|

시장보고서

상품코드

2066502

리튬이온 배터리 재활용 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Lithium-ion Battery Recycling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

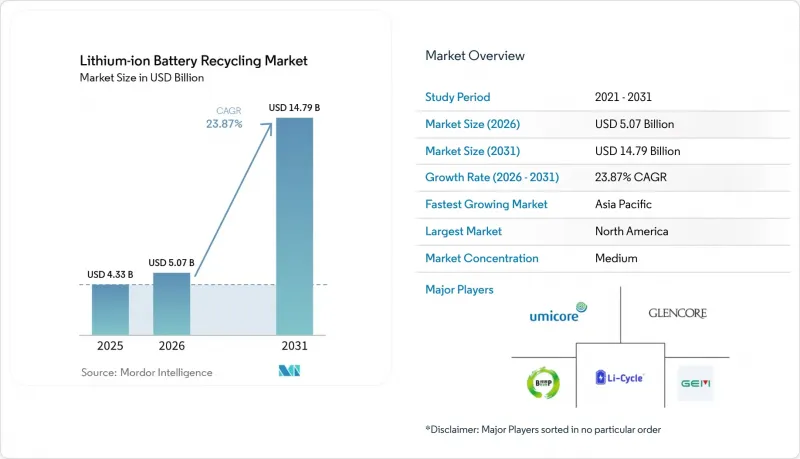

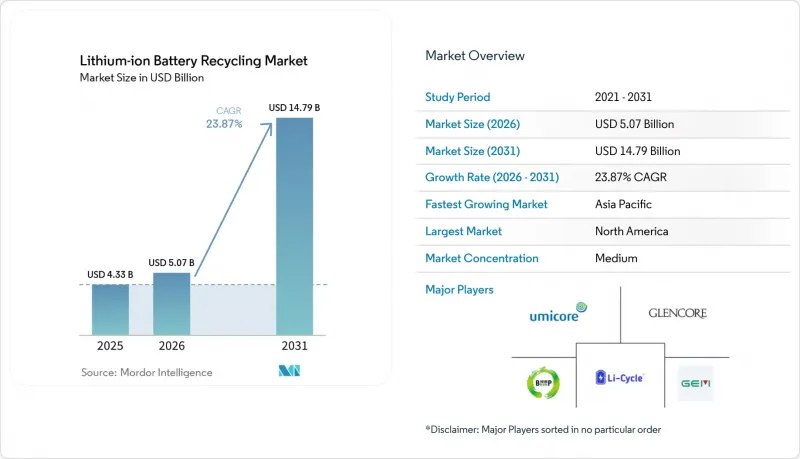

Mordor Intelligence에 의하면, 리튬이온 배터리 재활용 시장 규모는 2025년에 43억 3,000만 달러로 평가되었습니다. 2026년 50억 7,000만 달러에서 2031년까지 147억 9,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 23.87%를 나타낼 전망입니다.

본 보고서는 폐기 시 발생원(자동차 배터리 등), 배터리의 화학 조성(NMC 등), 재활용 기술(습식 야금법 등), 공정 단계(기계적 파쇄·선별 등), 회수된 재료의 용도(배터리 등급 리튬 화합물 등), 최종 사용자 산업(자동차 등), 지역(북미, 아시아태평양 등)

세계의 리튬이온 배터리 재활용 시장 동향 및 인사이트

EV 배터리 폐기가 가속화되는 추세

2015년부터 2018년에 걸쳐 판매된 초기 대중형 전기자동차는 2024년부터 2025년에 걸쳐 보증 기간이 만료되기 시작했으며, 약 28만 톤의 배터리 팩이 전 세계 각국의 회수 시스템으로 유입되었습니다. 2016년부터 2018년까지 이어진 보조금 붐기에 도입된 중국의 전기 버스나 택시가 현재 점차 퇴역하고 있는 반면, 유럽의 닛산 ‘리프’와 르노 ‘조이’ 차량들도 재활용 과정으로 넘어가고 있습니다. 이러한 변화로 인해 재활용 업체들은 수익성이 낮은 제조 스크랩에 의존하는 대신, 고부가가치인 코발트가 풍부하게 함유된 배터리 팩을 활용할 수 있게 될 것입니다. 테슬라는 자사의 4680 셀에 포함된 중요 광물의 92%를 회수해 새로운 배터리에 재사용할 수 있다고 보고했으며, 이를 통해 폐쇄형 순환 시스템의 경제적 타당성이 입증되었습니다. 2019년부터 2022년까지 판매가 급증했던 시기에 판매된 차량이 폐차 시기를 맞이하는 2027년부터 2030년에 걸쳐, 회수량이 더욱 급증할 것으로 예측됩니다.

전 세계 EPR(생산자 책임) 및 EU 배터리 규제의 요건 강화

2024년 2월에 발효된 EU 배터리 규정에 따르면, 2027년까지 63%, 2030년까지 73%의 회수 목표가 설정되어 있으며, 이를 위반할 경우 연간 매출액의 최대 4%에 해당하는 벌금이 부과됩니다. 중국은 디지털 추적 시스템을 통해 2025년까지 동력용 배터리의 65%를 재활용하도록 의무화하고 있으며, 한국은 2028년까지 80%를 회수하도록 의무화하고 있습니다. 따라서 자동차 제조업체는 역물류 네트워크 구축에 자금을 투자해야 합니다. 폭스바겐은 2025년 3월, 1,200곳의 판매점과 350곳의 제3자 시설을 통합하기 위해 2억 유로를 배정했습니다. 컴플라이언스 비용 증가로 인해 리튬이온 배터리 재활용 시장은 규모 확대와 수직 통합의 방향으로 나아가고 있습니다.

금속 가격 변동과 높은 역물류 비용

2024년 3월부터 2025년 12월까지 탄산리튬 가격이 85% 급락함에 따라 블랙마스 가격은 톤당 6,500달러까지 떨어졌으며, 일부 재활용 업체들은 마이너스 이익률에 몰리게 되었습니다. 역물류 비용은 톤당 150-250달러에 달할 전망입니다. 이는 배터리 팩이 UN 3480 규정에 따라 위험물로 분류되어 있어, 내화성 포장 및 충전 상태 검사가 의무화되어 있기 때문입니다. 이러한 구조적 비용은 금속 가격이 하락할 때마다 이익률을 압박합니다.

부문별 분석

2025년에는 자동차 배터리 팩이 매출의 63.8%를 차지했으나, 2015년부터 2020년 사이에 제조된 차량이 폐차됨에 따라 이 비율은 더욱 상승했습니다. 한편, 제조 스크랩은 즉시 공급량을 확보해 주며, 회수 과정의 병목 현상을 피할 수 있기 때문에 습식 제련 플랜트의 신속한 가동 확대를 가능하게 합니다. GM의 ‘Ultium’ 보증과 같은 OEM의 회수 프로그램은 소비자의 부담을 덜어줄 뿐만 아니라, 휴대용 전자기기보다 자동차용의 목표치가 더 높기 때문에 자원의 흐름은 더욱 차량용 배터리로 쏠리고 있습니다. 자동차용 리튬이온 배터리 재활용 시장 규모는 연평균 성장률(CAGR) 25.3%로 확대될 전망이지만, 소비자용 전자기기의 경우 수거 체계가 분산되어 있거나 ‘서랍 속에 방치된 채’ 있는 등의 상황으로 인해 성장세가 더딘 임베디드니다.

2025년 시점에서 제조 스크랩은 총 처리량의 불과 7%에 불과했으나, 직접 재활용 시범 사업을 뒷받침하는 안정적이고 화학 성분이 균일한 원료를 공급했습니다. 기가팩토리의 초기 수율률이 2022년 89%에서 2025년에는 96%로 향상됨에 따라, 이 공급원은 한계에 도달할 것입니다. 그렇긴 하지만, 스크랩 계약에 포함된 최소 수량 조항 덕분에 Umicore와 같은 재활용 업체의 경우 신규 생산 능력에 대한 투자 위험이 완화되고 있습니다.

NMC는 장거리 전기자동차 시장에서의 우위와 높은 코발트 함유량 덕분에 2025년에도 50.1%의 시장 점유율을 유지했으며, 이것이 우수한 경제성을 뒷받침하고 있습니다. LFP는 테슬라와 BYD가 표준 주행거리 차량에 이 화학 조성을 채택함에 따라 가장 빠르게 성장하고 있습니다. 그러나 코발트를 전혀 포함하지 않는 조성은 본질적인 가치를 떨어뜨려, NMC에 비해 블랙매스의 가격을 65%나 낮추고 있습니다. 따라서 재활용 업체들은 LFP 공급을 통해 이익을 얻기 위해 높은 처리 능력과 규제 상의 크레딧에 의존하고 있습니다.

LCO는 노트북이나 스마트폰 분야에서 여전히 수익성이 높지만, 기기의 소형화가 진행되면서 처리량은 정체 상태에 있습니다. NCA, LMO, LTO는 고성능 또는 장수명 용도에서 틈새 시장을 차지하고 있습니다. 중국이 LFP 리튬 회수율 요건을 70%에서 85%로 상향 조정하는 규정안을 마련한 것은 이러한 가치 격차를 해소하기 위한 것으로, LFP 재활용의 경제적 타당성을 더욱 확대할 가능성을 내포하고 있습니다.

지역별 분석

아시아태평양은 중국의 65% 재활용 의무화와 브룬프(Brunp)사의 12만 톤 처리 능력을 바탕으로, 2025년에는 전 세계 매출의 44.6%를 차지했습니다. 유럽은 노스볼트(Northvolt)사의 ‘Revolt’ 공장과 EU의 엄격한 배터리 규제 목표에 힘입어 28%의 점유율을 차지했습니다. 북미는 IRA(인플레이션 억제법)가 세액 공제를 재활용 함유율 기준치와 연계하고 있기 때문에 2031년까지의 연평균 성장률(CAGR) 전망치가 27.1%로 가장 높으며, 레드우드 머티리얼즈사의 100GWh 규모 양극재 생산 시설 등, 미국 에너지부(DOE)가 지원하는 프로젝트를 뒷받침하고 있습니다.

남미의 점유율은 4%에 그치지만, 리튬 자원이 풍부한 각국이 국내에서 재활용 시범 사업을 시작함에 따라 상승 추세를 보이고 있습니다. 중동 및 아프리카 시장 점유율은 3%이지만, 싱가포르에 거점을 둔 지역 허브와 걸프 연안 국가들의 태양광 발전 및 에너지 저장 설비를 결합한 시스템 도입과 관련된 인센티브를 통해 확대될 가능성이 있습니다. 일본과 인도는 각각 보조금 프로그램과 규정안을 발표하고 있지만, 상업적 전개는 아직 초기 단계에 머물러 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the lithium-ion battery recycling market size was valued at USD 4.33 billion in 2025 and is estimated to grow from USD 5.07 billion in 2026 to reach USD 14.79 billion by 2031, at a CAGR of 23.87% during the forecast period (2026-2031).

This report is Segmented by End-Of-Life Source (Automotive Batteries, and More), Battery Chemistry (NMC, and More), Recycling Technology (Hydrometallurgical, and More), Process Stage (Mechanical Shredding/Sorting, and More), Application of Recovered Materials (Battery-Grade Lithium Compound, and More), End-User Industry (Automotive, and More), and Geography (North America, Asia-Pacific, and More)

Global Lithium-ion Battery Recycling Market Trends and Insights

Accelerating wave of EV battery retirements

Early cohorts of mass-market EVs sold between 2015 and 2018 began hitting end-of-warranty in 2024-2025, sending an estimated 280,000 tonnes of packs into global collection systems. China's electric buses and taxis from the 2016-2018 subsidy boom are now retiring, while Europe's Nissan Leaf and Renault Zoe fleets move into recycling channels. The shift means recyclers can tap higher-value cobalt-rich packs instead of relying on lower-margin manufacturing scrap. Tesla reported that 92% of critical minerals in its 4680 cells can be recovered and looped back into new batteries, validating the economic case for closed loops. A subsequent surge in volumes is expected from 2027-2030 as vehicles sold in the 2019-2022 growth spurt reach retirement.

Tightening global EPR & EU Battery Regulation mandates

The EU Battery Regulation, effective February 2024, sets a 63% collection target by 2027 and 73% by 2030, underpinned by fines of up to 4% of annual turnover for non-compliance. China mandates 65% recycling of power batteries by 2025 through a digital traceability system, and South Korea requires 80% collection by 2028. Automakers, therefore, must finance reverse logistics networks; Volkswagen allocated EUR 200 million in March 2025 to integrate 1,200 dealerships and 350 third-party sites. Compliance costs are driving the lithium-ion battery recycling market toward scale and vertical integration.

Volatile Metal Prices & High Reverse-Logistics Costs

Lithium carbonate's 85% crash between March 2024 and December 2025 dragged black-mass prices down to USD 6,500 per tonne, forcing some recyclers into negative margins. Reverse-logistics costs range from USD 150-250 per tonne because packs are hazmat-classified under UN 3480 rules that require fire-resistant packaging and state-of-charge testing. These structural costs compress margins whenever metals fall.

Other drivers and restraints analyzed in the detailed report include:

- Raw-Material Price Inflation Spurring Closed-Loop Supply Chains

- Step-change yields from next-generation hydro & direct recycling

- Regional Over-Capacity Creating Feedstock Scarcity Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automotive packs accounted for 63.8% of revenue in 2025, a figure expected to rise as the 2015-2020 vehicle cohort retires. Manufacturing scrap, however, supplies immediate volume, sidestepping collection bottlenecks and enabling rapid ramp-up of hydrometallurgical plants. OEM take-back programs such as GM's Ultium warranty eliminate consumer friction, and higher targets for automotive than portable electronics further tilt flows toward vehicle batteries. The lithium-ion battery recycling market size for automotive sources is set to expand at a 25.3% CAGR, while consumer electronics lags due to fragmented collection and "drawer hoarding."

Manufacturing scrap represented only 7% of tonnage in 2025 but supplied steady, chemistry-homogeneous feedstock that supports direct recycling pilots. As the gigafactories' first-pass yields improve from 89% in 2022 to 96% in 2025, this stream will plateau; nonetheless, minimum-volume clauses in scrap contracts de-risk new capacity investments for recyclers like Umicore.

NMC held a 50.1% share in 2025 thanks to its dominance in long-range EVs and high cobalt content, which sustains favorable economics. LFP is growing fastest as Tesla and BYD deploy the chemistry in standard-range vehicles; however, its zero-cobalt composition erodes intrinsic value, lowering black-mass pricing by 65% relative to NMC. Recyclers, therefore, rely on high throughput and regulatory credits to profit from LFP streams.

LCO remains lucrative in laptops and smartphones, but shrinking device footprints cap tonnage. NCA, LMO, and LTO fill niche roles in high-performance or long-cycle applications. China's draft rule raising the required lithium recovery for LFP from 70% to 85% aims to close the value gap, potentially unlocking a broader economic case for LFP recycling.

Geography Analysis

Asia-Pacific generated 44.6% of global revenue in 2025, buoyed by China's 65% recycling mandate and Brunp's 120,000-tonne capacity. Europe held a 28% share, anchored by Northvolt's Revolt plant and strict EU Battery Regulation targets. North America posted the highest 27.1% CAGR forecast through 2031 as the IRA links tax credits to recycled content thresholds, catalyzing DOE-backed projects such as Redwood Materials' 100 GWh cathode facility.

South America's share sits at 4% but is rising as lithium-rich nations launch domestic recycling pilots. The Middle East and Africa claim 3% but may expand through regional hubs in Singapore and incentives tied to solar-plus-storage installations in Gulf states. Japan and India have announced subsidy programs and draft rules, respectively, yet commercial deployments remain early-stage.

- Umicore SA

- Glencore PLC

- Brunp Recycling (CATL)

- GEM Co., Ltd.

- Li-Cycle Holdings Corp.

- Redwood Materials Inc.

- Ascend Elements (Battery Resources)

- Ecobat

- American Battery Technology Co. (ABTC)

- RecycLiCo Battery Materials

- Retriev Technologies Inc.

- Cirba Solutions

- Duesenfeld GmbH

- TES-AMM Pte Ltd.

- Recupyl SAS

- Raw Materials Company Inc.

- Glencore-Li-Cycle Portovesme JV

- Ganfeng Lithium Co., Ltd.

- Eramet-Suez JV (Recyclage Batteries)

- InoBat-Minerals JV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating wave of EV battery retirements

- 4.2.2 Tightening global EPR & EU Battery Regulation mandates

- 4.2.3 Raw-material price inflation spurring closed-loop supply chains

- 4.2.4 Step-change yields from next-gen hydro & direct recycling

- 4.2.5 OEM design-for-recycling battery packs reducing dismantling cost

- 4.2.6 Emergence of liquid "black-mass" spot markets

- 4.3 Market Restraints

- 4.3.1 Volatile metal prices & high reverse-logistics costs

- 4.3.2 Safety & haz-mat compliance in high-voltage collection

- 4.3.3 Regional over-capacity creating feedstock scarcity risk

- 4.3.4 Low intrinsic value of LFP chemistries

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By End-of-Life Source

- 5.1.1 Automotive Batteries

- 5.1.2 Consumer Electronics Batteries

- 5.1.3 Industrial and ESS Batteries

- 5.1.4 Manufacturing Scrap

- 5.2 By Battery Chemistry

- 5.2.1 Lithium Cobalt Oxide (LCO)

- 5.2.2 Lithium Iron Phosphate (LFP)

- 5.2.3 Lithium Nickel Manganese Cobalt (NMC)

- 5.2.4 Lithium Nickel Cobalt Aluminium (NCA)

- 5.2.5 Lithium Manganese Oxide (LMO)

- 5.2.6 Lithium Titanate (LTO)

- 5.3 By Recycling Technology

- 5.3.1 Hydrometallurgical

- 5.3.2 Pyrometallurgical

- 5.3.3 Direct/Mechanical

- 5.3.4 Hybrid and Emerging (Bio/ Electro-chemical)

- 5.4 By Process Stage

- 5.4.1 Collection and Logistics

- 5.4.2 Dismantling and Discharge

- 5.4.3 Mechanical Shredding/Sorting

- 5.4.4 Black-Mass Production

- 5.4.5 Material Refining and Recovery

- 5.5 By Application of Recovered Materials

- 5.5.1 Cathode Active Materials

- 5.5.2 Anode/Graphite

- 5.5.3 Battery-grade Lithium Compounds

- 5.5.4 Cobalt and Nickel Salts

- 5.5.5 Manganese

- 5.5.6 Others (Cu, Al)

- 5.6 By End-user Industry

- 5.6.1 Automotive

- 5.6.2 Marine

- 5.6.3 Power and Energy Storage

- 5.6.4 Consumer Electronics

- 5.6.5 Others

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 Germany

- 5.7.2.3 France

- 5.7.2.4 Spain

- 5.7.2.5 NORDIC Countries

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 ASEAN Countries

- 5.7.3.6 Australia and New Zealand

- 5.7.3.7 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Colombia

- 5.7.4.4 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 South Africa

- 5.7.5.4 Egypt

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Umicore SA

- 6.4.2 Glencore PLC

- 6.4.3 Brunp Recycling (CATL)

- 6.4.4 GEM Co., Ltd.

- 6.4.5 Li-Cycle Holdings Corp.

- 6.4.6 Redwood Materials Inc.

- 6.4.7 Ascend Elements (Battery Resources)

- 6.4.8 Ecobat

- 6.4.9 American Battery Technology Co. (ABTC)

- 6.4.10 RecycLiCo Battery Materials

- 6.4.11 Retriev Technologies Inc.

- 6.4.12 Cirba Solutions

- 6.4.13 Duesenfeld GmbH

- 6.4.14 TES-AMM Pte Ltd.

- 6.4.15 Recupyl SAS

- 6.4.16 Raw Materials Company Inc.

- 6.4.17 Glencore-Li-Cycle Portovesme JV

- 6.4.18 Ganfeng Lithium Co., Ltd.

- 6.4.19 Eramet-Suez JV (Recyclage Batteries)

- 6.4.20 InoBat-Minerals JV

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment