|

시장보고서

상품코드

2066528

소프트웨어 정의 광역 네트워크 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Software-Defined Wide Area Network - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

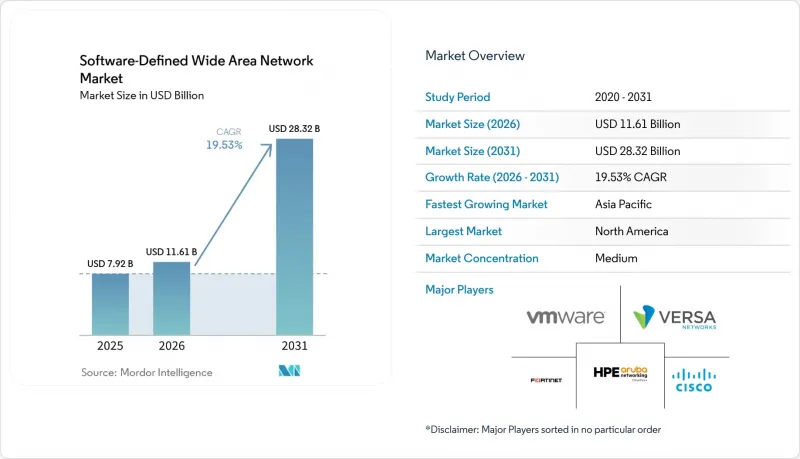

Mordor Intelligence에 의하면, 소프트웨어 정의 광역 네트워크(SD-WAN) 시장 규모는 2025년 79억 2,000만 달러에서 2026년에는 116억 1,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 19.53%로 성장을 지속하여, 2031년에는 283억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 도입 형태(On-Premise, 클라우드, 하이브리드), 구성 요소(솔루션 및 서비스), 조직 규모(대기업 및 중소기업), 최종 사용 산업(의료, 은행, 금융서비스 및 보험(BFSI), 소매·소비자 서비스, 제조, 운송 및 물류, IT 및 통신) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 소프트웨어 정의 광역 네트워크(SD-WAN) 시장 동향 및 인사이트

클라우드 기반 용도의 폭발적인 증가

2025년까지 기업 워크로드의 약 65%가 퍼블릭 클라우드 또는 하이브리드 클라우드 플랫폼으로 이전됨에 따라, 허브 앤 스포크형 WAN 토폴로지의 지연 문제가 두드러지게 나타났습니다. SD-WAN 오버레이를 통해 지사 거점에서 인터넷에 직접 연결할 수 있게 되었으며, Microsoft 365, Dynamics 365 및 기타 SaaS 제품군의 용도 응답 시간이 몇 초 단축되었습니다. SD-WAN 게이트웨이와 통합된 Azure ExpressRoute 포트는 전년 대비 43% 증가했으며, 이는 확정적인 클라우드 경로에 대한 수요가 증가하고 있음을 보여줍니다. Amazon Web Services, Google Cloud, Oracle Cloud에 걸친 멀티 클라우드 전략으로 인해 동적 경로 제어의 필요성이 더욱 커지고 있습니다. 기업 측에서는 도입 후 페이지 로딩 속도가 최대 40% 향상되었습니다는 보고가 있었으며, 네트워크 성능이 경쟁상의 차별화 요소로 작용하고 있습니다.

하이브리드/원격 근무가 가져오는 WAN의 민첩성

2025년에는 주 3일 이상 원격 근무를 하는 직원의 비율이 38%로 안정화되었으며, 하이브리드 근무 방식이 영구적인 운영 모델로 자리 잡았습니다. 통합형 방화벽, 침입 방지 기능, 보안 웹 게이트웨이를 갖춘 SD-WAN 플랫폼은 본사에서 재택 사무실에 이르기까지 일관된 보안 체계를 구축합니다. 시스코는 고객이 개별 도구를 통합된 정책으로 통합한 결과, 2025년에 Meraki SD-WAN 구독 건수가 31% 증가했습니다. 사용자의 신원, 기기의 상태, 용도의 컨텍스트를 지속적으로 검증하는 제로 트러스트 프레임워크는 특히 엄격한 지연 요건이나 규정 준수 요건이 요구되는 금융 서비스 업계에서 그 도입이 더욱 가속화되고 있습니다.

데이터 플레인의 보안과 제어 플레인의 공격 표면

클라우드 호스팅형 SD-WAN 컨트롤러는 오케스트레이션을 일원화하기 때문에 고가치 표적이 됩니다. 2025년 3월 미국 사이버보안 및 인프라 보안국(CISA)이 발표한 권고안에서는 해킹당한 컨트롤러가 트래픽을 우회하거나, 암호화를 무력화하거나, 악성 광고를 삽입할 가능성이 있다고 경고했습니다. Black Hat에서 시연된 개념 증명(PoC) 공격을 통해, 설정 오류가 있는 API가 공격자에게 토폴로지 맵이나 키를 제공해 버린다는 사실이 밝혀졌습니다. 의료 및 국방 등 규제 대상 분야에서는 FedRAMP 및 HIPAA 감사 결과가 나올 때까지 도입이 주춤하고 있는 반면, 도입 기업에서는 제어 평면의 트래픽을 세분화하고 다단계 인증을 의무화하고 있어 도입 일정이 장기화되고 있습니다.

부문별 분석

2025년에는 On-Premise 구축이 가장 큰 비중을 차지하여 SD-WAN 시장의 42.50%를 차지했습니다. 규제가 엄격한 조직은 자사 데이터센터 내에 설치된 어플라이언스 기반의 제어 플레인을 중시하고 있으며, 이는 GDPR(EU 개인정보보호규정) 및 HIPAA의 주권 관련 규정에 부합하는 것입니다. 한편, 클라우드 도입은 설비 투자를 피하려는 중견 기업들의 주도 하에 연평균 성장률(CAGR) 25.50%로 확대될 것으로 전망됩니다. 클라우드 도입과 관련된 SD-WAN 시장 규모는 2026년 49억 4,000만 달러에서 2031년까지 154억 달러로 확대될 것으로 예측되며, 이는 ‘소비 중심 경제’로의 전환을 여실히 보여주고 있습니다.

하이브리드 아키텍처는 On-Premise의 주권과 클라우드의 확장성을 결합합니다. VMware의 보고서에 따르면, 2025년에 이 기술을 도입한 기업의 58%가 하이브리드 설계를 선택했으며, 그 이유로 성능이 중요한 워크로드는 On-Premise에 남겨두면서 원격지 지점에서는 SaaS 기반 오케스트레이션을 활용하고 있다는 점이 꼽히고 있습니다(2). SASE 통합이 가속화되는 가운데, 클라우드 네이티브 컨트롤러가 보안 서비스를 내장함으로써 보수적인 업계조차도 하이브리드 도입을 촉진하고 있습니다. SD-WAN 시장은 현재 아키텍처 결정에 있어 하드웨어 소유권이 아닌 도입의 유연성이 중요한 요소임을 거듭 보여주고 있습니다.

2025년, 솔루션 부문은 가상 어플라이언스, 영구 라이선스, 오케스트레이션 콘솔을 포함해 매출 점유율 54.60%를 유지했습니다. 그러나 통합에 대한 수요가 증가함에 따라 예산이 서비스 분야로 이동하고 있으며, 서비스 분야는 연평균 성장률(CAGR) 21.16%를 나타낼 것으로 예측됩니다. 딜로이트의 조사에 따르면, 사내 전문 지식 부족을 배경으로 기업의 47%가 SD-WAN 운영을 적어도 일부는 아웃소싱하고 있는 것으로 나타났습니다.

전문 서비스에는 평가, 설계, 개념 검증(PoC)이 포함됩니다. 한편, 매니지드 서비스에서는 전송, 보안, 모니터링이 예측 가능한 운영 비용(OPEX)으로 제공됩니다. 액센츄어(Accenture)나 타타 컨설팅 서비스(TCS)와 같은 시스템 통합 업체들은 현재 멀티 벤더를 지원하는 SD-WAN 센터 오브 엑설런스를 운영하고 있어, 오버레이에 대한 락인 우려를 완화하고 있습니다. AI 기반 분석 기술이 성숙해짐에 따라, 서비스 제공업체들은 정책 추천을 자동화하여 차별화를 꾀하고 있으며, SD-WAN 시장이 라이프사이클 파트너십으로 점차 전환되는 추세가 더욱 뚜렷해지고 있습니다.

지역별 분석

북미는 클라우드의 조기 도입, 풍부한 광대역 환경, 그리고 적극적인 SASE 실증 실험을 통해 2025년 매출의 41.20%를 차지했습니다. 미국 연방통신위원회(FCC)의 보고서에 따르면, 2025년에는 기업 거점의 92%가 기가비트 인터넷에 접속하게 될 것이며, 이를 통해 오버레이 네트워크가 저비용 회선을 통합하여 MPLS 수준의 신뢰성을 실현할 수 있게 되었습니다. 뉴욕과 샬럿의 금융 서비스 거점, 보스턴과 휴스턴의 의료 시스템, 실리콘밸리의 기술 클러스터가 어우러져 통합된 네트워크 보안 스택에 대한 수요를 견인했습니다. 캐나다 기업들은 광범위한 지리적 분산이라는 과제에 직면해 있는 반면, 미국 국경 인근의 멕시코 제조업체들은 인더스트리 4.0 이니셔티브를 지원하기 위해 SD-WAN을 활용하고 있습니다.

아시아태평양은 인도의 12억 달러 규모의 ‘디지털 인디아’ 프로그램, 중국의 스마트 제조 추진, 그리고 아세안(ASEAN)의 전자상거래 붐에 힘입어 2031년까지 연평균 성장률(CAGR) 29.90%라는 가장 빠른 성장세를 기록할 것으로 전망됩니다. 일본, 한국, 호주에서 도입이 진행 중인 독립형 5G 코어 네트워크는 SD-WAN을 통한 오케스트레이션과 시너지 효과를 발휘하는 네트워크 슬라이싱 시범 프로젝트를 촉진하고 있습니다. 인도네시아에서 베트남에 이르는 신흥 시장에서는 SD-WAN을 활용하여 고가의 MPLS 인프라를 피하고, 국경을 초월한 디지털 무역을 지원하고 있습니다.

유럽의 동향은 기밀성이 높은 데이터를 On-Premise에 보관하는 하이브리드 아키텍처를 권장하는 GDPR(EU 개인정보보호규정)의 데이터 거주 요건에 의해 형성되고 있습니다. 독일의 한 대형 자동차 제조업체는 공장과 엔지니어링 센터를 연계하고, 영국의 한 은행은 SD-WAN과 제로 트러스트를 통합하여 고부가가치 거래 흐름을 보호하고 있습니다. 프랑스와 독일의 통신 사업자들은 2025년, 네트워크 담당 인력이 부족한 중견 기업을 대상으로 번들형 매니지드 서비스를 시작했습니다. 중동 국가들, 특히 사우디아라비아와 아랍에미리트(UAE) 정부는 국가 디지털 전략에 SD-WAN을 포함시키고 있는 반면, 아프리카에서는 남아프리카공화국과 나이지리아가 도입을 주도하고 있습니다. 남미에서는 브라질과 아르헨티나가 전자상거래 및 하이브리드 근무를 유지하기 위해 SD-WAN 오버레이를 통해 프레임 릴레이 환경을 현대화하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

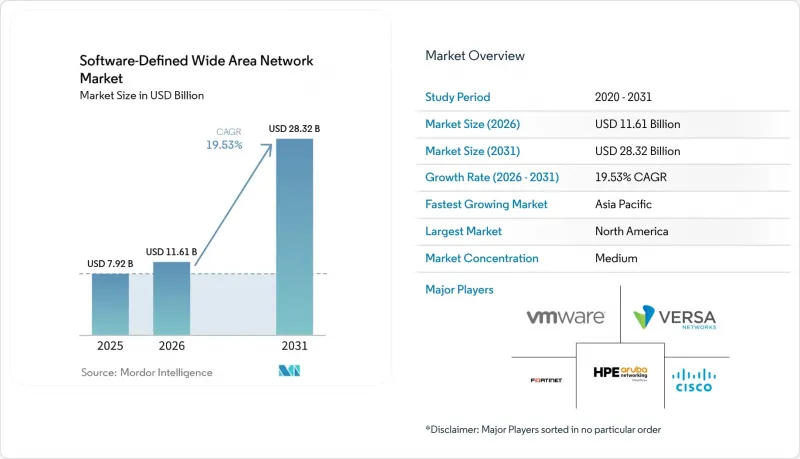

JHS 26.06.29According to Mordor Intelligence, the software-Defined wide area network market size is expected to grow from USD 7.92 billion in 2025 to USD 11.61 billion in 2026 and is forecast to reach USD 28.32 billion by 2031 at 19.53% CAGR over 2026-2031.

This report is Segmented by Deployment Mode (Premise, Cloud, and Hybrid), Component (Solutions and Services), Organization Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (Healthcare, BFSI, Retail and Consumer Services, Manufacturing, Transport and Logistics, and IT and Telecom), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Software-Defined Wide Area Network Market Trends and Insights

Cloud-centric Application Explosion

Nearly 65% of enterprise workloads had shifted to public or hybrid cloud platforms by 2025, exposing the latency penalties of hub-and-spoke WAN topologies. SD-WAN overlays enable direct internet breakout at branch locations, shaving seconds off application response times for Microsoft 365, Dynamics 365, and other SaaS suites. Azure ExpressRoute ports integrated with SD-WAN gateways grew 43% year over year, illustrating demand for deterministic cloud paths. Multi-cloud strategies spanning Amazon Web Services, Google Cloud, and Oracle Cloud intensify the need for dynamic path steering. Enterprises report up to 40% faster page loads after deployment, turning network performance into a competitive differentiator.

Hybrid/Remote-work-driven WAN Agility

Remote employees working three or more days off-site stabilized at 38% in 2025, cementing hybrid work as a permanent operating model. SD-WAN platforms equipped with integrated firewalls, intrusion prevention, and secure web gateways enforce uniform security posture from headquarters to home offices. Cisco recorded 31% growth in Meraki SD-WAN subscriptions during 2025 as customers consolidated point tools into unified policies. Zero-trust frameworks that continuously verify user identity, device posture, and application context further amplify adoption, especially in financial services with stringent latency and compliance needs.

Data-Plane Security and Control-Plane Attack Surface

Cloud-hosted SD-WAN controllers centralize orchestration, creating high-value targets. A March 2025 advisory from the U.S. Cybersecurity and Infrastructure Security Agency warned that compromised controllers could reroute traffic, disable encryption, or inject malicious advertisements. Proof-of-concept exploits demonstrated at Black Hat exposed misconfigured APIs granting attackers topology maps and keys. Regulated sectors such as healthcare and defense slowed rollouts pending FedRAMP and HIPAA audits, while adopters segment control-plane traffic and require multi-factor authentication, extending deployment timelines.

Other drivers and restraints analyzed in the detailed report include:

- MPLS Cost-out and Bandwidth Optimisation

- 5G Network Slicing and SD-WAN Convergence

- Shortage of SD-WAN Architecture Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises deployments held the largest 2025 position, capturing 42.50% of the SD-WAN market. Heavily regulated entities valued appliance-based control planes residing in owned data centers, aligning with GDPR and HIPAA sovereignty rules. Conversely, cloud deployments are forecast to climb at a 25.50% CAGR, propelled by mid-sized enterprises sidestepping capital purchases. The SD-WAN market size for cloud implementations is projected to expand from USD 4.94 billion in 2026 to USD 15.4 billion by 2031, underscoring the pivot toward consumption economics.

Hybrid architecture blends on-premises sovereignty with cloud scalability. VMware reported that 58% of 2025 adopters chose hybrid designs, citing performance-critical workloads that remain on-site while remote branches leverage SaaS-based orchestration[2]. As SASE convergence accelerates, cloud-native controllers infuse security services, nudging even conservative sectors toward hybrid adoption. The SD-WAN market repeatedly illustrates that deployment flexibility, rather than hardware ownership, now dictates architecture decisions.

Solutions retained a 54.60% revenue share in 2025, spanning virtual appliances, perpetual licenses, and orchestration consoles. However, mounting integration demands are shifting budgets toward services, expected to post a 21.16% CAGR. Deloitte surveys showed 47% of enterprises outsourcing at least partial SD-WAN operations, driven by scarce internal expertise.

Professional services cover assessments, design, and proofs of concept, whereas managed services wrap transport, security, and monitoring into predictable OPEX. System integrators such as Accenture and Tata Consultancy Services now run multi-vendor SD-WAN centers of excellence, reducing overlay lock-in fears. As AI-based analytics mature, service providers differentiate by automating policy recommendations, reinforcing the gradual tilt of the SD-WAN market toward lifecycle partnerships.

Geography Analysis

North America controlled 41.20% of 2025 revenue owing to early cloud adoption, abundant broadband, and aggressive SASE experimentation. The U.S. Federal Communications Commission reported that 92% of business addresses accessed gigabit internet in 2025, allowing overlays to aggregate low-cost circuits for MPLS-grade reliability. Financial services hubs in New York and Charlotte, healthcare systems in Boston and Houston, and technology clusters in Silicon Valley collectively drove demand for consolidated network-security stacks. Canadian enterprises confront vast geographic dispersion, while Mexican manufacturers along the U.S. border lean on SD-WAN to support Industry 4.0 initiatives.

Asia-Pacific is forecast to post the fastest expansion at a 29.90% CAGR to 2031, propelled by India's USD 1.2 billion Digital India program, China's intelligent manufacturing push, and ASEAN's e-commerce boom. Standalone 5G cores rolling out across Japan, South Korea, and Australia fuel network slicing pilots that dovetail with SD-WAN orchestration. Emerging markets from Indonesia to Vietnam capitalize on SD-WAN to bypass expensive MPLS footprints and support cross-border digital trade.

Europe's trajectory is shaped by GDPR data-residency mandates that favor hybrid architectures keeping sensitive payloads on-premises. Germany's automotive giants link factories with engineering centers, while U.K. banks integrate SD-WAN and zero-trust to protect high-value trading flows. French and German operators launched bundled managed services in 2025, targeting mid-market firms lacking network personnel. Middle Eastern governments, notably Saudi Arabia and the United Arab Emirates, embed SD-WAN in national digital strategies, whereas South Africa and Nigeria anchor African adoption. In South America, Brazil and Argentina modernize frame relay estates via SD-WAN overlays to sustain e-commerce and hybrid work.

- Cisco Systems, Inc.

- Fortinet, Inc.

- VMware, Inc.

- Aryaka Networks, Inc.

- Versa Networks, Inc.

- Hewlett Packard Enterprise Company

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- Tata Communications Limited

- Telefonaktiebolaget LM Ericsson

- Cato Networks Ltd.

- Palo Alto Networks, Inc.

- Silver Peak Systems, LLC

- Masergy Communications, Inc.

- Juniper Networks, Inc.

- Citrix Systems, Inc.

- Zscaler, Inc.

- Riverbed Technology, LLC

- Check Point Software Technologies Ltd.

- Barracuda Networks, Inc.

- AT&T Inc. (AT&T Business division)

- Telstra Corporation Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-Centric Application Explosion

- 4.2.2 Hybrid/Remote-Work-Driven WAN Agility

- 4.2.3 MPLS Cost-Out and Bandwidth Optimization

- 4.2.4 5G Network Slicing and SD-WAN Convergence

- 4.2.5 AI-Driven Self-Healing Route Optimisation

- 4.2.6 ESG-Linked Carbon-Aware Routing Demand

- 4.3 Market Restraints

- 4.3.1 Data-Plane Security and Control-Plane Attack Surface

- 4.3.2 Shortage of SD-WAN Architecture Talent

- 4.3.3 Proprietary Overlay Lock-In Risks

- 4.3.4 CPE Supply-Chain Bottlenecks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Solutions

- 5.2.2 Services

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-User Industry

- 5.4.1 Healthcare

- 5.4.2 BFSI

- 5.4.3 Retail and Consumer Services

- 5.4.4 Manufacturing

- 5.4.5 Transport and Logistics

- 5.4.6 IT and Telecom

- 5.4.7 Others End-User Industry

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Turkey

- 5.5.4.4 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Nigeria

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Fortinet, Inc.

- 6.4.3 VMware, Inc.

- 6.4.4 Aryaka Networks, Inc.

- 6.4.5 Versa Networks, Inc.

- 6.4.6 Hewlett Packard Enterprise Company

- 6.4.7 Nokia Corporation

- 6.4.8 Huawei Technologies Co., Ltd.

- 6.4.9 Tata Communications Limited

- 6.4.10 Telefonaktiebolaget LM Ericsson

- 6.4.11 Cato Networks Ltd.

- 6.4.12 Palo Alto Networks, Inc.

- 6.4.13 Silver Peak Systems, LLC

- 6.4.14 Masergy Communications, Inc.

- 6.4.15 Juniper Networks, Inc.

- 6.4.16 Citrix Systems, Inc.

- 6.4.17 Zscaler, Inc.

- 6.4.18 Riverbed Technology, LLC

- 6.4.19 Check Point Software Technologies Ltd.

- 6.4.20 Barracuda Networks, Inc.

- 6.4.21 AT&T Inc. (AT&T Business division)

- 6.4.22 Telstra Corporation Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment