|

시장보고서

상품코드

2066500

호버크래프트 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Hovercraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

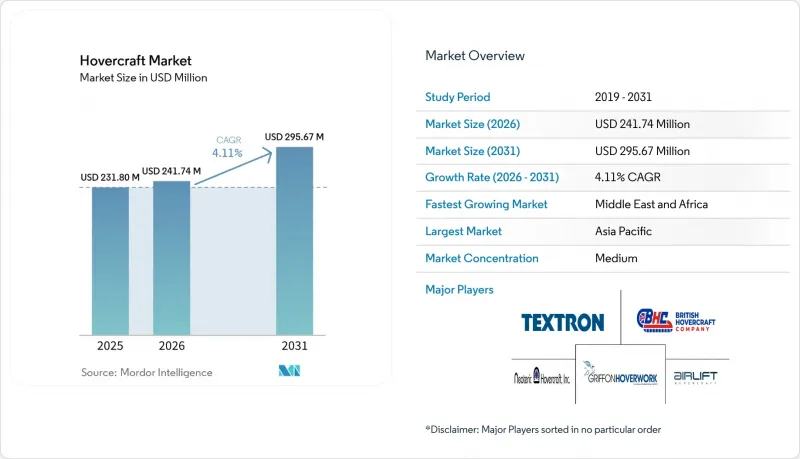

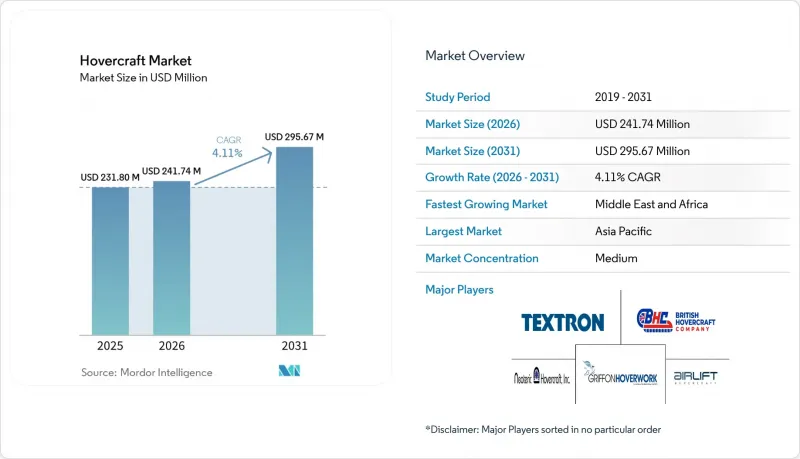

Mordor Intelligence에 의하면, 호버크래프트 시장 규모는 2025년 2억 3,180만 달러로 평가되었고, 2026년에는 2억 4,174만 달러로 추정되고, 2026-2031년 CAGR 4.11%로 성장을 지속할 전망이며, 2031년에는 2억 9,567만 달러에 이를 것으로 예측됩니다.

본 보고서는 호버크래프트 크기별(소형, 중형, 대형), 용도별(방위 및 보안, 여객 페리 서비스, 해양 에너지 지원 등), 추진 시스템별(디젤 엔진, 가스 터빈, 하이브리드 전기, 완전 전기, 수소 연료전지), 최종 사용자별(군사 및 민간), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 호버크래프트 시장 동향 및 분석

기후 변화로 인한 홍수로 인해 수륙 양용 운송 수단에 대한 수요가 증가하고 있습니다.

극심한 강우로 인해 연안 도시에서는 침수된 도로, 잔해가 쌓인 운하, 얼음으로 막힌 하천을 횡단할 수 있는 전지형 보트 수요가 증가하고 있습니다. 인도의 PROTECT 기금을 통한 재해 대책 프로그램과 미국 교통부(DoT)의 90억 달러 규모의 회복탄력성 기금은 모두 지방자치단체의 호버크래프트 조달을 위한 보조금 체계를 마련하고 있습니다. 네덜란드와 영국의 주·군급 기관에서는 선박의 침수 깊이가 너무 깊어 항해할 수 없거나, 바퀴 달린 차량이 진흙에 빠져 움직일 수 없게 되는 제방 붕괴 사태에 대비해 에어쿠션식 구조정의 시범 운용을 진행하고 있습니다. 홍수는 간헐적으로 발생하기 때문에 리스 모델이 주목받고 있으며, 이를 통해 도시는 지속적인 자본 지출 없이도 대응 능력을 확보할 수 있게 됩니다. 수요의 급증은 몬순 시즌의 남아시아 및 동남아시아, 그리고 허리케인 시즌의 미국 멕시코만 연안 지역에 집중되어 있어, 예측 가능하기는 하지만 단기간의 배치 기간이 발생하고 있습니다. 모듈식 구조로 신속하게 배치할 수 있는 소형 선박을 공급하는 제조업체는 주기적이면서도 지속적인 수익원을 확보할 수 있는 입장에 있습니다.

현대 강습 및 병참용 호버크래프트의 군용 함정 교체 주기

미 해군의 ‘십-투-쇼어 커넥터(SSC)’ 프로그램은 방위 장비의 교체에 보통 10년이 소요되는 전형적인 일정을 보여주는 좋은 사례입니다. 첫 번째 시제기는 2020년에 취항했으며, 3억 9,430만 달러 규모의 추가 발주에 따른 납품은 2030년까지 이어질 전망입니다. 최신형 SSC 선체는 74톤을 상륙시킬 수 있으며, M1A2 전차를 수송하기에 충분한 능력을 갖추고 있습니다. 또한, 기어박스 수를 절반으로 줄임으로써 수명 주기 전반에 걸친 유지 관리 비용을 절감하고 있습니다. 중국이 2024년 12월에 취역시킨 076형 강습상륙함은 상륙정이나 호버크래프트를 수용할 수 있는 크기의 웰데크를 갖추고 있어, 태평양 지역의 군비 경쟁을 더욱 격화시키고 있습니다. 북유럽 국가들도 이러한 추세를 따르고 있으며, 핀란드는 2025년 빙해 순찰 임무를 위해 그리폰 마린(Griffon Marine)사에 북극해 대응형 전장 12.7미터의 호버크래프트 3척을 발주했습니다. 국방 예산은 지방 자치단체의 재원보다 비용 초과분을 흡수하기 쉬운 편이지만, 미국의 ‘폴라 시큐리티 커터’와 같은 경쟁 프로그램이 자금을 흡수하고 있어 보조용 호버크래프트의 조달 속도는 둔화되고 있습니다.

연안 지역의 높은 운전 소음과 환경 규제

가스 터빈이나 고회전 디젤 엔진을 탑재한 선박은 일상적으로 85 dB(A)를 초과하여, 미국 국립공원관리청이 정한 항해 중 소음 제한치인 75 dB(A) 및 캘리포니아주와 스칸디나비아 국가들의 동등한 규정을 위반하고 있습니다. 사우샘프턴, 샌프란시스코, 오사카의 각 항만 당국은 계절에 따른 운항 제한을 부과하고 있으며, 이로 인해 관광 크루즈와 페리의 운항 일정이 제한되고 있습니다. 규정 준수를 목표로 하는 운항 사업자는 엔진 출력을 낮추거나, 방음 커버를 추가하거나, 혹은 전기 구동 방식으로 전환할 수밖에 없지만, 어느 선택지든 항속 거리나 비용 면에서 단점이 따릅니다. 세계에서 가장 오래된 여객 운송 서비스인 호버트래블사는 지역 사회의 엄격한 감시 아래 소렌토 해협에서 운항을 계속하고 있으며, 60년에 걸친 항로를 유지하기 위해 현재 자사 선단의 동력원을 배터리식 전기 기술로 전환하는 방안을 검토하고 있습니다. 2028년까지 제로 배출을 위한 개조 비용이 경제적 측면에서 동등한 수준이 될 전망이 없는 한, 운항 사업자는 더 엄격한 소음 제한 하에서도 운항할 수 있는 수중익선에 대한 투자로 방향을 전환할 가능성이 있습니다.

부문별 분석

중형 항공기는 방위 및 해양 물류 임무를 통해 2025년 매출의 46.27%를 차지했습니다. 한편, 소형 선박 부문은 도시 지역에서의 전기 구조정 도입과 레저 이용자들의 무공해 모델로의 전환 추세에 힘입어 연평균 성장률(CAGR) 5.23%로 성장할 것으로 전망되며, 이는 호버크래프트 시장의 성장세를 더욱 강화할 것으로 보입니다. 74톤급 SSC와 같은 중형 함정은 앞으로도 군사 전개 전략에서 없어서는 안 될 존재로 남을 것입니다. 또한, 러시아의 ‘허스키-10’은 북극권에서의 적재량 수요가 중형 선체에 대한 수요를 뒷받침하고 있음을 보여줍니다.

15미터 미만의 소형 설계는 신속한 대응이 요구되는 순찰 활동에 적극적인 핀란드와 캐나다의 기관들이 진행하는 예산 제약이 있는 입찰에서 유리한 입지를 점하고 있습니다. 배터리의 무게는 선체 부피에 비례하여 증가하기 때문에 소형 선체라도 100해리의 항속 거리 기준을 조기에 달성할 수 있으며, 이로 인해 지자체 차원의 호버크래프트 시장 확대가 촉진되고 있습니다. 대형 선박의 경우, 중국과 러시아를 제외한 지역에서는 수륙양용 모함의 갑판 공간이 여전히 제한적이기 때문에 고객 기반이 축소되는 추세입니다. 그 결과, 모듈식 소형 선박 생산 체계를 구축한 제조업체는 수년에 걸친 방위 조달 지연을 걱정할 필요 없이 증가하는 수주를 확보할 수 있을 것으로 보입니다.

2025년 시장 규모에서 방위 분야는 37.44%를 차지했습니다. 그럼에도 불구하고, 해상 에너지 지원 분야는 풍력 발전소 운영 사업자들이 헬리콥터에서 고속 표면 효과 셔틀로 전환함에 따라 2031년까지 연평균 성장률(CAGR) 5.24%를 나타낼 것으로 예측되며, 추적 대상 용도 중 가장 높은 성장률을 보이고 있습니다. Hovertravel을 대표로 하는 여객 페리는 저소음과 연료비 절감을 내세우는 하이드로포일 업체들의 경쟁 압박에 직면해 있습니다.

수색구조(SAR) 및 측량 분야는 여전히 틈새 시장이지만, 특히 극지 항로로 접근하기가 쉬워짐에 따라 전략적으로 매우 중요한 위치를 차지하고 있습니다. 해상 작업원 수송의 경제성은 자본 비용을 일일 순환에 분산시키는 정기 계약을 촉진하고 있으며, 이는 간헐적인 국방 분야 조달과는 대조적입니다. IMO와 해상 풍력 발전 선급 협회 양측 모두로부터 선체를 인증받을 수 있는 부문의 사업자는 높은 이익률을 확보하게 되며, 이는 호버크래프트 시장 점유율이 기존의 군사 의존에서 다각화되는 수요의 전환을 여실히 보여주고 있습니다.

지역별 분석

중국, 일본, 인도가 수륙 양용 능력 및 재난 대응 능력을 강화한 결과, 2025년 납품 대수의 33.11%를 아시아태평양이 차지했습니다. 중국의 076형 진수식을 포함한 해당 지역의 해군 프로그램이 수요 기반을 뒷받침하는 한편, 남아시아 전역에서 증가하고 있는 지방 자치단체의 발주가 수요를 더욱 끌어올리고 있습니다. 그러나 호버크래프트 시장 점유율에 대한 주도권은 중동 및 아프리카에 의해 서서히 위협받고 있습니다. 이 지역에서는 해상 석유 시설에 대한 승무원 수송 계약과 홍해에서의 치안 순찰을 원동력으로 연평균 성장률(CAGR) 6.01%의 성장이 예상됩니다.

ADNOC이나 사우디 아람코와 같은 걸프 지역 기업들은 헬리콥터 운영 비용 절감액을 연간 수,000만 달러 규모로 추산하고 있으며, 이로 인해 하이브리드 전기식 승무원 수송선에 대한 추가 투자가 촉진되고 있습니다. 앙골라에서의 AIRCAT 35 도입은 서아프리카 석유 개발 지역의 유사한 경제 상황을 반영하고 있습니다. 유럽은 환경 규제 강화로 인해 제약을 받고 있지만, 북극권 순찰용 장비 조달 및 수년에 걸친 소렌토 해협 여객 운송 서비스를 통해 안정적인 수주 파이프라인을 유지하고 있습니다.

북미에서는 SSC의 기체 교체 주기와 캐나다의 제로 배출 설계 연구의 혜택을 받고 있습니다. 그러나 미국 해안경비대의 예산이 쇄빙선에 배정되면서 보조용 호버크래프트 구매가 주춤해져, 해당 지역의 확장은 더디게 진행되고 있습니다. 남미에서는 여전히 시장 침투율이 낮고, 얕은 흘수(吃水)를 가진 강철 선박의 가격이 에어쿠션 선박의 도입 비용보다 저렴하기 때문입니다. 전반적으로 호버크래프트 시장은 전 세계 에너지 투자 동향을 점점 더 반영하고 있으며, 풍력 발전소나 탄화수소 거점과 관련된 지역에서 높은 성장이 예상됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the hovercraft market size is expected to grow from USD 231.80 million in 2025 to USD 241.74 million in 2026 and is forecasted to reach USD 295.67 million by 2031 at a 4.11% CAGR over 2026-2031.

This report is Segmented by Hovercraft Size (Small, Medium, and Large), Application (Defense and Security, Passenger Ferry Services, Offshore Energy Support, and More), Propulsion System (Diesel Engine, Gas Turbine, Hybrid-Electric, Fully Electric, and Hydrogen Fuel-Cell), End User (Military and Commercial), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Hovercraft Market Trends and Insights

Rising Demand for Amphibious Transport Driven by Climate-Related Flooding

Extreme rainfall pushed coastal cities to seek all-terrain craft that can traverse submerged streets, debris-laden canals, and ice-choked rivers. India's PROTECT-funded disaster program and the US Department of Transportation's (DoT's) USD 9 billion resilience fund both create grant pathways for municipal hovercraft procurement. Provincial and county-level agencies in the Netherlands and the United Kingdom are trialing air-cushion rescue fleets for dike-breach scenarios where boats draw too much draft and wheeled vehicles stall in mud. Leasing models are emerging because flood events are episodic, allowing cities to secure capabilities without a permanent capital outlay. Demand spikes concentrate in South and Southeast Asia during monsoon seasons and along the US Gulf Coast during hurricane months, creating a predictable but short deployment window. Manufacturers that supply modular, quickly deployable small craft stand to capture this cyclical but resilient revenue stream.

Military Fleet Replacement Cycles for Modern Assault and Logistics Hovercraft

The US Navy's Ship-to-Shore Connector (SSC) program exemplifies the typical decade-long timeline of defense recapitalization. The first experimental unit sailed in 2020, and deliveries under the USD 394.3 million follow-on order are expected to run through 2030. Modern SSC hulls can lift 74 tons, enough to support an M1A2 tank, while halving the gearbox count, which reduces life-cycle maintenance costs. China's December 2024 launch of the Type 076 amphibious assault ship widens the Pacific arms race by adding a well deck sized for landing craft and hovercraft. Nordic states echo the trend; Finland ordered three 12.7 m Arctic-capable units from Griffon Marine in 2025 for ice patrol duties. Although defense budgets absorb cost overruns better than municipal coffers, competing programs such as the Polar Security Cutter in the United States siphon funds, slowing auxiliary hovercraft acquisitions.

High Operating Noise and Environmental Restrictions in Coastal Regions

Gas-turbine and high-RPM diesel fans routinely exceed 85 dB(A), breaching the US National Park Service's 75 dB(A) underway limit and comparable rules in California and Scandinavia. Port authorities at Southampton, San Francisco, and Osaka have imposed seasonal curfews that curtail tourist runs and ferry schedules. Operators pursuing compliance must derate engines, add acoustic shields, or switch to electric drives, each option imposing range or cost penalties. Hovertravel, the world's oldest passenger service, continues its Solent operations under community scrutiny and is now studying the repower of its fleet with battery-electric technology to preserve its 60-year route. Unless zero-emission retrofits reach economic parity by 2028, operators may divert investment toward hydrofoil alternatives that sail under stricter noise caps.

Other drivers and restraints analyzed in the detailed report include:

- Advances in Low-Noise Electric and Hydrogen Propulsion Technologies

- Growing Offshore Energy and Polar Logistics Requirements

- Scarcity of Certified Pilots and Specialized Maintenance Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium units secured 46.27% of 2025 revenue due to defense and offshore logistics missions, while the small-craft cohort is forecast to grow at 5.23% CAGR as cities adopt electric rescue fleets and leisure users upgrade to zero-emission models, reinforcing momentum in the hovercraft market. Medium hulls, such as the 74-ton SSC, will remain integral to force-projection strategies, and Russia's Husky-10 demonstrates how Arctic payload needs sustain mid-size demand.

Small designs under 15 meters are winning budget-constrained tenders from Finnish and Canadian agencies keen on rapid-response patrols. Battery weights scale linearly with hull volume, allowing compact footprints to reach 100-nautical-mile range thresholds sooner, thereby fueling the expansion of the hovercraft market at the municipal level. Large craft face a contracting customer base outside China and Russia because amphibious mothership decks remain limited. As a result, producers that master modular small-craft production stand to capture rising orders without the multiyear defense procurement lag.

Defense retained 37.44% of the 2025 value. Still, offshore energy support is projected to deliver a 5.24% CAGR through 2031, the fastest among the tracked uses, as wind farm operators shift from helicopters to high-speed surface-effect shuttles. Passenger ferries, exemplified by Hovertravel, face pressure from hydrofoil rivals that promise lower noise and fuel costs.

Search-and-rescue (SAR) and surveying remain niche yet strategically vital, especially as polar routes become more accessible. Offshore crew transfer economics drive recurring contracts that spread capital cost over daily rotations, contrasting with episodic defense buys. Segment operators who can certify hulls to both the IMO and offshore wind classification societies will anchor premium margins, underlining a demand pivot that diversifies the hovercraft market share away from traditional military reliance.

Geography Analysis

The Asia-Pacific region accounted for 33.11% of 2025 deliveries, as China, Japan, and India bolstered their amphibious and disaster response capabilities. The region's naval programs, including China's Type 076 launch, anchor baseline demand, while emerging municipal orders across South Asia add incremental volume. However, the hovercraft market share leadership is gradually being challenged by the Middle East and Africa, which are projected to grow at a 6.01% CAGR, driven by offshore oil crew-transfer contracts and Red Sea security patrols.

Gulf operators, such as ADNOC and Saudi Aramco, quantify helicopter cost savings in the tens of millions of dollars annually, prompting further investment in hybrid-electric crew liners. Angola's AIRCAT 35 deployment reflects similar economic conditions in West African oil plays. Europe, although hampered by tighter environmental scrutiny, maintains a steady pipeline via Arctic patrol procurements and the long-running Solent passenger service.

North America benefits from the SSC fleet renewal cycle and Canadian zero-emission design studies. Yet, US Coast Guard budget reallocations toward icebreakers slow auxiliary hovercraft buys, moderating regional expansion. South America remains underpenetrated, where shallow-draft steel boats undercut the acquisition costs of air-cushion vessels. Overall, the hovercraft market is increasingly mirroring global energy investment patterns, with high-growth corridors tied to wind-farm and hydrocarbon hubs.

- Griffon Hoverwork Ltd.

- Textron Systems Corporation (Textron Inc.)

- The British Hovercraft Company Ltd.

- Neoteric Hovercraft Inc.

- AEROHOD Ltd.

- Airlift Hovercraft Pty Ltd.

- CHRISTY HOVERCRAFT

- Hovertechnics, LLC.

- Ivanoff Hovercraft AB

- Bill Baker Vehicles Ltd.

- Mad Hovercraft

- Vigor Industrial LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for amphibious transport amid climate-driven floods

- 4.2.2 Military fleet replacement cycles for modern assault craft

- 4.2.3 Advances in low-noise electric and hydrogen propulsion

- 4.2.4 Relaxed regulations supporting commercial passenger services

- 4.2.5 Offshore energy and polar logistics requirements

- 4.2.6 Increased investment in flood-oriented emergency response

- 4.3 Market Restraints

- 4.3.1 High operating noise and coastal environmental restrictions

- 4.3.2 Scarcity of certified pilots and maintenance technicians

- 4.3.3 Competition from ground-effect and hydrofoil vessels

- 4.3.4 Fuel-cost volatility affecting military procurement cycles

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Hovercraft Size

- 5.1.1 Small

- 5.1.2 Medium

- 5.1.3 Large

- 5.2 By Application

- 5.2.1 Defense and Security

- 5.2.2 Passenger Ferry Services

- 5.2.3 Offshore Energy Support

- 5.2.4 Search and Rescue

- 5.2.5 Surveying and Mapping

- 5.2.6 Agricultural and Environmental Management

- 5.3 By Propulsion System

- 5.3.1 Diesel Engine

- 5.3.2 Gas Turbine

- 5.3.3 Hybrid-Electric

- 5.3.4 Fully Electric

- 5.3.5 Hydrogen Fuel-Cell

- 5.4 By End User

- 5.4.1 Military

- 5.4.2 Commercial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Griffon Hoverwork Ltd.

- 6.4.2 Textron Systems Corporation (Textron Inc.)

- 6.4.3 The British Hovercraft Company Ltd.

- 6.4.4 Neoteric Hovercraft Inc.

- 6.4.5 AEROHOD Ltd.

- 6.4.6 Airlift Hovercraft Pty Ltd.

- 6.4.7 CHRISTY HOVERCRAFT

- 6.4.8 Hovertechnics, LLC.

- 6.4.9 Ivanoff Hovercraft AB

- 6.4.10 Bill Baker Vehicles Ltd.

- 6.4.11 Mad Hovercraft

- 6.4.12 Vigor Industrial LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment