|

시장보고서

상품코드

2066432

인도의 안과용 의료기기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Ophthalmology Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

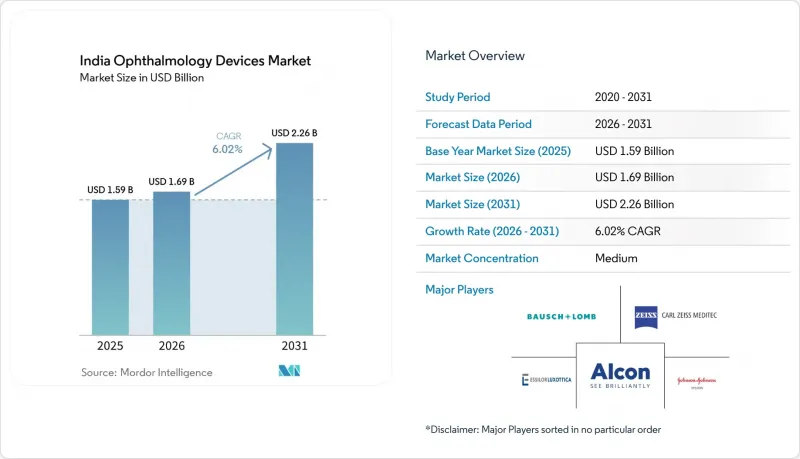

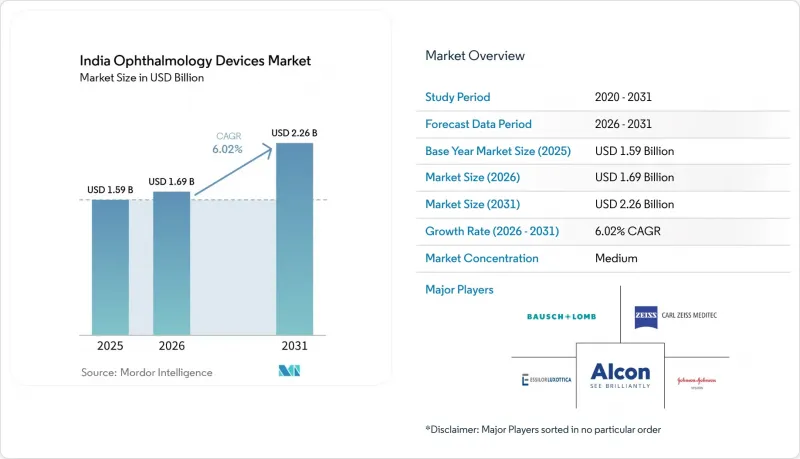

Mordor Intelligence에 의하면, 인도의 안과용 의료기기 시장 규모는 2025년에 15억 9,000만 달러로 평가되었습니다. 2026년 16억 9,000만 달러에서 2031년까지 22억 6,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 6.02%를 나타낼 전망입니다.

본 보고서는 기기 유형(진단·모니터링 기기, 수술용 기기, 시력 관리 기기), 질환별(백내장, 녹내장, 당뇨성 망막병증, 기타 질환), 최종 사용자(병원, 안과 전문 클리닉 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도의 안과용 의료기기 시장 동향 및 분석

시력 상실 예방·대책 국가 프로그램(NPCB)이 주 차원의 장비 조달을 촉진

NPCB(실명 예방·대책 국가 프로그램)는 현재 계획 주기에서 지역 차원의 안과 의료 프로젝트에 250억 6900만 루피를 배정하고 있으며, 현재 입찰에서는 2차 의료기관용 휴대용 슬릿 램프, 휴대용 안저 카메라, 그리고 모듈식 백내장 초음파 유화 흡입 장비가 우선적으로 선정되고 있습니다. 이동식 안과 진료 유닛을 도입한 주에서는 진료 의뢰까지 걸리는 시간이 단축된 것으로 보고되고 있으며, 이에 따라 민간 공급업체들은 제품 설계에 배터리 백업 기능과 견고한 외장을 반영하도록 권장받고 있습니다. 또한, 이 자금 지원에는 연수 할당량도 의무화되어 있기 때문에 현장에서 워크숍을 함께 제공하는 제조업체는 경쟁 우위를 점하고 있습니다. 결국, NPCB의 안정적인 자금 지원은 인도 안과 의료기기 시장 전체의 기초 수요를 뒷받침하고 있으며, 공급업체들이 현지 조립 라인 설치를 정당화할 수 있는 근거가 되는 가시성을 창출하고 있습니다.

아유슈만 바라트 헬스 인프라스트럭처 펀드(AB-HIF)가 안과 수술실 현대화를 추진

연방 예산에 따르면, 2025년에 AB-HIF(아유슈만 바라트 보건 인프라 기금)에 9만 크롤 이상의 루피가 배정되어, 1만 2,000개 공립 병원의 수술실 현대화를 위한 자금이 투입되었습니다. 안과 부문에서는 이러한 보조금을 활용하여 네트워크 연결형 현미경, 멸균 포드, 그리고 수술 후 감염률을 낮추는 환경 제어 시스템을 도입하고 있습니다. 상호 운용이 가능한 소프트웨어를 통해 새로운 하드웨어가 ‘아유슈만 바라트 디지털 미션’과 통합되며, 향후 조달 모델에 영향을 미칠 자산 활용 현황 분석 데이터가 제공됩니다. 이용률이 투명해짐에 따라 관리자들은 가동 시간 내역이 기록된 플랫폼을 선호하게 되었으며, 이에 따라 국내외 공급업체들은 인도 안과 의료기기 시장에서의 점유율을 지키기 위해 검증된 서비스 지표를 제공해야 하는 압박을 받고 있습니다.

제2·제3급 도시에서 훈련을 받은 유리체·망막 외과 전문의의 부족

인도는 14억 명 이상의 인구에 비해 등록된 망막 전문의가 약 1,400명에 불과하여, 많은 지역에서 충분한 외과적 의료 서비스를 받지 못하는 실정입니다. 자격을 갖춘 인력이 여전히 부족한 상황에서 병원들은 첨단 유리체 절제술용 콘솔에 대한 투자를 주저하고 있으며, 대도시권 이외 지역에서는 고성능 장비에 대한 수요가 부진한 상태입니다. 기기 제조업체들은 직관적인 그래픽 인터페이스와 원격 지원 모듈을 통해 이에 대응하고 있지만, 진정한 시장 확대를 위해서는 상주 인력 양성 체제의 개혁이 시급합니다. 그 전까지는 인력 부족으로 인해 인도의 안과용 의료기기 시장의 광범위한 지역에서 복잡한 시스템의 보급이 지연되고 있습니다.

부문별 분석

안경테부터 자동 렌즈 연마 시스템에 이르는 ‘시력 관리 기기’는 2025년 인도의 안과용 의료기기 시장에서 63.12%의 점유율을 차지했습니다. 체계화된 소매 체인 및 기업의 웰니스 프로그램이 확산됨에 따라, 내원 당일에 처방전을 처리할 수 있게 해주는 신속한 굴절 검사 도구와 렌즈 코팅 장치에 대한 수요가 증가하고 있습니다. 이와 동시에, 전자상거래 플랫폼이 온라인 구매자들을 최종 피팅을 위해 매장으로 유도하고 있으며, 이로 인해 객관적 굴절 검사 키오스크를 이용하는 방문객 수가 증가하고 있습니다. AI가 탑재된 렌즈 측정 앱은 진료 시간을 더욱 단축하고, 막대한 설비 투자 없이도 진료 효율을 높이고 있습니다.

진단·모니터링 기기 중 휴대용 OCT 스캐너, 스마트폰 연동형 안저 카메라, 가정용 안압 측정 키트 등은 합리적인 가격과 임상적 정확도를 모두 갖추고 있어 연평균 성장률(CAGR) 8.87%로 성장할 전망입니다. 2024년 CDSCO가 Remidio사의 ‘Medios DR AI’를 승인한 사례에서 볼 수 있듯이, 오프라인 AI에 대한 규제 당국의 승인이 확대됨에 따라 임상의들의 신뢰도가 높아지고 있습니다. 이미지 데이터를 분석하는 클라우드 플랫폼에 대한 투자가 유입되고 있으며, 초기 하드웨어 이익률을 희생하면서 구독 수익을 확보하고 있습니다. 수술용 기기 시장 규모는 여전히 작지만, 협력 병원에서 FLACS 및 미세 절개 유리체 절제 장치가 기존의 백내장 수술 시스템을 대체함에 따라 고부가가치 지출을 확보하고 있습니다. 공급업체는 가동률 95%를 보장하는 서비스 계약을 활용하고 있으며, 이를 통해 인도의 안과용 의료기기 시장 규모 산정 시 고객 충성도 및 지속적인 부품 판매가 반영되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the india ophthalmology devices market size was valued at USD 1.59 billion in 2025 and is estimated to grow from USD 1.69 billion in 2026 to reach USD 2.26 billion by 2031, at a CAGR of 6.02% during the forecast period (2026-2031).

This report is Segmented by Device Type (Diagnostic & Monitoring Devices, Surgical Devices, and Vision Care Devices), Disease Indication (Cataract, Glaucoma, Diabetic Retinopathy, Other Disease Indications), End-User (Hospitals, Specialty Ophthalmic Clinics, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Ophthalmology Devices Market Trends and Insights

National Programme for Prevention and Control of Blindness Catalysing State-level Device Procurements

The NPCB earmarked INR 2 506.9 crore for district eye-care projects in the current plan cycle, and tenders now prioritise portable slit lamps, handheld fundus cameras, and modular phaco machines for secondary facilities. States that deploy mobile ophthalmic units report shorter referral times, nudging private vendors to embed battery back-up and rugged casings in product designs. The funding stream also mandates training quotas, so manufacturers that bundle onsite workshops gain a competitive edge. Ultimately, steady NPCB financing shores up baseline demand across the India ophthalmology devices market, creating visibility that helps suppliers justify local assembly lines.

Ayushman Bharat Health Infrastructure Fund Driving Ophthalmic OT Upgrades

The Union budget allocates more than INR 90 000 crore for AB-HIF in 2025, releasing capital to modernise operating theatres in 12 000 public hospitals. Ophthalmology departments are utilising these grants to install networked microscopes, sterilisation pods, and environment-control systems that reduce postoperative infection rates. Interoperable software integrates the new hardware with the Ayushman Bharat Digital Mission, providing asset-usage analytics that influence future procurement models. When utilisation rates become transparent, administrators favour platforms with documented uptime histories, pushing global and domestic vendors to deliver verified service metrics to protect India ophthalmology devices market share.

Shortage of Trained Vitreo-Retinal Surgeons in Tier-II/III Cities

India has about 1 400 registered retinal specialists for more than 1.4 billion citizens, leaving many districts without adequate surgical coverage. Hospitals hesitate to invest in advanced vitrectomy consoles when qualified staff remain scarce, muting high-end device demand outside metros. Equipment makers respond with intuitive graphical interfaces and remote-support modules, yet real expansion awaits residency pipeline reforms. Until then, the talent deficit slows penetration of complex systems in large pockets of the India ophthalmology devices market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Uptake of Femtosecond Laser-Assisted Cataract Surgery in Tier-I Cities

- Surge in Screen-Induced Myopia Among 6-18 Year-olds Boosting Prescription Spectacles

- High GST on Ophthalmic Capital Equipment Raising Cap-ex Barriers for Small Clinics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vision Care Devices, ranging from frames to automated lens edging systems, held 63.12% India ophthalmology devices market share in 2025. The rise of organised retail chains and corporate wellness programmes drives demand for quick refraction tools and lens-coating units that allow same-visit dispensing. Parallel e-commerce platforms funnel online shoppers into stores for final fittings, boosting traffic for objective refraction kiosks. AI-enabled lens-measurement apps further compress consultation times, increasing throughput without large capital spend.

Diagnostic & Monitoring Devices are on track for a 8.87% CAGR because portable OCT scanners, smartphone-linked fundus cameras, and home tonometry kits blend affordability with clinical precision. Regulatory acceptance of offline AI, illustrated by the CDSCO nod to Remidio's Medios DR AI in 2024, enhances clinician confidence. Investment flows into cloud platforms that analyse imaging data, trading upfront hardware margins for subscription revenues. Surgical Devices remain smaller but capture high-value spend as FLACS and microincision vitrectomy units replace legacy phaco systems in referral hospitals. Suppliers leverage service contracts that guarantee 95% uptime, embedding loyalty and recurring part sales into the India ophthalmology devices market size calculus.

List of Companies Covered in this Report:

- Alcon

- Johnson & Johnson

- Bausch + Lomb Corp.

- EssilorLuxottica

- Carl Zeiss

- Hoya Corp.

- Topcon Corp.

- Nidek

- Appasamy Associates Private Limited

- Remidio Innovative Solutions Pvt Ltd.

- OmniLens Pvt Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 National Program for Prevention & Control of Blindness (NPCB) Catalysing State-level Device Procurements

- 4.2.2 Expansion of Ayushman Bharat Health Infrastructure Fund Driving Ophthalmic OT Up-grades

- 4.2.3 Rapid Uptake of Femto-second Laser Assisted Cataract Surgery (FLACS) in Tier-I Cities

- 4.2.4 Surge in Screen-induced Myopia Among 6-18 Year-olds Boosting Prescription Spectacles

- 4.2.5 Growing Penetration of CSR-funded Mobile Eye-Surgery Camps in Rural West India

- 4.2.6 Emergence of Indigenous Low-cost OCT & Fundus Cameras from Start-ups (e.g., Remidio)

- 4.3 Market Restraints

- 4.3.1 Shortage of Trained Vitreo-retinal Surgeons in Tier-II/III Cities

- 4.3.2 High GST (12%) on Ophthalmic Capital Equipment Raising Cap-ex Barriers for Small Clinics

- 4.3.3 Price-sensitive Consumer Base Limiting Adoption of Daily-Disposable Contact Lenses

- 4.3.4 Fragmented After-sales Service Network Outside Metro Clusters

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Diagnostic & Monitoring Devices

- 5.1.1.1 OCT Scanners

- 5.1.1.2 Fundus & Retinal Cameras

- 5.1.1.3 Autorefractors & Keratometers

- 5.1.1.4 Corneal Topography Systems

- 5.1.1.5 Ultrasound Imaging Systems

- 5.1.1.6 Perimeters & Tonometers

- 5.1.1.7 Other Diagnostic & Monitoring Devices

- 5.1.2 Surgical Devices

- 5.1.2.1 Cataract Surgical Devices

- 5.1.2.2 Vitreoretinal Surgical Devices

- 5.1.2.3 Refreactive Surgical Devices

- 5.1.2.4 Glaucoma Surgical Devices

- 5.1.2.5 Other Surgical Devices

- 5.1.3 Vision Care Devices

- 5.1.3.1 Spectacles Frames & Lenses

- 5.1.3.2 Contact Lenses

- 5.1.1 Diagnostic & Monitoring Devices

- 5.2 By Disease Indication

- 5.2.1 Cataract

- 5.2.2 Glaucoma

- 5.2.3 Diabetic Retinopathy

- 5.2.4 Other Disease Indications

- 5.3 By End-user

- 5.3.1 Hospitals

- 5.3.2 Specialty Ophthalmic Clinics

- 5.3.3 Ambulatory Surgery Centers (ASCs)

- 5.3.4 Other End-users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Alcon Inc.

- 6.3.2 Johnson & Johnson Vision Care Inc.

- 6.3.3 Bausch + Lomb Corp.

- 6.3.4 EssilorLuxottica SA

- 6.3.5 Carl Zeiss Meditec AG

- 6.3.6 Hoya Corp.

- 6.3.7 Topcon Corp.

- 6.3.8 Nidek Co. Ltd.

- 6.3.9 Appasamy Associates Private Limited

- 6.3.10 Remidio Innovative Solutions Pvt Ltd.

- 6.3.11 OmniLens Pvt Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment