|

시장보고서

상품코드

2066399

아시아태평양의 생명보험 및 손해보험 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Life And Non-Life Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

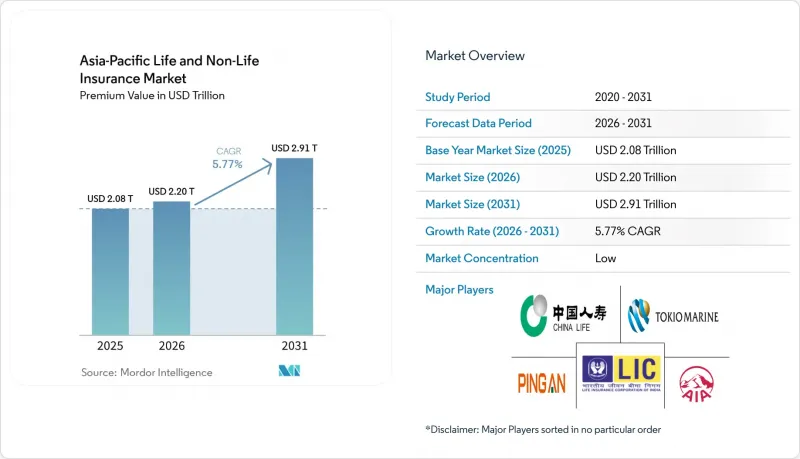

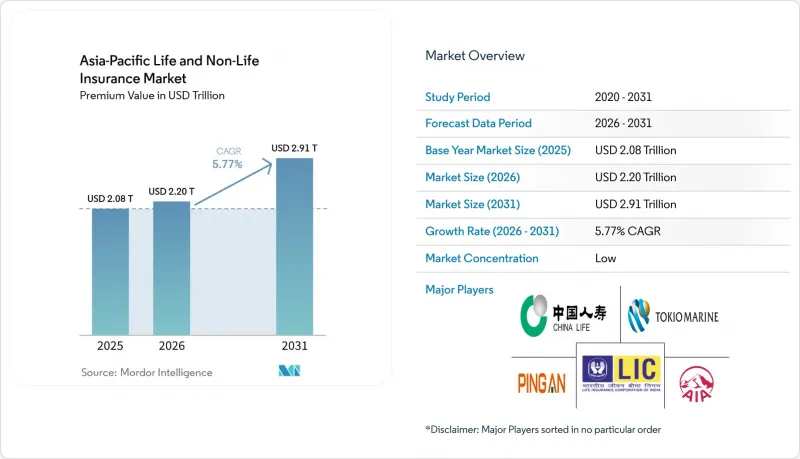

Mordor Intelligence에 의하면, 아시아태평양의 생명보험 및 손해보험 시장 규모는 2025년에 2조 800억 달러로 평가되었고, 2026년에 2조 2,000억 달러로 추정되고, 2031년까지 2조 9,100억 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 5.77%로 성장할 전망입니다.

본 보고서는 보험 유형별(생명보험, 손해보험(자동차, 건강, 재산, 배상책임 등)), 고객 부문별(개인, 법인), 판매 채널별(브로커, 대리점, 은행, 직접 판매, 기타 채널) 및 지역별(인도, 중국, 일본, 호주, 한국, 동남아시아 등)로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

아시아태평양의 생명보험 및 손해보험 시장 동향과 인사이트

의료비 급등과 공적 보험 제도의 미비점을 배경으로 한 민간 의료보험의 확대

2026년 1월, 인도의 의료보험료는 전년 동월 대비 27.17% 증가했습니다. 이는 소매용 보험 계약에 대한 GST(상품 및 서비스세)가 18%에서 5%로 인하된 점과 ‘아유슈만 바라트’ 제도의 이용 확대에 힘입어 총 순보험료가 37.78% 증가한 것이 뒷받침되었습니다. Aon의 보고서에 따르면, 2026년 인도의 의료비 증가율은 11.5%로 세계 평균을 상회하며, 많은 소비자들이 만성 질환이나 전문 치료 비용을 충당하기 위해 보상 한도가 더 높은 보험 상품으로 전환하고 있는 것으로 지적되고 있습니다. 중국에서는 2026년 의료비 증가율이 11.1%를 나타낼 것으로 전망되고 있으며, 2025년까지 기준금리가 하락함에 따라 각 보험사들은 보장 금액이 낮은 배당형 의료보험 상품으로의 전환을 추진하고 있습니다. 이는 저금리 환경에 맞추어 상품의 수익성을 조정하는 한편, 보험금 지급 증가에 대응하기 위한 조치입니다. 싱가포르, 말레이시아, 필리핀은 이 지역에서 2026년 의료비 상승률이 가장 급격한 국가 중 하나로 꼽히며, 규제 당국은 이용을 억제하고 부정행위를 방지하기 위해 본인부담금 및 면책액을 통한 비용 분담 제도를 도입하고 있습니다. 스위스리는 2024년 기준 아시아의 의료 보장 격차를 보험료 기준으로 2,580억 달러로 추산하며, 민간 보험, 소액 보험, 단체 보험을 통한 접근성 확대에 큰 여지가 있음을 시사하고 있습니다. 말레이시아의 ‘저렴한 의료 로드맵’이나 인도네시아의 공동보험 의무화 선택적 연기 같은 정책 체계는 저렴한 비용, 지속가능성, 그리고 더 광범위한 보장 범위 사이에서 지속적인 균형이 유지되고 있음을 보여줍니다.

유리한 금리 환경과 연금 개혁을 배경으로, 생명보험과 퇴직 저축이 회복세를 보이고 있습니다.

일본의 생명보험 부문은 2030년까지 연평균 5.4%의 성장 궤도에 올라 있으며, 2024년 정책 전환 이후 수익률이 개선되고 엔화 표시 저축 상품의 지급 이율이 상승함에 따라 직접 보험료 수입은 3,377억 달러에 달할 것으로 전망됩니다. 중국에서는 2024년 12월, 세제 혜택과 유리한 인출 제도를 갖춘 전국적인 자발적 개인연금 제도가 도입되었으며, 2024년 11월까지 7,280만 건의 계좌가 개설되었습니다. 또한, 기업들의 조기 도입은 보완적인 퇴직연금 제도에 대한 관심이 높아지고 있음을 보여줍니다. 한국은 기금의 장기적인 지급 능력 유지와 소득 대체율 향상을 목적으로, 2026년부터 국민연금 제도의 보험료율을 9%에서 13%로 단계적으로 인상할 것을 제안했습니다. 인도의 연금 개혁에서는 특정 인출에 대한 대기 기간 연장 및 최소 잔액 규정이 도입되었습니다. 한편, 2025년 9월부터 시행된 생명보험 및 의료보험 보험료에 대한 GST(상품 및 서비스세) 면제는 보험료 부담 경감과 장기적인 복리 효과 증진에 기여하고 있습니다. 일본과 한국의 인구 고령화, 그리고 인도의 고령층 확대는 아시아태평양의 생명보험 및 손해보험 시장에서 연금, 의료 특약, 보장형 저축보험에 대한 지속적인 수요를 뒷받침하고 있습니다.

재보험 인수 여력과 엄격한 계약 조건이 자연재해 보험료율과 면책액을 끌어올려, 합리적인 가격으로 가입하는 데 부담을 주고 있습니다.

2025년 아시아태평양 지역의 재해 손실액은 730억 달러에 달했으나, 보험금 지급액은 고작 90억 달러에 그쳐 막대한 무보험 격차가 남았습니다. 이 때문에 격차를 신속하게 메울 수 있는 가격 수준에서 재보험 수용 능력을 투입하려는 의지가 위축되고 있습니다. 2024년 4월 대만에서 발생한 규모 7.2의 지진은 총 13억 달러의 피해액과 심각한 사업 중단을 초래했으며, 이로 인해 손해 실적이 양호한 시장과 비교하여 이후 갱신 계약에서 보험료율 인상과 계약 조건의 강화로 이어졌습니다. 태국에서도 지진이나 태풍으로 인한 활동 이후, 보험료율이 상승하는 현상이 나타났습니다. 이는 2025년 말까지 전 세계 재보험사의 자본이 사상 최고 수준에 도달했음에도 불구하고 발생한 일입니다. 필리핀의 손해보험 부문은 견조한 성장세를 보이고 있지만, 반복되는 이상 기후로 인한 보험금 청구 증가에 직면해 있어, 각 보험사는 보장 범위의 폭과 보험료의 부담 가능성 사이에서 균형을 맞추고 있습니다. 호주의 사이클론 풀에서는 2025년에 막대한 보험금 청구가 발생했으나, 정부가 지원하는 보험 인수 능력 덕분에 풀 설립 이전 시기와 비교해 위험이 높은 지역의 보험료는 하락했습니다. 2026년 1월 갱신 계약에서는 무사고 계약의 상당수에서 보험료가 하락하는 추세를 보였으나, 면책 금액과 공동 부담률은 상승했으며, 특정 자연재해 위험에 노출된 재보험 계약자 중에는 보험료가 보합세에서 두 자릿수 증가를 기록한 사례도 있어, 아시아태평양의 생명보험 및 손해보험 시장에서 결과의 편차가 두드러지게 나타났습니다.

부문별 분석

2025년, 생명보험은 아시아태평양의 생명보험 및 손해보험 시장 점유율의 63.21%를 차지했습니다. 이는 중국이나 일본과 같은 대규모 시장에서 장기 보장, 연금, 저축 상품에 대한 수요가 뒷받침한 결과입니다. 아시아태평양의 생명·손해보험 시장에서 건강보험 시장 규모는 2031년까지 연평균 성장률(CAGR) 9.10%로 성장할 전망입니다. 이는 의료비 인플레이션, 만성 질환 유병률의 상승, 그리고 고용주가 보험 가입을 장려하도록 유도하는 규제적 조치로 인해 보험금 청구 빈도와 심각도가 증가하면서 보험료 인상을 부추기고 있기 때문입니다. 자동차 보험 분야는 중국 및 일부 아세안 시장의 자동차 판매량 증가와 전기차(EV) 보급의 혜택을 누리고 있지만, 배터리 및 특수 부품과 관련된 보험금 지급 비용은 여전히 수익성 측면에서 과제로 남아 있습니다. 재산보험의 보험료는 자연재해 위험에 노출된 시장에서 조정이 진행되고 있으며, 이러한 시장에서는 인수 규율과 재보험 구조가 갱신 시 보험료율 및 면책 한도 결정에 영향을 미치고 있습니다. 배상책임보험 및 특수보험 분야는 기업의 리스크 이전에 대한 관심이 확대됨에 따라 소규모 기반에서 성장하고 있으며, 브로커를 통한 계약 주선 및 구조화된 솔루션이 이러한 확산을 뒷받침하고 있습니다.

의료 보험의 호조는 규제 당국과 고용주가 비용 분담과 책임 있는 이용을 장려하기 위해 본인 부담금, 면책액 및 보험 플랜 재설계를 도입하고 있는 지역에서 특히 두드러지게 나타납니다. 인도의 소액 의료보험 부문은 감세 정책의 호재와 디지털화를 통한 가입 절차 개선을 바탕으로 2026년까지 성장이 가속화되었습니다. 한편, 단체 의료보험의 갱신 요율 산정은 이용 데이터와 급여 한도를 반영함으로써 더욱 세밀하게 이루어지고 있습니다. 중국과 인도의 자동차 보험사들은 전기화 및 이용 패턴의 변화에 따라 위험을 구분하고 손실 추세를 완화하기 위해 행동 기반 가격 책정 및 텔레매틱스를 도입하고 있습니다. 아시아태평양의 생명보험 및 손해보험 시장에서는 수익률 환경의 변화에 따라 저축형 및 보장형 보험 상품의 혁신이 계속되고 있으며, 보장 수익률이 인하된 분야에서는 배당형 및 유닛링크형 상품의 점유율이 확대되고 있습니다. 이러한 변화는 2031년까지 아시아태평양의 생명보험 및 손해보험 시장에서 생명보험과 손해보험 양쪽 포트폴리오 모두에서 보험금 지급 설계가 보다 데이터 기반이며 모듈식 접근 방식으로 전환될 것임을 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the asia-Pacific life and non-Life insurance market size is projected to be USD 2.08 trillion in 2025, USD 2.20 trillion in 2026, and reach USD 2.91 trillion by 2031, growing at a CAGR of 5.77% from 2026 to 2031.

This report is Segmented by Insurance Type (Life Insurance, Non-Life Insurance (Motor, Health, Property, Liability and More)), Customer Segment (Retail, and Corporate), Distribution Channel (Broker, Agents, Banks, Direct Sales, and Other Channels), and Geography (India, China, Japan, Australia, South Korea, Southeast Asia and More). The Market Forecasts are Provided in Value (USD).

Asia-Pacific Life And Non-Life Insurance Market Trends and Insights

Private Health Insurance Expansion Amid Medical Inflation And Public Scheme Gaps

India's health insurance premiums rose 27.17% year over year in January 2026, supported by a reduction of GST on retail policies from 18% to 5% and stronger Ayushman Bharat uptake that lifted gross written premiums by 37.78%. Aon reported India's 2026 medical trend at 11.5%, higher than the global average, and noted that most consumers are moving to higher coverage limits to manage the costs of chronic conditions and specialty treatments. In China, medical trend rates are projected at 11.1% for 2026, and insurers are pivoting to participating health products with lower guarantees as benchmark rates fell through 2025, aligning product economics with a lower-yield environment while addressing claims inflation. Singapore, Malaysia, and the Philippines face some of the steepest 2026 medical trend rates in the region, with regulators adding cost-sharing through co-payments and deductibles to temper utilization and fraud. Swiss Re estimated Asia's health protection gap at USD 258 billion in premium-equivalent terms as of 2024, signaling significant headroom for private cover, micro-policies, and group schemes to expand access. Policy frameworks like Malaysia's affordable health roadmap and selective delays to co-insurance mandates in Indonesia indicate an ongoing balance between affordability, sustainability, and wider coverage.

Life Protection And Retirement Savings Rebound Under Favorable Rates And Pension Reforms

Japan's life sector is on a 5.4% growth path through 2030, reaching USD 337.7 billion in direct written premiums as yields improved after the 2024 policy shift, lifting credited rates on yen-denominated savings products. China's nationwide voluntary personal pensions, implemented in December 2024 with tax incentives and a favorable withdrawal structure, drew 72.8 million account openings by November 2024, and early corporate adoption signals rising interest in supplemental retirement plans. South Korea proposed raising National Pension Scheme contributions from 9% to 13% starting in 2026 with phased increases, targeting longer fund solvency and an improved income replacement rate. India's pension reforms introduced longer waiting periods for certain withdrawals and a minimum balance rule, while the GST exemption on life and health premiums set in September 2025 supports better affordability and long-term compounding. Demographic aging across Japan and South Korea, together with India's expanding senior cohort, is reinforcing persistent demand for annuities, health riders, and protection-backed savings policies in the Asia-Pacific life and non-life insurance market.

Reinsurance Capacity And Tight Terms Raising NatCat Rates And Deductibles, Pressuring Affordability

Asia-Pacific's USD 73 billion in 2025 disaster losses carried only USD 9 billion in insured payouts, leaving a large uninsured gap that constrains appetite to deploy capacity at price levels that would close the gap quickly. Taiwan's 7.2 magnitude earthquake in April 2024 caused USD 1.3 billion in overall losses with significant business interruption, which drove higher pricing and stricter terms at subsequent renewals relative to markets with benign loss experience. Thailand also saw rate increases after seismic and typhoon activity, even as global reinsurer capital reached record levels by late 2025. The Philippines' property segment is experiencing stronger growth but faces rising claims tied to recurring severe weather, with insurers balancing coverage breadth against affordability pressures. Australia's cyclone pool saw large claim volumes in 2025, yet government-backed capacity helped lower premiums in higher-risk areas compared with the period before the pool's establishment. At January 2026 renewals, softening was evident for many loss-free accounts, but deductibles and co-participations rose, and certain catastrophe-exposed cedants faced flat to double-digit increases, underscoring heterogeneous outcomes within the Asia-Pacific life and non-life insurance market.

Other drivers and restraints analyzed in the detailed report include:

- Motor Exposure Growth And EV-Led Telematics And Usage-Based Pricing Adoption

- Climate And Catastrophe Risk Repricing Lifting Property And Engineering Premiums

- Bancassurance Conduct And Product Rules Curbing Investment-Linked Sales In Select Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Life insurance held 63.21% of the Asia-Pacific life and non-life insurance market share in 2025, supported by demand for long-term protection, annuities, and savings products in large markets such as China and Japan. The Asia-Pacific life and non-life insurance market size for health insurance is set to grow at a 9.10% CAGR through 2031, as medical inflation, chronic disease prevalence, and regulatory nudges for employer coverage increase both frequency and severity of claims and drive premium expansion. Motor lines are benefitting from higher vehicle sales and EV penetration in China and select ASEAN markets, although claim costs linked to batteries and specialized parts remain a profitability challenge. Property premiums are adjusting in catastrophe-exposed markets, where underwriting discipline and reinsurance structures are steering rate and deductible decisions at renewal. Liability and specialty lines are growing from smaller bases as corporate risk transfer preferences broaden, with adoption aided by broker placement and structured solutions.

Health's outperformance is visible where regulators and employers introduce co-payments, deductibles, and plan redesign to share costs and encourage responsible utilization. India's retail health segment accelerated into 2026 on the back of a tax-cut tailwind and better digital onboarding, while group health renewal pricing has become more granular, incorporating utilization data and benefit caps. Motor insurers across China and India are deploying behavior-based pricing and telematics to differentiate risk and mitigate loss trends as electrification and usage patterns evolve. The Asia-Pacific life and non-life insurance market continues to see product innovation in savings and protection policies as yield environments change, with participating and unit-linked structures gaining share where guaranteed returns were lowered. These shifts point to a more data-driven and modular approach to benefit design through 2031 in both life and non-life portfolios in the Asia-Pacific life and non-life insurance market.

List of Companies Covered in this Report:

- China Life Insurance (Group) Company

- Ping An Insurance (Group) Company of China, Ltd.

- People's Insurance Company of China (PICC)

- Nippon Life Insurance Company

- Dai-ichi Life Holdings, Inc.

- China Pacific Insurance (Group) Co., Ltd. (CPIC)

- AIA Group Limited

- Tokio Marine Holdings, Inc.

- MS&AD Insurance Group Holdings, Inc.

- Sompo Holdings, Inc.

- QBE Insurance Group Limited

- Insurance Australia Group (IAG)

- Suncorp Group Limited

- Life Insurance Corporation of India (LIC)

- HDFC Life Insurance Company Limited

- SBI Life Insurance Company Limited

- ICICI Prudential Life Insurance Company Limited

- Samsung Life Insurance Co., Ltd.

- Hanwha Life Insurance Co., Ltd.

- Cathay Life Insurance Co., Ltd.

- Fubon Life Insurance Co., Ltd.

- Great Eastern Holdings Limited

- Prudential plc (Asia)

- Manulife Asia

- Sun Life Asia

- AXA Asia & Africa

- Chubb Asia Pacific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Private health insurance expansion amid medical inflation and public scheme gaps (China, India, SEA)

- 4.2.2 Life protection and retirement savings rebound under favorable rates and pension reforms

- 4.2.3 Motor exposure growth and EV-led telematics/usage-based pricing adoption

- 4.2.4 Climate and catastrophe risk repricing lifting property and engineering premiums

- 4.2.5 Embedded insurance via super-apps and real-time payments rails scaling micro coverage

- 4.2.6 IFRS 17 and RBC modernization enabling product redesign and data-driven distribution

- 4.3 Market Restraints

- 4.3.1 Reinsurance capacity/tight terms raising NatCat rates and deductibles, pressuring affordability

- 4.3.2 Bancassurance conduct and product rules curbing investment-linked sales in select markets

- 4.3.3 Health claims inflation elevating loss ratios and premium burdens for employers/retail

- 4.3.4 Capital, talent and data-governance frictions under IFRS17/RBC slowing launches at mid-tier carriers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (value)

- 5.1 By Insurance Type

- 5.1.1 Life Insurance

- 5.1.2 Non-Life Insurance

- 5.1.2.1 Motor Insurance

- 5.1.2.2 Health Insurance

- 5.1.2.3 Property Insurance

- 5.1.2.4 Liability Insurance

- 5.1.2.5 Other Insurance

- 5.2 By Customer Segment

- 5.2.1 Retail

- 5.2.2 Corporate

- 5.3 By Distribution Channel

- 5.3.1 Brokers

- 5.3.2 Agents

- 5.3.3 Banks

- 5.3.4 Direct Sales

- 5.3.5 Other Channels

- 5.4 By Geography

- 5.4.1 India

- 5.4.2 China

- 5.4.3 Japan

- 5.4.4 Australia

- 5.4.5 South Korea

- 5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 China Life Insurance (Group) Company

- 6.4.2 Ping An Insurance (Group) Company of China, Ltd.

- 6.4.3 People's Insurance Company of China (PICC)

- 6.4.4 Nippon Life Insurance Company

- 6.4.5 Dai-ichi Life Holdings, Inc.

- 6.4.6 China Pacific Insurance (Group) Co., Ltd. (CPIC)

- 6.4.7 AIA Group Limited

- 6.4.8 Tokio Marine Holdings, Inc.

- 6.4.9 MS&AD Insurance Group Holdings, Inc.

- 6.4.10 Sompo Holdings, Inc.

- 6.4.11 QBE Insurance Group Limited

- 6.4.12 Insurance Australia Group (IAG)

- 6.4.13 Suncorp Group Limited

- 6.4.14 Life Insurance Corporation of India (LIC)

- 6.4.15 HDFC Life Insurance Company Limited

- 6.4.16 SBI Life Insurance Company Limited

- 6.4.17 ICICI Prudential Life Insurance Company Limited

- 6.4.18 Samsung Life Insurance Co., Ltd.

- 6.4.19 Hanwha Life Insurance Co., Ltd.

- 6.4.20 Cathay Life Insurance Co., Ltd.

- 6.4.21 Fubon Life Insurance Co., Ltd.

- 6.4.22 Great Eastern Holdings Limited

- 6.4.23 Prudential plc (Asia)

- 6.4.24 Manulife Asia

- 6.4.25 Sun Life Asia

- 6.4.26 AXA Asia & Africa

- 6.4.27 Chubb Asia Pacific

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment