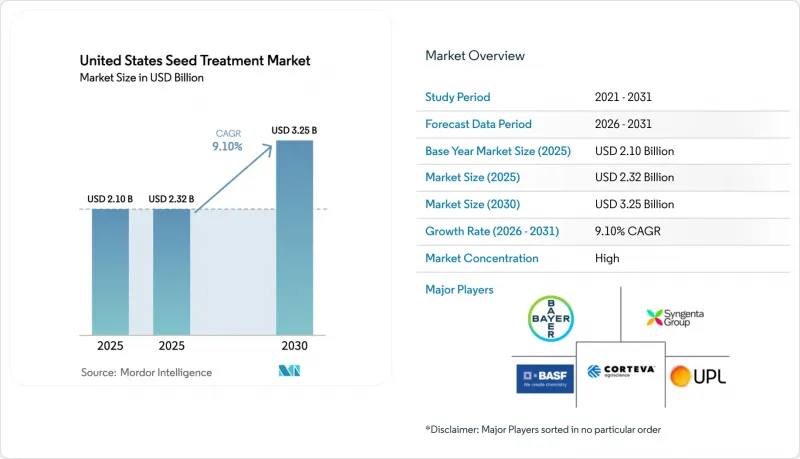

Mordor Intelligence에 의하면, 미국의 종자 처리 시장 규모는 2025년에 21억 달러로 평가되었고, 2026년 23억 2,000만 달러로 추정되고, 2031년까지 32억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 9.10%를 나타낼 전망입니다.

본 보고서는 제품 유형별(살균제, 살충제, 선충제) 및 작물 유형별(상업용 작물, 과일 및 채소, 곡물, 콩류 및 지방종자, 잔디 및 관상용 식물)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 종자 처리 시장 동향 및 인사이트

기존 농약에 대한 규제 압력

미국 환경보호청(EPA)은 2024년 7월, 클로티아니딘, 이미다클로프리드, 티아메톡삼에 대한 직업적 노출 평가를 갱신하고, 엽면 살포용 네오니코티노이드계 농약에 대한 규정 준수 부담을 강화하는 한편, 생산자들을 종자 처리형 대체품으로 유도하고 있습니다. 2025년에 예정된 라벨 개정에서는 광범위한 완충지대 설정과 전면 살포 시 더욱 엄격한 개인 보호구 착용이 의무화될 전망이며, 이에 따라 종자 처리가 규제 측면에서 저항이 가장 적은 선택지라는 인식이 더욱 강해지고 있습니다. 멸종 위기 종 보호법에 따른 협의가 장기화되면서 제초제 승인 절차는 이미 지연되고 있으며, 새로운 엽면 살포용 살충제에 대해서도 유사한 장애가 발생할 것으로 예측됩니다. 종자용 제제 제조업체들은 재등록 기간이 짧다는 점을 활용하여, 기존의 유효 성분을 종자 전용 제제로 재조제함으로써 시장 출시까지의 기간을 단축하고 있습니다. 그 결과, 전용 종자용 제제 플랫폼에 투자하고 있는 기업들은 시장 출시 속도의 우위뿐만 아니라, 취급 시 주의사항이 적은 제품을 선호하는 생산자들로부터도 신뢰를 얻고 있습니다.

처리된 피복 작물용 종자에 대한 탄소 크레딧의 수익화

피복 작물의 도입은 토양 탄소 고정에 대해 농가에 보상을 지급하는 탄소 시장을 통해 지원되고 있지만, 해당 프로토콜에서는 종자 처리 비용의 투입이 거의 고려되지 않습니다. 천연자원보전국(NRCS)은 동적 토양 특성 모니터링을 확대함으로써, 처리된 종자로 인해 발생하는 바이오매스 증가량을 정량화하는 조사 기법의 길을 열었습니다. 처리된 피복 작물의 발아와 검증된 탄소 증가를 연결 짓는 실증 연구는 아직 존재하지 않기 때문에 수익 증가 전망은 현시점에서는 가설의 범위를 벗어나지 못합니다. 조기 도입자들은 짧은 가을 파종 기간 동안 작물 재배를 안정적으로 유지하기 위해, 향후 신뢰성을 기대하며 종자 처리 비용을 자비로 부담하고 있습니다. Verra와 같은 등록 기관이 시드(seed)를 포함한 탄소 규정을 공표하면, 제제 제조업체는 처리와 프로젝트 참여를 패키지로 제공할 수 있게 되겠지만, 그 전까지는 그 추진력은 제한된 범위에 그칠 것입니다.

네오니코티노이드계 농약에 대한 주 차원의 규제 동향과 그 영향

버몬트주의 ‘제182호 법안’은 2029년 1월부터 네오니코티노이드 계열로 처리된 대두 및 곡물 종자의 사용을 금지하고 있으며, 뉴욕주와 코네티컷주 의회에서도 유사한 법안이 심의 중입니다. 이에 대해 각 공급업체들은 캐나다산 곡물에서 최초로 상용화된 신젠타사의 ‘PLINAZOLIN’, 비네오니코계 살충제를 사용한 코르테바사의 ‘LumiGEN’ 혼합제 등의 유효 성분으로 대응하고 있습니다. 제품 포트폴리오의 세분화는 물류를 복잡하게 만들지만, 대체 화학물질의 조기 등록을 확보한 기동성이 뛰어난 제제 제조업체에게는 호기가 됩니다. 주 차원의 네오니코티노이드(네오닉스) 규제가 시장에 미치는 영향은 미국의 종자 처리 시장이 규제 구역별로 분할될 것임을 시사하고 있습니다. 이로 인해 제제 제조업체는 여러 제품 포트폴리오를 관리해야 할 필요가 생기며, 공급망의 물류가 복잡해지게 됩니다. 반면, 비네오니코계 대체품에 조기에 투자하여 경쟁사보다 앞서 규제 당국의 승인을 확보한 기업에게는 좋은 기회가 될 것입니다.

부문별 분석

살균제는 가장 큰 시장 점유율을 차지하고 있으며, 2025년에는 미국 종자 처리 시장 점유율의 46%를 차지했으며, 생산자들이 푸사리움, 피시움, 리조크토니아와 싸우는 데 도움을 주었습니다. 이러한 우위는 시들음병, 뿌리썩음병, 종자 부패 등 토양 전염성 및 생육 초기 병해로부터 종자와 모종을 보호하는 데 있어 살균제가 필수적인 역할을 하고 있다는 점에 기인합니다. 살균제를 광범위하게 사용함으로써, 특히 옥수수, 대두, 밀 등의 작물에서 작물의 정착이 확실해지고 발아가 균일해집니다. 대두 재배자들은 방치할 경우 식물 수를 크게 감소시킬 우려가 있는 피시움이나 리조크토니아 등의 병원균으로부터 작물을 보호하기 위해, 살균제를 이용한 종자 처리를 자주 실시했습니다. 이러한 일관된 예방적 보호 덕분에 살균제는 다양한 재배 지역의 농가들에게 없어서는 안 될 자재가 되었습니다.

살충제 시장은 가장 빠르게 성장하고 있는 분야로, 2026-2031년 연평균 성장률(CAGR) 13.5%를 나타낼 것으로 전망됩니다. 이러한 성장은 해충 피해 증가, 내성 문제에 대한 우려, 그리고 작물의 초기 단계에서 보호의 필요성에 힘입어 이루어지고 있습니다. 와이어웜, 옥수수 종자 구더기, 진딧물 등의 해충은 계속해서 수확량을 위협하고 있으며, 농가들은 예방책으로 살충제를 이용한 종자 처리를 채택하고 있습니다. 종합 해충 관리(IPM)와 정밀 농업의 실천이 보급됨에 따라, 각 농지의 위험도에 맞추어 살충제를 선별적으로 사용하는 방식이 확대되고 있습니다. 생육 초기 해충 피해를 입기 쉬운 지역의 옥수수 농가들은 재배 손실을 방지하고 재파종에 드는 비용을 피하기 위해 살충제 처리 종자를 선택하는 경향이 있으며, 이것이 해당 부문의 급속한 성장을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the united states seed treatment market size was valued at USD 2.10 billion in 2025 and estimated to grow from USD 2.32 billion in 2026 to reach USD 3.25 billion by 2031, at a CAGR of 9.10% during the forecast period (2026-2031).

This report is Segmented by Product Type (Fungicide, Insecticide, and Nematicide), and by Crop Type (Commercial Crops, Fruits and Vegetables, Grains and Cereals, Pulses and Oilseeds, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD).

United States Seed Treatment Market Trends and Insights

Regulatory Pressure on Conventional Pesticides

The Environmental Protection Agency updated occupational exposure assessments for clothianidin, imidacloprid, and thiamethoxam in July 2024, intensifying compliance burdens for foliar neonicotinoids and steering growers toward seed-applied alternatives. Anticipated 2025 label amendments are likely to mandate wider buffers and stricter personal protective equipment for broadcast sprays, reinforcing the perception that seed placement is the regulatory path of least resistance. Extended Endangered Species Act consultations have already lengthened herbicide approvals, signaling similar hurdles for new foliar insecticides. Seed formulators exploit a shorter re-registration window by reformulating existing actives into seed-specific packages, giving them a faster route to market. As a result, companies investing in dedicated seed formulation platforms capture both time-to-market advantage and stewardship goodwill with growers who prefer products that require fewer handler precautions.

Carbon-Credit Monetization for Treated Cover-Crop Seeds

Cover-crop adoption is subsidized through carbon markets that pay farmers for sequestering soil carbon, yet protocols rarely account for seed treatment inputs. The Natural Resources Conservation Service expanded dynamic soil property monitoring, paving the way for methodologies to quantify the biomass acceleration delivered by treated seed. Empirical studies linking treated cover-crop emergence to verified carbon gains are still absent, so revenue upside is hypothetical. Early adopters self-fund seed treatment to stabilize stands in narrow autumn planting windows, betting on future credibility. Once registries such as Verra publish seed-inclusive carbon rules, formulators can bundle treatments with project enrollment, but until then, the driver remains modest in scope.

Emerging State-Level Restrictions on Neonics and Their Impact

Vermont's Act 182 bans neonic-treated soybean and cereal seed from January 2029, and similar proposals are pending in the New York and Connecticut legislatures. Suppliers answer with actives such as Syngenta's PLINAZOLIN, first commercialized in Canadian cereals, and Corteva's LumiGEN recipes that rely on non-neonic insecticides. Portfolio fragmentation complicates logistics but creates an opening for agile formulators that secure early registrations of alternative chemistries. The market implications of state-level neonicotinoid (neonics) restrictions suggest a fragmented United States seed treatment market divided into regulatory zones. This will require formulators to manage multiple product portfolios, complicating supply chain logistics. It also presents opportunities for companies that invest early in non-neonic alternatives and secure regulatory approvals ahead of competitors.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for On-Farm Seed Treating to Enhance Crop Yields

- Adoption of Digital Prescription Planting for Precision Agriculture

- Addressing the Perception Gap Compared to Fully Organic Farming Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fungicides hold the largest position, accounting for 46% of the United States seed treatment market share in 2025, helping growers combat Fusarium, Pythium, and Rhizoctonia. This dominance is attributed to their essential role in protecting seeds and seedlings from soil-borne and early-season diseases such as damping-off, root rot, and seed decay. Their widespread use ensures strong crop establishment and uniform germination, particularly in crops like corn, soybeans, and wheat. Soybean growers frequently use fungicide seed treatments to protect against pathogens such as Pythium and Rhizoctonia, which can significantly reduce stand counts if left unmanaged. This consistent and preventive protection has made fungicides a critical input for farmers across various growing regions.

Insecticides are the fastest-growing segment, projected to grow at a 13.5% CAGR through 2026-2031, whose growth is driven by increasing pest pressures, concerns over resistance, and the need for early-stage crop protection. Pests such as wireworms, seedcorn maggots, and aphids continue to threaten yields, prompting farmers to adopt insecticide seed treatments as a proactive measure. The adoption of integrated pest management and precision agriculture practices is promoting the targeted use of insecticides based on field-specific risks. Corn farmers in areas prone to early-season pest infestations may choose insecticide-treated seeds to prevent stand loss and avoid replanting costs, thereby fueling the rapid expansion of this segment.

List of Companies Covered in this Report:

- Bayer AG

- Syngenta AG

- Corteva, Inc.

- BASF SE

- UPL Limited

- ADAMA Ltd.

- Germains Seed Technology Ltd.

- Incotec Group B.V.

- Valent U.S.A. LLC

- Nufarm Limited

- Chromatech Incorporated

- BrettYoung

- Loveland Products, Inc.(Nutrien Ltd.)

- Helena Agri-Enterprises, LLC

- Roquette Freres

- Precision Laboratories, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory pressure on conventional pesticides

- 4.2.2 Urgency in resistance management to combat pests and diseases

- 4.2.3 Shift to polymer encapsulation for reduced dust-off

- 4.2.4 Carbon-credit monetization for treated cover crops

- 4.2.5 Increasing demand for on-farm seed treating to enhance crop yields

- 4.2.6 Adoption of digital prescription planting for precision agriculture

- 4.3 Market Restraints

- 4.3.1 Impact of large grower consolidation on the agricultural market

- 4.3.2 Lag in Environmental Protection Agency (EPA) approvals for new actives

- 4.3.3 Emerging state-level restrictions on neonics and their impact

- 4.3.4 Addressing the perception gap compared to fully organic farming systems

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Insecticides

- 5.1.2 Fungicides

- 5.1.3 Nematicides

- 5.1.4 Combination Products

- 5.2 By Crop Type

- 5.2.1 Grains and Cereals

- 5.2.2 Oilseeds and Pulses

- 5.2.3 Fruits and Vegetables

- 5.2.4 Commercial Crops

- 5.2.5 Turf and Ornamentals

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market-level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for key Companies, Products and Services, and Recent Developments)

- 6.4.1 Bayer AG

- 6.4.2 Syngenta AG

- 6.4.3 Corteva, Inc.

- 6.4.4 BASF SE

- 6.4.5 UPL Limited

- 6.4.6 ADAMA Ltd.

- 6.4.7 Germains Seed Technology Ltd.

- 6.4.8 Incotec Group B.V.

- 6.4.9 Valent U.S.A. LLC

- 6.4.10 Nufarm Limited

- 6.4.11 Chromatech Incorporated

- 6.4.12 BrettYoung

- 6.4.13 Loveland Products, Inc.(Nutrien Ltd.)

- 6.4.14 Helena Agri-Enterprises, LLC

- 6.4.15 Roquette Freres

- 6.4.16 Precision Laboratories, LLC