|

시장보고서

상품코드

2066440

무인 해양 시스템 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Unmanned Sea Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

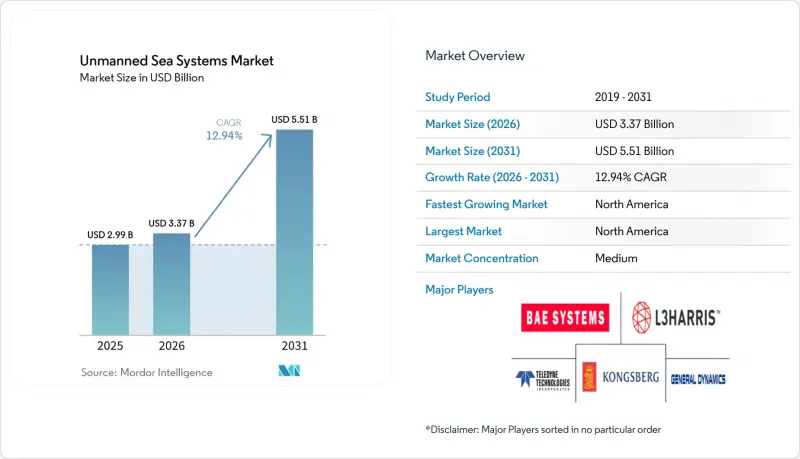

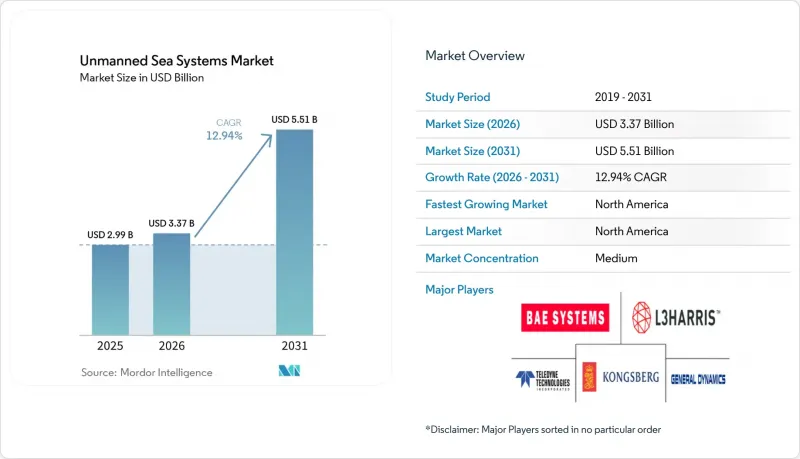

Mordor Intelligence에 의하면, 무인 해양 시스템 시장 규모는 2025년 29억 9,000만 달러로 평가되었고, 2026년에는 33억 7,000만 달러로 추정되고, 2026-2031년 CAGR 12.94%로 성장을 지속할 전망이며, 2031년까지 55억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 플랫폼 유형별(무인 수중정(UUV) 및 무인수상정(USV)), 기체 크기별(소형, 중형, 대형), 추진 방식별(전기, 하이브리드 등), 용도별(군용 및 상업용), 구성 요소 유형별(선체, 자율 항행 시스템, 센서 시스템 등), 그리고 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 무인 해양 시스템 시장 동향 및 분석

세계 각국 해군의 현대화 및 전력 개편 프로그램 확대

방위 조달 분야에서는 경쟁이 치열한 해양 환경에서 작전 효율을 높이는 전력 증강 수단으로서 자율형 플랫폼이 중시되고 있습니다. 새로 도입된 프로그램과 시제품은 기뢰전, ISR(정보·감시·정찰) 능력, 그리고 분산형 수중 효과기가 실험 단계에서 함대 계획 내 운용 통합 단계로 진전되고 있음을 보여줍니다. 록히드 마틴은 2026년 2월, ISR, 전자전 및 키네틱 임무를 지원하기 위한 재구성 가능한 페이로드 베이를 갖춘 모듈식 잠수함인 ‘램프리(Lamprey) 다목적 자율형 수중 차량’을 발표했습니다. 사브(Saab AB)는 전략적 방위 목표를 지원하는 유럽의 공식 프로그램을 통해 장거리 억지력과 해저 방어에 중점을 두고, 국가 계약에 기반한 대형 수중 차량 개발을 추진하고 있습니다. 나토(NATO)는 규격과 체계를 통해 상호운용성을 공식적으로 확립함으로써, 다국적 임무 부대 내 통합과 관련된 과제를 완화하고 있습니다. 이러한 조치로 인해 자율형 자산의 배치 일정이 앞당겨지고, 모듈식 페이로드의 업데이트가 표준화됨에 따라 동맹국 함대 전체의 작전 효율이 향상될 것입니다.

해상 풍력 발전소 점검 및 해저 조사 임무에 대한 수요 증가

해상 풍력 발전 사업자들이 사업을 확대해 나가는 가운데, 제한된 운영 및 유지보수(O&M) 예산과 엄격한 ESG 규정 준수 요건 간의 균형을 맞추는 데 있어 자율 점검은 매우 중요합니다. 2023년 4월, 후구로사는 자사의 ‘블루 에센스’ USV와 ‘블루 볼타’ eROV를 활용하여, 사상 최초로 완전 원격 조종을 통한 해상 풍력 발전소 점검을 실시했습니다. 유럽의 풍력 발전소 이해관계자들은 승무원 이동을 줄이고 점검 가능 기간을 확대하기 위해 자율 기술을 도입하고 있으며, 현장에 이를 도입함으로써 지속적인 모니터링에 있어 운영 비용과 가동 시간 측면에서 큰 이점이 드러나고 있습니다. 이러한 노력은 기상 조건으로 인한 가동 중단 시간을 줄이고, 인력을 해상에서 육상으로 전환하며, 점검 투자 회수 기간을 단축함으로써 ‘무인 운용’이라는 개념을 한층 더 강화할 것입니다. 이를 통해 여러 풍력 발전 해역에 걸친 견고한 O&M 계약을 바탕으로, 무인 플랫폼을 위한 확실한 수요 기반이 확립될 것입니다.

수출 관리 규제 및 ITAR 제한이 전 세계 판매에 제약을 가하고 있습니다.

라이선스 규제 및 방위 물자 분류로 인해 자율주행 차량 및 탑재 장비의 거래 주기가 장기화되고 있으며, 공급업체들은 생산의 현지화, 구성의 맞춤화, 또는 공통된 규정 준수 체계에 부합하는 지역 내 판매를 우선시해야 하는 상황에 직면해 있습니다. 모듈식 아키텍처를 제공하는 기업은 플랫폼 재인증을 회피하는 페이로드 업그레이드를 통해 기능을 향상시킬 수 있으며, 이러한 방식을 통해 향후 생산 로트에 대한 규정 준수 부담을 줄일 수 있습니다. 이러한 동향은 확립된 컴플라이언스 팀과 문서화된 품질 시스템을 갖춘 기존 기업에 유리하게 작용하여, 규제 방향이 명확한 지역으로 시장 점유율을 이동시킬 가능성이 있습니다.

부문별 분석

2025년 매출액 중 무인 수중 차량(UUV)이 62.24%를 차지했습니다. 이는 고객이 고위험 지역에서의 ISR(정보·감시·정찰) 및 기뢰전 수행 시, 은밀성, 항속 시간, 그리고 낮은 감지 가능성을 우선시했기 때문입니다. 수중 함대에서는 조작 및 검사 업무에 ROV(원격 조종 무인 잠수정)의 도입 대수가 여전히 많은 반면, 광역 조사를 위한 경로 계획, 분류, 자율성 향상에 따라 AUV(자율형 무인 잠수정)의 보급이 급속히 확대되고 있습니다. 시장에서는 많은 주요 프로그램이 신속한 페이로드 교체를 가능하게 하는 모듈식 베이를 갖춘 심해 대응 선체에 계속해서 의존하고 있으며, 이를 통해 플랫폼 전체를 교체하는 것에 비해 업그레이드 소요 시간을 단축하고 있습니다. 수상 분야에서는 원격 조작 센터의 보급과 지속 가능한 무인 검사·순찰 임무를 지원하는 규제 당국의 승인이 도입 확대의 원동력이 되고 있습니다. USV(무인수상정)는 13.99%라는 가장 높은 성장률을 보이고 있으며, 이는 풍력 발전소 점검과 같은 활용 사례에 힘입은 결과입니다. 이 이용 사례에서는 무인수상정이 전동 ROV의 모선으로 기능하여, 혹독한 기상 조건에서도 지속적인 운용이 가능하도록 하고 있습니다. 플러그 앤 플레이 방식의 페이로드 제품군을 제공하는 플랫폼 제조업체는 선체를 대폭 재설계하지 않고도 국방 분야와 상업 분야 모두의 워크플로우에 대응할 수 있는 유연성을 확보하고 있습니다.

규제 체계 또한 수상 시스템과 수중 시스템 시장 진입 경로에 차이를 가져오고 있습니다. 국제해사기구(IMO)는 무인 수상 선박의 충돌 방지, 원격 조종 자격 요건 및 사이버 복원력에 관한 거버넌스의 기반이 되는 ‘MASS 코드’의 제정을 추진하고 있습니다. 일부 국가 당국은 무인 해양 작업에 관한 선례가 될 만한 허가를 발급하고 있으며, 육상 거점의 선장을 대상으로 한 면허 제도를 마련하고 있습니다. 이는 상용 USV(무인수상정)를 위한 지속 가능한 운영 모델이 점차 확립되고 있음을 시사하는 움직임입니다. 수중 플랫폼의 경우, 압력 안전성, 이중화 및 특정 임무 프로파일에서의 구조화된 자율성에 대한 검증을 중시하는 선급 규정이 계속해서 적용되고 있습니다. 두 분야의 성장은 통합 부담을 최소화하면서도 플랫폼 유형에 관계없이 전환이 가능한 모듈형 센서 및 자율성 스택에 힘입어 가속화되고 있습니다.

소형 선박은 2025년 시장 점유율의 49.20%를 차지한 것으로 평가되었으며, 구매자들이 수동으로 전개 가능한 시스템이나 육상에서 여러 자산을 제어할 수 있는 방식을 선호함에 따라 연평균 성장률(CAGR) 13.40%라는 가장 빠른 성장세를 보일 것으로 전망됩니다. 훈련이나 원정 시의 이용 사례에서는 대형 선박 없이도 발진 및 회수가 가능한 선박이 유리하게 작용하여, 용선 비용 절감과 전개 빈도 증가로 이어집니다. 무인 해양 시스템 시장에서는 이러한 특징이 예산 주기의 단축과 임무 일정의 유연성이라는 측면에서 높이 평가되며, 그 결과 가동률과 전체 수명 주기 가치가 향상됩니다. 중형급은 적재량과 항속 거리, 그리고 운송 및 갑판에서의 취급 편의성 사이에서 균형을 잘 맞추고 있어, 프로젝트 간에 자산을 순환 배치하는 측량 회사나 에너지 관련 고객에게 가장 적합합니다. 이 등급에는 장시간 임무를 수행할 수 있는 견고한 항법 기능과 동력원이 필요한 작업용 ROV 및 중수심용 AUV가 대표적으로 포함됩니다. 자본 집약도가 가장 높은 대형 및 초대형 함정은 작전 깊이와 기간의 장기화로 인해 높은 단가가 정당화되는 전략적 임무, 심해 임무, 혹은 장기간의 초계 임무에 사용됩니다.

임무 프로파일에 따른 조달 경향은 국방 및 상선 함대에서 어떤 규모 대가 가장 빠르게 확대될지에 영향을 미칩니다. 방위 분야의 기뢰전 팀과 ISR(정보·감시·정찰) 운용자들은 신속한 전개, 분산형 감지, 그리고 짧은 주기 내에서의 높은 재사용성을 추구하며 소형 및 중형급 장비에 주목하고 있습니다. 한편, 상업 분야의 O&M(운영·유지보수) 팀은 터빈 검사용 소형 유닛과 조사 범위를 커버하는 중형 유닛 모두의 도입 타당성을 입증할 수 있으며, 대부분의 경우 수상·수중 쌍으로 구성되어 운영됩니다. 단위당 경제성이라는 관점에서 볼 때, 빈도가 높은 임무에는 소형 차량이 유리하지만, 해저 매핑이나 전략적 해저 인프라 감시 같은 용도에서는 심해 대응 프리미엄 차량이 주류를 이루고 있습니다. 모든 규모에서 소프트웨어 중심의 자율 항해 및 군집 제어를 통해, 단일 선체가 아닌 함대 전체에 걸친 센서 융합 및 명령 미들웨어의 가치가 더욱 높아지고 있습니다.

지역별 분석

북미는 2025년 매출의 38.36%를 차지했으며, 대인·대물 기뢰전 및 ISR(정보·감시·정찰) 분야의 지속적인 조달과 활발한 시제품 개발 프로그램에 힘입어, 2031년까지 연평균 성장률(CAGR) 14.09%라는 지역 내 가장 높은 성장률을 나타낼 것으로 전망됩니다. 새로운 다목적 AUV의 도입 및 시험 단계는 보다 대규모의 함대 구상 속에서 잠수함과 호환성을 갖춘 차량과 수상 자율 기술을 융합한, 점차 성숙해 가고 있는 개발 파이프라인을 뒷받침하고 있습니다. 해당 지역의 무인 해양 시스템 시장에서는 분쟁 지역에서 얻은 교훈을 반영한 대기뢰 장비의 연속 납품도 진행되고 있습니다. 이를 통해 신속한 구축이 가능한 모듈식 시스템이 제공되고 있습니다. 미국 및 캐나다공급업체들은 확립된 방위 체계와 연계된 수직 통합형 페이로드 및 자율 제어 스택을 통해 리더십을 강화하고 있습니다. 해상 풍력 발전 및 환경 모니터링 계약에 따른 상업 활동도 확대되고 있으며, 대규모 무인 운영을 뒷받침하기 위한 인허가 및 인프라 구축이 진행되고 있습니다.

유럽에서는 특히 북해, 발트해, 대서양 항로에서 국방 분야와 민간 분야의 도입이 발맞추어 진행되고 있습니다. 스칸디나비아 국가들은 자율주행 및 배터리 구동 방식의 확산과 부합하는 무인 운행 허가, 원격 조종, 그리고 무공해 규제의 선구자 역할을 계속해 오고 있으며, 이는 결과적으로 민간 검사 및 물류 분야에서의 활용 사례를 촉진하고 있습니다. 유럽의 방위 프로그램에는 해저 지도 작성, 기뢰 감지, 심해 인프라 보호를 목적으로 하는 대형 수중 차량 및 군집형 프로젝트가 포함되어 있습니다. 민간 사업자는 유인 조사선에 비해 연료 소비 및 배기가스 배출 측면에서 이점이 있는 USV와 ROV를 결합한 풍력 발전 설비의 24시간 365일 점검 워크플로우에 대한 검증을 계속하고 있습니다. 이 지역의 정책 환경과 프로젝트 집중도로 인해, 고위도 지역이나 급변하는 해상 상황에 적합한 플랫폼과 센서 모두에 대해 지속적인 수요가 발생하고 있습니다.

아시아태평양 지역 수요는 국방력 현대화, 해상 풍력 발전의 확대, 그리고 복잡한 해안선을 따라 해양 영역을 파악해야 할 필요성에 의해 주도되고 있습니다. 이 지역의 조사 결과는 초대형 UUV(무인 잠수함)의 항속 시간, 잠수 깊이, 항해 안정성 측면에서 성능이 향상되었음을 여실히 보여주고 있으며, 총 조달액을 끌어올리는 치열한 기술 개발 경쟁이 진행 중임을 시사하고 있습니다. 한국과 싱가포르는 국내 프로그램 및 파트너십을 통해 해상 보안 및 상업 활동에 자율 기술을 지속적으로 통합하고 있습니다. 한편, 호주의 생태계에서는 조달 활동이 인도-태평양 지역의 지속적인 감시 및 억지력 강화와 연계되어 있습니다. 이 지역 전체에서 각국의 규제가 MASS형 거버넌스와 부합하고, 에너지 당국이나 항만 당국이 관리하는 항로에서 무인 운항이 가능하도록 허용하는 지역에서는 도입이 더욱 신속하게 진행될 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the unmanned sea systems market size is expected to grow from USD 2.99 billion in 2025 to USD 3.37 billion in 2026 and is forecast to reach USD 5.51 billion by 2031 at a 12.94% CAGR over 2026-2031.

This report is Segmented by Platform Type (Unmanned Underwater Vehicles (UUVs) and Unmanned Surface Vehicles (USVs)), Vehicle Size (Small, Medium, and Large), Propulsion (Electric, Hybrid, and More), Application (Military and Commercial), Component Type (Hull, Autonomy Suite, Sensors Suite, and More), and Geography (North America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Unmanned Sea Systems Market Trends and Insights

Expansion of Global Naval Modernization and Force Transformation Programs

Defense procurement emphasizes autonomous platforms as force multipliers for operational efficiency in contested maritime environments. Newly introduced programs and prototypes highlight navies' progression from experimental phases to operational integration of mine warfare, ISR capabilities, and distributed undersea effectors in fleet planning. Lockheed Martin Corporation introduced the Lamprey Multi-Mission Autonomous Undersea Vehicle in February 2026 as a modular submersible with a reconfigurable payload bay to support ISR, electronic warfare, and kinetic missions. Saab AB advances large undersea vehicles under national contracts, focusing on long-range deterrence and seabed defense, through formal European programs supporting strategic defense objectives. NATO is formalizing interoperability through standards and frameworks, reducing integration challenges for multinational task groups. These measures accelerate deployment timelines for autonomous assets and standardize modular payload updates, enhancing operational efficiency across allied fleets.

Rising Demand for Offshore Wind Farm Inspection and Seabed Survey Missions

Autonomous inspection is critical as offshore wind operators expand operations, balancing limited O&M budgets with stringent ESG compliance requirements. In April 2023, Fugro conducted the first fully remote offshore wind farm inspection using its Blue Essence USV and Blue Volta eROV. European wind-farm stakeholders are introducing autonomy to reduce crew transfers and expand inspection windows, with field deployments that reveal strong operating cost and uptime benefits for persistent monitoring. These initiatives enhance zero-crew concepts by mitigating weather-related downtime, transitioning labor from sea to shore, and streamlining inspection payback. This establishes a dependable pipeline for unmanned platforms, underpinned by resilient O&M contracts across multiple wind basins.

Export Control Regulations and ITAR Restrictions Limiting Global Sales

Licensing regulations and defense article classifications extend transaction cycles for autonomous vehicles and payloads, prompting vendors to localize production, customize configurations, or prioritize sales within regions aligned with shared compliance frameworks. Companies that deliver modular architectures can advance capability through payload upgrades that avoid fresh platform certifications, a method that can reduce the compliance burden on subsequent tranches. These dynamics collectively favor incumbents with established compliance teams and documented quality systems and can nudge market share toward geographies with clearer regulatory pathways.

Other drivers and restraints analyzed in the detailed report include:

- Declining Cost per Sea Mile Compared to Crewed Surface Vessels

- Increased Adoption of Swarm-Capable USVs for MCM Operations

- High Vulnerability to GNSS Denial in Contested Maritime Environments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Unmanned Underwater Vehicles (UUVs) accounted for 62.24% of 2025 revenue, as customers prioritized stealth, endurance, and low-observable signatures for ISR and mine warfare in high-risk zones. Within subsurface fleets, ROVs hold a larger installed base for manipulation and inspection tasks, while AUVs are scaling faster as route planning, classification, and autonomy improve for wide-area survey. The market continues to anchor many of its premium programs on deep-rated hulls with modular bays that support rapid payload swaps, which compresses upgrade timelines versus full platform replacement. On the surface, rising adoption is being driven by remote operations centers and regulatory green lights that support persistent, uncrewed inspection and patrol missions. USVs grow fastest at 13.99%, reinforced by wind-farm inspection use cases, where uncrewed surface craft act as motherships for electric ROVs, enabling continuous operation through challenging weather. Platform makers that deliver plug-and-play payload suites gain flexibility to address both defense and commercial workflows without major hull redesigns.

Regulatory frameworks also differentiate the pathway to market for surface and subsurface systems. The International Maritime Organization is progressing the MASS Code, which provides the governance foundation for collision avoidance, remote operations qualifications, and cyber resilience for uncrewed surface vessels. Select national authorities have issued precedent-setting permits for uncrewed offshore operations and are building licensing regimes for shore-based masters, a move that signals durable operating models for commercial USVs. Subsurface platforms continue to follow classification rules that emphasize pressure safety, redundancy, and the validation of structured autonomy across specific mission profiles. Growth on both vectors is strengthened by modular sensors and autonomy stacks that can migrate across platform types with limited integration overhead.

Small-class vehicles captured 49.20% of the 2025 share and are set to deliver the fastest growth, 13.40% CAGR, as buyers favor hand-deployable systems and multi-asset control from shore. Training and expeditionary use cases benefit from vehicles that can be launched and recovered without the need for large ships, reducing charter costs and expanding deployment frequency. The unmanned sea systems market rewards these attributes with shorter budgeting cycles and mission-scheduling agility, thereby lifting utilization and total lifecycle value. Medium-class formats balance payload and endurance with transport and deck-handling practicalities, which make them well-suited for survey firms and energy customers that rotate assets across projects. This class is the typical home for work-class ROVs and mid-depth AUVs that require robust navigation and power for longer missions. The most capital-intensive large and extra-large vehicles serve strategic, deep-ocean, or long-patrol missions where mission depth and duration justify higher unit costs.

Procurement preferences by mission profile influence which size bands scale fastest across defense and commercial fleets. Defense mine warfare teams and ISR operators lean toward small and medium classes for rapid deployment, distributed sensing, and high reusability across short cycles. Commercial O&M teams can justify both small units for turbine inspections and medium units for survey coverage, often in paired surface-subsurface configurations. Unit economics favor small vehicles for high-frequency tasks, while deep-rated premium vehicles dominate applications such as seabed mapping and strategic undersea infrastructure monitoring. Across all sizes, software-centric autonomy and swarm control are pushing more value into sensor fusion and command middleware that span fleets rather than single hulls.

Geography Analysis

North America accounted for 38.36% of 2025 revenue and is projected to register the fastest regional CAGR of 14.09% through 2031, supported by ongoing procurement and active prototype programs across mine warfare and ISR. New multi-mission AUV introductions and test milestones underscore a maturing pipeline that blends submarine-compatible vehicles and surface autonomy within larger fleet concepts. The unmanned sea systems market in the region also reflects serial deliveries of mine countermeasures that leverage lessons from contested theaters to deliver modular systems ready for rapid deployment. The US and Canadian suppliers reinforce leadership with vertically integrated payloads and autonomy stacks linked to established defense frameworks. Commercial activity is growing from offshore wind and environmental monitoring contracts, with approvals and infrastructure emerging to support uncrewed operations at scale.

Europe shows synchronized defense and commercial adoption, especially in the North Sea, Baltic, and Atlantic corridors. Scandinavian countries continue to pioneer uncrewed permitting, remote operations, and zero-emission mandates that align with autonomous, battery-electric deployments, which, in turn, catalyze commercial inspection and logistics use cases. European defense programs include large undersea vehicles and swarm projects that target seabed mapping, mine hunting, and infrastructure protection at depth. Commercial operators continue to validate 24/7 inspection workflows for wind assets using USVs paired with ROVs, with fuel and emissions benefits relative to crewed survey ships. This region's policy environment and project density create durable demand for both platforms and sensors suited to high latitudes and variable sea states.

Asia-Pacific demand is driven by defense modernization, offshore wind build-out, and maritime domain awareness needs along complex coastlines. Regional research output highlights advancing capabilities in extra-large UUVs across endurance, depth, and navigation resilience, pointing to a competitive technology race that drives aggregate procurement. South Korea and Singapore continue to integrate autonomy into maritime security and commercial operations through domestic programs and partnerships. At the same time, Australia's ecosystem ties procurement to persistent Indo-Pacific monitoring and deterrence. Across the region, swifter adoption is likely where national rules align with MASS-style governance and where energy and port authorities enable zero-crew operations in controlled corridors.

- TKMS GmbH

- BAE Systems plc

- General Dynamics Corporation

- Lockheed Martin Corporation

- Unique Group

- Teledyne Technologies Incorporated

- Saab AB

- L3Harris Technologies, Inc.

- Maritime Robotics AS

- The Boeing Company

- Exail Technologies SA

- Elbit Systems Ltd.

- SAILDRONE, Inc.

- EDGE Group PJSC

- SeaRobotics Corporation

- Ocean Aero

- Textron Inc.

- Sea Machines Robotics, Inc.

- Thales Group

- Kongsberg Gruppen ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of global naval modernization and force transformation programs

- 4.2.2 Rising demand for offshore wind farm inspection and seabed survey missions

- 4.2.3 Declining cost per sea mile compared to crewed surface vessels

- 4.2.4 Increased adoption of swarm-capable USVs for MCM operations

- 4.2.5 ESG-linked Insurance Discounts for Zero-crew Craft

- 4.2.6 Defense offset policies promoting domestic integration of USS

- 4.3 Market Restraints

- 4.3.1 Export control regulations and ITAR restrictions limiting global sales

- 4.3.2 High vulnerability to GNSS denial in contested maritime environments

- 4.3.3 Limited availability of certified maritime AI-assurance and testing ranges

- 4.3.4 Disruptions in lithium-titanate battery supply impacting endurance-focused platforms

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform Type

- 5.1.1 Unmanned Underwater Vehicles (UUVs)

- 5.1.1.1 Remotely Operated Vehicles (ROVs)

- 5.1.1.2 Autonomous Underwater Vehicles (AUVs)

- 5.1.2 Unmanned Surface Vehicles (USVs)

- 5.1.2.1 Remotely Operated Surface Vehicles (ROSVs)

- 5.1.2.2 Autonomous Surface Vehicles (ASVs)

- 5.1.1 Unmanned Underwater Vehicles (UUVs)

- 5.2 By Vehicle Size

- 5.2.1 Small

- 5.2.2 Medium

- 5.2.3 Large

- 5.3 By Propulsion

- 5.3.1 Electric

- 5.3.2 Hybrid

- 5.3.3 Diesel and Gas-Turbine

- 5.3.4 Renewable (Solar/Wave)

- 5.4 By Application

- 5.4.1 Military

- 5.4.1.1 Intelligence, Surveillance, and Reconnaissance (ISR)

- 5.4.1.2 Mine Counter-Measures (MCM)

- 5.4.1.3 Anti-Submarine Warfare (ASW)

- 5.4.1.4 Logistics and Resupply

- 5.4.2 Commercial

- 5.4.2.1 Environment Monitoring

- 5.4.2.2 Infrastructure Inspection

- 5.4.2.3 Hydrographic Survey

- 5.4.2.4 Others

- 5.4.1 Military

- 5.5 By Component Type

- 5.5.1 Hull

- 5.5.2 Autonomy Suite

- 5.5.3 Communications and Navigation

- 5.5.4 Sensors Suite

- 5.5.5 Propulsion and Power Systems

- 5.5.6 Others (Payload, Launch/Recovery systems)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 TKMS GmbH

- 6.4.2 BAE Systems plc

- 6.4.3 General Dynamics Corporation

- 6.4.4 Lockheed Martin Corporation

- 6.4.5 Unique Group

- 6.4.6 Teledyne Technologies Incorporated

- 6.4.7 Saab AB

- 6.4.8 L3Harris Technologies, Inc.

- 6.4.9 Maritime Robotics AS

- 6.4.10 The Boeing Company

- 6.4.11 Exail Technologies SA

- 6.4.12 Elbit Systems Ltd.

- 6.4.13 SAILDRONE, Inc.

- 6.4.14 EDGE Group PJSC

- 6.4.15 SeaRobotics Corporation

- 6.4.16 Ocean Aero

- 6.4.17 Textron Inc.

- 6.4.18 Sea Machines Robotics, Inc.

- 6.4.19 Thales Group

- 6.4.20 Kongsberg Gruppen ASA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment