|

시장보고서

상품코드

2066428

조영제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Contrast Media - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

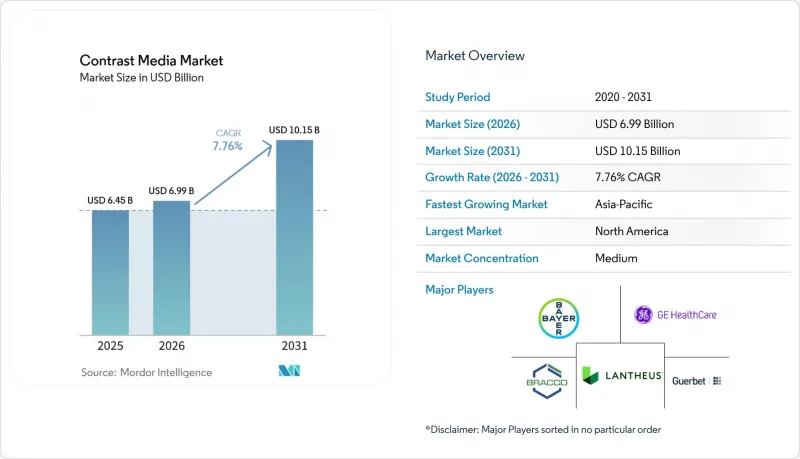

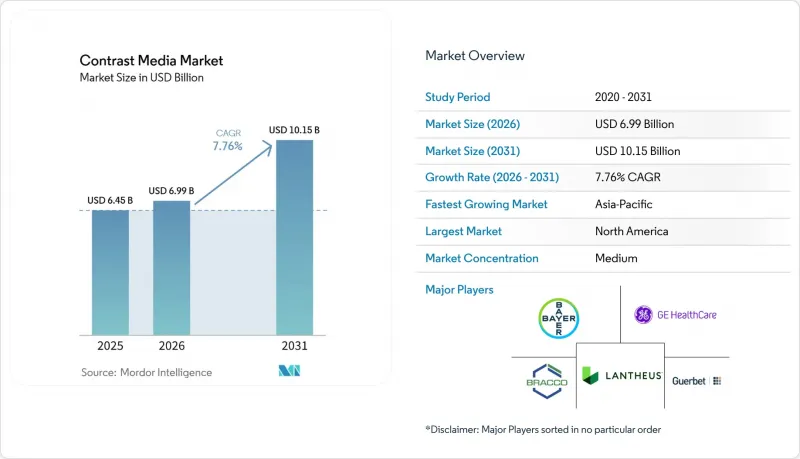

Mordor Intelligence에 의하면, 조영제 시장 규모는 2025년 64억 5,000만 달러로 평가되었습니다. 2026년에는 69억 9,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 7.76%로 성장을 지속하여, 2031년에는 101억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(요오드계, 바륨계, 가돌리늄계, 마이크로버블 및 신흥 조영제), 모달리티(X선/CT, MRI, 초음파), 투여 경로(혈관 내, 경구, 직장), 용도(심혈관, 종양학 등), 최종 사용자(병원, 영상진단센터 등), 지역(북미 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 조영제 시장 동향 및 인사이트

만성 질환 유병률 상승이 영상 진단 수요를 견인하고 있습니다.

2024년, 전 세계 암 신규 환자 수는 2,000만 명에 달했으며, 심혈관 질환으로 인한 사망자 수는 1,860만 명에 이르렀습니다. 지속적인 조영 영상 진단은 현재 종양학 및 순환기학 지침에 포함되어 있으며, 그 결과 환자 1인당 연간 여러 차례의 검사가 이루어지고 있습니다. 안정형 협심증 환자의 40%에서 관상동맥 CT 혈관조영술이 침습적인 카테터 검사를 대체하고 있으며, 검사 1회당 80-120밀리리터의 요오드계 조영제가 사용되고 있습니다. 일본과 독일에서는 각각 65세 이상 인구가 전체 인구의 5분의 1 이상을 차지하고 있으며, 이것이 검사 건수 증가를 부추기고 있습니다. 1회 검사당 사용량이 감소하더라도, 검사 건수 증가가 선량 저감 속도를 앞지르기 때문에 총 사용량(밀리리터)에 대한 수요는 증가하고 있습니다.

전 세계 영상 진단 검사 건수 증가

2024년, 전 세계 방사선과에서 52억 건의 영상 검사가 실시되어 전년(48억 건)보다 증가했습니다. 중국은 조영 초음파 검사의 보험 적용 범위를 확대하여, 3억 명의 농촌 주민이 검사를 받을 수 있게 되었습니다. 또한 인도는 ‘아유슈만 바라트’ 계획을 통해 2025년까지 1만 5,000곳의 영상진단센터를 신설했습니다. 미국의 메디케어 어드밴티지 플랜에서는 1,400만 명의 고위험 흡연자를 대상으로 연 1회 폐 CT 검진이 보험 적용 대상이며, 한편, 걸프협력회의(GCC) 회원국에서는 의료 관광 수요에 부응하기 위해 2024년에 조영제 수입량을 22% 늘렸습니다.

가돌리늄 침착 및 조영제 유발성 신증에 대한 우려

2024년에 발표된 부검 결과, 뇌 조직에서 가돌리늄 침착이 확인되었으며, 이에 따라 FDA는 첨부 문서의 수정을 요구했습니다. 긴급성이 없는 증례에서 가돌리늄계 조영제의 사용이 12% 감소했습니다. 요오드계 조영제는 고위험군 환자의 최대 5%에서 급성 신장 손상을 유발하기 때문에 신장 기능 검사가 의무화되어 있으며, 그 결과 검사의 8%가 지연되거나 중단되고 있습니다. 현재 유럽의 지침에서는 예방적 수분 보충이 권장되고 있으며, 이로 인해 사례당 80-150달러의 추가 비용이 발생할 뿐만 아니라, 경계선에 있는 검사 의뢰가 자제되고 있습니다. 미국의 의료과실 보험사들은 평균 이상의 유해 사건이 발생하고 있는 방사선과 의사들에게 보험료를 인상하고, 보험 적용 기준을 더욱 엄격하게 적용하고 있습니다.

부문별 분석

2025년, 요오드계 조영제는 조영제 시장의 71.52%를 차지하며, CT 혈관조영술, 요로조영술 및 소화관 검사 분야에서 그 우위를 입증했습니다. 비이온성 제제는 삼투압이 낮아 주사 시의 불편감이나 부작용을 줄일 수 있기 때문에 이 부문을 주도하고 있습니다. 바륨 화합물은 투시 하에 시행하는 식도 및 대장 검사에서 여전히 유용하지만, CT 대장조영술의 보급에 따라 그 비중은 줄어들고 있습니다. 가돌리늄 조영제는 뇌 및 척추의 영상 진단에 있어 필수적인 존재이지만, 침착에 대한 우려로 인해 임의적인 사용은 제한되고 있습니다. 가장 빠른 성장세를 보이고 있는 분야는 마이크로버블 및 신흥 조영제이며, 자원이 제한된 환경에서 초음파 검사가 선호됨에 따라 2031년까지 연평균 성장률(CAGR)은 10.23%를 나타낼 것으로 전망됩니다.

마이크로버블 조영제는 휴대용 초음파 장치를 사용하여 방사선 피폭 없이 심벽 운동 이상을 감지할 수 있는 현장 심초음파 검사 분야에서 점차 보급되고 있습니다. 란테우스(Lanteus)사의 ‘Definity’는 2024년에 부하 심초음파 검사의 정확도가 핵의학에 의한 관류 영상과 맞먹는 수준에 이르렀다는 점을 계기로, 더욱 널리 채택되기 시작했습니다. 이온성 요오드계 제품은 고소득 국가에서는 단계적으로 폐지되고 있지만, 가격에 민감한 지역에서는 여전히 수요의 12%를 차지하고 있습니다. 나노 입자 산화철 조영제는 현재 안전한 대안이 없는 1,500만 명의 신장 기능 장애 환자에게 적용됨으로써 MRI의 경제성을 획기적으로 바꿀 가능성이 있지만, 생산 규모 확대에는 여전히 과제가 남아 있습니다.

2025년, X선 및 CT는 조영제 시장의 58.35%를 차지했으며, 이는 전 세계적으로 7만 대에 달하는 CT 스캐너의 도입 대수에 의해 뒷받침되고 있습니다. MRI 시장 점유율은 약 30%를 차지하며, 초음파 검사는 연평균 성장률(CAGR) 9.14%로 성장하고 있습니다. 현재 휴대용 초음파 장비는 5,000달러 미만으로 판매되고 있어, 외래 진료나 지방의 진료소에서도 조영 초음파 검사를 실시할 수 있게 되었습니다. 간학 분야에서 초음파 검사의 부상은 간 병변의 특성 평가에 초음파 검사를 권장하는 새로운 지침과 병행하여 진행되고 있으며, 이를 통해 비용 절감과 신독성 위험 제거가 도모되고 있습니다.

순환기 분야에서는 마이크로버블을 이용한 부하 심초음파 검사가 관상동맥 질환의 진단 정확도 89%를 달성함으로써 그 혜택을 누리고 있습니다. MRI의 발전에는 안전성 문제가 따르지만, 연조직의 대비가 중요한 상황에서는 여전히 필수적입니다. 단층 영상 진단이 투영식 X선 촬영을 대체함에 따라, 투시 검사 건수는 감소하고 있습니다. 이 세 가지 모달리티를 모두 아우르는 제품 포트폴리오를 보유한 공급업체는 이용 패턴의 변화에 대한 내성이 높은 반면, 단일 모달리티를 취급하는 공급업체는 이익률 압박에 직면해 있습니다.

지역별 분석

북미는 2025년 매출의 38.66%를 차지했습니다. 이는 1인당 영상 진단 실시율이 가장 높다는 점과, 조영제를 ‘통과 비용’으로 분류하는 환급 정책에 힘입은 결과입니다. 미국만 해도 주민 1인당 연간 평균 1.2건의 조영 검사가 시행되고 있지만, 캐나다의 단일 지불자 제도에서는 처방약 목록의 제한으로 인해 사용이 억제되고 있습니다. 멕시코는 규모는 작지만, 민간 보험의 보급과 주요 도시에 새로운 병원이 개원함에 따라 시장이 점차 확대되고 있습니다.

아시아태평양은 대규모 정부 투자를 바탕으로 2031년까지 연평균 성장률(CAGR) 9.38%를 나타낼 것으로 전망됩니다. 중국은 2024년에 현립 병원에 CT 및 MRI를 도입하는 데 42억 달러를 배정했으며, 2027년까지 90%의 보급률을 목표로 하고 있습니다. 인도의 공적 의료 제도에서는 CT 혈관조영술의 보험 적용 범위가 확대되어, 그동안 침습적 검사로만 제한되었던 방대한 환자층이 이 검사를 이용할 수 있게 되었습니다. 일본의 성숙한 시장은 안정적이지만, 종합 건강검진을 선호하는 문화적 경향으로 인해 1인당 소비량은 여전히 높은 수준을 유지하고 있습니다. 호주와 한국에서는 광자 계수형 CT와 AI 주입 장치가 도입되어 효율이 향상되었으며, 도입 분야에서 계속해서 선두를 달리고 있습니다.

유럽에서는 상황에 따라 차이가 있습니다. 독일에서는 검사 건수가 많기 때문에 가격이 비싸다는 점에도 불구하고 마크로사이클릭 가드리늄을 권장하는 엄격한 안전 기준이 적용되고 있습니다. 프랑스에서는 요오드계 조영제 가격을 12% 인하하는 조치가 시행되면서 공급업체의 이익률이 압박받고 있습니다. 영국의 국민보건서비스(NHS)는 가돌리늄의 사용을 종양학과 신경학 분야로 제한하고 있으며, 그 결과 1인당 사용량은 독일보다 30% 낮습니다. 이탈리아와 스페인은 2024년에 140곳의 시설을 추가하여 외래 진료 수용 능력을 확대했습니다. 중동 및 아프리카에서는 걸프 연안 국가들이 의료 관광 거점으로의 구축을 추진하는 가운데 평균 이상의 성장세를 보이고 있는 반면, 남미에서는 암 검진 노력으로 인해 요오드계 조영제 사용량이 증가하고 있음에도 불구하고 비용 대비 효과 문제에 직면해 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the contrast media market size is expected to grow from USD 6.45 billion in 2025 to USD 6.99 billion in 2026 and is forecast to reach USD 10.15 billion by 2031 at 7.76% CAGR over 2026-2031.

This report is Segmented by Product Type (Iodinated, Barium-Based, Gadolinium-Based, Microbubble & Emerging Agents), Modality (X-ray/CT, MRI, Ultrasound), Route of Administration (Intravascular, Oral, Rectal), Application (Cardiovascular, Oncology, and More), End User (Hospitals, Diagnostic Imaging Centers and More), and Geography (North America and More). Market Forecasts are Provided in Terms of Value (USD).

Global Contrast Media Market Trends and Insights

Rising Prevalence of Chronic Diseases Drives Imaging Demand

Global cancer incidence reached 20 million new cases in 2024, while cardiovascular disease caused 18.6 million deaths.Serial contrast-enhanced imaging is now embedded in oncology and cardiology guidelines, resulting in multiple scans per patient each year. Coronary CT angiography replaces invasive catheterization in 40% of stable angina cases, consuming 80-120 milliliters of iodinated agent per study. Populations in Japan and Germany each have more than one-fifth of citizens over age 65, which boosts procedure volumes. Even when per-scan volumes decline, total milliliter demand rises because the number of examinations grows faster than dose reductions.

Growing Global Diagnostic Imaging Procedure Volumes

Radiology departments performed 5.2 billion imaging examinations worldwide in 2024, up from 4.8 billion one year earlier. China extended reimbursement for contrast-enhanced ultrasound, opening access for 300 million rural residents, and India added 15,000 imaging centers through Ayushman Bharat by 2025. Medicare Advantage plans in the United States cover annual lung CT screening for 14 million high-risk smokers, while Gulf Cooperation Council nations increased contrast imports by 22% in 2024 to meet medical-tourism demand.

Gadolinium Deposition and Contrast-Induced Nephropathy Concerns

Autopsy findings published in 2024 revealed gadolinium deposits in brain tissue, prompting the FDA to demand label changes. Utilization of gadolinium-based agents fell 12% for non-critical cases. Iodinated agents trigger acute kidney injury in up to 5% of high-risk patients, leading to mandatory renal screening that delays or cancels 8% of procedures. European guidelines now recommend prophylactic hydration, adding USD 80-150 per case and discouraging borderline orders. U.S. malpractice insurers raised premiums for radiologists with above-average adverse events, further tightening use.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in High-Resolution CT and MRI Scanners

- Regulatory Approvals of Safer Low- or Iso-Osmolar Agents

- High Capital Cost of Advanced Imaging Equipment and Agents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Iodinated agents represented 71.52% of the contrast media market in 2025, confirming their primacy across CT angiography, urography, and gastrointestinal studies. Non-ionic formulations command the segment because low osmolality limits injection discomfort and adverse reactions. Barium compounds remain useful in fluoroscopic esophageal and colon exams, yet their share erodes as CT colonography adoption rises. Gadolinium agents remain indispensable for brain and spine imaging, though deposition concerns suppress discretionary use. The fastest expansion belongs to microbubble and emerging agents, which post a 10.23% CAGR through 2031 as ultrasound gains favoritism in resource-constrained settings.

Microbubble agents thrive in point-of-care echocardiography, where portable ultrasound detects wall-motion abnormalities without radiation. Lantheus's Definity enjoyed broader adoption in 2024 when stress echocardiography started rivaling nuclear perfusion imaging in accuracy. Ionic iodinated products are being phased out in high-income nations but still cover 12% of demand in price-sensitive areas. Nanoparticle iron-oxide agents could reshape MRI economics by serving the 15 million renal-impaired patients currently left without safe options, although scale-up challenges persist.

X-ray and CT accounted for 58.35% of the contrast media market in 2025, grounded in an installed base of 70,000 CT scanners worldwide. MRI holds roughly 30% share, and ultrasound is growing at a 9.14% CAGR. Portable ultrasound devices now sell for less than USD 5,000, making contrast-enhanced ultrasound feasible in outpatient and rural clinics. Ultrasound's rise in hepatology parallels new guidelines that endorse it for liver lesion characterization, reducing costs and removing nephrotoxicity risk.

Cardiology benefits as stress echocardiography with microbubbles reaches 89% diagnostic accuracy for coronary disease. MRI growth faces safety questions but remains vital where soft-tissue contrast is critical. Fluoroscopic volumes shrink as cross-sectional imaging supersedes projection radiography. Vendors with portfolios spanning all three modalities are better insulated against shifts in use patterns, while single-modality suppliers experience margin pressure.

Geography Analysis

North America accounted for 38.66% of revenue in 2025, supported by the highest per-capita imaging rates and reimbursement policies that classify contrast as a pass-through expense. The United States alone conducts an average of 1.2 contrast-enhanced studies per resident each year, while Canada's single-payer system constrains usage through formulary limits. Mexico, though smaller, is rising as private insurance spreads and new hospitals open in major cities.

Asia-Pacific is set to post a 9.38% CAGR through 2031, reflecting large-scale government investments. China allocated USD 4.2 billion in 2024 to install CT and MRI in county hospitals, targeting 90% coverage by 2027. India's public scheme expanded reimbursements for CT angiography, unlocking a massive population base previously limited to invasive tests. Japan's mature market stays stable, but high per-capita consumption endures due to cultural preference for comprehensive checkups. Australia and South Korea embrace photon-counting CT and AI injectors, raising efficiency and keeping adoption at the forefront.

Europe shows mixed dynamics. Germany pairs high volumes with strict safety standards favoring macrocyclic gadolinium despite its price premium. France pushed through a 12% price cut for iodinated agents, squeezing supplier margins. The UK National Health Service restricts gadolinium to oncology and neurology, leading to 30% lower per-capita use than Germany. Italy and Spain broadened outpatient capacity by adding 140 centers in 2024. Middle East and Africa enjoy above-average growth as Gulf nations build medical-tourism hubs, while South America wrestles with affordability even as cancer-screening initiatives raise iodinated contrast volumes.

- Bayer

- Bracco Imaging S.p.A.

- Canon

- CMC Contrast AB

- Daiichi Sankyo

- Fujifilm Holdings Corp.

- GE Healthcare

- Guerbet Group

- Hengrui Medicine

- iMAX Diagnostic Imaging

- Koninklijke Philips

- Lantheus

- Nanopet Pharma GmbH

- Nemoto Kyorindo Co. Ltd.

- Siemens Healthineers

- Spago Nanomedical

- Taejoon Pharm

- Trivitron Healthcare

- Ulrich GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic Diseases (Cancer & CVD)

- 4.2.2 Growing Global Diagnostic Imaging Procedure Volumes

- 4.2.3 Technological Advances in High-Resolution CT & MRI Scanners

- 4.2.4 Regulatory Approvals of Safer Low-/Iso-Osmolar Agents

- 4.2.5 AI-Guided Injector Protocols Boosting Dose Optimization

- 4.2.6 Emergence of Renal-Safe Iron-Oxide Nanoparticle Agents

- 4.3 Market Restraints

- 4.3.1 Gadolinium Deposition & Contrast-Induced Nephropathy Concerns

- 4.3.2 High Capital Cost of Advanced Imaging Equipment & Agents

- 4.3.3 Iodine Feedstock Price Volatility & Supply Disruptions

- 4.3.4 Rise of Non-Contrast Imaging Modalities (Spectral CT, DL-Recon)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Iodinated Contrast Media

- 5.1.1.1 Ionic Iodinated

- 5.1.1.2 Non-ionic Iodinated

- 5.1.2 Barium-based Contrast Media

- 5.1.3 Gadolinium-based Contrast Media

- 5.1.4 Microbubble & Emerging Agents

- 5.1.1 Iodinated Contrast Media

- 5.2 By Modality

- 5.2.1 X-ray / CT

- 5.2.2 MRI

- 5.2.3 Ultrasound

- 5.3 By Route of Administration

- 5.3.1 Intravascular

- 5.3.2 Oral

- 5.3.3 Rectal

- 5.4 By Application / Indication

- 5.4.1 Cardiovascular Disorders

- 5.4.2 Oncology

- 5.4.3 Neurological Disorders

- 5.4.4 Gastrointestinal Disorders

- 5.4.5 Musculoskeletal Disorders

- 5.4.6 Nephrological Disorders

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Diagnostic Imaging Centers

- 5.5.3 Clinics & Ambulatory Surgery Centers

- 5.5.4 Research & Academic Institutes

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 France

- 5.6.2.3 United Kingdom

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Bayer AG

- 6.3.2 Bracco Imaging S.p.A.

- 6.3.3 Canon Medical Systems

- 6.3.4 CMC Contrast AB

- 6.3.5 Daiichi Sankyo Company

- 6.3.6 Fujifilm Holdings Corp.

- 6.3.7 GE Healthcare

- 6.3.8 Guerbet Group

- 6.3.9 Hengrui Medicine

- 6.3.10 iMAX Diagnostic Imaging

- 6.3.11 Koninklijke Philips N.V.

- 6.3.12 Lantheus Medical Imaging

- 6.3.13 Nanopet Pharma GmbH

- 6.3.14 Nemoto Kyorindo Co. Ltd.

- 6.3.15 Siemens Healthineers

- 6.3.16 Spago Nanomedical AB

- 6.3.17 Taejoon Pharm

- 6.3.18 Trivitron Healthcare

- 6.3.19 Ulrich GmbH & Co. KG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment