|

시장보고서

상품코드

2066508

항공우주용 코팅 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Aerospace Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

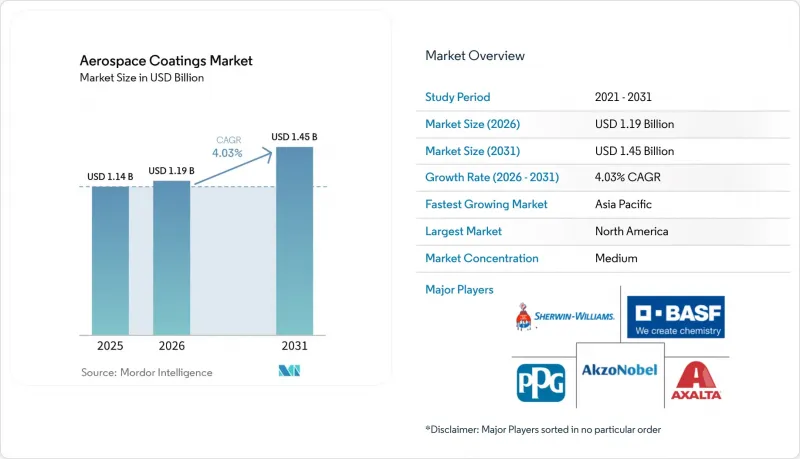

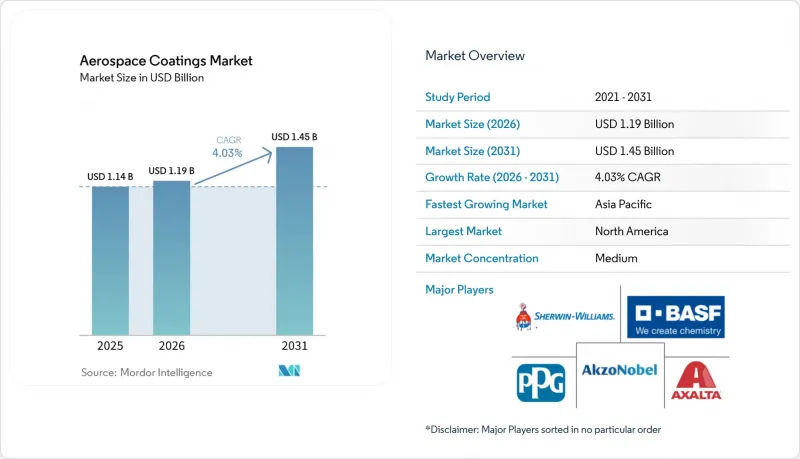

Mordor Intelligence에 의하면, 항공우주용 코팅 시장 규모는 2025년에 11억 4,000만 달러로 평가되었고, 2026년에 11억 9,000만 달러로 추정되고, 2031년까지 14억 5,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 4.03%로 성장할 전망입니다.

본 보고서는 수지 유형별(에폭시, 폴리우레탄, 아크릴, 기타 수지), 기술별(용제형, 수성, 기타 기술), 최종 사용자별(OEM 및 MRO), 항공기 유형별(민간, 군용, 일반), 지역별(아시아태평양, 북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 항공우주용 코팅 시장 동향 및 인사이트

민간 항공기 생산 대수 증가

2025년, 737 MAX와 A320neo와 같은 단일 통로형 항공기 시리즈는 월평균으로 높은 기체 완성률을 기록했습니다. 에어버스사가 올해 상당한 수량의 납품을 예상하고 있는 만큼, 생산성 향상은 밑칠 도료 및 마감 도료 수요 증가로 이어질 것입니다. 이는 와이드바디 항공기가 나로우바디 항공기에 비해 더 넓은 도장 면적이 필요하기 때문입니다. 그러나 특히 티타늄 단조 제품 및 복합재 프리프레그 분야 공급망 문제가 여전히 지속되고 있어, 일부 도장 부스의 예약이 연기된 결과, 매출 인식이 하반기 분기로 미뤄지는 상황이 발생하고 있습니다. 이에 대한 대책으로, 기존 스프레이 라인은 2교대제로 가동되고 있습니다. 이는 리드타임이 18-24개월 소요되는 새로운 자동 도장 부스가 가동될 때까지의 임시 조치입니다. 또한, 처리량의 급증에 따라, 특히 인라인 색상 조정 및 두께 모니터링과 같은 분야에서 품질 보증에 대한 수요가 높아지고 있습니다.

항공기 제조에서 복합재료의 사용 확대

현재 보잉 787과 에어버스 A350의 중량 중 상당 부분을 탄소섬유 구조가 차지하고 있으며, 기존의 알루미늄 동체에 비해 중량이 현저히 증가했습니다. 현재 표준으로 자리 잡은 에폭시 프라이머에는 크롬산염을 포함하지 않는 억제제가 사용되고 있습니다. 이러한 프라이머는 하이드록실기를 풍부하게 함유한 섬유 표면과 효과적으로 결합하는 동시에, 갈바닉 부식을 방지할 수 있습니다. 배합 설계자는 요구되는 기준을 충족하기 위해 트리아졸계 및 희토류 첨가제를 배합에 포함시키고 있습니다. 표면 저항률을 낮게 유지하는 전도성 탑코트는 재료 비용을 증가시키지만, 낙뢰 시 방전에 있어서는 필수적입니다. 오토클레이브를 이용한 가열 과정 없이 실온에서 경화되는 에폭시 수지는 사용 중인 복합재료의 수리를 한층 더 용이하게 합니다. 다만, 현재 FAA(미국 연방항공청)의 승인을 받은 공급업체는 극히 일부에 불과하다는 점에 유의해야 합니다.

휘발성 유기 화합물(VOC) 배출에 대한 우려

미국에서는 프라이머 및 탑코트에 포함된 휘발성 유기 화합물(VOC)의 함량이 제한되어 있습니다. 유럽연합(EU)도 2028년까지 이와 유사한 제한 조치를 도입할 예정입니다. 이러한 기준을 준수하기 위해서는 배합 설계자가 증발 속도가 느린 용매로 전환해야 하므로, 원자재 비용이 증가합니다. 그 결과, 도장 공장의 사이클 타임이 길어지며, 처리 능력 저하로 이어집니다. 수성 도료라면 이러한 규제를 더 쉽게 충족할 수 있지만, 습도가 관리되는 작업실이 필요하고 폐수량도 증가하기 때문에 소규모 정비 업체에게는 과제가 됩니다. 이러한 재정적 장벽이 통합 추세를 부추기고 있으며, 더 견실한 현금 흐름을 보유한 대규모 MRO 사업자가 유리한 입장에 있습니다.

부문별 분석

2025년 기준으로 에폭시는 항공우주용 코팅 시장 점유율의 58.36%를 차지했으며, 이 부문은 2031년까지 연평균 성장률(CAGR) 4.22%를 나타낼 것으로 예측됩니다. 이는 특히 복합재료를 많이 사용한 기체에서 꾸준한 수요가 있음을 보여줍니다. 2위를 차지한 폴리우레탄은 자외선 안정성이 뛰어난 탑코트를 필요로 하는 항공사들에게 최우선 선택지로 자리 잡고 있습니다. 다만, 공급업체들이 광안정제 패키지를 배합함에 따라 이러한 원자재의 가격이 상승 추세를 보이고 있다는 점은 주목할 만합니다.

유전 특성으로 높은 평가를 받고 있는 아크릴 계열은 특수 레이돔의 틈새 시장을 공략하고 있습니다. 그러나 내화학성이 제한적이기 때문에 보다 광범위한 도입에는 제약이 있습니다. 한편, 실리콘 및 불소 수지 분야에서는 성장세가 주춤하고 있습니다. 이는 주로 OEM 인증 획득에 어려움을 초래하는 새로운 PFAS 규제의 도입에 기인한 것입니다. 게다가, 종종 수년에 달하는 긴 인증 기간 또한 혁신적인 신규 시장 진출기업들에게 장벽이 되고 있습니다. 그 결과, 적어도 다음 규제 주기가 시작될 때까지는 기존의 수지 계층 구조가 확고하게 유지될 전망입니다.

용제 기반 기술은 군용기 및 기존 협폭기 분야에서 쌓아온 실적을 바탕으로, 2025년에는 매출의 54.41%를 차지했습니다. 수성 시스템은 부스 내 공기를 연소시키지 않고도 점점 강화되는 배출 규제를 충족할 수 있기 때문에 2031년까지 연평균 성장률(CAGR) 4.18%로 성장하고 있습니다.

도입에 대한 장벽은 여전히 남아 있습니다. 수성 도막은 습도가 높은 환경에서는 경화되는 데 시간이 오래 걸리며, 불필요한 폐수를 발생시킵니다. 분체 도장은 180°C에서 소성하는 과정이 복합재료의 채택을 방해하기 때문에 여전히 착륙 장치나 객실 부품에 한정되어 있습니다. 수십년전부터 이어져 온 MIL-PRF 규격은 최소 수요 기준을 보장하고 있으며, 이를 통해 용제계 도료가 급속히 대체되는 것을 막고 있습니다.

지역별 분석

2025년, 북미는 매출의 40.05%를 차지했습니다. 이는 워싱턴주에 위치한 보잉사의 조립 거점과 광범위한 기존 MRO(정비·수리·오버홀) 부문을 반영한 것입니다. 그러나 국내 인건비가 높기 때문에 각 항공사들은 대규모 도장 작업을 위해 제트기를 아시아로 운송하는 경향이 있어, 이 지역의 판매량 증가를 억제하고 있습니다. 유럽은 툴루즈와 함부르크에 위치한 에어버스사의 최종 조립 라인은 물론, 기술 혁신을 촉진하는 엄격한 배출 규제의 덕분에 2위 자리를 차지하고 있습니다.

아시아태평양은 중국과 인도의 제조업 주도 전략, 그리고 세계적 물류 허브로서의 역할에 힘입어 연평균 성장률(CAGR) 3.22%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. COMAC은 현지 조달을 목표로 하고 있지만, 국내 공급업체가 FAA 또는 EASA의 승인을 획득할 때까지는 필수적인 에폭시 프라이머를 계속 수입하고 있습니다. 한편, 중동에는 와이드바디 항공기를 운항하는 항공사가 밀집해 있어 코팅, 특히 사막 기후에서 필수적인 자외선 내성 탑코트에 대한 수요가 증가하고 있습니다.

관세 제도와 환율 변동은 신흥 시장에서의 조달 결정에 영향을 미칩니다. 예를 들어, 브라질 레알의 가치 하락은 수입 수지의 원가를 상승시켜, 다른 지역의 규제 압력에도 불구하고 검증된 용제형 시스템에 대한 의존을 장기화시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the aerospace coatings market size is projected to be USD 1.14 billion in 2025, USD 1.19 billion in 2026, and reach USD 1.45 billion by 2031, growing at a CAGR of 4.03% from 2026 to 2031.

This report is Segmented by Resin Type (Epoxy, Polyurethane, Acrylic, and Other Resin Types), Technology (Solvent-Borne, Water-Borne, and Other Technologies), End User (Original Equipment Manufacturer and Maintenance Repair and Operations), Aviation Type (Commercial, Military, and General), and Geography (Asia-Pacific, North America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Aerospace Coatings Market Trends and Insights

Rising Production Rates of Commercial Aircraft

In 2025, families like the 737 MAX and A320neo, both single-aisle aircraft, averaged high monthly airframe completion rates. With Airbus projecting a significant number of deliveries for the year, the uptick in build rates translates to heightened volumes of primer and topcoat. This is due to wide-body aircraft requiring more surface coverage compared to their narrow-body counterparts. However, ongoing supply-chain challenges, particularly in titanium forgings and composite prepregs, have led to deferrals in some paint-booth slots, resulting in delayed recognition into later quarters. As a workaround, existing spray lines are operating on dual shifts. This is a temporary measure until the new automated booths, which come with lead times of 18 to 24 months, become operational. Furthermore, the surge in throughput amplifies the demand for quality assurance, especially in areas like in-line color matching and film thickness monitoring.

Increasing Use of Composites in Aircraft Manufacturing

Carbon-fiber structures now make up a significant portion of the weight in Boeing's 787 and Airbus's A350, a notable increase from older aluminum fuselages. Epoxy primers, now standard, utilize chromate-free inhibitors. These primers effectively bond with hydroxyl-rich fiber surfaces while steering clear of galvanic corrosion. Formulators incorporate triazole and rare-earth additives to meet required benchmarks. While conductive top coats, which ensure surface resistivity stays low, add to material costs, they're essential for lightning-strike dissipation. Room-temperature-cure epoxy, which bonds without the need for autoclave heat, further enhances composite repairs in service. However, it's worth noting that only a select few suppliers possess current FAA approvals.

Concerns of Volatile Organic Compound Emissions

U.S. regulations limit primer volatile-organic-compound content and top coats. The European Union plans to implement these same limits by 2028. Adhering to these standards increases raw material costs as formulators shift to slower-evaporating solvents. Consequently, paint-shop cycle times extend, leading to reduced throughput. While water-borne alternatives can more readily meet these regulations, they require humidity-controlled booths, which produce higher wastewater loads, posing a challenge for smaller maintenance operations. This financial hurdle is driving a trend of consolidation, favoring larger MRO houses with more robust cash flows.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for Air Travel

- Accelerating Maintenance, Repair and Overhaul Demand for Aging Fleets

- Lengthy Certification Cycles for New Chemistries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy held 58.36% of the aerospace coatings market share in 2025, and the segment is expected to grow at a 4.22% CAGR to 2031, underscoring a robust demand, particularly in composite-rich fuselages. Polyurethanes, securing the second position, are the top choice for airlines seeking ultraviolet-stable top coats. However, it's worth noting that as suppliers incorporate light-stabilizer packages, the prices of these raw materials are on the rise.

Acrylics, prized for their dielectric properties, cater to specialty radome niches. Yet, their limited chemical resistance curtails wider adoption. Meanwhile, the silicone and fluoropolymer families are experiencing sluggish growth. This is largely due to emerging PFAS restrictions, which pose challenges for OEM qualification. Furthermore, the lengthy certification timelines, often spanning several years, act as a deterrent for disruptive newcomers. As a result, the existing resin hierarchies remain firmly entrenched, at least until the next regulatory cycle.

Solvent technologies accounted for 54.41% of revenue in 2025, supported by established performance records on military fleets and legacy narrow-body lines. Water-borne systems are advancing at a 4.18% CAGR through 2031 because they meet evolving emission limits without booth-air incineration.

Adoption hurdles linger. Water-borne films cure more slowly in high humidity and produce extra wastewater. Powder coating stays confined to landing-gear and cabin parts because the 180 °C bake impeded composites. MIL-PRF specifications that date back decades ensure a baseline of demand that shields solvent chemistries from rapid displacement.

Geography Analysis

North America supplied 40.05% of revenue in 2025, reflecting Boeing assembly in Washington State and an extensive legacy MRO sector. Domestic labor rates, however, motivate carriers to ferry jets to Asia for heavy paint work, tempering volume growth in the region. Europe holds the second-largest position thanks to Airbus' final-assembly lines in Toulouse and Hamburg and to aggressive emission rules that push technical innovation.

Asia-Pacific is the fastest-expanding region at 3.22% CAGR, driven by Chinese and Indian manufacturing initiatives and by its role as a global transit hub. COMAC aims for local content but continues to import essential epoxy primers until domestic suppliers obtain FAA or EASA approvals. However, the Middle East's high concentration of wide-body operators bolsters the demand for coatings, particularly ultraviolet-resistant top coats essential for desert climates.

Tariff regimes and currency swings influence procurement decisions in emerging markets. Brazilian real depreciation, for instance, raises imported resin costs and prolongs reliance on proven solvent-borne systems despite regulatory pressure elsewhere.

- Advanced Deposition & Coating Technologies, Inc.

- Akzo Nobel N.V.

- Axalta Coating Systems, LLC

- BASF SE

- BryCoat Inc.

- Henkel AG & Co. KGaA

- Hentzen Coatings, Inc.

- Ionbond

- Jotun

- Mankiewicz Gebr. & Co.

- PPG Industries, Inc.

- Socomore

- The Sherwin-Williams Company

- Zircotec

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising production rates of commercial aircraft

- 4.2.2 Increasing use of composites in aircraft manufacturing

- 4.2.3 Increasing Demand for Air Travel

- 4.2.4 Accelerating Mainenance, Reapir and Overhaul demand for aging fleets

- 4.2.5 Increase in Manufacturing of Aircrafts in Emerging Economies

- 4.3 Market Restraints

- 4.3.1 Concerns of VOC emissions

- 4.3.2 Lengthy certification cycles for new chemistries

- 4.3.3 Early substitution risk from next-gen fluoropolymer films

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Polyurethane

- 5.1.3 Acrylic

- 5.1.4 Other Resin Types (Silicone, Fluoropolymer, etc.)

- 5.2 By Technology

- 5.2.1 Solvent-borne

- 5.2.2 Water-borne

- 5.2.3 Other Technologies (Powder,etc.)

- 5.3 By End User

- 5.3.1 Original Equipment Manufacturer (OEM)

- 5.3.2 Maintenance, Repair and Operations (MRO)

- 5.4 By Aviation Type

- 5.4.1 Commercial Aviation

- 5.4.2 Military Aviation

- 5.4.3 General Aviation

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information,Products and Services, and Recent Developments)

- 6.4.1 Advanced Deposition & Coating Technologies, Inc.

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Axalta Coating Systems, LLC

- 6.4.4 BASF SE

- 6.4.5 BryCoat Inc.

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Hentzen Coatings, Inc.

- 6.4.8 Ionbond

- 6.4.9 Jotun

- 6.4.10 Mankiewicz Gebr. & Co.

- 6.4.11 PPG Industries, Inc.

- 6.4.12 Socomore

- 6.4.13 The Sherwin-Williams Company

- 6.4.14 Zircotec

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment