|

시장보고서

상품코드

2066396

반도체 실리콘 지적재산권 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Semiconductor Silicon Intellectual Property - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

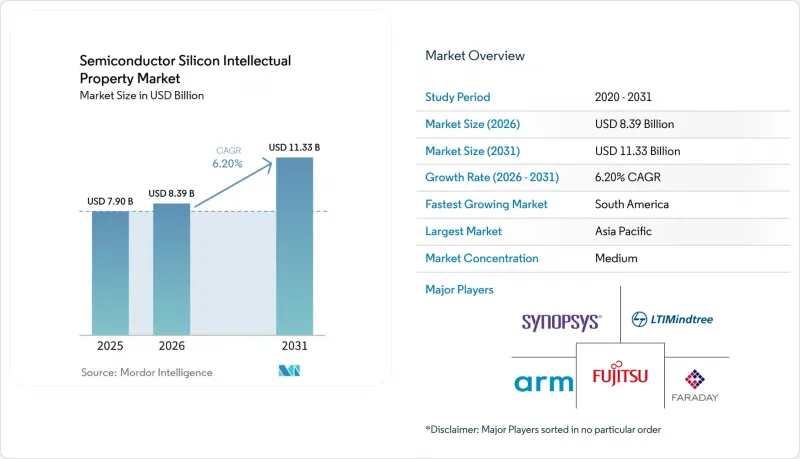

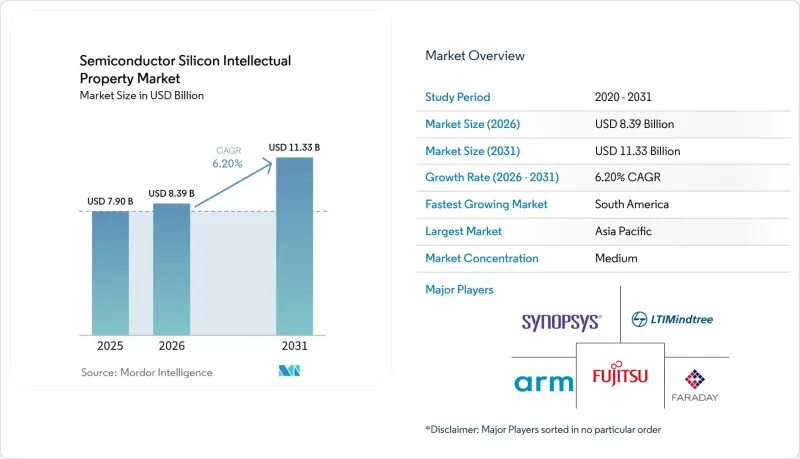

Mordor Intelligence에 의하면, 반도체 실리콘 IP 시장 규모는 2025년 79억 달러로 평가되었고, 2026년에는 83억 9,000만 달러로 추정되고, 2026-2031년 CAGR 6.2%로 성장을 지속할 전망이며, 2031년에는 113억 3,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 수익 유형별(라이선스 및 서비스), IP 유형별(프로세서 IP, 유선 인터페이스 IP, 기타 IP 유형), 최종 사용자 산업별(소비자용 전자기기, 컴퓨터 및 주변기기, 자동차, 산업용, 기타 산업), 공정 노드별(28nm 이상, 16/14nm, 10/7nm, 5nm 이하), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 반도체 실리콘 지적재산권(IP) 시장 동향 및 인사이트

IoT 지원 연결 기기의 보급

스마트 미터, 웨어러블 기기, 자산 추적 태그의 출하 대수가 사상 최고치를 기록하고 있으며, 저전력 프로세서, 무선 송수신기, 센서 허브 IP에 대한 수요가 급증하고 있습니다. 엣지 아키텍처에서는 현재 데이터 소스 근처에서 실시간 추론을 수행하는 도메인 특화형 블록이 선호되고 있으며, 이를 통해 지연 시간과 백홀 대역폭이 감소하고 있습니다. MPU, RF 및 보안 요소 IP를 묶어 제공하는 턴키 서브시스템 공급업체는 각 OEM 업체가 사내 팀을 확대하지 않고도 연결 기능을 통합할 수 있도록 함으로써 설계 채택을 확보하고 있습니다. 하드웨어 기반의 보안에 대한 중요성이 부각되면서, 특히 중요한 인프라가 사이버 위험에 노출된 분야에서 암호화 가속기 및 물리적으로 복제 불가능한 함수(PUF) 시드의 도입률이 증가하고 있습니다. 2024년에 스마트 팩토리 및 유틸리티 분야에서 시범 도입된 개념 검증(PoC)이 양산 단계로 접어들고 있으며, 이에 따라 특수 IP 포트폴리오의 성장세가 향후 수년간 유지될 전망입니다.

SoC 설계의 복잡화 및 시장 출시 기간 단축

현재, 최고 수준의 스마트폰 및 자동차용 칩에는 여러 전압 아일랜드와 비동기 클럭 도메인에 걸쳐 50개 이상의 IP 블록이 통합되어 있습니다. 이처럼 환경 전반에 걸친 검증 조정은 일정상의 위험을 초래하지만, 대부분의 OEM은 공개된 안전성 실적이 있는 사전 검증된 IP를 조달함으로써 이러한 위험을 완화하고 있습니다. 누설 전류, 편차, 전기이동을 줄이기 위해 파운드리 인증을 받은 변형을 통해 테이프아웃 주기가 더욱 단축되었으며, 공급업체는 RTL, 물리적 구현, 패키지에 이르는 공동 설계를 아우르는 컨설팅 서비스를 확대되고 있습니다. 칩렛 아키텍처는 이종 다이가 벤더의 경계를 넘어 상호 운용되어야 하므로, UCIe 2.0 사양을 준수함으로써 인터페이스 IP의 가치를 한층 더 높이고 있습니다. 이러한 모듈형 플랫폼을 기반으로 한 실리콘 개발을 가속화함으로써, IP 재사용은 단순한 비용상의 이점을 넘어 업무상 필수 요건이 되었습니다.

높은 초기 라이선스 비용과 규모에 따른 불이익

고성능 프로세서나 SerDes IP를 도입하려면 수백만 달러에 달하는 비용이 들기 때문에 스타트업이나 틈새 시장 업체들은 시장 진입을 주저할 수밖에 없으며, 기능이 떨어지는 오픈소스 블록이나 구세대 노드에 의존할 수밖에 없는 실정입니다. 수익 분배형이나 구독형 라이선싱 모델이 등장하고는 있지만, 확고한 입지를 갖춘 공급업체들이 검증된 실적을 바탕으로 한 프리미엄 가격을 유지하고 있기 때문에 여전히 소수에 그치고 있습니다. 인기 있는 IP 코어를 28nm에서 5nm로 이식하면 엔지니어링 비용이 2배로 늘어나는 경우가 많으며, 이로 인해 Tier 1 칩 제조업체와 소규모 설계 회사 간의 격차가 더욱 벌어지고 있습니다. 그 결과, 시장 진입 장벽이 혁신의 전반적인 속도를 저해하여, 대체적인 라이선싱 체계가 보급될 때까지는 중규모 OEM 제조업체의 잠재적 수요를 억제할 가능성이 있습니다.

부문별 분석

서비스 관련 지출은 반도체 실리콘 IP 시장에서 가장 빠르게 성장하고 있는 분야로, 칩 제조업체들이 사내 처리 능력을 초과하는 맞춤형 개발, 하드닝 및 브링업 작업을 외부에 위탁함에 따라 2031년까지 연평균 성장률(CAGR) 8.12%로 증가하고 있습니다. 그러나 2025년에는 라이선스 수입이 매출의 58.22%를 차지했으며, 5nm 이하 공정을 채택하는 고객들로부터 라이선스 취득 후 엔지니어링 공수가 급증하고 있다는 보고가 있어, 서비스가 포함된 계약이 매력적인 선택지로 떠오르고 있습니다. IP 벤더들은 현재 지속적인 성능 튜닝, 무선(OTA)을 통한 보안 패치 지원, 실리콘 수명 주기 분석 등을 포함하는 플랫폼 구독 서비스를 제공합니다. 이러한 프로그램은 고객 유지율을 높이고, 테이프아웃 물량에 따른 주기적인 변동을 완화합니다.

이러한 변화는 특히 미드레인지 프로세서 및 이더넷 IP 부문에서 코모디티 코어가 직면한 가격 압박을 완화하고 있습니다. 대규모 현장 용도 팀을 보유한 벤더들은 통합 컨설팅을 수익성 향상 전략으로 활용하여, 비용 중심의 IoT 기기로의 전환에 따라 감소하는 단위당 로열티를 상쇄하고 있습니다. 하이브리드 수익 모델은 지속적인 현금 흐름을 창출하고, 공급업체의 인센티브를 고객의 생산 단계와 연계함으로써, 이번 세기 말까지 해당 서비스가 반도체 실리콘 IP 시장 규모에서 더 큰 점유율을 확보할 것이라는 전망을 더욱 확고히 하고 있습니다.

5G 인프라 확대, Wi-Fi 7 도입, 그리고 Bluetooth LE Audio 업그레이드에 힘입어 무선 인터페이스 IP 시장은 연평균 성장률(CAGR) 7.05%를 기록하며 성장하고 있습니다. 다중 표준 무선 기능을 통합하는 칩 제조업체들은 전 세계 인증 요건을 충족하는 기성 RF, 베이스밴드 및 공존 로직을 찾고 있으며, 이를 통해 촉박한 일정 속에서도 소비자용 기기를 출시할 수 있게 되었습니다. 그럼에도 불구하고, 2025년에도 프로세서 IP는 모든 SoC에 CPU 코어가 널리 채택되고 있다는 점을 배경으로 45.88%의 비중을 차지하며 여전히 최대 수익원이 되었습니다.

RISC-V의 등장으로 프로세서 IP 분야의 경쟁이 치열해지고 있으며, 기존 기업들은 AI 가속 기능의 통합 및 전력 관리 기능 강화를 통해 차별화 요소를 확대해야 하는 상황에 직면해 있습니다. 이와 동시에, 유선 인터페이스 IP는 데이터센터 및 자동차 분야의 연결성 수요에 지속적으로 부응하며, 안정적인 한 자릿수 중반대의 성장세를 유지하고 있습니다. 보안, 메모리 컨트롤러, 아날로그 IP가 시장 기회의 전체적인 구도를 이루고 있으며, 이들은 SoC의 실리콘 면적 확대와 전용 서브시스템이 필요한 특정 용도 설계의 부상으로 인해 전반적으로 혜택을 보고 있습니다.

지역별 분석

2025년에는 아시아태평양 지역이 전 세계 매출의 52.14%를 차지해 1위를 차지했습니다. 이는 중국, 한국, 대만, 일본에 구축된 탄탄한 제조 생태계에 더해, 반도체 산업을 지원하는 경제 대책이 뒷받침한 결과입니다. 파운드리와의 공동 개발 프로그램을 통해 설계 규칙 및 IP 하드닝에 관한 긴밀한 협력이 촉진되었으며, 그 결과 국내외 포트폴리오 모두 해당 지역에서의 채택률이 향상되고 있습니다. 중국의 자급자족 정책은 RISC-V 및 보안 IP에 대한 투자를 촉진하고 있는 반면, 한국의 ‘K-반도체 벨트’는 메모리 중심의 인터페이스 블록에 대한 수요를 강화하고 있습니다. 일본은 자동차용 반도체와 첨단 패키징에 주력하고 있으며, 기능 안전 IP 및 칩렛 상호 연결에 대한 수요 증가에 기여하고 있습니다.

북미는 주요 IP 라이선스 제공업체, 하이퍼스케일 데이터센터용 칩 설계 기업, 방위 관련 기업의 거점으로서 여전히 매우 중요한 위치를 차지하고 있습니다. ‘CHIPS법’에 따른 국내 생산 인센티브는 공급망의 회복탄력성을 최우선으로 하여, IP, EDA, 파운드리 간의 협력적인 노력을 촉진하고 있습니다. AI 스타트업에 대한 대규모 벤처 자금 조달은 맞춤형 액셀러레이터의 신속한 프로토타이핑으로 이어지며, 모든 IP 범주에 걸친 국내 수요를 뒷받침하고 있습니다. 또한, 캐나다에서 지속적으로 성장하고 있는 양자 컴퓨팅 생태계도 극저온 인터페이스 IP의 틈새 고객층으로 부상하고 있습니다.

유럽은 총 매출 규모는 작지만, 자동차용 전자기기, 산업용 자동화, 파워 반도체 분야에서의 선도적 입지를 바탕으로 그 규모 이상의 영향력을 발휘하고 있습니다. EU의 ‘CHIPS법’에 따른 보조금은 최첨단 시범 생산 라인에 투입되고 있으며, 고장 시 작동 안전 로직이 통합된 7nm 이하 IP에 대한 수요를 촉진하고 있습니다. 한편, 남미의 반도체 실리콘 IP 시장은 브라질의 현지화 인센티브와 아르헨티나의 인재 기반이 설계 센터를 유치함으로써 검증된 IP 코어의 지역 내 소비를 확대시킬 것으로 예상에 따라, 8.24%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 중동 및 아프리카는 여전히 개발도상 시장이지만, 걸프협력회의(GCC) 차원의 정부 주도 데이터센터 투자와 엣지 AI 감시 시스템 도입을 통해 잠재력을 보여주고 있으며, 향후 IP 지출을 위한 기반을 다지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the semiconductor silicon IP market size is expected to grow from USD 7.9 billion in 2025 to USD 8.39 billion in 2026 and is forecast to reach USD 11.33 billion by 2031 at 6.2% CAGR over 2026-2031.

This report is Segmented by Revenue Type (License, and Services), IP Type (Processor IP, Wired Interface IP, and Other IP Types), End-User Vertical (Consumer Electronics, Computers and Peripherals, Automotive, Industrial, and Other Verticals), Process Node (28 Nm and Above, 16/14 Nm, 10/7 Nm, 5 Nm and Below), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Semiconductor Silicon Intellectual Property Market Trends and Insights

Proliferation of IoT-Enabled Connected Devices

Record shipments of smart meters, wearables, and asset-tracking tags are driving a surge in low-power processor, wireless transceiver, and sensor-hub IP demand. Edge architectures now favor domain-specific blocks that execute real-time inference close to the data source, reducing latency and backhaul bandwidth. Vendors offering turnkey subsystems that bundle MPU, RF, and secure-element IP are capturing design wins because they enable OEMs to integrate connectivity without expanding their internal teams. Heightened emphasis on hardware-rooted security is driving up attachment rates for cryptographic accelerators and physically unclonable function seeds, particularly where critical infrastructure is exposed to cyber risk. Proof-of-concepts piloted in smart factories and utilities during 2024 are moving to volume production, sustaining a multiyear growth runway for specialized IP portfolios.

Complexity of SoC Designs and Shrinking Time-to-Market

Top-tier smartphone and automotive chips now integrate upward of 50 IP blocks, spanning multiple voltage islands and asynchronous clock domains. Coordinating verification across this landscape adds schedule risk that most OEMs mitigate by sourcing pre-verified IP with published safety artifacts. Foundry-qualified variants trimmed for leakage, variation, and electromigration further shorten tape-out cycles, prompting suppliers to expand consultancy services that cover RTL, physical implementation, and package co-design. Chiplet architectures amplify the value of interface IP, adhering to the UCIe 2.0 spec because heterogeneous dies must interoperate across vendor boundaries. Fast-tracking silicon on these modular platforms has turned IP reuse into an operational necessity rather than a cost preference.

High Upfront Licensing Costs and Scale Disadvantages

Multi-million-dollar entry fees for high-end processors or SerDes IP deter startups and niche players, forcing them toward less capable open-source blocks or older nodes. Revenue-sharing and subscription licensing models are emerging but remain a minority, as entrenched suppliers protect premium pricing tied to proven validation collateral. Porting a popular IP core from 28 nm to 5 nm frequently doubles engineering cost, further widening the gap between tier-one chipmakers and smaller design houses. Consequently, market entry barriers slow overall innovation velocity and may cap addressable demand among mid-volume OEMs until alternative licensing frameworks scale.

Other drivers and restraints analyzed in the detailed report include:

- AI and ML Accelerators Integrated into Edge Devices

- Commercial Demand for Verified RISC-V CPU IP

- Royalty Disputes and Patent-Litigation Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Service-related payments represent the fastest-growing portion of the Semiconductor silicon IP market, climbing at an 8.12% CAGR through 2031 as chipmakers outsource customization, hardening, and bring-up tasks that exceed their internal bandwidth. However, licenses controlled 58.22% of revenue in 2025, and customers deploying 5 nm and below reported a steep rise in post-license engineering hours, making bundled service contracts attractive. IP vendors now position platform subscriptions that include continuous performance tuning, over-the-air security patch support, and silicon lifecycle analytics. These programs enhance account stickiness and mitigate cyclical swings associated with tape-out volume.

The shift also cushions price pressure facing commodity cores, particularly in mid-range processor and Ethernet IP categories. Vendors with large field-application teams leverage integration consulting as a margin-enhancing strategy, offsetting declining per-unit royalties as volumes shift to cost-sensitive IoT devices. Hybrid revenue models spur recurring cash flows and align supplier incentives with customer production milestones, reinforcing the prospect that services could capture a larger slice of the Semiconductor silicon IP market size by the end of the decade.

Expanding 5G infrastructure, WiFi 7 adoption, and Bluetooth LE Audio upgrades are propelling wireless interface IP toward a 7.05% CAGR. Chipmakers integrating multi-standard radios seek ready-made RF, baseband, and coexistence logic that meets global certification requirements, allowing for consumer device launches on aggressive timelines. Processor IP nevertheless remained the single biggest revenue contributor at 45.88% in 2025, anchored by the ubiquity of CPU cores in every SoC.

Competitive intensity within processor IP has increased due to the entry of RISC-V entrants, prompting incumbents to widen their differentiators through integrated AI acceleration and power management enhancements. In parallel, wired interface IP continues to serve data center and automotive connectivity demands at stable mid-single-digit growth. Security, memory-controller, and analog IP round out the opportunity landscape, collectively benefiting from SoC silicon area inflation and the rise of application-specific designs that require specialized subsystems.

Geography Analysis

The Asia-Pacific region led global revenue with a 52.14% stake in 2025, driven by its deep manufacturing ecosystems in China, South Korea, Taiwan, and Japan, as well as supportive semiconductor stimulus packages. Foundry co-development programs foster close collaboration on design rules and IP hardening, thereby enhancing regional adoption rates for both domestic and international portfolios. China's self-reliance mandate propels investment into RISC-V and security IP, while South Korea's K-Semiconductor Belt strengthens demand for memory-centric interface blocks. Japan concentrates on automotive semiconductors and advanced packaging, adding traction for functional-safety IP and chiplet interconnects.

North America remains pivotal as home to major IP licensors, hyperscale data center chip designers, and defense contractors. The CHIPS Act's incentives for onshore fabrication encourage coordinated IP, EDA, and foundry engagements that prioritize supply chain resiliency. Strong venture funding for AI startups translates into rapid prototyping of custom accelerators, sustaining domestic demand across all IP categories. Canada's growing quantum-computing ecosystem also emerges as a niche customer segment for cryogenic interface IP.

Europe, though smaller in aggregate revenue, exerts outsized influence through leadership in automotive electronics, industrial automation, and power semiconductors. EU Chips Act subsidies are earmarked for state-of-the-art pilot lines, spurring requests for 7 nm and below IP with built-in fail-operational safety logic. Meanwhile, South America's Semiconductor silicon IP market is projected to post the highest 8.24% CAGR as Brazil's localization incentives and Argentina's talent base attract design centers, expanding regional consumption of verified IP cores. Middle East and Africa remain a nascent market but shows potential through sovereign datacenter investments and edge-AI surveillance rollouts in the Gulf Cooperation Council, laying groundwork for future IP spending.

- Arm Ltd.

- Synopsys Inc.

- Cadence Design Systems Inc.

- Faraday Technology Corp.

- Fujitsu Ltd.

- CEVA Inc.

- Andes Technology Corp.

- LTIMindtree Ltd.

- MediaTek Inc.

- Digital Media Professionals Inc.

- Imagination Technologies Ltd.

- VeriSilicon Holdings Co. Ltd.

- Achronix Semiconductor Corp.

- Rambus Inc.

- eMemory Technology Inc.

- MIPS Tech LLC

- SiFive Inc.

- Alphawave IP Group plc

- Arteris Inc.

- Flex Logix Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of IoT-enabled connected devices

- 4.2.2 Complexity of SoC designs and shrinking time-to-market

- 4.2.3 AI/ML accelerators integrated into edge devices

- 4.2.4 Commercial demand for verified RISC-V CPU IP

- 4.2.5 Chiplet and UCIe-based heterogeneous integration

- 4.2.6 Automotive functional-safety (ISO 26262) compliance

- 4.3 Market Restraints

- 4.3.1 High upfront licensing costs and scale disadvantages

- 4.3.2 Royalty disputes and patent-litigation exposure

- 4.3.3 Government chip-sovereignty programs favouring in-house IP

- 4.3.4 Security vulnerabilities eroding third-party IP trust

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Revenue Type

- 5.1.1 License

- 5.1.2 Royalty

- 5.1.3 Services

- 5.2 By IP Type

- 5.2.1 Processor IP

- 5.2.2 Wired Interface IP

- 5.2.3 Wireless Interface IP

- 5.2.4 Other IP Types

- 5.3 By End-User Vertical

- 5.3.1 Consumer Electronics

- 5.3.2 Computers and Peripherals

- 5.3.3 Automotive

- 5.3.4 Industrial

- 5.3.5 Other Verticals

- 5.4 By Process Node

- 5.4.1 28 nm and Above

- 5.4.2 16/14 nm

- 5.4.3 10/7 nm

- 5.4.4 5 nm and Below

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Arm Ltd.

- 6.4.2 Synopsys Inc.

- 6.4.3 Cadence Design Systems Inc.

- 6.4.4 Faraday Technology Corp.

- 6.4.5 Fujitsu Ltd.

- 6.4.6 CEVA Inc.

- 6.4.7 Andes Technology Corp.

- 6.4.8 LTIMindtree Ltd.

- 6.4.9 MediaTek Inc.

- 6.4.10 Digital Media Professionals Inc.

- 6.4.11 Imagination Technologies Ltd.

- 6.4.12 VeriSilicon Holdings Co. Ltd.

- 6.4.13 Achronix Semiconductor Corp.

- 6.4.14 Rambus Inc.

- 6.4.15 eMemory Technology Inc.

- 6.4.16 MIPS Tech LLC

- 6.4.17 SiFive Inc.

- 6.4.18 Alphawave IP Group plc

- 6.4.19 Arteris Inc.

- 6.4.20 Flex Logix Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment