|

시장보고서

상품코드

2066541

보툴리눔톡신(보톡스) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Botulinum Toxin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

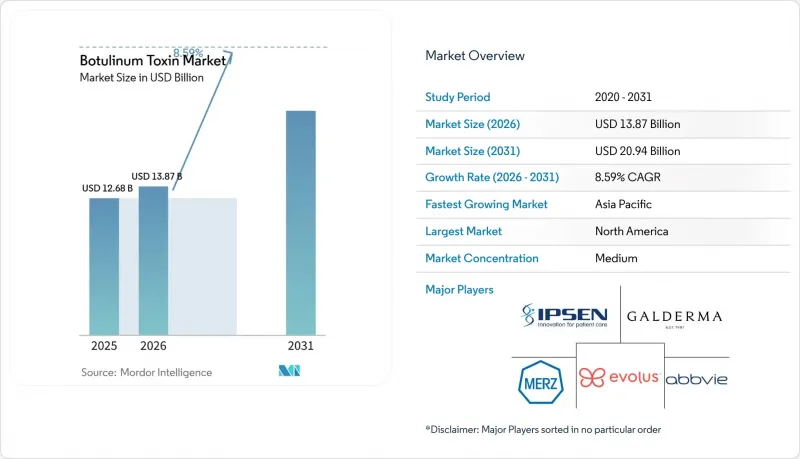

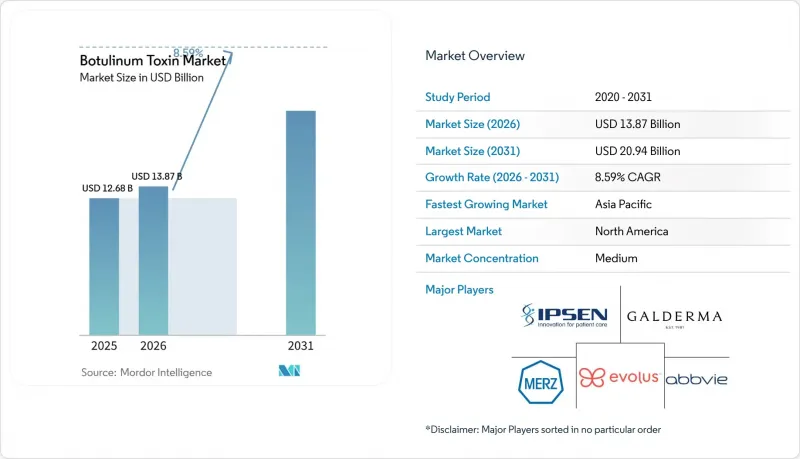

Mordor Intelligence에 의하면, 보툴리눔톡신(보톡스) 시장 규모는 2025년 126억 8,000만 달러로 평가되었습니다. 2026년 138억 7,000만 달러에서 2031년까지 209억 4,000만 달러에 이를 것으로 예상되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 8.59%를 나타낼 전망입니다.

본 보고서에서는 업계를 제품 유형(보툴리눔톡신 A형, 보툴리눔톡신 B형), 용도(미용, 치료), 최종 사용자(전문 클리닉·피부과 클리닉, 병원·외과 센터, 스파·미용 센터 등), 그리고 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류하고 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 보툴리눔툭신(보톡스) 시장 동향 및 분석

저침습 미용 시술에 대한 수요 증가

뉴로모듈레이터는 수술에 따른 회복 기간이 없고, 즉각적인 효과가 있으며, 효과가 가역적이기 때문에 소셜 미디어 중심의 문화 속에서 높은 평가를 받고 있으며, 전 세계적으로 시술 건수가 꾸준히 증가하고 있습니다. 미국 성형외과학회(ASPS)의 기록에 따르면, 2024년 미국 내 뉴로모듈레이터 시술 건수는 988만 건에 달하고, 전년 대비 4% 증가했으나, 이 수치 뒤에는 처음으로 시술을 받는 남성 이용자와 30세 미만 환자층에서 더욱 급격한 성장이 숨어 있습니다. 인스타그램과 틱톡은 고려 기간을 단축시켜, 환자가 인지 단계에서 시술에 이르기까지 걸리는 기간을 18개월 미만으로 단축하고 있습니다. 당일 상담 예약을 받는 클리닉은 이러한 충동적인 내원을 효과적으로 활용함으로써, 환자 1인당 연간 3.2회의 내원 빈도를 기록하며 지속적인 수익을 유지하고 있습니다. ‘트위크먼트(미세 조정)’라는 문화는 극적인 안면 리프팅보다는 절제된 시술을 반복적으로 받는 것을 선호하는 경향이 있어, 그 결과 거시경제 상황이 악화되더라도 시술 건수가 안정적으로 유지되며 보툴리눔톡신(보톡스) 시장의 성장을 뒷받침하고 있습니다. 그러나 이러한 급증은 규제가 완화된 지역에서 의사 이외의 시술자들의 진입을 초래하여 품질 면에서 우려를 불러일으키고 있으며, 당국도 이에 대한 단속을 시작했습니다.

만성 편두통 예방 요법에서의 적용 확대

만성 편두통은 인구의 약 2%에게 영향을 미치고 있습니다. 오나보툴리눔톡신 A는 수년에 걸친 임상시험을 통해 입증된 레벨 A 근거에 힘입어, 2024년 미국 두통학회(American Headache Society) 지침에서 1차 선택 약물로 자리매김했습니다. 유나이티드 헬스케어는 2025년에 사전 승인 요건을 폐지했으며, 그 결과 6개월 이내에 치료 중단률이 34% 감소했습니다. 의료 경제 분석에 따르면, 환자가 보툴리눔툭신(보톡스)를 이용한 예방 요법을 시작하면 응급실 내원 횟수가 47% 감소하고, 오피오이드 처방량이 52% 감소하는 것으로 나타났으며, 이를 통해 1건당 연간 4,200달러의 순절감 효과를 얻을 수 있습니다. 신경과 전문의가 진료소에서 주사를 놓는 사례가 늘어나고 있으며, 그로 인해 치료의 기반이 확대되고 있습니다. ACO(Accountable Care Organization)가 하방 리스크를 부담하는 가운데, 보툴리눔툭신(보톡스)는 가치 기반 진료 모델에 잘 부합하여 치료법으로의 도입이 가속화되고 있습니다.

면역 저항성 및 중화 항체의 위험

반복 사용자의 1-3%에서 중화 항체가 생성됩니다. 이는 일반적으로 7주기 경과 후 또는 누적 투여량이 200단위를 초과한 후에 발생하며, 치료 실패로 이어져 약물 변경이 필요할 수 있습니다. 무단백질 독소와 기존 독소를 비교한 데이터는 여전히 부족하여, 임상의들은 실용적인 투여 전략이나 치료 간격 확대에 의존할 수밖에 없는 상황입니다. 실세계에서의 유효성을 면밀히 주시하는 보험사는 항체 검사 도입을 검토할 가능성이 있으며, 이로 인해 비용과 행정 절차가 증가하여, 특히 환자가 본인 부담으로 치료를 받는 미용 분야에서 도입에 걸림돌이 될 우려가 있습니다.

부문별 분석

2025년 보툴리눔툭신(보톡스) 시장에서 A형 제품 시장 규모는 총 매출의 87.81%를 차지했습니다. 이는 미용 및 치료 두 분야에 걸친 FDA의 광범위한 적응증을 반영한 것입니다. ‘제오민(Xeomin)’과 같이 복합 단백질을 포함하지 않는 제제는 2024년에 승인된 ‘1회 시술로 상안면을 치료한다’는 적응증 덕분에 시술 시간을 단축하고 시술 건수를 중시하는 클리닉 수요를 충족시킴으로써, 기존 제품 시장 점유율을 서서히 잠식하고 있습니다. 주보는 시장 선두 기업보다 20-30% 저렴한 가격 정책과 소셜 미디어를 중심으로 한 캠페인을 통해 밀레니얼 세대를 공략함으로써, 미국 내 시장 점유율을 2019년 4%에서 2025년 14%로 확대했습니다. 닥시파이의 ‘6개월 지속’이라는 차별화 요소는 의료 종사자에 대한 교육 요건으로 인해 도입이 지연되고 있어, 아직 그에 상응하는 보급으로 이어지지는 못하고 있습니다. 가격을 30-40% 낮게 책정한 한국의 신규 진출기업들은 아시아와 라틴아메리카 일부 지역에서 계속해서 성장세를 보이고 있으며, 보툴리눔툭신(보톡스) 시장 점유율 구도를 더욱 형성해 나가고 있습니다.

B형 시장 점유율 기여도는 미미하지만, A형에 대한 항체로 인해 반응하지 않는 사람이 증가함에 따라 2031년까지 연평균 성장률(CAGR) 10.58%로 상승하고 있습니다. ‘리마보툴리눔톡신 B’는 24-48시간 내에 효과가 나타나기 때문에 급성 경부 디스토니아 증례에서 매력적인 치료법입니다. 에자이는 2024년 유럽에서 매출이 19% 증가했습니다. 이는 신규 치료 환자에 의한 것이 아니라, 신경과 전문의가 치료법을 변경한 것이 주된 원인입니다. 효과 지속 기간이 짧은 경우, 기능적 개선이 미용적 지속 기간을 능가할 때, 임상의들은 유효성을 위해 내원 횟수 증가를 수용하는 경향이 있습니다. 그 결과, 비록 틈새 시장이지만 보툴리눔톡신 업계의 포트폴리오를 다각화하는 안정적인 수익원이 되고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 42.36%를 차지하며, 신제품 출시 및 규제 선례 측면에서 여전히 주요 시장으로 자리매김했습니다. 2024년 미국의 시술 건수는 988만 건에 달했으며, 미용 목적의 시술은 해안 지역의 대도시권에 집중된 반면, 치료 목적의 시술은 신경과나 비뇨기과 진료소에 분산되어 있습니다. 캐나다 보건부가 2024년에 ‘나보타’를 승인함에 따라 경쟁이 촉발될 것이며, 이는 가격에 민감한 소비자층에 대한 접근성 확대로 이어질 가능성이 있습니다. 멕시코 의료 관광을 통해 50-60%의 비용 절감이 가능하지만, 위조품의 위험에 직면해 있어 그 규모 확대를 억제하고 있습니다. 2025년 ‘트레비봇 E’의 생물학적 제제 승인 신청(BLA)에서 볼 수 있듯이, FDA가 새로운 혈청형에 대해 관대한 태도를 보이고 있는 것은 지속적인 혁신을 의미하지만, 외딴 지역으로의 확산과 관련된 안전성 정보 공개는 의료 과실 보험에 대한 우려를 불러일으키고 있습니다.

아시아태평양은 국내 생산 규모 확대와 중산층 확장에 힘입어 연평균 성장률(CAGR) 12.13%를 나타낼 것으로 예측되며, 이는 세계에서 가장 빠른 성장 속도입니다. 한국의 1인당 사용량은 문화적 수용도와 정부의 수출 장려 정책에 힘입어 미국과 맞먹는 수준에 이르렀습니다. 중국 시장은 품질에 대한 인식에 따라 양극화되어 있습니다. 1급 도시에서는 서유럽 브랜드가 선호되는 반면, 2급 및 3급 도시에서는 1바이알당 80-100달러인 국산 제품이 선택되고 있습니다. 일본에서는 고령화에 따라 치료 수요가 증가하고 있으며, ‘제오민’은 2024년에야 비로소 PMDA의 승인을 받았지만, 보급 속도는 가속화되고 있습니다. 인도의 미용 의료 부문은 도시 지역에서 연평균 20-25%의 성장세를 보이고 있지만, 콜드체인의 미비로 인해 시장 내 추가적인 확산이 저해되고 있습니다. 방콕 등 동남아시아의 주요 도시에서는 연간 약 12만 명의 해외 미용 의료 환자에게 40% 할인된 가격으로 치료를 제공하고 있으며, 이로 인해 보툴리눔톡신(보톡스) 시장의 지역적 확장이 촉진되고 있습니다.

유럽은 중간 수준 시장 점유율을 차지하고 있지만, 유럽의약품청(EMA)이 2025년부터 원격 확산에 대한 경고를 강화하도록 의무화함에 따라 성장이 둔화되고 있으며, 프랑스와 이탈리아에서는 판매 주기가 길어지고 있습니다. 독일과 영국에서는 만성 편두통 및 경련에 대한 국민건강보험 적용 덕분에 치료가 널리 보급되고 있습니다. 영국의 간호사가 주도하는 과활동성 방광(OAB) 클리닉에서는 대기 시간이 9개월에서 6주로 단축되었습니다. 동유럽 국가들에서는 소득 증가와 서유럽에서 연수를 마친 의사들의 귀국에 힘입어 시장이 성장세를 보이고 있습니다. 중동에서는 아랍에미리트(UAE)와 사우디아라비아가 높은 1인당 소득과 의료 관광 인프라를 바탕으로 성장을 주도하고 있습니다. 남아프리카에서는 민간 부문에서 꾸준한 성장이 나타나고 있지만, 사하라 이남 지역으로의 추가적인 확산은 인프라 및 공중보건 분야의 우선 과제로 인해 제약을 받고 있습니다. 남미에서는 브라질이 중심이 되고 있으며, 브라질 ANVISA가 한국 및 중국의 보툴리눔툭신(보톡스)를 심사 중이고, 승인이 나면 더 많은 사람들이 이를 이용할 수 있게 될 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the botulinum toxin market size is projected to expand from USD 12.68 billion in 2025 and USD 13.87 billion in 2026 to USD 20.94 billion by 2031, registering a CAGR of 8.59% between 2026 to 2031.

This report Segments the Industry Into by Product Type (Botulinum Toxin Type A, Botulinum Toxin Type B), Application (Aesthetic, Therapeutic), End User (Specialty & Dermatology Clinics, Hospitals & Surgery Centers, Spas & Beauty Centers, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Botulinum Toxin Market Trends and Insights

Rising Demand for Minimally Invasive Aesthetic Procedures

Global procedure counts continue to climb because neuromodulators offer immediate, reversible results without surgical downtime, qualities highly valued in social-media-driven cultures. The American Society of Plastic Surgeons recorded 9.88 million U.S. neuromodulator sessions in 2024, a 4% year-over-year uptick that masks even steeper growth among first-time male users and patients under 30. Instagram and TikTok compress consideration windows, pushing patients from awareness to treatment in under 18 months. Clinics that can schedule same-day consults capture these impulse conversions and report a 3.2-visit annual cadence per patient, sustaining recurring revenue. The "tweakment" culture favors subtle, repeat interventions rather than dramatic facelifts, which in turn stabilizes volume even when macroeconomic conditions soften and reinforces botulinum toxin market growth. Yet the surge also invites non-physician injectors where regulation is light, prompting quality concerns that authorities are beginning to police.

Growing Adoption in Chronic Migraine Prophylaxis

Chronic migraine affects roughly 2% of the population; onabotulinumtoxinA now holds first-line status under 2024 American Headache Society guidelines, supported by Level A evidence from multi-year trials. UnitedHealthcare removed prior-authorization requirements in 2025, resulting in a 34% reduction in dropout rates within six months. Health-economic analyses show that emergency department visits decrease by 47% and opioid prescriptions by 52% once patients initiate toxin prophylaxis, resulting in an annual net savings of USD 4,200 per case. Neurologists are increasingly administering injections in-office, thereby broadening the treatment base. As accountable-care organizations shoulder downside risk, botulinum toxin fits neatly into value-based care models, accelerating its therapeutic adoption.

Immunoresistance & Neutralizing Antibody Risk

Neutralizing antibodies arise in 1-3% of repeat users, typically after seven cycles or cumulative doses exceeding 200 units, which can lead to treatment failure and necessitate product switching. Comparative data on protein-free versus conventional toxins remain sparse, leaving clinicians reliant on pragmatic dosing strategies and wider inter-treatment intervals. Payers watching real-world effectiveness may introduce antibody testing, adding cost and administrative steps that could dampen uptake, especially in aesthetic settings where patients pay out-of-pocket.

Other drivers and restraints analyzed in the detailed report include:

- Expansion in APAC Via Indigenous Manufacturers

- Longer-Lasting, Complexing-Protein-Free Formulations

- Cold-Chain & Handling Gaps in Low-Income Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The botulinum toxin market size for Type A products accounted for 87.81% of total revenue in 2025, reflecting their broad FDA labeling across both aesthetic and therapeutic domains. Complex-protein-free formulations, such as Xeomin, are gradually eroding legacy share because the single-session upper-face indication, cleared in 2024, reduces chair time and appeals to volume-driven clinics. Jeuveau increased its U.S. market share from 4% in 2019 to 14% in 2025 by targeting millennials with social media-centric campaigns at prices 20-30% lower than the market leader. Daxxify's six-month duration differentiator has not yet translated into proportional uptake because provider training requirements slow onboarding. Korean entrants with 30-40% lower pricing continue gaining traction in Asia and parts of Latin America, further shaping botulinum toxin market share.

Type B's contribution is small yet rising at a 10.58% CAGR through 2031 as antibody-induced non-responders to Type A accumulate. RimabotulinumtoxinB offers a 24- to 48-hour onset, making it appealing for acute cervical dystonia cases. Eisai logged 19% European revenue growth in 2024, driven by neurologist switches rather than new-to-therapy patients. Duration is shorter, but where functional improvement outweighs cosmetic longevity, clinicians are willing to trade repeat visits for efficacy. The result is a stable, if niche, revenue driver that diversifies the botulinum toxin industry portfolio.

Geography Analysis

North America accounted for 42.36% of global revenue in 2025 and remains the leading market for new product launches and regulatory precedents. U.S. volume reached 9.88 million procedures in 2024, concentrated in coastal metros for aesthetic purposes and dispersed across neurology and urology practices for therapeutic use. Health Canada's 2024 approval of Nabota injects pricing competition that may expand access among cost-sensitive consumers. Mexico's medical-tourism flow offers 50-60% cost savings but faces counterfeit risk, curbing its scale. The FDA's openness to novel serotypes, exemplified by TrenibotE's 2025 BLA, signals ongoing innovation, although distant-spread safety communications raise concerns about malpractice insurance.

The Asia-Pacific region is forecast to grow at a 12.13% CAGR, the fastest worldwide, driven by domestic manufacturing scale and an expanding middle class. South Korea's per-capita usage rivals that of the U.S., driven by cultural acceptance and government export incentives. China's market divides along quality perceptions: tier-1 cities prefer Western labels, whereas tier-2 and tier-3 cities opt for domestic products priced at USD 80-100 per vial. Japan's aging population pushes therapeutic demand; Xeomin only secured PMDA clearance in 2024, but uptake is accelerating. India's aesthetic segment grows at a rate of 20-25% annually in urban centers, yet cold-chain gaps constrain its broader penetration. Southeast Asian hubs, such as Bangkok, treat approximately 120,000 international aesthetic patients annually at 40% discounts, thereby extending the regional reach of the botulinum toxin market.

Europe holds a mid-tier share, with growth tempered by the European Medicines Agency's 2025 mandate for enhanced distant-spread warnings, which lengthen sales cycles in France and Italy. Germany and the UK lead therapeutic uptake through national health coverage for chronic migraine and spasticity; the UK's nurse-led OAB clinics have reduced wait times from nine months to six weeks. Eastern European countries are catching up as incomes rise and Western-trained physicians return to their homeland. In the Middle East, the UAE and Saudi Arabia drive growth, leveraging their high per-capita wealth and medical tourism infrastructure. South Africa exhibits steady private-sector growth, but wider sub-Saharan penetration is limited by infrastructure and public health priorities. South America pivots on Brazil, where ANVISA reviews Korean and Chinese toxins, potentially democratizing access once approvals land.

- Abbvie

- Aesthetic Biomedical Inc.

- Coretox (Medytox subsidiary)

- Daewoong Pharmaceutical Co., Ltd.

- Eisai

- Evolus Inc.

- Galderma

- Huons Global

- Hugel Inc.

- Ipsen Group

- Lanzhou Institute of Biological Products Co., Ltd.

- Medytox

- Merz Pharma

- Revance Therapeutics

- Shanghai Haohai Biological Technology Co., Ltd.

- Sihuan Pharmaceutical Holdings Ltd.

- Stemline Therapeutics

- Syndax Pharmaceuticals

- Suneva Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Minimally-Invasive Aesthetic Procedures

- 4.2.2 Growing Adoption in Chronic Migraine Prophylaxis

- 4.2.3 Expansion in APAC Via Indigenous Manufacturers

- 4.2.4 Longer-Lasting, Complexing-Protein-Free Formulations

- 4.2.5 Rising Male and "Pre-Juvenation" Patient Segments

- 4.2.6 Reimbursement Gains for Neurogenic Bladder & OAB

- 4.3 Market Restraints

- 4.3.1 Immunoresistance & Neutralizing Antibody Risk

- 4.3.2 Cold-Chain & Handling Gaps in Low-Income Markets

- 4.3.3 Counterfeit / Grey-Market Toxin Supply

- 4.3.4 High Out-of-Pocket Costs for Cosmetic Indications

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Botulinum Toxin Type A

- 5.1.1.1 OnabotulinumtoxinA (Botox)

- 5.1.1.2 AbobotulinumtoxinA (Dysport)

- 5.1.1.3 IncobotulinumtoxinA (Xeomin)

- 5.1.1.4 PrabotulinumtoxinA (Jeuveau)

- 5.1.1.5 DaxibotulinumtoxinA (Daxxify)

- 5.1.1.6 Complexing-protein-free (Coretox & others)

- 5.1.2 Botulinum Toxin Type B

- 5.1.1 Botulinum Toxin Type A

- 5.2 By Application

- 5.2.1 Aesthetic

- 5.2.1.1 Glabellar Lines

- 5.2.1.2 Crow's Feet

- 5.2.1.3 Forehead Lines

- 5.2.1.4 Masseter Reduction & Jaw Contouring

- 5.2.1.5 Body Contouring & Hyperhidrosis

- 5.2.2 Therapeutic

- 5.2.2.1 Chronic Migraine

- 5.2.2.2 Spasticity

- 5.2.2.3 Cervical Dystonia

- 5.2.2.4 Neurogenic Detrusor Overactivity / OAB

- 5.2.2.5 Sialorrhea

- 5.2.2.6 Others (Strabismus, Tremor, TMD)

- 5.2.1 Aesthetic

- 5.3 By End User

- 5.3.1 Specialty & Dermatology Clinics

- 5.3.2 Hospitals & Surgery Centers

- 5.3.3 Spas & Beauty Centers

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc. (Allergan Aesthetics)

- 6.3.2 Aesthetic Biomedical Inc.

- 6.3.3 Coretox (Medytox subsidiary)

- 6.3.4 Daewoong Pharmaceutical Co., Ltd.

- 6.3.5 Eisai Co., Ltd.

- 6.3.6 Evolus Inc.

- 6.3.7 Galderma S.A.

- 6.3.8 Huons Global

- 6.3.9 Hugel Inc.

- 6.3.10 Ipsen Group

- 6.3.11 Lanzhou Institute of Biological Products Co., Ltd.

- 6.3.12 Medytox Inc.

- 6.3.13 Merz Pharma GmbH & Co. KGaA

- 6.3.14 Revance Therapeutics Inc.

- 6.3.15 Shanghai Haohai Biological Technology Co., Ltd.

- 6.3.16 Sihuan Pharmaceutical Holdings Ltd.

- 6.3.17 Stemline Therapeutics

- 6.3.18 Syndax Pharmaceuticals

- 6.3.19 Suneva Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment