|

시장보고서

상품코드

2066539

비휘발성 메모리 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Non-Volatile Memory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

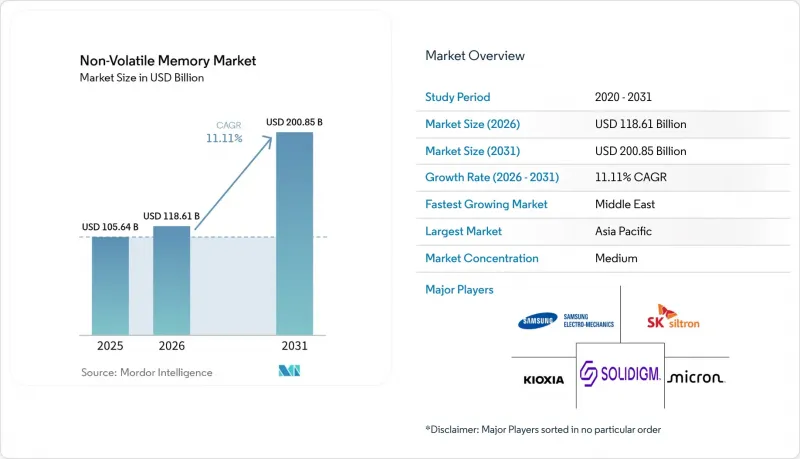

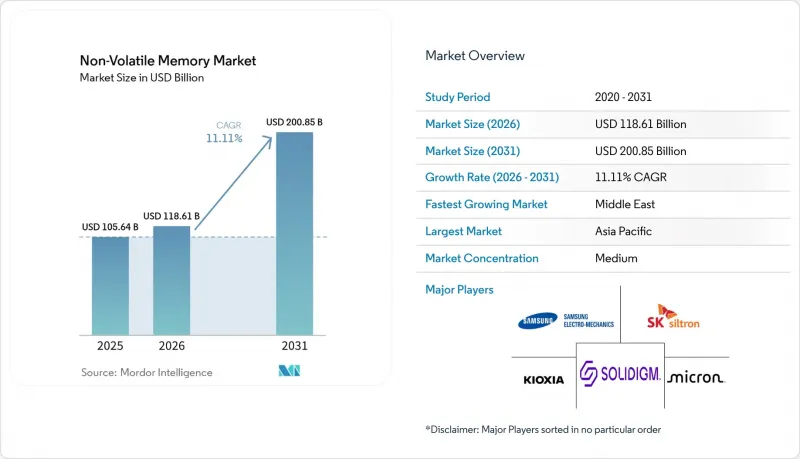

Mordor Intelligence에 의하면, 비휘발성 메모리 시장 규모는 2025년 1,056억 4,000만 달러로 평가되었습니다. 2026년 1,186억 1,000만 달러에서 2031년까지 2,008억 5,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 11.11%를 나타낼 것으로 예측됩니다.

본 보고서는 메모리 유형(기존 비휘발성 메모리, 차세대 메모리 등), 최종 사용자 산업(소비자용 전자기기, IT 및 통신, 기타), 인터페이스(PCIe/NVMe, SATA, SPI/I2C, 기타), 용량(256 Mb 이하, 512 Mb-1 Gb, 2 Gb-4Gb, 8 Gb 이상), 용도(엔터프라이즈 스토리지, 산업용 자동화, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 비휘발성 메모리 시장 동향 및 인사이트

데이터센터의 급속한 확장에 따라 엔터프라이즈급 NVM에 대한 수요가 증가하고 있습니다.

각 하이퍼스케일러 기업들은 2026년부터 2030년 사이에 100GW 규모의 신규 데이터센터용량을 구축할 계획이며, 각 랙에는 추론 워크로드를 처리하기 위해 페타바이트 규모의 올플래시 어레이가 통합되어 있습니다. 마이크론의 9650 등 PCIe Gen 6 SSD는 28 GB/s의 순차 읽기 처리량을 실현하여, 연산 처리와 스토리지 처리량 간의 격차를 해소하고 있습니다. NVIDIA의 ‘Inference Compute Memory Storage Platform’은 키-값 스토어를 고대역폭 메모리에서 엔터프라이즈용 SSD로 오프로드하여, 가속기 비용을 30% 절감하는 동시에 검색 지연 시간을 1밀리초 미만으로 억제하고 있습니다. 이러한 변화로 인해 하루 3회의 드라이브 쓰기 작업을 견딜 수 있는 트리플 레벨 셀(TLC) NAND가 유리한 입지를 차지하게 되었으며, 비휘발성 메모리 시장은 DRAM과 오브젝트 스토리지 사이의 전략적 완충 역할로서의 위상을 높이고 있습니다. 서버 교체 주기가 5년에서 3년으로 단축되는 가운데, 펌웨어 수준에서 내구성을 극대화한 공급업체들은 하이퍼스케일러와 장기 계약을 체결하고 있습니다.

자동차용 ADAS 및 차량용 인포테인먼트의 보급

소프트웨어 정의 차량에서는 고해상도 지도, 무선 업데이트, 센서 융합 로그를 위해 2-4 TB의 저장 공간이 할당되어 있습니다. 인피니언의 SEMPER NOR 플래시는 ISO 26262에 기반한 ASIL-D 안전 인증을 획득했으며, 레벨 3 자율 주행에서 페일-오퍼레이셔널 부트 아키텍처를 구현합니다. 유니버설 플래시 스토리지 4.0은 기존의 임베디드용 멀티미디어 카드(MMC)를 대체하며, 저전력으로 4K 동영상 스트리밍을 유지합니다. 자동차용 등급의 NAND는 -40°C-125°C의 온도 범위와 3,000회의 쓰기·지우기 사이클을 견뎌야 하며, 일반 소비자용 등급 모듈에 비해 가격이 40% 더 높게 책정되어 있습니다. 12V에서 48V로 전기 시스템이 전환됨에 따라 전압 과도 현상이 발생하게 되었기 때문에 각 OEM 업체들은 온다이 오류 정정 코드(ECC) 및 전원 손실 보호 기능을 사양으로 요구하게 되었으며, 이로 인해 부품 비용은 증가했으나 회생 제동 시 데이터 무결성이 확보되고 있습니다.

특정 NVM 아키텍처의 낮은 쓰기 내구성

쿼드 레벨 셀 NAND의 프로그램·삭제 사이클 수는 불과 500회, 펜타 레벨 셀은 200회에 그치지만, 트리플 레벨 셀은 3,000회입니다. 데이터베이스 로깅이나 AI 체크포인트 처리의 경우, 쓰기 증폭률이 5를 초과하기 때문에 쿼드 레벨 셀 드라이브는 18개월 이내에 수명이 다하게 됩니다. 머신러닝용 컨트롤러는 수명을 40% 연장하지만, 28%의 오버프로비저닝이 추가되기 때문에 비용 면에서의 이점이 줄어들게 됩니다. 현재, 각 하이퍼스케일러 기업들은 핫 데이터용으로 트리플 레벨 셀을 확보하고, 쿼드 레벨 셀을 콜드 스토리지로 전환하고 있기 때문에 조달 계획이 세분화되어 있습니다. 이러한 내구성 격차는 교체 비용이 모듈의 초기 가격을 초과하는 산업용 로거나 자동차용 블랙박스에서 MRAM 및 ReRAM에 대한 시장 기회를 창출하고 있습니다.

부문별 분석

2025년, 플래시 메모리는 비휘발성 메모리 시장 점유율의 63.78%를 차지했습니다. 꾸준한 비용 절감으로 그 우위는 유지되었지만, MRAM은 2031년까지 연평균 성장률(CAGR) 11.97%로 성장할 것으로 전망됩니다. 플래시에 의존하는 비휘발성 메모리 시장 규모는 계속 확대되고 있지만, 쓰기 부하가 높은 엣지 워크로드에서는 수명이라는 병목 현상이 드러나고 있습니다. 64 Mb, 128 Mb, 256 Mb 용량의 MRAM이 출하되어 산업용 컨트롤러, 철도 신호 시스템, 항공기 블랙박스에 채택되었습니다. 이러한 기술들은 펌웨어 업데이트 시 NAND의 블록 삭제 한도를 초과하는 상황에서 NOR 플래시를 대체했습니다.

2세대 스핀-궤도 토크 기술을 통해 MRAM의 밀도는 1Gb 수준으로 향상되고 있으며, 28nm 임베디드 로직과의 통합을 통해 10ns의 결정론적 쓰기 속도가 실현되고 있습니다. 강유전체 RAM은 10^14 사이클의 내구 수명이 요구되며, 용량이 킬로바이트 단위에 그치는 RFID 태그에 활용되고 있습니다. ReRAM 및 3D XPoint는 스토리지 클래스 메모리 분야를 목표로 하고 있지만, 인텔이 옵테인(Optane) 사업에서 철수함에 따라 상용화가 일시적으로 주춤했습니다. 현재 Weebit Nano와 같은 스타트업 기업들은 파운드리와의 제휴를 통해 이 과제를 극복하고자 하고 있습니다. 이러한 동향은 시스템 아키텍트가 내구성과 비용의 균형을 맞추기 위해 대용량 NAND와 바이트 단위로 주소 지정이 가능한 MRAM을 결합하는 전환점을 보여주고 있으며, 이러한 설계는 예측 기간 동안 비휘발성 메모리 시장을 재편하게 될 것입니다.

2025년에는 20억 대를 넘는 스마트폰, 태블릿, 노트북의 성장에 힘입어, 소비자용 전자기기가 수요의 44.81%를 차지했습니다. 한편, 자동차용 전자기기 분야는 전기자동차 판매 대수 증가와 첨단 운전자 보조 시스템(ADAS)이 ASIL-D 인증을 받은 저장 장치를 필요로 함에 따라, 2031년까지 연평균 성장률(CAGR) 11.56%를 나타낼 것으로 전망됩니다. 각 소프트웨어 정의 플랫폼에는 256MB에서 4GB 용량의 플래시 메모리를 탑재한 10-20개의 전자 제어 장치(ECU)가 내장되므로, 자동차 관련 비휘발성 메모리 시장 규모는 비약적으로 확대될 것입니다.

고해상도 지도, 무선 업데이트, 센서 로그가 로컬에 캐시되므로, 차량당 비휘발성 메모리 탑재량은 내연기관 차량에 비해 8배 증가했습니다. 통신 인프라는 기업용 SSD 출하량의 28%를 차지하고 있으며, 한편 의료 분야의 아카이브 용도에서는 10년간의 보관이 의무화된 AES-256 암호화 지원 NAND가 필수적입니다. 산업용 자동화 분야에서는 -40°C까지의 내충격성을 갖춘 NAND가 지정되어 있으며, 소매 단말기에서는 부팅 시간을 단축하기 위해 UFS 3.1이 채택되고 있습니다. 최종 사용자의 다양화로 인해 경기 변동의 영향이 완화되어, 스마트폰의 모델 교체 주기가 3년을 초과하는 경우에도 공급업체에 미치는 영향이 완화되고 있습니다.

지역별 분석

2025년, 아시아태평양은 비휘발성 메모리 매출의 46.11%를 차지했으며, 삼성, SK하이닉스, 키오크시아 및 대만의 파운드리 업체들이 이를 주도했습니다. 이 기업들은 전 세계 NAND 생산량의 75%를 공급하고 있습니다. 한국이 21조 6,000억 원(157억 달러)의 세액 공제를 통해 용인 클러스터에 자금을 지원하고, 일본 경제산업성이 마이크론사의 히로시마 공장에 5,000억 엔(34억 달러)를 지원함에 따라, 해당 지역의 성장률은 연평균 성장률(CAGR) 11.84%로 예측되고 있습니다. 중국은 ‘창장 메모리’를 통해 국내 NAND 생산을 가속화하고 있지만, 극자외선(EUV) 스캐너에 대한 미국의 수출 규제로 인해 128층 노드를 넘어서는 발전은 정체되어 있습니다.

북미는 2025년에 24%의 점유율을 차지했으며, 아마존, 마이크로소프트, 구글이 이를 주도하고 있습니다. 이 3개사의 총 40EB에 달하는 엔터프라이즈용 SSD 도입이 장기적인 조달을 뒷받침하고 있습니다. 'CHIPS and Science Act'에 따라 527억 달러의 보조금이 지원되며, 이 중 64억 4,000만 달러는 마이크론의 뉴욕 및 아이다호주 사업 확장, 47억 4, 500만 달러는 삼성의 텍사스주 생산 라인에, 9억 5,000만 달러는 SK하이닉스의 인디애나주 패키징 사업에 배정됩니다. 유럽은 전체 수요의 16%를 차지하고 있으며, 독일의 자동차 1차 공급업체들이 인피니온 및 ST마이크로일렉트로닉스로부터 ASIL-D 규격을 준수하는 NAND를 조달하고 있습니다.

중동은 스마트시티 및 인공지능(AI) 서비스를 위한 데이터센터 인프라에 정부계 펀드로부터 337억 9,000만 달러가 투자됨에 따라, 지역별로는 가장 높은 연평균 성장률(CAGR) 12.25%를 기록했습니다. 남미와 아프리카를 합치면 시장의 8%를 차지하고 있으며, 백본 회선의 대역폭이 제한적이라는 점을 보완하기 위해 기지국 서버에서 UFS 패키지를 활용한 엣지 캐싱에 의존하고 있습니다. 정부의 보조금으로 인해 지역적 집중도는 완화되고 있지만, 비휘발성 메모리 시장은 여전히 동북아시아의 3대 경제권에 의존하고 있으며, 공급은 지진, 정치 상황, 수출 규제 등의 사건에 영향을 받기 쉬운 상황입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the non-volatile memory market size is projected to expand from USD 105.64 billion in 2025 and USD 118.61 billion in 2026 to USD 200.85 billion by 2031, registering a CAGR of 11.11% between 2026 and 2031.

This report is Segmented by Memory Type (Traditional Non-Volatile Memory, and Next-Generation and More), End-User Industry (Consumer Electronics, IT and Telecom, and More), Interface (PCIe/NVMe, SATA, SPI/I2C, and More), Density (<=256 Mb, 512 Mb-1 Gb, 2 Gb-4 Gb, and >=8 Gb), Application (Enterprise Storage, Industrial Automation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Non-Volatile Memory Market Trends and Insights

Exploding Data-Center Build-Outs Elevate Demand for Enterprise-Class NVM

Hyperscalers plan to deploy 100 GW of new data-center capacity between 2026 and 2030, and each rack integrates petabyte-scale all-flash arrays to serve inference workloads. PCIe Gen 6 solid-state drives, such as Micron's 9650, deliver 28 GB/s of sequential read throughput, closing the gap between compute and storage throughput. NVIDIA's Inference Compute Memory Storage Platform offloads key-value stores from high-bandwidth memory to enterprise SSDs, trimming accelerator costs by 30% while holding retrieval latency below one millisecond. This shift favors triple-level cell NAND that withstands 3 drive writes per day, elevating the non-volatile memory market as a strategic buffer between DRAM and object storage. As server refresh cycles accelerate from five to three years, suppliers that master firmware-level endurance optimization secure long-term contracts with hyperscalers.

Proliferation of Automotive ADAS and In-Vehicle Infotainment

Software-defined vehicles allocate 2-4 TB of storage for high-definition maps, over-the-air updates, and sensor-fusion logs. Infineon's SEMPER NOR Flash earned ASIL-D safety certification under ISO 26262, enabling fail-operational boot architectures in Level 3 autonomy. Universal Flash Storage 4.0 replaces legacy embedded MultiMediaCard to sustain 4K video streaming at lower power. Automotive-grade NAND must survive -40 °C to 125 °C and 3 000 program-erase cycles, commanding a 40% premium over consumer-grade modules. The transition from 12-V to 48-V electrical systems introduces voltage transients, prompting original equipment manufacturers to specify on-die error-correcting code and power-loss protection, boosting the bill of materials yet ensuring data integrity during regenerative braking.

Low Write-Endurance in Certain NVM Architectures

Quad-level cell NAND endures only 500 program-erase cycles and penta-level cell just 200, compared with 3 000 for triple-level cell. Database logging and AI checkpointing reach write amplification factors above 5, exhausting quad-level cell drives within 18 months. Machine-learning controllers extend life by 40% but add 28% over-provisioning, eroding cost advantages. Hyperscalers now reserve triple-level cells for hot data and relegate quad-level cells to cold storage, fragmenting procurement plans. The endurance gap opens white space for MRAM and ReRAM in industrial loggers and automotive black boxes, where replacement costs exceed initial module pricing.

Other drivers and restraints analyzed in the detailed report include:

- Edge AI Workloads Requiring Persistent, Low-Latency Storage

- Mainstream Adoption of UFS 4.0 Interface in Smartphones

- Thermal Runaway Risks in High-Density 3D NAND Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flash memory accounted for 63.78% of the non-volatile memory market share in 2025. Steady cost declines sustained its dominance, yet MRAM is projected to grow at an 11.97% CAGR through 2031. The non-volatile memory market size tied to flash continues to expand, although write-heavy edge workloads expose endurance bottlenecks. MRAM shipments of 64 Mb, 128 Mb, and 256 Mb entered industrial controllers, railway signaling, and aviation black boxes, replacing NOR Flash where firmware updates exceed NAND's block-erase limitations.

Second-generation spin-orbit torque technology raises MRAM densities toward 1 Gb, and integration on 28 nm embedded logic yields deterministic 10 ns writes. Ferroelectric RAM services RFID tags that need 10^14 cycles but only kilobyte capacities. ReRAM and 3D XPoint aim for the storage-class memory tier, yet Intel's Optane exit created a commercialization pause that startups like Weebit Nano now aim to overcome through foundry alliances. These dynamics illustrate a pivot where system architects pair high-capacity NAND with byte-addressable MRAM to balance endurance and cost, a design that reshapes the non-volatile memory market over the forecast horizon.

Consumer electronics accounted for 44.81% of demand in 2025, driven by more than 2 billion smartphones, tablets, and laptops. Automotive electronics, however, is anticipated to post an 11.56% CAGR through 2031 as electric vehicle volumes rise and advanced driver-assistance systems require ASIL-D-certified storage. The non-volatile memory market size attributable to vehicles multiplies as each software-defined platform embeds 10-20 electronic control units with 256 MB to 4 GB flash.

High-definition maps, over-the-air updates, and sensor logs are cached locally, elevating per-vehicle non-volatile memory content eightfold relative to internal-combustion models. Telecommunications infrastructure accounts for 28% of enterprise SSD shipments, while healthcare archiving mandates AES-256-encrypted NAND with 10-year retention. Industrial automation specifies shock-resistant NAND rated to -40 °C, and retail terminals adopt UFS 3.1 to cut boot times. Diversified end users reduce cyclicality, insulating suppliers when smartphone refresh cycles extend beyond three years.

Geography Analysis

Asia-Pacific accounted for 46.11% of non-volatile memory revenue in 2025, led by Samsung, SK hynix, Kioxia, and Taiwanese foundries, which supply 75% of global NAND output. Regional growth is projected at an 11.84% CAGR as South Korea's 21.6 trillion won (USD 15.7 billion) tax credits finance the Yongin cluster, and Japan's Ministry of Economy, Trade and Industry grants JPY 500 billion (USD 3.4 billion) to Micron's Hiroshima fab. China accelerates domestic NAND at Yangtze Memory, but U.S. export controls on extreme-ultraviolet scanners stall progress beyond 128-layer nodes.

North America held 24% share in 2025, buoyed by Amazon, Microsoft, and Google, whose collective 40 EB of enterprise SSD deployments anchor long-term procurement. The CHIPS and Science Act unlocks USD 52.7 billion in subsidies, with USD 6.44 billion for Micron's New York and Idaho expansions, USD 4.745 billion for Samsung's Texas line, and USD 950 million for SK hynix packaging in Indiana. Europe captured 16% demand as Germany's automotive tier-ones source ASIL-D NAND from Infineon and STMicroelectronics.

The Middle East posts the fastest regional CAGR of 12.25%, driven by USD 33.79 billion in sovereign-wealth spending on data-center infrastructure for smart-city and artificial intelligence services. South America and Africa together account for 8% of the market and rely on edge caching to offset limited backbone bandwidth, using UFS packages in base-station servers. Government subsidies reduce geographic concentration, yet the non-volatile memory market still hinges on three Northeast Asian economies, leaving supply vulnerable to seismic, political, and export-control events.

- ROHM Co. Ltd

- STMicroelectronics NV

- Fujitsu Ltd

- Solidigm Inc.

- Honeywell International Inc.

- Micron Technology Inc.

- Samsung Electronics Co. Ltd

- Crossbar Inc.

- Infineon Technologies AG

- Avalanche Technology Inc.

- Western Digital Corp.

- SK Hynix Inc.

- Kioxia Holdings Corp.

- NXP Semiconductors NV

- Sony Semiconductor Solutions Corp.

- Seagate Technology Holdings PLC

- Renesas Electronics Corp.

- Intel Corporation

- GigaDevice Semiconductor Inc.

- Winbond Electronics Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exploding Data-Center Build-Outs Elevate Demand for Enterprise-Class NVM

- 4.2.2 Proliferation of Automotive ADAS and In-Vehicle Infotainment

- 4.2.3 Edge AI Workloads Requiring Persistent, Low-Latency Storage

- 4.2.4 Mainstream Adoption of UFS 4.0 Interface in Smartphones

- 4.2.5 Commercialization of 3D-XPoint-Based Persistent Memory Modules

- 4.2.6 Government Incentives for Domestic Semiconductor Manufacturing

- 4.3 Market Restraints

- 4.3.1 Low Write-Endurance in Certain NVM Architectures

- 4.3.2 Thermal Runaway Risks in High-Density 3D NAND Stacks

- 4.3.3 Geopolitical Export Controls on Advanced Memory Nodes

- 4.3.4 Supply-Demand Cyclicality Causing Price Volatility

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Regulatory Landscape

- 4.6 Industrial Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Memory Type

- 5.1.1 Traditional Non-Volatile Memory

- 5.1.1.1 Flash Memory

- 5.1.1.2 EEPROM

- 5.1.1.3 SRAM

- 5.1.1.4 EPROM

- 5.1.1.5 Rest of Traditional Non-Volatile Memory

- 5.1.2 Next-Generation Non-Volatile Memory

- 5.1.2.1 MRAM

- 5.1.2.2 FRAM

- 5.1.2.3 ReRAM

- 5.1.2.4 3D XPoint

- 5.1.2.5 Nano RAM

- 5.1.2.6 Rest of Next-Generation Non-Volatile Memory

- 5.1.1 Traditional Non-Volatile Memory

- 5.2 By End-User Industry

- 5.2.1 Consumer Electronics

- 5.2.2 Retail

- 5.2.3 IT and Telecom

- 5.2.4 Healthcare

- 5.2.5 Other End-User Industries

- 5.3 By Interface

- 5.3.1 PCIe/NVMe

- 5.3.2 SATA

- 5.3.3 USB

- 5.3.4 SPI/I2C

- 5.3.5 Other Interfaces

- 5.4 By Density

- 5.4.1 <=256 Mb

- 5.4.2 512 Mb-1 Gb

- 5.4.3 2 Gb-4 Gb

- 5.4.4 >=8 Gb

- 5.5 By Application

- 5.5.1 Enterprise Storage

- 5.5.2 Connected and Wearable Devices

- 5.5.3 Industrial Automation

- 5.5.4 Automotive Electronics

- 5.5.5 Rest of Applications

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ROHM Co. Ltd

- 6.4.2 STMicroelectronics NV

- 6.4.3 Fujitsu Ltd

- 6.4.4 Solidigm Inc.

- 6.4.5 Honeywell International Inc.

- 6.4.6 Micron Technology Inc.

- 6.4.7 Samsung Electronics Co. Ltd

- 6.4.8 Crossbar Inc.

- 6.4.9 Infineon Technologies AG

- 6.4.10 Avalanche Technology Inc.

- 6.4.11 Western Digital Corp.

- 6.4.12 SK Hynix Inc.

- 6.4.13 Kioxia Holdings Corp.

- 6.4.14 NXP Semiconductors NV

- 6.4.15 Sony Semiconductor Solutions Corp.

- 6.4.16 Seagate Technology Holdings PLC

- 6.4.17 Renesas Electronics Corp.

- 6.4.18 Intel Corporation

- 6.4.19 GigaDevice Semiconductor Inc.

- 6.4.20 Winbond Electronics Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment