|

시장보고서

상품코드

2066391

듀얼 카본 배터리 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Dual Carbon Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

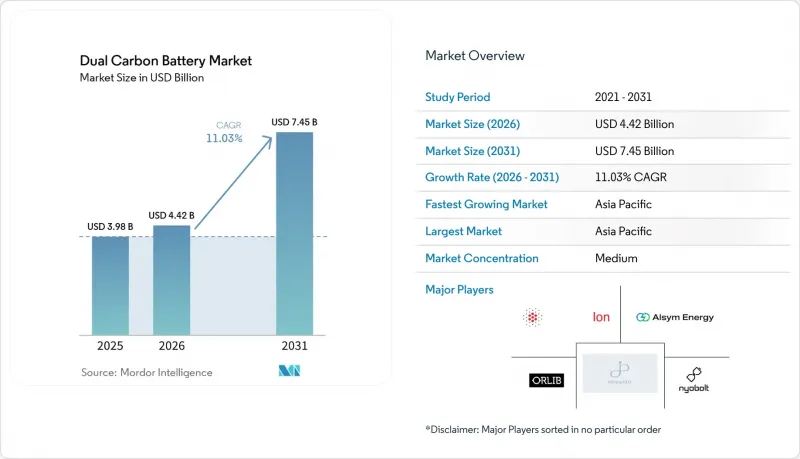

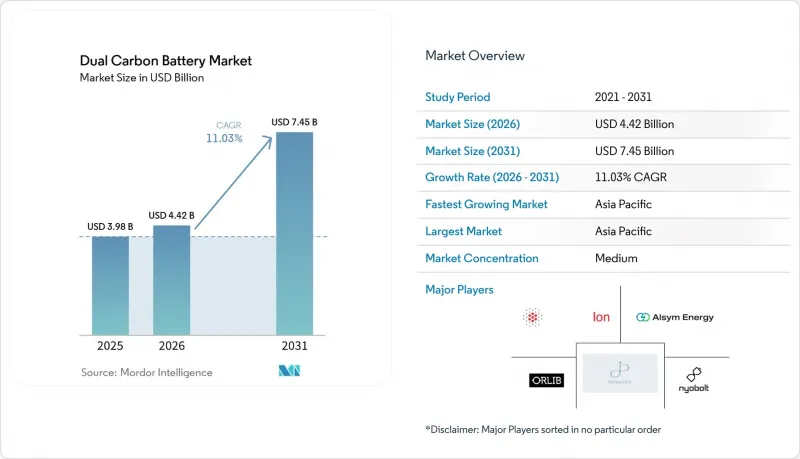

Mordor Intelligence에 의하면, 듀얼 카본 배터리 시장 규모는 2025년 39억 8,000만 달러에서 2026년에는 44억 2,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 11.03%로 성장을 지속하여, 2031년에는 74억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 배터리 유형(일회용 듀얼 카본 배터리 및 충전식 듀얼 카본 배터리), 용량(10 KWh 미만, 10-100 KWh, 100-500 KWh, 500 KWh 이상), 용도(자동차 배터리, 산업용 고정형 축전, 휴대용/가정용 전자기기, 항공우주 및 방위, 기타), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다.

세계 듀얼 카본 배터리 시장 동향 및 인사이트

전기차(EV)의 급속한 전동화를 위한 규제

EU 및 미국의 일부 주에서 2035년 이후 내연기관 차량의 신규 판매 금지 정책이 도입됨에 따라, 고비용의 냉각 루프 없이 5분 만에 10-80%까지 충전할 수 있는 배터리에 대한 잠재 수요가 크게 확대되고 있습니다. 듀얼 카본 전극은 대전류를 견디면서도 동급 리튬 이온 팩에 비해 코어 온도를 18°C 낮게 유지할 수 있으므로, 열 관리 하드웨어를 간소화할 수 있습니다. 중국이 2030년까지 신에너지차 판매 점유율 40% 달성을 목표로 하고 있는 점도 수요 증가를 더욱 뒷받침하고 있습니다. 국내 자동차 제조업체들은 니켈과 코발트의 가격 변동 위험을 피하기 위해 NMC 계열 화학 조성 이외의 소재로 다각화를 추진하고 있습니다. 규제 준수 기한이 단계적으로 설정되어 있는 점은 기가팩토리의 생산 확대 전망과 부합하며, 이를 통해 전문 개발 기업은 기존 공급업체가 대응을 완료하기 전에 공급 계약을 확실하게 체결할 수 있게 됩니다.

탄소 중립 공급망에 대한 인센티브

2027년 2월부터 의무화되는 EU의 ‘배터리 여권’ 제도에 따라, 제조업체는 제조 시작부터 공장 출하까지의 CO2 배출 강도 및 재활용 함유율을 공개해야 합니다. 풀 카본 전극은 고온에서의 금속 제련을 필요로 하지 않음으로써 매립 배출량을 줄여주며, 이러한 화학 성분이 규제 하에서 높은 평가를 받는 데 기초가 됩니다. 미국에서는 ‘인플레이션 억제법(Inflation Reduction Act)’에 따른 세액 공제가 국내 조달률이 60%를 초과할 경우, 1kWh당 45달러로 인상됩니다. 이 기준은 미국의 천연 흑연이나 탄소섬유를 사용하는 ‘듀얼 카본’ 생산자라면 달성할 수 있습니다. 스코프 3 배출량 감축을 목표로 하는 기업 구매 담당자들은 견적 요청 단계에서 생애주기 평가(LCA) 데이터 제공을 요구하는 사례가 늘어나고 있으며, 저탄소 화학 성분은 단순한 마케팅상의 부가가치가 아니라 조달의 필수 조건으로 자리 잡고 있습니다.

셀부터 팩에 이르는 열 폭주 시험이 보류 중

대부분의 형식 인증 프로토콜은 여전히 리튬 이온 배터리의 오용 모드를 중심으로 구성되어 있으며, 듀얼 카본과 같은 화학적 조성에 대해서는 명확한 합격·불합격 기준이 정해져 있지 않습니다. 규제 당국은 개별 시험 매트릭스를 요구하고 있으며, 문서화된 기준이 없기 때문에 차량 프로그램 1건당 6-9개월의 인증 기간 연장을 불가피하게 하고 있습니다. 현재 ISO 및 IEC에서 잠정 지침 초안이 작성 중이지만, 2026년 하반기까지 마련되지 않을 전망이며, 이로 인해 단기적으로 자동차 시장 출시가 제약을 받게 될 것입니다. 이러한 지연은 여러 지역에서 동시에 검증 프로그램을 시행할 자원이 부족한 중견 공급업체들에게 특히 큰 타격이 됩니다.

부문별 분석

2025년, 듀얼 카본 배터리 시장 중 충전식 제품이 86.35%를 차지했습니다. 이는 승용 전기차나 플릿용 전기버스 등 반복적인 충·방전이 이루어지는 용도에 이 화학 계열이 적합하다는 점을 반영한 것입니다. 장기 노상 시험 결과, 3,000회의 완전 깊이 사이클 후에도 80%의 용량 유지율이 확인되었으며, 보증 의무를 충족하기 위해 팩을 과도하게 설계해야 하는 금속계 셀에 비해 총 소유 비용(TCO)이 낮습니다. 일회용 듀얼 카본 전지는 여전히 틈새 시장 제품으로, 주로 항공우주 분야의 비상 전원 등으로 채택되고 있지만, 이 분야에서는 경제성보다 안전한 고장 모드가 우선시되고 있습니다.

2025년, 한 대형 개발 기업이 3,000만 달러 규모의 시리즈 C 자금 조달을 확보하고 자동차 분야에서 8건의 설계 채택 실적을 발표한 것을 계기로, 충전식 배터리의 상업적 보급이 가속화되었습니다. 표준화된 21700 및 46xx 폼 팩터가 현재 시범 생산 단계에서 양산 단계로 접어들고 있어, 배터리 팩 제조업체들은 금형 변경을 최소화하면서 통합이 가능해졌습니다. 도입이 확대됨에 따라 규모의 경제 효과로 인해 2025년부터 2028년 사이에 kWh당 비용이 약 22% 감소할 것으로 예상되며, 이에 따라 인산철 리튬 배터리와의 가격 차이가 좁혀질 것으로 전망됩니다.

지역별 분석

2025년 아시아태평양 시장 점유율은 49.02%에 달하며, 니들 코크스 원료부터 완성된 전극에 이르기까지의 심도 있는 수직 통합이 두드러집니다. 중국의 합성 흑연 제조업체들은 수력 발전 및 태양광 발전을 통한 자체 발전을 활용하고 있으며, 내재된 배출량을 kWh당 4kg CO2-eq 미만으로 억제하고 있는데, 이는 유럽 평균보다 훨씬 낮은 수준입니다. 각 지역 정부는 시범 생산 라인에 대해 20%의 자본 보조율을 제공하고 있으며, 이를 통해 현지 생산이 가속화되고 수출 비용 측면에서의 우위가 유지되고 있습니다. 아시아태평양의 듀얼 카본 배터리 시장 규모는 전기차 배터리 팩에 대한 국내 부품 사용률 최저 기준을 의무화하는 각국의 정책에 힘입어 2031년까지 연평균 성장률(CAGR) 12.1%로 확대될 것으로 전망됩니다.

북미는 이 지역에서 가장 빠르게 성장하고 있는 시장입니다. '인플레이션 억제법(Inflation Reduction Act)'에 따라 차량용 배터리 모듈 1개당 최대 3,750달러의 세액 공제가 제공됨에 따라, 2025년에는 최소 4개의 OEM이 미국의 듀얼 카본 계열 스타트업 기업과 조건부 인수 계약을 체결했습니다. 에너지부가 주도한 2,500만 달러 규모의 자금 조달 라운드는 국내에서 전극 코팅 및 이온 액체 전해질 합성을 확대하는 11개 프로젝트를 지원하고 있습니다. 캐나다의 광업 벤처 기업은 2027년에 가동을 시작할 예정인 두 개의 대규모 플레이크 흑연 프로젝트를 통해 원료의 안정적인 공급을 확보하고 있으며, 이를 통해 물류 비용 절감에도 기여하고 있습니다.

유럽의 향후 전망은 탄소계 화학물질과 완벽하게 부합하는 지속가능성 규제에 달려 있습니다. '배터리 패스포트'는 추적성을 확보하고, 저배출 소재를 권장하고 있습니다. 핀란드와 스웨덴에 위치한 리그닌 유래 탄소 시범 공장은 2028년까지 총 연간 생산 능력 1만 5,000톤을 목표로 하고 있습니다. 유럽의 자동차 제조업체들은 현재 일본의 생산 라인에서 시제품 셀을 수입하고 있지만, 전구체공급 체계가 갖춰지는 대로 모듈을 현지에서 생산할 계획입니다. 중동 및 아프리카 시장은 여전히 규모가 작지만, 걸프 지역의 전력 회사들은 높은 주변 온도가 기존 리튬이온 시스템에 악영향을 미치는 사막 기후 하에서 전력 저장 시스템에 관심을 보이고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the dual carbon battery market size is expected to grow from USD 3.98 billion in 2025 to USD 4.42 billion in 2026 and is forecast to reach USD 7.45 billion by 2031 at 11.03% CAGR over 2026-2031.

This report is Segmented by Battery Type (Disposable Dual-Carbon Cells and Rechargeable Dual-Carbon Cells), Capacity (Below 10 KWh, 10 To 100 KWh, 100 To 500 KWh, and Above 500 KWh), Application (Automotive Batteries, Industrial Stationary Storage, Portable/Consumer Electronics, Aerospace and Defense, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Global Dual Carbon Battery Market Trends and Insights

Rapid EV Electrification Mandates

Policies banning new internal-combustion models from 2035 in the EU and several U.S. states significantly expand the addressable demand for batteries that can charge from 10-80% in five minutes without high-cost cooling loops. Dual carbon electrodes withstand elevated currents while maintaining core temperatures 18 °C lower than those of comparable lithium-ion packs, enabling simpler thermal management hardware. China's New Energy Vehicle target of 40% sales penetration by 2030 further cements volume pull, as domestic OEMs diversify beyond NMC chemistries to hedge against nickel and cobalt volatility. Staggered compliance deadlines align with expected gigafactory ramp-ups, allowing specialist developers to lock in offtake agreements before legacy suppliers adapt.

Carbon-Neutral Supply-Chain Incentives

The EU Battery Passport, which becomes compulsory from February 2027, requires manufacturers to disclose cradle-to-gate CO2 intensities and recycled-content percentages. Full-carbon electrodes reduce embodied emissions by eliminating high-temperature metal smelting, positioning the chemistry for premium scoring under the regulation. In the United States, the Inflation Reduction Act tax credits increase to USD 45 per kWh when domestic content exceeds 60%, a threshold that is attainable for dual carbon producers using U.S. natural graphite or carbon fiber. Corporate buyers seeking Scope 3 emission reductions increasingly request life-cycle assessment data at the request-for-quotation stage, turning low-carbon chemistries into a procurement prerequisite rather than a marketing plus.

Cell-to-Pack Thermal-Runaway Tests Pending

Most homologation protocols still revolve around lithium-ion abuse modes, leaving chemistries like dual carbon without explicit pass-fail criteria. Regulatory agencies require bespoke test matrices, and the absence of codified standards prolongs qualification by six to nine months per vehicle program. Interim guidelines are currently under draft at the ISO and IEC, but are not expected until late 2026, which will constrain near-term automotive launches. The delay particularly hurts mid-tier suppliers that lack the resources to run parallel validation programs across multiple regions.

Other drivers and restraints analyzed in the detailed report include:

- End-of-Life Recyclability Regulations

- 20x-Faster Charge Pilots in E-buses

- Limited Large-Scale Carbon Precursor Supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rechargeable products accounted for 86.35% of the dual carbon battery market in 2025, reflecting the chemistry's suitability for repeated-cycle applications, such as passenger EVs and fleet e-buses. Long-term road tests demonstrate 3,000 full-depth cycles with 80% capacity retention, resulting in a lower total cost of ownership compared to metal-based cells that require pack oversizing to meet warranty obligations. Disposable dual-carbon formats remain niche, chiefly in aerospace emergency power, where benign failure modes trump unit economics.

Commercial traction for rechargeables accelerated after a leading developer secured USD 30 million Series C funding and disclosed eight automotive design wins in 2025. Standardized 21700 and 46xx form factors now roll off pilot lines, enabling pack-maker integration with minimal tooling change. As deployment widens, economies of scale are expected to reduce the cost per kWh by an estimated 22% between 2025 and 2028, thereby narrowing the pricing gap with lithium-iron-phosphate.

Geography Analysis

Asia-Pacific's 49.02% share in 2025 underscores deep vertical integration from needle coke feedstock to finished electrodes. Chinese synthetic-graphite producers leverage captive power sourced from hydroelectric and solar sources, keeping embodied emissions under 4 kg CO2-eq per kWh, which is well below European averages. Regional governments offer 20% capital-grant ratios for pilot lines, accelerating local output and maintaining export cost leadership. The dual carbon battery market size in Asia-Pacific is forecast to advance at a 12.1% CAGR to 2031, supported by national policies mandating minimum domestic content in EV packs.

North America is the fastest-growing market in the region. Inflation Reduction Act credits worth up to USD 3,750 per vehicle battery module drove at least four OEMs to sign conditional offtake agreements with U.S. dual carbon start-ups in 2025. The Department of Energy's USD 25 million funding round supports eleven projects that scale electrode coating and ionic-liquid electrolyte synthesis onshore. Canadian mining ventures enhance feedstock security with two large flake-graphite projects scheduled for commissioning in 2027, which helps lower logistics costs.

Europe's trajectory hinges on sustainability regulations that align squarely with carbon-based chemistries. The Battery Passport favors traceable, low-emission materials. Lignin-derived carbon pilot plants in Finland and Sweden target a combined annual capacity of 15,000 tons by 2028. European automakers currently import prototype cells from Japanese lines but intend to localize modules once the precursor supply matures. Middle East and African markets remain small, although Gulf utilities have expressed interest in desert-climate storage, where high ambient temperatures penalize traditional lithium-ion systems.

- PJP Eye Ltd (Power Japan Plus)

- Nyobolt

- Alsym Energy

- Carbon-Ion

- ORLIB Ltd

- Farad Power

- Panasonic Energy

- LG Energy Solution

- BYD Co. Ltd

- CATL

- Samsung SDI

- Hitachi Energy

- Toshiba

- Envision AESC

- Sion Power

- StoreDot

- Enevate

- QuantumScape

- Skeleton Technologies

- Northvolt

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid EV electrification mandates

- 4.2.2 Carbon-neutral supply-chain incentives

- 4.2.3 End-of-life recyclability regulations

- 4.2.4 20x-faster charge pilots in e-buses

- 4.2.5 OEM shift to anode-free chemistries

- 4.2.6 Grid-edge ultra-fast storage tenders

- 4.3 Market Restraints

- 4.3.1 Cell-to-pack thermal-runaway tests pending

- 4.3.2 Absence of ISO/IEC performance standard

- 4.3.3 Limited large-scale carbon precursor supply

- 4.3.4 VC funding tilt towards solid-state

- 4.4 Comparative Analysis: Dual-Carbon vs Other Battery Technologies

- 4.5 Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Disposable Dual-Carbon Cells

- 5.1.2 Rechargeable Dual-Carbon Cells

- 5.2 By Capacity

- 5.2.1 Below 10 kWh

- 5.2.2 10 to 100 kWh

- 5.2.3 100 to 500 kWh

- 5.2.4 Above 500 kWh

- 5.3 By Application

- 5.3.1 Automotive Batteries

- 5.3.2 Industrial Stationary Storage

- 5.3.3 Portable/Consumer Electronics

- 5.3.4 Aerospace and Defense

- 5.3.5 Other Niche Uses

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 ASEAN Countries

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Argentina

- 5.4.4.2 Brazil

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 PJP Eye Ltd (Power Japan Plus)

- 6.4.2 Nyobolt

- 6.4.3 Alsym Energy

- 6.4.4 Carbon-Ion

- 6.4.5 ORLIB Ltd

- 6.4.6 Farad Power

- 6.4.7 Panasonic Energy

- 6.4.8 LG Energy Solution

- 6.4.9 BYD Co. Ltd

- 6.4.10 CATL

- 6.4.11 Samsung SDI

- 6.4.12 Hitachi Energy

- 6.4.13 Toshiba

- 6.4.14 Envision AESC

- 6.4.15 Sion Power

- 6.4.16 StoreDot

- 6.4.17 Enevate

- 6.4.18 QuantumScape

- 6.4.19 Skeleton Technologies

- 6.4.20 Northvolt

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment