|

시장보고서

상품코드

2066412

북미의 사료용 아미노산 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Feed Amino Acids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

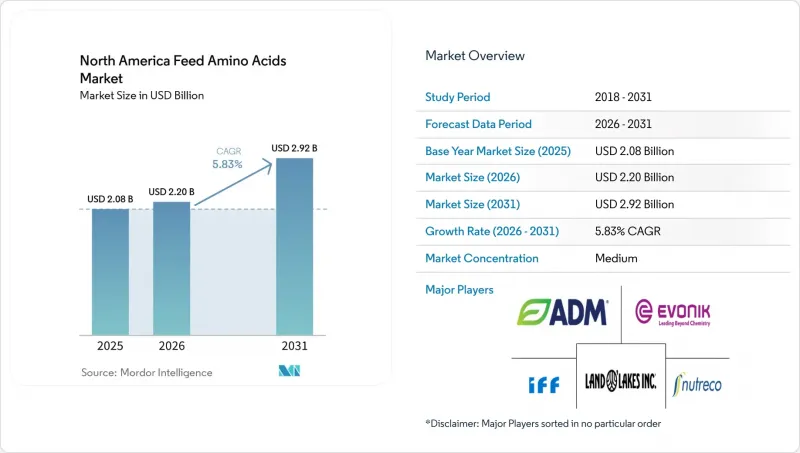

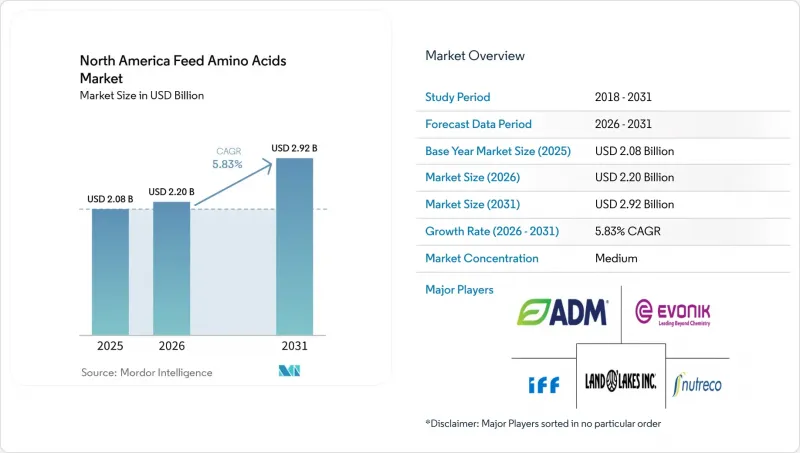

Mordor Intelligence에 의하면, 북미의 사료용 아미노산 시장 규모는 2025년 20억 8,000만 달러로 평가되었습니다. 2026년 22억 달러에서 2031년까지 29억 2,000만 달러에 이를 것으로 예상되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 5.83%를 나타낼 전망입니다.

본 보고서는 부첨가물별(라이신, 메티오닌 등), 대상 동물별(수산물 양식, 가금류, 반추동물 등), 그리고 지역별(캐나다, 멕시코 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(미터톤) 단위로 제시되어 있습니다.

북미의 사료용 아미노산 시장 동향 및 인사이트

가금류 및 돼지 사육 분야에서 고효율 단백질 전환에 대한 수요 증가

축산 농가들은 사료비 급등에 대처하기 위해 사료 전환 효율을 최우선 과제로 삼고 있습니다. 육계 통합 생산 업체들은 메티오닌과 리신을 보충함으로써, 기존 프로그램의 1.8 대 1에 비해 1.5 대 1 미만의 사료 전환율을 일상적으로 달성하고 있으며, 이를 통해 생체중 1kg당 0.15달러의 사료비를 절감하고 있습니다. 트레오닌을 강화한 비육돈용 사료에서는 체중 증가율을 유지하면서 조단백질 함량을 16%에서 14%로 낮출 수 있었습니다. 아미노산 균형을 개선함으로써 질소 배설량을 최대 25% 줄였으며, 여러 주에서 정한 영양 관리 규정을 충족하고 있습니다. 이러한 경제적 이점은 규정 준수 목표 달성을 뒷받침하는 동시에, 북미의 사료용 아미노산 시장에 대한 수요를 공고히 하고 있습니다.

멕시코 및 미국에서의 산업 규모 가금류 사육 사업 확대

멕시코와 미국 전역에서 진행되고 있는 현대화 프로젝트에서는 아미노산의 정확한 배합을 보장하는 자동 투여 시스템이 도입되고 있습니다. 멕시코에서는 2024년, 수천 채의 닭사 전체에 걸쳐 영양 프로파일을 표준화하는 5억 달러 규모의 사료 공장 개보수를 배경으로, 닭고기 생산량이 완만하게 증가했습니다. 미국의 육계 생산 분야에서도 마찬가지로 통합이 진행되고 있으며, 주요 10개사가 국내 생산량의 최대 점유율을 차지하고 있습니다. 이 기업들이 체결하는 다년간의 조달 계약은 안정적인 구매처를 확보해 주며, 아미노산 공급업체의 규모의 경제를 강화하고 있습니다.

아미노산 생산의 수익성에 영향을 미치는 옥수수 및 대두 가격 변동

2024년에는 옥수수 가격 급등으로 인해 리진 생산 비용이 25% 상승하여, 분기별 계약 재검토와 매출 총이익률 축소를 초래했습니다. 메티오닌의 가격은 천연가스 가격 변동에 따라 분기마다 톤당 200-400달러 범위 내에서 변동하고 있습니다. 이러한 불확실성으로 인해 선물 계약이 제한되면서, 북미의 사료용 아미노산 시장 전반에 걸쳐 운전자금 수요가 증가하고 있습니다. 시장에 진출한 기업들은 업무 효율성과 재무적 안정성을 유지하면서, 이러한 급변하는 상황에 적응해야 합니다.

부문별 분석

라이신은 가금류 및 돼지용 옥수수·대두 혼합 사료에서 제1 제한 아미노산으로서의 위상에 힘입어, 2025년에는 북미의 사료용 아미노산 시장에서 42.15%의 점유율을 차지했습니다. 메티오닌 시장은 육계에서의 사용 확대와 젖소를 위한 새로운 루멘 보호형 제품의 등장으로 뒷받침되어, 2026년부터 2031년까지 연평균 성장률(CAGR) 6.05%를 기록하며 성장하고 있습니다. 에보닉사가 앨라배마주 모빌에서 실시한 후방 통합을 통해 메티오닌의 원가가 15% 절감되었으며, 공급 안정성이 향상되었습니다. 트레오닌은 산란계 사료 시장에서 꾸준히 시장 점유율을 확대하고 있는 반면, 트립토판은 운송 시 스트레스를 줄이기 위한 틈새 용도로 채택이 확대되고 있습니다.

메티오닌의 성장을 뒷받침하고 있는 것은 루멘 보호형 제제 분야의 획기적인 기술 혁신이며, 이를 통해 낙농가는 조단백질 함량을 늘리지 않고도 우유 단백질 품질을 향상시킬 수 있게 되었습니다. 발린, 이소류신, 히스티딘 등의 특수 아미노산은 북미의 사료용 아미노산 시장 규모의 10% 미만을 차지할 뿐이지만, 정밀 영양학이 성숙해짐에 따라 향후 성장이 기대되고 있습니다. 각 공급업체는 캡슐화 및 서방 기술과 관련된 지적 재산을 육성하고 있으며, 범용 등급 제품보다 높은 프리미엄 가격을 실현하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 보고서 내용

제3장 주요 요약 및 조사 결과

제4장 주요 업계 동향

제5장 시장 세분화

제6장 경쟁 구도

제7장 CEO에 대한 주요 전략적 질문

KTH 26.06.29According to Mordor Intelligence, the north america feed amino acids market size is projected to expand from USD 2.08 billion in 2025 and USD 2.20 billion in 2026 to USD 2.92 billion by 2031, registering a CAGR of 5.83% between 2026 and 2031.

This report is Segmented by Sub Additive (Lysine, Methionine, and More), by Animal (Aquaculture, Poultry, Ruminants, and More), and Geography (Canada, Mexico, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

North America Feed Amino Acids Market Trends and Insights

Growing demand for high-efficiency protein conversion in poultry and swine production

Livestock producers are prioritizing feed conversion efficiency to counter elevated feed costs. Broiler integrators routinely achieve feed conversion ratios below 1.5:1 after supplementing methionine and lysine, compared with 1.8:1 in conventional programs, reducing feed expense by USD 0.15 for each kilogram of live weight. Swine finisher diets fortified with threonine cut crude protein from 16% to 14% while sustaining gain rates. Improved amino acid balance trims nitrogen excretion by up to 25%, meeting nutrient management rules in several states. These economics solidify demand for the North America feed amino acids market while supporting compliance goals.

Expansion of industrial-scale poultry farming operations in Mexico and the United States

Modernization projects across Mexico and the United States are embedding automated dosing systems that guarantee precise amino acid inclusion. Mexico produced a modest amount of poultry meat in 2024, underpinned by USD 500 million in feed-mill upgrades that standardize nutrient profiles across thousands of houses. United States broiler production is similarly consolidated, with the top ten firms producing the maximum share of national output. Their multi-year procurement contracts create steady off-take, reinforcing economies of scale for amino acid suppliers.

Volatility in corn and soybean prices affecting amino-acid production economics

Surging corn prices lifted lysine production costs 25% in 2024, prompting quarterly contract resets and shrinking gross margins. Methionine costs fluctuate with natural gas swings, moving USD 200-400 per metric ton quarter to quarter. Such uncertainty limits forward contracting and raises working capital needs across the North America feed amino acids market. The market participants must adapt to these dynamic conditions while maintaining operational efficiency and financial stability.

Other drivers and restraints analyzed in the detailed report include:

- Feed-cost pressures driving optimized amino-acid supplementation strategies

- Carbon-footprint labeling programs incentivizing amino-acid balanced diets

- Import tariffs and trade uncertainties disrupting supply chains

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lysine held 42.15% of the North America feed amino acids market share in 2025, driven by its status as the first limiting amino acid in corn-soy formulas for poultry and swine. Methionine is progressing at a 6.05% CAGR between 2026 to 2031, buoyed by wider use in broilers and novel rumen-protected forms for dairy cows. Evonik's backward integration in Mobile, Alabama, trims methionine costs by 15%, advancing supply reliability. Threonine enjoys steady gains in layer diets, whereas tryptophan sees niche uptake for stress mitigation in transport settings.

Rumen-protected delivery breakthroughs underpin methionine's momentum, enabling dairy operators to elevate milk protein without increasing crude protein. Specialty amino acids such as valine, isoleucine, and histidine account for less than 10% of the North America feed amino acids market size but offer future upside as precision nutrition matures. Suppliers cultivate intellectual property around encapsulation and timed release, commanding premiums over commodity grades.

List of Companies Covered in this Report:

- Evonik Industries AG

- Archer-Daniels-Midland Co.

- IFF (Danisco Animal Nutrition)

- SHV (Nutreco NV)

- Land O' Lakes

- Adisseo

- Ajinomoto Co., Inc.

- CJ CheilJedang (CJ BIO)

- BASF SE (Animal Nutrition)

- Novus International, Inc.

- Cargill, Inc.

- Kemin Industries

- Alltech, Inc.

- Balchem Corporation

- Phibro Animal Health Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Growing demand for high-efficiency protein conversion in poultry and swine production

- 4.5.2 Expansion of industrial-scale poultry farming operations in Mexico and the United States

- 4.5.3 Feed-cost pressures driving optimized amino-acid supplementation strategies

- 4.5.4 Rise of precision-fermentation-derived feed-grade amino acids lowering price barriers

- 4.5.5 Carbon-footprint labeling programs incentivizing amino-acid balanced diets

- 4.5.6 Increasing adoption of amino-acid enriched insect meal in aquaculture diets

- 4.6 Market Restraints

- 4.6.1 Volatility in corn and soybean prices affecting amino-acid production economics

- 4.6.2 Import tariffs and trade uncertainties disrupting supply chains

- 4.6.3 Excess Chinese lysine capacity triggering dumping concerns in North America

- 4.6.4 Consumer pushback against chemically synthesized additives in organic meat supply chains

5 MARKET SEGMENTATION (VALUE AND VOLUME)

- 5.1 Sub Additive

- 5.1.1 Lysine

- 5.1.2 Methionine

- 5.1.3 Threonine

- 5.1.4 Tryptophan

- 5.1.5 Other Amino Acids

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 Other Aquaculture Species

- 5.2.1.1 By Sub Animal

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.2.1 By Sub Animal

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 Geography

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Evonik Industries AG

- 6.4.2 Archer-Daniels-Midland Co.

- 6.4.3 IFF (Danisco Animal Nutrition)

- 6.4.4 SHV (Nutreco NV)

- 6.4.5 Land O' Lakes

- 6.4.6 Adisseo

- 6.4.7 Ajinomoto Co., Inc.

- 6.4.8 CJ CheilJedang (CJ BIO)

- 6.4.9 BASF SE (Animal Nutrition)

- 6.4.10 Novus International, Inc.

- 6.4.11 Cargill, Inc.

- 6.4.12 Kemin Industries

- 6.4.13 Alltech, Inc.

- 6.4.14 Balchem Corporation

- 6.4.15 Phibro Animal Health Corporation