|

시장보고서

상품코드

2066418

핵산 추출 및 정제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Nucleic Acid Isolation And Purification - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

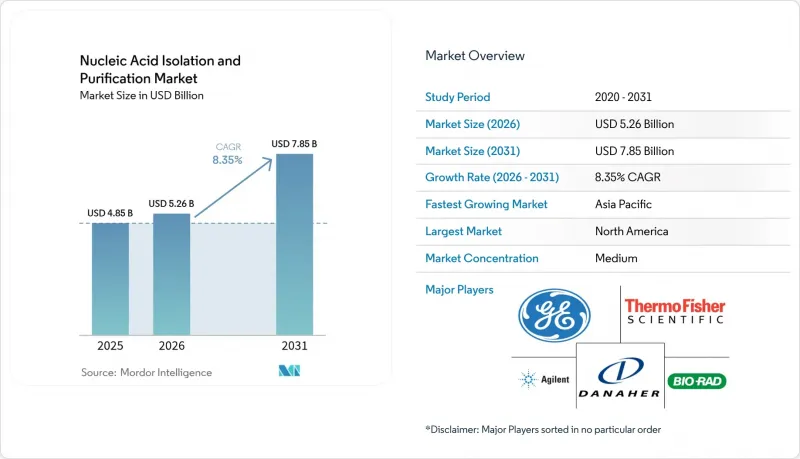

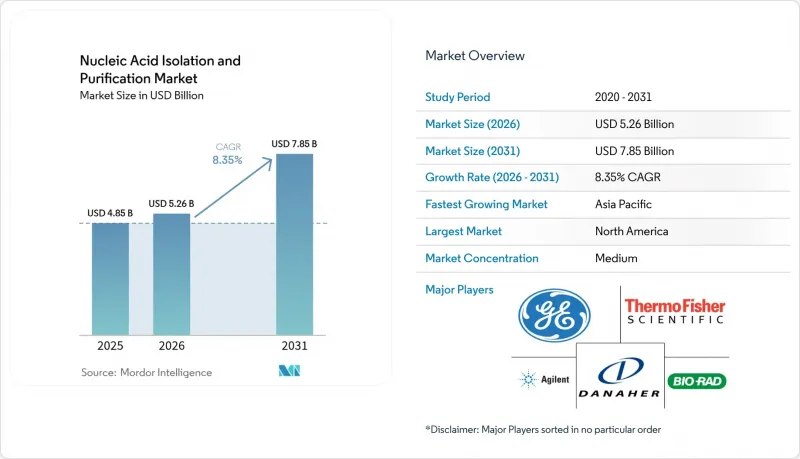

Mordor Intelligence에 의하면, 핵산 추출 및 정제 시장 규모는 2025년에 48억 5,000만 달러로 평가되었습니다. 2026년 52억 6,000만 달러에서 2031년까지 78억 5,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 8.35%를 나타낼 전망입니다.

본 보고서에서는 해당 업계를 기술별(컬럼식 정제 등), 제품별(키트 및 시약 등), 용도별(플라스미드 DNA 분리 등), 최종 사용자별(병원, 학술·연구 기관 등) 및 지역별로 분류하고 있습니다. 시장 규모 및 전망은 금액(달러)으로 표시되어 있습니다.

세계의 핵산 추출 및 정제 시장 동향 및 인사이트

종양학 분야에서 액체 생검용 cfDNA 추출 수요의 급증

종양학 검사가 조직 기반에서 혈액 기반으로 전환됨에 따라, 초고감도 cfDNA 분리 프로토콜에 대한 수요가 증가하고 있습니다. 현재 임상 종양 전문의들은 치료법 선택의 지침으로 극미량의 순환 종양 DNA에 의존하고 있으며, 배경 신호를 최소화하면서 피코그램 수준의 DNA를 회수할 수 있는 키트에 대한 수요가 급증하고 있습니다. cfDNA에 특화된 자성 비드 기술을 통해 90% 이상의 회수율을 달성함으로써, 폐암, 유방암, 대장암의 종양 부하를 실시간으로 모니터링할 수 있게 되었습니다. 기기 제조업체는 사전에 검증된 cfDNA 스크립트를 자동 워크스테이션에 탑재해 놓았으며, 이를 통해 병원 검사실에서는 96개의 혈장 검체를 2시간 이내에 처리할 수 있게 되었습니다. 보험 적용 범위가 확대됨에 따라 주요 종양 센터에서는 cfDNA 검사 건수가 조직 생검 건수를 넘어설 것으로 예측됩니다.

기술의 발전

로봇 기술, AI를 활용한 추출 매개변수 최적화, 그리고 대체 분리 기술이 일상적인 업무 흐름을 혁신하고 있습니다. 고성능 플랫폼을 통해 수작업 개입을 최대 80%까지 줄이고, 배치 간 재현성을 향상시키며, 오염 위험을 낮출 수 있게 되었습니다. 이소타코포레시스는 고체상 결합이 아닌 전기장을 이용함으로써, 단편화를 최소화하면서 고분자량 DNA를 회수하고, 롱 리드 시퀀싱에 필수적인 후성유전학적 특징을 유지합니다. 이와 상호 보완적인 획기적인 기술로, 3D 프린팅으로 제작된 일체형 분리 장치가 있으며, 자력을 사용하지 않고 1분 이내에 추출을 완료함으로써 핵심 시설의 처리 능력을 향상시키고 있습니다.

높은 초기 투자 비용 및 유지 관리 비용

자동 워크스테이션의 가격은 전용 플라스틱 및 연간 서비스 계약을 제외하면 5만 달러에서 20만 달러 사이입니다. 소규모 연구소에서는 업그레이드를 미루거나 외주 업체에 의존하는 경우가 많아, 그 결과 자금력이 있는 센터에 최첨단 기능이 집중되는 계층적인 생태계가 고착화되어 있습니다. 리스 모델은 현금 흐름의 제약을 완화해 주지만, 사용자를 소모품 구매 의무에 얽매이게 하여 수명 주기 비용을 상승시킵니다.

부문별 분석

컬럼 기반 정제는 2025년 매출의 47.55%를 차지했으며, 이는 임상 및 학술 연구소에서 확립된 프로토콜을 반영한 것입니다. 그럼에도 불구하고, 자성 비드 시스템은 연평균 성장률(CAGR) 9.42%를 나타낼 것으로 예측되며, 이는 핵산 추출 및 정제 시장 내에서 가장 높은 수치입니다. 표면 화학의 발전으로 선택적 결합과 신속한 용출이 가능해졌을 뿐만 아니라, INTEGRA사의 MAG 플랫폼과 같은 오픈 데크형 자동화 모듈이 96웰 처리를 효율화하고 있습니다. 암 및 유전성 질환 검사에서 고처리량 시퀀싱이 일상화됨에 따라, 자성 비드 플랫폼에 기인한 핵산 추출 및 정제 시장 규모가 급속히 확대될 것으로 예측됩니다. 시약 기반 기법이나 새롭게 등장한 전기영동법은 속도보다는 비용이나 시료의 무결성이 중시되는 분야에서 틈새 수요를 유지하고 있습니다.

자동화가 비즈로의 전환을 촉진하고 있습니다. 제약 기업의 품질 관리(QC) 실험실에서는 완전 밀폐형 로봇을 이용해 비드를 활용한 워크플로우의 유효성 검증이 이루어졌으며, 스핀 컬럼에 비해 사이클 타임을 20% 단축하는 데 성공했습니다. 한편, 이를 조기에 도입한 기업들로부터는 밀폐형 칩 구조 덕분에 교차 오염이 감소했다는 보고가 있습니다. 이러한 장점 덕분에, 새로 설립된 핵심 시설에서 자성 비드의 도입 대수가 컬럼과 어깨를 나란히 하고 있는 이유를 설명할 수 있습니다. 이러한 추세는 2031년까지 더욱 강화될 전망입니다.

2025년 매출액 중 키트 및 시약이 67.10%를 차지했으며, 이는 다양한 워크플로우에서 일상적으로 사용되는 소모품에 대한 수요를 반영하고 있습니다. 그럼에도 불구하고, 연구소들이 수동 작업대를 통합형 로봇 시스템으로 대체함에 따라 해당 장비의 판매는 연평균 성장률(CAGR) 10.05%를 나타낼 것으로 예측되며, 이는 핵산 추출 및 정제 시장 내에서 가장 높은 성장률입니다. 기기 분야의 핵산 추출 및 정제 시장 규모는 추적 가능성과 표준화가 최우선 과제로 꼽히는 기업 전반의 자동화 추진과 함께 확대되고 있습니다. Trilobio사의 전체 연구소를 대상으로 한 자동화 제품군은 시범 도입 과정에서 처리 능력이 33% 향상되었음을 입증함으로써, 대량 처리를 수행하는 사용자에게 있어 ROI(투자 대비 효과)를 뒷받침했습니다. 스핀 컬럼, 비드, 플레이트 등의 소모품은 안정적인 수요를 유지하고 있으며, 자본 지출의 주기적인 변동으로부터 공급업체를 보호하는 지속적인 수익원이 되고 있습니다.

확장성은 여전히 결정적인 구매 기준입니다. DNA 및 RNA의 병렬 추출이 가능한 멀티모듈형 로봇이 제약 업계의 파이프라인을 휩쓸고 있는 반면, 소형 카트리지식 시스템은 분산형 병원 검사실에 널리 보급되고 있습니다. 각 벤더사는 업스트림 공정의 품질 관리(QC) 지표를 바탕으로 인큐베이션 시간을 자동으로 조정하는 AI 가이드형 실행 설정을 통해 차별화를 꾀하고 있으며, 이를 통해 수동 플랫폼에서 자동화 플랫폼으로의 전환을 더욱 공고히 하고 있습니다.

지역별 분석

북미는 성숙한 바이오의약품 부문과 자동 추출 플랫폼의 조기 도입에 힘입어 2025년에는 전 세계 매출의 38.70%를 차지했습니다. 유전체 분석에 대한 유리한 보험 환급 제도와 명확하게 정의된 규제 절차가 이 지역의 경쟁력을 더욱 강화하고 있습니다. 미국 내 핵산 추출 및 정제 시장 규모는 차세대 염기서열 분석을 치료 방침 결정에 통합하는 ‘myeloMATCH’와 같은 정밀 종양학 임상시험의 혜택을 받았습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR) 9.12%를 나타낼 것으로 전망됩니다. 의료비 증가, 국내 바이오 생산 능력 확충, 그리고 각국의 유전체 정책이 중국, 인도, 한국에서의 도입을 뒷받침하고 있습니다. ‘Genome India’와 같은 고처리량 프로젝트에서는 일관성 있고 확장 가능한 추출 워크플로가 요구되고 있으며, 이는 키트와 자동화 장비 모두에 대한 수요를 촉진하고 있습니다. 암 및 감염병 발생률 증가는 분자진단의 도입을 더욱 가속화하여 시장의 지속적인 확대를 확실히 하고 있습니다.

유럽은 확립된 연구 네트워크와 고품질 추출 솔루션을 뒷받침하는 엄격한 품질 기준 덕분에 여전히 큰 시장 점유율을 유지하고 있습니다. IVDR(체외진단 의료기기 규정)의 시행에 따라 공급업체 선정 기준이 재편되었으며, 검사 기관은 종합적인 성능 데이터 시트를 제시할 수 있는 공급업체를 우선적으로 선정하고 있습니다. 중동이나 남미와 같은 신흥 지역에서는 시장 규모는 작지만, 공중보건 시스템이 분자진단 인프라의 현대화를 추진함에 따라 도입이 가속화되고 있으며, 기술 보급을 위한 새로운 길이 열리고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the nucleic acid isolation and purification market size was valued at USD 4.85 billion in 2025 and estimated to grow from USD 5.26 billion in 2026 to reach USD 7.85 billion by 2031, at a CAGR of 8.35% during the forecast period (2026-2031).

This report Segments the Industry Into by Technology (Column-Based Purification, and More), by Product (Kits and Reagents, and More), by Application (Plasmid DNA Isolation, and More), by End User (Hospitals, Academic and Research Institutes, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Nucleic Acid Isolation And Purification Market Trends and Insights

Surge in Liquid-Biopsy cfDNA Extraction Demand in Oncology

The transition from tissue to blood-based oncology testing has amplified requirements for ultra-sensitive cfDNA isolation protocols. Clinical oncologists now rely on circulating tumor DNA at fractional abundance levels to guide therapy selection, sparking a spike in demand for kits that recover picogram-level DNA with minimal background. Magnetic bead chemistries tailored for cfDNA have achieved >90% recovery, enabling real-time tumor burden monitoring for lung, breast, and colorectal cancers . Instrument makers are embedding pre-validated cfDNA scripts into automated workstations, allowing hospital labs to process 96 plasma samples in under two hours. As payer reimbursement expands, cfDNA volumes are expected to outpace tissue biopsies in leading oncology centers.

Growing Technological Advancements

Robotics, AI-curated extraction parameters, and alternative separation chemistries are reshaping day-to-day workflows. High-end platforms now cut manual intervention by up to 80%, improve batch-to-batch consistency, and curtail contamination risk. Isotachophoresis leverages electric fields rather than solid-phase binding, delivering higher-molecular-weight DNA with less fragmentation and preserving epigenetic signatures essential for long-read sequencing . Complementary breakthroughs include 3D-printed integrated separators that complete magnetic-free extractions in under one minute, accelerating throughput in core facilities.

High Capital and Maintenance Costs

Automated workstations list between USD 50,000 and USD 200,000, excluding proprietary plastics and annual service contracts. Smaller laboratories often delay upgrades or depend on fee-for-service partners, reinforcing a tiered ecosystem where cutting-edge capabilities concentrate in well-funded centers. Leasing models ease cash flow constraints yet lock users into consumable commitments, raising life-cycle costs.

Other drivers and restraints analyzed in the detailed report include:

- Wide Range Applications of Nucleic Acid Testing in Diagnostics

- Genomics Initiatives Driving gDNA Preparation

- Stringent Regulatory Norms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Column-based purification generated 47.55% of 2025 revenue, reflecting entrenched protocols in clinical and academic labs. Nonetheless, magnetic bead systems are projected to register a 9.42% CAGR, the highest within the nucleic acid isolation and purification market. Enhanced surface chemistries now enable selective binding and rapid elution, while open-deck automation modules like INTEGRA's MAG platform streamline 96-well processing. The nucleic acid isolation and purification market size attributable to magnetic bead platforms is forecast to expand steeply as high-throughput sequencing becomes routine in oncology and hereditary disease testing. Reagent-based and emerging electrophoretic methods retain niche traction where cost or sample integrity considerations outweigh speed.

Automation drives the migration toward beads. Pharmaceutical QC laboratories have validated bead workflows on fully enclosed robots, achieving 20% shorter cycle times relative to spin columns. Meanwhile, early adopters report lower cross-contamination thanks to sealed tip architectures. These advantages explain why magnetic bead installations are approaching parity with columns in newly built core facilities, a trend likely to intensify through 2031.

Kits and reagents contributed 67.10% of 2025 turnover, reflecting daily consumable demand across diverse workflows. Still, instrument sales are poised for a 10.05% CAGR, the fastest within the nucleic acid isolation and purification market, as laboratories replace manual benches with integrated robotics. The nucleic acid isolation and purification market size for instruments is expanding alongside enterprise-wide automation initiatives where traceability and standardization are priorities. Trilobio's whole-lab automation suite demonstrated a 33% rise in throughput during pilot deployments, validating ROI for high-volume users. Consumables such as spin columns, beads, and plates maintain steady demand, providing recurring revenue that cushions vendors from capital expenditure cyclicality.

Scalability remains the decisive buying criterion. Multi-module robots capable of parallel DNA and RNA extractions dominate pharmaceutical pipelines, while compact cartridge-based systems penetrate decentralized hospital labs. Vendors are differentiating through AI-guided run set-ups that auto-adjust incubation times based on upstream QC metrics, further cementing the shift from manual to automated platforms.

Geography Analysis

North America commanded 38.70% of global revenue in 2025, anchored by mature biopharmaceutical sectors and early uptake of automated extraction platforms. Favorable reimbursement for genomic assays and well-defined regulatory pathways further reinforce regional dominance. The nucleic acid isolation and purification market size in the United States alone benefited from precision oncology trials such as myeloMATCH that integrate next-generation sequencing into treatment assignment.

Asia-Pacific is the fastest-growing territory, forecast at a 9.12% CAGR until 2031. Expanding healthcare expenditure, domestic biomanufacturing capacity, and national genomics drives fuel uptake in China, India, and South Korea. High-throughput projects such as Genome India require consistent, scalable extraction workflows, propelling demand for both kits and automated instruments. Rising incidence of cancer and infectious diseases further amplifies molecular diagnostic adoption, ensuring sustained market expansion.

Europe maintains a significant share owing to established research networks and stringent quality standards that favor premium extraction solutions. Implementation of IVDR is reshaping supplier selection criteria, prompting laboratories to prioritize vendors with comprehensive performance dossiers. Emerging regions in the Middle East and South America register smaller bases but exhibit accelerating adoption as public health systems modernize molecular diagnostics infrastructure, opening fresh avenues for technology diffusion.

- Agilent Technologies

- Bio-Rad Laboratories

- Thermo Fisher Scientific

- Danaher Corp. (Beckman Coulter & Cepheid)

- Roche

- QIAGEN

- Merck

- Promega Corp.

- GE Healthcare

- PerkinElmer

- Illumina

- Takara Bio

- New England Biolabs

- Zymo Research Corp.

- Oxford Nanopore Technologies

- Norgen Biotek

- LGC Biosearch Technologies

- Analytik Jena

- Invitek Molecular

- Biovision

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Liquid-Biopsy cfDNA Extraction Demand in Oncology

- 4.2.2 Growing Technological Advancements

- 4.2.3 Wide Range Applications of Nucleic Acid Testing in Diagnostics

- 4.2.4 Decentralization of Infectious-Disease RNA Testing in LMICs

- 4.2.5 Genomics Initiatives (e.g., Genome India) Driving gDNA Prep

- 4.2.6 Rise in R&D Funding in Biotechnology

- 4.3 Market Restraints

- 4.3.1 High Capital and Maintenance Costs

- 4.3.2 Supply-Chain Volatility for Critical Raw Materials

- 4.3.3 Stringent Regulatory Norms

- 4.3.4 Contamination Concerns in Magnetic-Bead Workflows

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value & Volume)

- 5.1 By Technology

- 5.1.1 Column-Based Purification

- 5.1.2 Magnetic Bead-Based Purification

- 5.1.3 Reagent-Based Purification

- 5.1.4 Others

- 5.2 By Product

- 5.2.1 Kits & Reagents

- 5.2.2 Instruments & Workstations

- 5.2.3 Consumables (Spin-Columns, Beads, Cartridges)

- 5.3 By Application

- 5.3.1 Genomic DNA Isolation & Purification

- 5.3.2 mRNA Isolation & Purification

- 5.3.3 microRNA Isolation & Purification

- 5.3.4 Cell-free DNA / Liquid Biopsy Isolation

- 5.3.5 Plasmid DNA Isolation

- 5.3.6 PCR Clean-up

- 5.4 By End-User

- 5.4.1 Academic & Research Institutes

- 5.4.2 Pharmaceutical / Biotechnology Companies

- 5.4.3 Hospitals & Diagnostic Labs

- 5.4.4 Contract Research & Manufacturing Organizations

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Agilent Technologies

- 6.3.2 Bio-Rad Laboratories Inc.

- 6.3.3 Thermo Fisher Scientific

- 6.3.4 Danaher Corp. (Beckman Coulter & Cepheid)

- 6.3.5 F. Hoffmann-La Roche Ltd.

- 6.3.6 Qiagen N.V.

- 6.3.7 Merck KGaA (Sigma-Aldrich)

- 6.3.8 Promega Corp.

- 6.3.9 GE HealthCare

- 6.3.10 PerkinElmer Inc.

- 6.3.11 Illumina Inc.

- 6.3.12 Takara Bio Inc.

- 6.3.13 New England Biolabs

- 6.3.14 Zymo Research Corp.

- 6.3.15 Oxford Nanopore Technologies

- 6.3.16 Norgen Biotek Corp.

- 6.3.17 LGC Biosearch Technologies

- 6.3.18 Analytik Jena AG

- 6.3.19 Invitek Molecular

- 6.3.20 BioVision Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment