|

시장보고서

상품코드

2066417

해양 시추 리그 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Offshore Drilling Rigs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

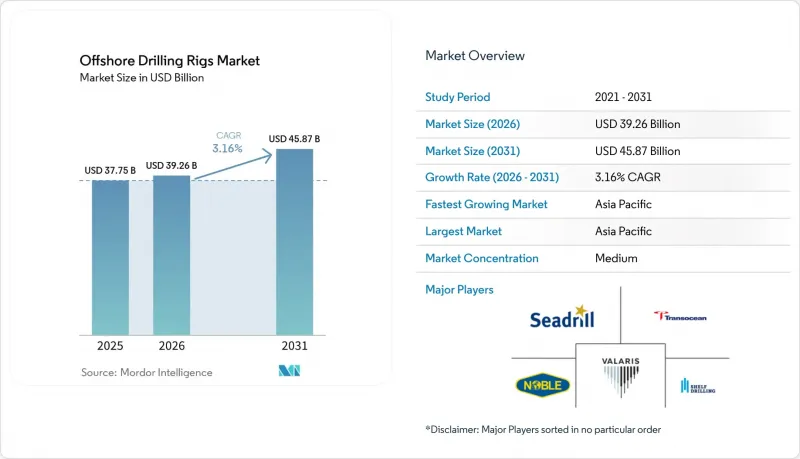

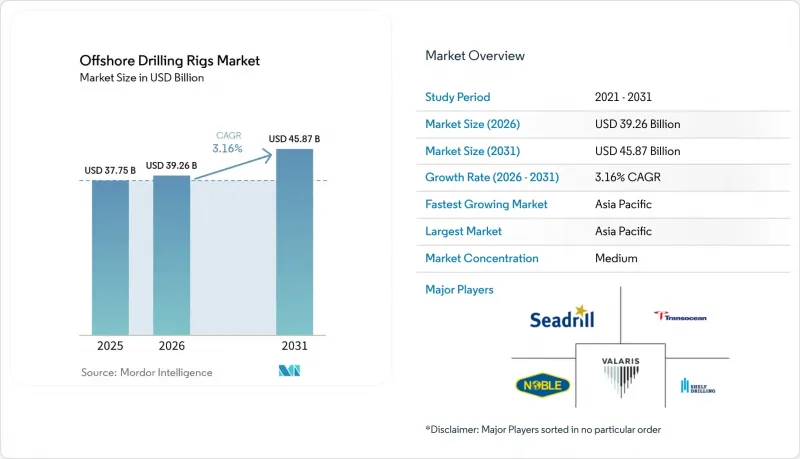

Mordor Intelligence에 의하면, 해양 시추 리그 시장 규모는 2025년 377억 5,000만 달러로 평가되었습니다. 2026년에는 392억 6,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 3.16%로 성장을 지속하여, 2031년에는 458억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 리그 유형(잭업식, 반잠수식, 드릴십, 기타 리그 유형), 수심(얕은 바다, 심해, 초심해) 및 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러)으로 표시되어 있습니다.

세계의 해양 시추 리그 시장 동향 및 분석

세계 에너지 수요 증가

석유 및 가스는 2030년까지 세계 에너지 구성에서 총 52%의 점유율을 유지할 것으로 예상되며, 이에 따라 해양 시추 사업에 지속적인 베이스로드 수요가 창출될 것입니다. ADNOC Drilling사는 UAE가 일일 500만 배럴의 생산 능력을 달성할 수 있도록 지원하기 위해 2028년까지 시추 장비 보유 대수를 125대로 확대할 계획이며, 이는 국영 석유 회사가 수요를 뒷받침하고 있는 실태를 여실히 보여주고 있습니다. 인도의 ONGC는 노후화된 유정의 생산량을 유지하기 위해 크리슈나-고다바리 분지에서 잭업식 시추 장비의 용선 계약을 연장하고 있으며, 이는 에너지 수요가 높은 신흥 경제국에서 얕은 바다 시추의 중요성을 입증하고 있습니다. 페트로브라스는 프레솔트층에서의 운영을 위해 12척의 시추선을 확보했습니다. 이는 국영 기업이 가격 주기의 변동과 관계없이 시추 활동을 유지할 수 있음을 시사합니다. OECD 국가들의 효율화와 비OECD 국가들의 확대라는 이러한 양극화로 인해, 잭업식 시추선이 아시아 지역의 증산분을 담당하고, 한편 고급 부유식 시추선이 개척 단계에 있는 심해 유전에서의 원유 생산을 담당하는 이중 구조 수요 패턴이 형성되고 있습니다.

미개발 해양 매장량의 탐사

나미비아의 오렌지 분지에는 추정 100억 배럴의 회수 가능 자원이 매장되어 있으며, 토탈에너지스와 쉘은 2024년부터 2025년에 걸쳐 총 4척의 시추선을 투입했습니다. 가이아나의 스타브로크 유전에서 발견 매장량이 110억 배럴을 초과함에 따라, 일일 64만 배럴 이상의 생산 확대를 유지하기 위해서는 6척의 시추선による 지속적인 운영이 필요합니다. 이러한 성공 사례로 인해 위험에 대한 인식이 낮아지고 있으며, 성공 확률이 높아지면 1억 달러를 넘는 시추 비용도 정당화되고 있습니다. 앙골라의 60억 달러 규모 카미뇨(Kaminho) 프로젝트에서는 4년에 걸쳐 드릴십 2척이 투입될 예정이며, 배럴당 35달러 전후의 손익분기점 상황에서도 프론티어 심해 개발에 자금을 투입하려는 의지가 뚜렷이 드러나고 있습니다. 따라서 수심 1만 피트, 2만 psi의 HPHT(고압·고온) 등급을 충족할 수 있는 최첨단 시추선이 해양 시추 리그 시장의 성장 동력이 되고 있습니다.

환경 문제와 ESG 규제 강화

2025년 이후, EU의 배출권 거래 제도(ETS)가 해양 선박에도 적용됨에 따라, 배출 감축 기술을 갖추지 않은 시추선에는 연간 최대 1,000만 달러의 탄소 비용이 추가로 부과됩니다. 또한, 미국 환경보호청(EPA)도 시추 유체의 배출 기준을 강화하여 설비 투자를 15-20% 늘렸습니다. 이러한 규제로 인해 트랜스오션사는 업그레이드가 경제적으로 타당하지 않게 된 구형 반잠수식 시추선 3기를 콜드 스택(가동 중단) 상태로 전환할 수밖에 없었습니다. 조달 담당자들이 조달 과정에 ESG 지표를 반영함에 따라, 하이브리드 동력 장치와 실시간 배출량 모니터링 시스템을 갖춘 계약업체들은 입찰에서 우위를 점하고 있습니다. 노르웨이 석유안전청은 메탄 연속 모니터링 요건을 도입하여 북해의 시추 플랫폼에 대한 추가적인 규정 준수 요건을 부과했습니다.

부문별 분석

2025년, 잭업식 시추선은 페르시아만, 동남아시아, 멕시코만에서의 높은 가동률에 힘입어 해상 시추선 시장 점유율의 43.9%를 차지했습니다. 반면, 드릴십은 2031년까지 연평균 성장률(CAGR) 7.2%를 나타낼 것으로 예측되며, 이 부문의 해양 시추 리그 시장 규모는 연말까지 180억 달러에 달할 것으로 전망됩니다. 2만 psi의 HPHT(고압·고온) 시추공에 대응할 수 있는 장비를 갖춘 고급 시추 장비는 하루에 50만 달러의 수익을 올리고 있습니다. 예를 들어, 트랜스오션의 ‘딥워터 아틀라스’는 2025년에 에퀴놀사와 3년간의 계약을 체결했습니다. 2025년에는 반잠수식 시추선이 중수심에서의 작업을 주도하며 가동률이 78%에 달했습니다. 그중 상당수는 서아프리카 및 북해 외해에서의 평가 작업에 투입되었습니다. 구형 시추 설비의 퇴역이 계속되는 가운데, 수요는 고사양 자산에 집중되고 있으며, 이로 인해 자사 선단을 현대화하는 계약업체들의 가격 결정력이 더욱 강화되고 있습니다.

해상 시추선 시장 동향은 선단의 표준화와 디지털화로의 전환을 여실히 보여주고 있습니다. 삼성중공업은 2024년부터 2025년에 걸쳐 신조 드릴십 2척을 인도했으며, 이 선박들은 즉시 페트로브라스의 프리솔트층 개발에 투입되었습니다. 이는 프리미엄 부유식 시추 장비 부문에서 여력이 극히 적음을 보여줍니다. 한편, 동남아시아 지역의 잭업식 시추 장비 공급 과잉으로 인해 볼 드릴링(Bol Drilling)사는 2025년에 4기를 중동으로 재배치할 수밖에 없게 되었으며, 태국에서 적용되는 요금보다 25% 높은 요금을 요구하며 이동했습니다. 2025년 말 기준 전 세계 잭업식 시추 설비의 가동률은 82%였던 반면, 부유식 시추 설비는 91%로, 얕은 해역의 설비가 수요 증가를 흡수하는 속도가 깊은 해역에 비해 더 느린 것으로 확인되었습니다.

지역별 분석

아시아태평양은 태국, 베트남, 인도의 성장에 힘입어 2025년에 매출의 37.6%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 4.1%를 기록하며 여전히 가장 빠르게 성장하는 지역으로 자리매김하고 있습니다. PTTEP는 2025년, 태국만에서의 가동 기간을 연장하기 위해 3건의 잭업식 시추선 계약을 체결했습니다. 한편, 페트로베트남은 프론티어 탐사를 지연시키는 영해상의 제약을 보완하기 위해 박호와 쿠롱에서 5기의 시추선을 계속 가동했습니다. 인도의 ONGC는 수입 의존도를 줄이기 위해 여러 대의 잭업식 시추선의 계약을 연장함으로써, 2030년까지 일일 100만 배럴의 국내 생산 목표를 제시한 정부의 방침을 뒷받침했습니다. 중국의 CNOOC는 광둥-홍콩-마카오 대만구의 산업 수요를 충족시키기 위해 남중국해 가스전에 6기의 부유식 시추 설비를 배치했습니다. 한편, 우드사이드사는 2026년에 최종 투자 결정(FID)이 내려질 가능성이 있는 스카버러 가스전의 타이백 프로젝트를 추진하고 있습니다.

북미에서는 지역에 따라 서로 다른 추세가 나타났습니다. 미국 멕시코만에서는 해저 타이백 프로젝트에 중점을 두면서 시추선 수요는 정체세를 보였으나, 멕시코의 페멕스(Pemex)는 일일 180만 배럴의 생산량을 안정적으로 유지하기 위해 2024년부터 2025년에 걸쳐 3건의 잭업식 시추선 계약을 확보했습니다. 남미에서는 브라질과 가이아나가 계속해서 주도적인 역할을 수행했습니다. 페트로브라스는 일일 생산량을 300만 배럴 이상으로 유지하기 위해 12척의 시추선을 운용했으며, 한편 가이아나의 스타브로크 블록에서는 개발정 및 탐사정에서 6척의 부유식 시추 설비가 가동되었습니다. 트리니다드의 얕은 해역 가스 유정은 애틀랜틱 LNG의 처리량을 뒷받침하며, 잭업식 시추 설비의 가동률을 적정 수준으로 유지하고 있습니다.

유럽에서의 활동은 노르웨이가 주도하고 있으며, 에퀴노르(Equinor)는 요한 스베르드루프 유전에서 디지털 트윈을 도입하여 비생산 시간을 15% 줄였습니다. 영국 대륙붕에서는 해체 작업이 우선적으로 진행되어, 4기의 잭업 리그가 유정 폐쇄 작업에 투입되었습니다. 중동에서는 얕은 해역에서의 활동이 계속해서 활발했습니다. ADNOC 드릴링사의 125기 시추 장비를 활용한 프로그램이 일일 500만 배럴의 생산 목표를 뒷받침했으며, 카타르의 노스 필드 이스트 가스전 확장 프로젝트에서는 2025년에 6기의 잭업 리그가 필요할 것으로 예상되며, 사우디 아람코의 리그 수는 OPEC+의 생산 상한선에 맞추어 변동했습니다. 아프리카의 초심해 개척지에서는 나미비아와 앙골라를 필두로 활동이 급증했습니다. 토탈에너지의 카민호 개발 및 나이지리아의 봉가 사우스웨스트 평가 사업은 아프리카 대륙의 장기적인 시추 장비 수요 전망을 더욱 확고히 했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the offshore drilling rigs market size is expected to grow from USD 37.75 billion in 2025 to USD 39.26 billion in 2026 and is forecast to reach USD 45.87 billion by 2031 at 3.16% CAGR over 2026-2031.

This report is Segmented by Rig Type (Jack-Ups, Semi-Submersibles, Drillships, and Other Rig Types), Water Depth (Shallow Water, Deepwater, and Ultra-Deepwater), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Offshore Drilling Rigs Market Trends and Insights

Increasing Global Energy Demand

Oil and gas are expected to retain a combined 52% share of the global energy mix through 2030, creating a durable baseload for offshore drilling campaigns. ADNOC Drilling plans to grow its fleet to 125 rigs by 2028 to help the UAE hit 5 million bpd production capacity, illustrating how national oil companies backstop demand. India's ONGC is extending jack-up charters in the Krishna-Godavari basin to preserve output from aging wells, reinforcing the shallow-water importance in energy-hungry emerging economies. Petrobras secured 12 drillships for pre-salt operations, signaling that state-backed operators can sustain drilling through price cycles. This bifurcation, OECD efficiency versus non-OECD expansion, results in a two-tier demand pattern where jack-ups cater to incremental volumes in Asia while premium floaters chase frontier deepwater barrels.

Exploration of Untapped Offshore Reserves

Namibia's Orange Basin holds an estimated 10 billion barrels of recoverable resources, with TotalEnergies and Shell collectively deploying four drillships during 2024-2025. Guyana's Stabroek block surpassed 11 billion barrels discovered, requiring a continuous fleet of six drillships to sustain its ramp-up past 640,000 bpd. These successes are lowering perceived risk and supporting well costs above USD 100 million when success probabilities rise. Angola's USD 6 billion Kaminho project will use two drillships over four years, highlighting the willingness to fund frontier deepwater when breakevens sit near USD 35 per barrel. Modern drillships capable of 10,000-foot water depths and 20,000-psi HPHT ratings thus form the growth engine of the offshore drilling rigs market.

Environmental Concerns & Stricter ESG Regulation

From 2025, the EU's Emissions Trading System extends to offshore vessels, adding up to USD 10 million per year in carbon costs for rigs lacking abatement technology. The U.S. EPA also tightened drilling-fluid discharge norms, increasing equipment spend by 15-20%. These mandates prompted Transocean to cold-stack three legacy semi-subs that were uneconomical to upgrade. Contractors with hybrid power packs and real-time emissions monitoring now enjoy bidding advantages as operators integrate ESG metrics into sourcing. Norway's Petroleum Safety Authority has introduced continuous methane monitoring requirements, adding further compliance layers for North Sea rigs.

Other drivers and restraints analyzed in the detailed report include:

- Rising Deep- & Ultra-Deepwater Discoveries in South America & Africa

- Decommissioning Backlog Driving Rig-Repurposing Demand

- Crude-Oil Price Volatility Impacting CAPEX Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Jack-ups controlled 43.9% of the offshore drilling rigs market share in 2025, supported by high utilization in the Persian Gulf, Southeast Asia, and the Gulf of Mexico. In contrast, drillships are forecast to post a 7.2% CAGR through 2031, pushing the offshore drilling rigs market size for this segment to an expected USD 18 billion by the end-year window. Premium units fetch USD 500,000 per day when equipped for 20,000-psi HPHT wells, such as Transocean's Deepwater Atlas, which began a three-year Equinor contract in 2025. Semi-submersibles filled mid-water campaigns with 78% utilization in 2025, largely for appraisal work in West Africa and the Far North Sea. The continuing retirement of vintage rigs concentrates demand on high-specification assets, promoting stronger pricing power for contractors that modernize their fleets.

The offshore drilling rigs market trajectory underscores a pivot toward fleet standardization and digital enablement. Samsung Heavy Industries delivered two newbuild drillships in 2024-2025 that immediately entered Petrobras' pre-salt pool, evidencing thin slack in the premium floater segment. Conversely, jack-up oversupply in Southeast Asia pressured Borr Drilling to redeploy four units to the Middle East in 2025, chasing rates 25% higher than in Thailand. Global jack-up utilization was 82% in late 2025 versus 91% for floaters, confirming that shallow-water capacity is absorbing the demand upswing more slowly than deepwater.

Geography Analysis

Asia-Pacific retained 37.6% revenue in 2025 thanks to Thailand, Vietnam, and India, and remains the fastest-growing region at 4.1% CAGR through 2031. PTTEP awarded three jack-up contracts in 2025 to extend life in the Gulf of Thailand, while PetroVietnam kept five rigs active on Bach Ho and Cuu Long, compensating for territorial constraints that slow frontier exploration. India's ONGC extended multiple jack-ups to guard against import dependence, backing the government's 1 million bpd domestic output goal by 2030. China's CNOOC deployed six floaters to South China Sea gas fields to feed the Greater Bay Area's industrial demand, while Woodside advances the Scarborough gas tieback that could enter final investment decision in 2026.

North America showed divergent trends. The U.S. Gulf of Mexico focused on subsea tieback projects, flattening rig demand, whereas Mexico's Pemex secured three jack-up contracts in 2024-2025 to stabilize 1.8 million bpd output. South America remained dominated by Brazil and Guyana. Petrobras operated twelve drillships to hold production above 3 million bpd, while Guyana's Stabroek block kept six floaters busy across development and exploration wells. Trinidad's shallow-water gas wells support Atlantic LNG throughput, sustaining moderate jack-up utilization.

Europe's activity centered on Norway, where Equinor deployed digital twins on Johan Sverdrup to shave 15% off non-productive time. The UK Continental Shelf prioritized decommissioning, letting four jack-ups work well-abandonment campaigns. The Middle East maintained high shallow-water intensity: ADNOC Drilling's 125-rig program underpins a 5 million bpd target, Qatar's North Field East gas expansion required six jack-ups in 2025, and Saudi Aramco's rig count fluctuated with OPEC+ output ceilings. Africa's ultra-deepwater frontier surged, led by Namibia and Angola. TotalEnergies' Kaminho development and Nigeria's Bonga Southwest appraisal reinforced the continent's longer-term rig demand profile.

- Keppel Corp

- Seatrium Ltd (Sembcorp Marine)

- Samsung Heavy Industries

- Hyundai Heavy Industries

- DSME

- China Merchants HI

- CIMC Raffles

- Friede & Goldman

- Damen Shipyards

- Irving Shipbuilding

- Transocean

- Valaris

- Seadrill

- Noble

- Shelf Drilling

- Borr Drilling

- Diamond Offshore

- Stena Drilling

- COSL

- KCA Deutag

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing global energy demand

- 4.2.2 Exploration of untapped offshore reserves

- 4.2.3 Rising deep- & ultra-deepwater discoveries in South America & Africa

- 4.2.4 Decommissioning backlog driving rig-repurposing demand

- 4.2.5 Emergence of offshore carbon-storage & geothermal drilling

- 4.2.6 Accessibility of stranded gas via FLNG developments

- 4.3 Market Restraints

- 4.3.1 Environmental concerns & stricter ESG regulation

- 4.3.2 Crude-oil price volatility impacting CAPEX cycles

- 4.3.3 Subsea tiebacks reducing demand for new exploration wells

- 4.3.4 Supply-chain bottlenecks for ultra-deepwater equipment

- 4.4 Supply-Chain Analysis

- 4.5 Historical Day-Rate Trends (Floaters & Jack-ups)

- 4.6 Major Offshore Upstream Projects Pipeline

- 4.7 Regulatory Landscape (environmental & safety)

- 4.8 Technological Outlook (rig automation, remote ops, digital twins)

- 4.9 Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Competitive Rivalry Intensity

5 Market Size & Growth Forecasts

- 5.1 By Rig Type

- 5.1.1 Jack-ups

- 5.1.2 Semi-submersibles

- 5.1.3 Drillships

- 5.1.4 Other Rig Types (Tender, Barges, Modu conversions)

- 5.2 By Water Depth

- 5.2.1 Shallow Water (Below 400 ft)

- 5.2.2 Deepwater (400 to 5,000 ft)

- 5.2.3 Ultra-deepwater (Above 5,000 ft)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Norway

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Thailand

- 5.3.3.4 Vietnam

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Trinidad and Tobago

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 Angola

- 5.3.5.7 Namibia

- 5.3.5.8 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Keppel Corp

- 6.4.2 Seatrium Ltd (Sembcorp Marine)

- 6.4.3 Samsung Heavy Industries

- 6.4.4 Hyundai Heavy Industries

- 6.4.5 DSME

- 6.4.6 China Merchants HI

- 6.4.7 CIMC Raffles

- 6.4.8 Friede & Goldman

- 6.4.9 Damen Shipyards

- 6.4.10 Irving Shipbuilding

- 6.4.11 Transocean

- 6.4.12 Valaris

- 6.4.13 Seadrill

- 6.4.14 Noble

- 6.4.15 Shelf Drilling

- 6.4.16 Borr Drilling

- 6.4.17 Diamond Offshore

- 6.4.18 Stena Drilling

- 6.4.19 COSL

- 6.4.20 KCA Deutag

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment