|

시장보고서

상품코드

2066403

대량 통지 시스템 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Mass Notification Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

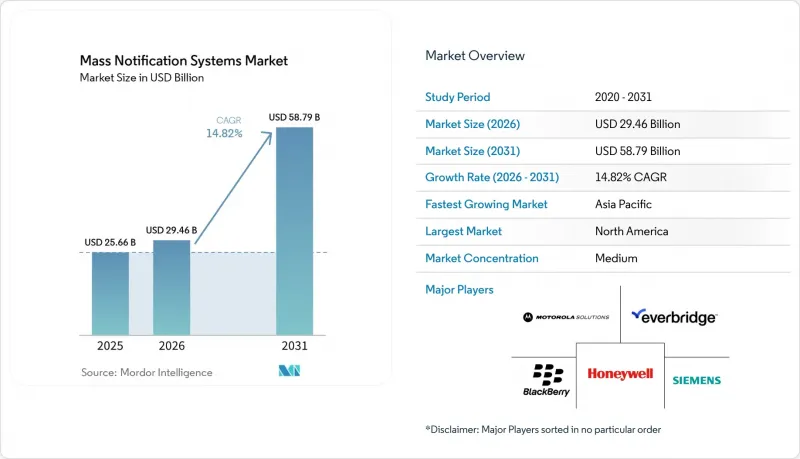

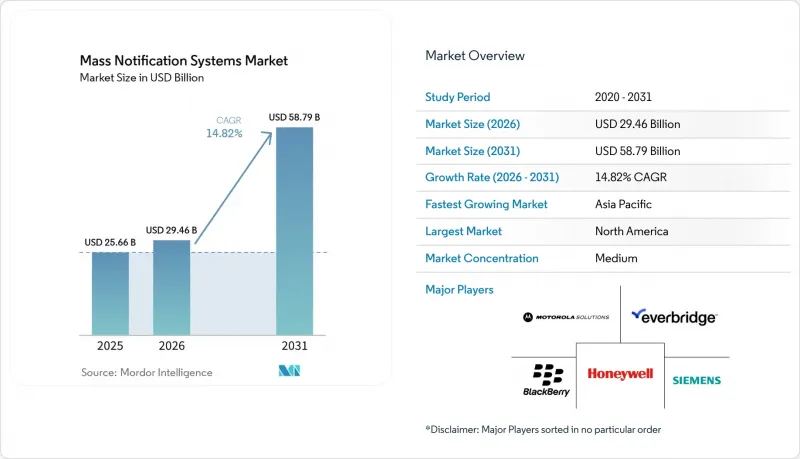

Mordor Intelligence에 의하면, 대량 통지 시스템 시장 규모는 2025년 256억 6,000만 달러로 평가되었고, 2026년에는 294억 6,000만 달러로 추정되고, 2026-2031년 CAGR 14.82%로 성장을 지속할 전망이며, 2031년에는 587억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서에서는 업계를 구성 요소별(솔루션, 서비스, 하드웨어), 도입 형태별(클라우드, 온프레미스, 하이브리드), 용도별(실내, 광역 등), 솔루션 목적별(사업 연속성 및 재해 복구 등), 최종 사용자 산업별(정부 및 국방 등), 그리고 지역별로 분류하고 있습니다. 시장 규모 및 전망은 금액(달러)으로 표시되어 있습니다.

세계의 대량 알림 시스템 시장 동향 및 인사이트

5G 보급이 가속화됨에 따라 실시간 멀티미디어 경보가 가능해졌습니다.

5G는 기가비트급 처리량과 밀리초 단위의 지연 시간을 실현하여, 플랫폼이 단순한 텍스트뿐만 아니라 고해상도 동영상, 평면도, 상호작용형 대피 지도 등을 제공할 수 있게 합니다. 일본, 한국, 싱가포르의 도심 지역에서는 이미 수신자가 시내를 이동함에 따라 상황에 맞추어 조정되는 위치 정보 기반 경보 시스템이 활용되고 있습니다. 통신사에 따르면, 대규모 행사 시 접속 만족도는 4G에 비해 20% 향상되었으며, 이 데이터는 네트워크 혼잡을 예상하여 계획을 수립하는 비상사태 관리 담당자들에게 큰 힘이 됩니다. 네트워크 슬라이싱 및 엣지 컴퓨팅 기능을 탑재할 수 있는 벤더들은 속도, 중복성, 컨텐츠의 풍부함 측면에서 차별화를 꾀하고 있습니다. 주파수 경매가 지속되고 단말기 보급률이 높아짐에 따라, 대량 알림 시스템 시장은 5G 커버리지 목표와 연계된 공공 안전 관련 추가 자금을 확보하게 될 것입니다.

EU의 EECC 제110조가 멀티채널 대응을 추진

이 지침은 EU 회원국 27개국 모두에게 ‘영향을 받는 인구의 최대 수’에 도달할 것을 의무화하고 있으며, 각국 정부는 셀 브로드캐스트, 위치 기반 SMS, 앱을 통한 경보를 조합하여 활용하도록 요구받고 있습니다. 규정 준수를 위해 배정된 자금을 바탕으로, 다국어 컨텐츠, 양방향 메시징, 국경을 초월한 상호 운용성을 지원하는 하이브리드 플랫폼의 도입이 가속화되고 있습니다. 상업용 사용자들도 사업 연속성을 위한 통신 효율화를 위해 유사한 아키텍처를 채택하고 있으며, 이로 인해 예상보다 빨리 민간 투자가 대량 알림 시스템 시장으로 유입되고 있습니다.

단편화된 주파수 정책이 아프리카에서의 도입을 저해하고 있습니다.

셀 브로드캐스트는 조화로운 주파수 대역 지침에 따라 운영되지만, 아프리카 54개국에서는 정책이 크게 다릅니다. 각 벤더사는 통신 사업자별로 개별적인 통합 대응을 강요받고 있어, 시범 사업의 장기화와 비용 증가를 초래하고 있습니다. 그 결과, 3G 및 4G의 커버리지율이 90%를 넘고 있음에도 불구하고, 공공 안전 분야에서의 도입이 지연되고 있습니다. 지역적 조화를 위한 노력이 진행 중이지만, 이러한 노력이 성숙기에 접어들기 전까지는 다른 신흥 지역에 비해 성장세가 둔화될 것으로 보입니다.

부문별 분석

솔루션 분야의 일괄 알림 시스템 시장 규모는 2025년에 168억 달러에 달했습니다. 이는 행정 기관과 기업이 하드웨어 중심의 체제에서 명령 센터용 소프트웨어로 전환한 결과, 65.50%의 점유율을 차지하게 된 것입니다. 이 소프트웨어는 SMS, 음성, 이메일, 사이렌, 사이니지를 하나의 콘솔로 통합하여 교육 필요성과 라이선스 중복을 줄여줍니다. 향후 10년의 후반에는 수신자의 행동을 예측하는 분석 모듈이 기존 고객의 업그레이드를 촉진할 것으로 예상되며, 솔루션 매출은 두 자릿수 성장세를 유지할 전망입니다. 서비스 부문은 시장 점유율은 작지만, 통합, 맞춤형 서비스, 연중무휴 24시간 모니터링에는 전문적인 기술이 요구되기 때문에 연평균 성장률(CAGR) 17.9%로 성장하고 있습니다.

하드웨어는 스트로브 비콘, 벽걸이형 스피커, 실외 사이렌이 여전히 필수적인 공장, 공항, 학교 등에서 확고한 입지를 유지하고 있습니다. 그러나 각 제조업체는 이러한 기기에 IP 연결 기능을 탑재하여 중앙 플랫폼에 상태를 보고할 수 있도록 하고 있습니다. 전문 서비스 팀은 평가, 규제 관련 컨설팅, 라이프사이클 유지보수를 다년 계약 형태로 패키지화하고 있으며, 이를 통해 공급업체에게는 예측 가능한 현금 흐름을 제공하고, 고객에게는 예상치 못한 비용 발생을 억제하고 있습니다. 이러한 매니지드 모델은 대규모 알림 시스템 시장에서 솔루션의 경쟁 우위를 더욱 확대되고 있습니다.

2025년에는 관리자들이 즉각적인 확장성, 종량제, 번거롭지 않은 업그레이드를 선호함에 따라 클라우드가 대량 알림 시스템 시장의 70.30%를 차지했습니다. SaaS 플랫폼은 수십 곳에 걸친 거점을 보유한 대기업의 멀티테넌트 관리도 간소화했습니다. 이 모델은 IT 인력을 보유하지 않은 중소기업들로부터도 지지를 얻으며, 신규 도입 기업 수의 최대 증가를 이끌고 있습니다. 그렇긴 하지만, 데이터 주권에 관한 규제, 온프레미스 환경에서의 내결함성 필요성, 벤더 종속성에 대한 우려로 인해 금융 서비스, 유틸리티, 병원 분야는 하이브리드 방식의 접근 방식으로 전환하고 있습니다. 하이브리드형 도입은 연평균 성장률(CAGR) 19.65%를 나타낼 것으로 예측되며, 이는 도입 형태 중 가장 높은 성장률입니다.

온프레미스 배포는 축소되는 추세이지만, 완전히 사라지지는 않을 것입니다. 중요 인프라의 소유자는 외부 연결이 끊긴 경우에도 메시지 전송이 원활하게 이루어지도록, 러기드 서버에서 로컬 인스턴스를 지속적으로 가동하는 경우가 많습니다. 컨테이너화된 아키텍처 덕분에 운영 담당자는 퍼블릭 클라우드와 로컬 클러스터 간에 워크로드를 이동할 수 있게 되어, 비용과 제어 간의 균형을 맞출 수 있게 되었습니다. 이러한 유연성이 주류가 됨에 따라, 일괄 알림 시스템 시장에서는 ‘클라우드’와 ‘온프레미스’의 경계가 모호해지며, 구매자들은 단일한 획일적인 모델이 아닌 워크로드별 정책을 선택하게 될 것입니다.

지역별 분석

북미는 2025년 매출의 39.60%를 차지했으며, 이는 성숙한 통신 인프라, 보조금, 그리고 극심한 기상 현상의 발생 실적을 반영한 것입니다. 지자체에서는 현재 교통 센서, 홍수 수위계, 산불 감시 카메라를 자동 알림 메시지와 연동하는 광범위한 스마트시티 플랫폼에 일제 경보 기능을 통합하고 있습니다. 또한, 클라우드 네이티브 업그레이드는 해당 지역의 엄격한 사이버 보험 요건과 맞물려, 모든 도입 환경에 데이터 보호 기능이 확실하게 통합되도록 하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 16.9%로 성장했으며, 이는 모든 지역 중 가장 높은 수치입니다. 한국, 일본, 호주에서 5G 도입이 가속화됨에 따라, 행정 기관은 경보에 동영상 클립이나 다국어 자막을 첨부할 수 있게 되어, 인구 밀집 도시에서의 이해도가 높아지고 있습니다. 필리핀 등 태풍이 빈번하게 발생하는 국가들의 재해 회복력 강화를 위한 정부의 경제 대책에 힘입어, 대량 알림 시스템 시장에 새로운 자본이 유입되고 있습니다. 한편, 중국의 메가시티 프로젝트에서는 경보 시스템을 감시 카메라 및 전자 지갑 기능을 갖춘 슈퍼 앱과 통합하여, 공공 안전과 일상적인 디지털 행동을 융합하고 있습니다.

유럽은 이 두 극단 사이의 중간에 위치하고 있지만, 그 성장은 규제 준수가 주도하고 있습니다. EECC 제110조의 기한에 따라 모든 회원국은 멀티채널 경보 예산을 확보할 수밖에 없게 되었으며, 한편 GDPR(EU 개인정보보호규정)에 따라 공급업체는 동의 관리 및 데이터 최소화에 대한 투자를 강요받게 되었습니다. 북유럽에서 다국어 컨텐츠에 주력하고 있는 탓에 일부 프로젝트의 진행이 지연되고 있지만, 궁극적으로는 수출용 제품 기능을 확충하는 결과로 이어지고 있습니다. EU 지침의 적용을 받지 않고 운영되고 있는 영국은 셀 브로드캐스트 모범 사례에 부합하는 독자적인 기준을 마련하여, 국경을 초월한 상호 운용성을 지속적으로 보장하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the mass notification systems market size is expected to grow from USD 25.66 billion in 2025 to USD 29.46 billion in 2026 and is forecast to reach USD 58.79 billion by 2031 at 14.82% CAGR over 2026-2031.

This report Segments the Industry Into Component (Solution, Services, Hardware), Deployment (Cloud, On-Premise, Hybrid), Application (In-Building, Wide-Area and More), Solution Purpose (Business Continuity and Disaster Recovery, and More), End-User Vertical (Government and Defense, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Mass Notification Systems Market Trends and Insights

Accelerated 5G roll-outs enabling real-time multimedia alerting

5G brings gigabit throughput and millisecond latency, allowing platforms to push high-definition video, floor plans, and interactive evacuation maps rather than plain text. Urban centers in Japan, South Korea, and Singapore already use location-based warnings that adapt as recipients move through a city. Operators report 20% higher connectivity satisfaction during large events compared with 4G, a data point that reassures emergency managers planning for congested networks. Vendors able to embed network- slicing and edge-compute features are differentiating on speed, redundancy, and content richness. As spectrum auctions continue and device penetration rises, the mass notification systems market will capture incremental public-safety funding tied to 5G coverage targets.

EU's EECC Article 110 driving multi-channel compliance

The code obliges all 27 EU states to reach "the maximum possible affected population," pushing governments to marry cell broadcast, location-based SMS, and app alerts. Funding streams earmarked for compliance have accelerated roll-outs of hybrid platforms that support multilingual content, two-way messaging, and cross-border interoperability. Commercial users are following the same architecture to streamline business continuity communications, pulling private investment into the mass notification systems market sooner than projected.

Fragmented spectrum policies hampering African adoption

Cell broadcast relies on harmonized spectrum guidelines, yet policies vary widely across 54 African nations. Vendors face custom integrations for each carrier, prolonging pilots and inflating costs, which slows public-safety deployments even as 3G and 4G coverage climbs above 90%. Regional harmonization efforts are underway, but until they mature, growth lags other emerging regions.

Other drivers and restraints analyzed in the detailed report include:

- Escalating climate catastrophes accelerating municipal deployments

- Campus digitization transforming educational safety

- Cyber-insurance premiums elevating cloud TCO in healthcare

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The mass notification systems market size for solutions reached USD 16.8 billion in 2025, translating to a 65.50% share as agencies and enterprises replaced hardware-centric setups with command-center software. Software unifies SMS, voice, email, sirens, and signage under one console, reducing training needs and license duplication. In the second half of the decade, analytics modules that predict recipient behavior are expected to prompt upgrades among existing customers, keeping solutions revenue on a double-digit climb. Services, while a smaller slice, are advancing at an 17.9% CAGR because integration, customization, and 24/7 monitoring demand specialist skills.

Hardware retains a foothold in plants, airports, and schools where strobe beacons, wall-mounted speakers, and outdoor sirens remain mission critical. Yet manufacturers are embedding IP connectivity in these devices so they can report status back to the central platform. Professional services teams are packaging assessments, regulatory consulting, and lifecycle maintenance into multi-year contracts, creating predictable cash flow for vendors and lowering surprise costs for clients. Such managed models are further widening the solutions edge within the mass notification systems market.

Cloud captured 70.30% of the mass notification systems market in 2025 as administrators favored instant scale, pay-as-you-go pricing, and hassle-free upgrades. SaaS platforms also simplified multi-tenant management for large enterprises spanning dozens of sites. That model resonates with SMEs that lack IT staff, fueling the highest net-new logo count. Even so, data-sovereignty rules, the need for on-site survivability, and concerns over vendor lock-in are steering financial services, utilities, and hospitals toward hybrid approaches. Hybrid adoption is forecast to grow at 19.65% CAGR, the fastest rate in deployment choices.

On-premise deployments are shrinking but will not disappear. Critical infrastructure owners often keep a local instance running on hardened servers so messages still flow when external links fail. Containerized architectures now let operators shift workloads between public clouds and local clusters, balancing cost and control. As such flexibility becomes mainstream, the mass notification systems market will likely see blurred lines between "cloud" and "on-premise," with buyers selecting per-workload policies rather than a single blanket model.

Geography Analysis

North America retained 39.60% of 2025 revenue, reflecting mature telecommunications infrastructure, grant funding, and a track record of extreme weather events. Municipalities now embed mass alerting into broader smart-city platforms that tie traffic sensors, flood gauges, and wildfire cameras to automatic outbound messaging. Cloud-native upgrades also coincide with the region's high cyber-insurance requirements, ensuring data protection features are woven into every deployment.

Asia-Pacific is expanding at a 16.9% CAGR, the highest among all regions. Accelerated 5G roll-outs in South Korea, Japan, and Australia let agencies attach video clips and multilingual subtitles to alerts, boosting comprehension in dense cities. Government stimulus for disaster resilience in typhoon-prone nations such as the Philippines is funneling fresh capital into the mass notification systems market. Meanwhile China's mega-city projects integrate alerts with surveillance cameras and e-wallet super-apps, blending public safety with everyday digital behavior.

Europe sits between these extremes, but its growth is dominated by regulatory compliance. The EECC Article 110 deadline drove every member state to budget for multi-channel warnings, while GDPR pushed vendors to invest in consent management and data minimization. The Nordic region's focus on multilingual content slows some projects but ultimately broadens product capability for export. The United Kingdom, operating outside EU directives, is drafting its own standards that still align with cell broadcast best practice, ensuring continued cross-border interoperability.

- Everbridge Inc.

- Motorola Solutions Inc.

- Honeywell International Inc.

- Siemens AG

- Blackberry AtHoc Inc.

- Eaton Corp.

- OnSolve LLC

- Singlewire Software LLC

- Alertus Technologies LLC

- xMatters

- AlertMedia Inc.

- F24 AG

- Rave Mobile Safety

- Regroup Mass Notification

- HipLink Software

- Volo (Volo Alert)

- BlackBoard Connect (Anthology)

- Preparis (Agility Recovery)

- Pocketstop RedFlag

- Vecima Networks (Engage IP)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated 5G roll-outs enabling real-time, multimedia alerting in APAC

- 4.2.2 Mandated multi-channel public-warning regulations in EU (EECC Article 110)

- 4.2.3 Escalating climate-induced catastrophes in North America driving municipal deployments

- 4.2.4 Rapid campus digitization creating BYOD-ready safety ecosystems in Higher-Ed

- 4.2.5 Utilities' grid-modernization projects demanding OT/IT converged alert platforms

- 4.3 Market Restraints

- 4.3.1 Fragmented spectrum policies delaying cell-broadcast adoption in Africa

- 4.3.2 Rising cyber-insurance premiums increasing TCO for cloud MNS in healthcare

- 4.3.3 Alarm fatigue concerns curbing message frequency in large enterprises

- 4.3.4 Limited multilingual content libraries slowing uptake in the Nordics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Fire Alarm Control Panels

- 5.1.1.2 Public Address and Voice Evacuation Systems

- 5.1.1.3 Notification Beacons and Digital Signage

- 5.1.2 Solutions

- 5.1.2.1 Emergency/Mass Notification Software

- 5.1.2.2 Incident Management and Situation Awareness

- 5.1.3 Services

- 5.1.3.1 Professional (Consulting, Integration)

- 5.1.3.2 Managed Services

- 5.1.1 Hardware

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Solution Purpose

- 5.3.1 Business Continuity and Disaster Recovery

- 5.3.2 Integrated Public Alert and Warning

- 5.3.3 Interoperable Emergency Communication

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Mid-size Enterprises (SMEs)

- 5.5 By Application

- 5.5.1 In-Building

- 5.5.2 Wide-Area

- 5.5.3 Distributed Recipient

- 5.6 By End-User Vertical

- 5.6.1 Government and Defense

- 5.6.2 Energy and Utilities

- 5.6.3 Healthcare

- 5.6.4 Education

- 5.6.5 Commercial and Industrial

- 5.6.6 Transportation and Logistics

- 5.6.7 IT and Telecommunications

- 5.6.8 Others

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Rest of Europe

- 5.7.4 Middle East

- 5.7.4.1 GCC

- 5.7.4.2 Turkey

- 5.7.4.3 Rest of Middle East

- 5.7.5 Africa

- 5.7.5.1 South Africa

- 5.7.5.2 Nigeria

- 5.7.5.3 Rest of Africa

- 5.7.6 Asia-Pacific

- 5.7.6.1 China

- 5.7.6.2 Japan

- 5.7.6.3 India

- 5.7.6.4 South Korea

- 5.7.6.5 Southeast Asia

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Everbridge Inc.

- 6.4.2 Motorola Solutions Inc.

- 6.4.3 Honeywell International Inc.

- 6.4.4 Siemens AG

- 6.4.5 Blackberry AtHoc Inc.

- 6.4.6 Eaton Corp.

- 6.4.7 OnSolve LLC

- 6.4.8 Singlewire Software LLC

- 6.4.9 Alertus Technologies LLC

- 6.4.10 xMatters

- 6.4.11 AlertMedia Inc.

- 6.4.12 F24 AG

- 6.4.13 Rave Mobile Safety

- 6.4.14 Regroup Mass Notification

- 6.4.15 HipLink Software

- 6.4.16 Volo (Volo Alert)

- 6.4.17 BlackBoard Connect (Anthology)

- 6.4.18 Preparis (Agility Recovery)

- 6.4.19 Pocketstop RedFlag

- 6.4.20 Vecima Networks (Engage IP)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment