|

시장보고서

상품코드

2066556

압박 요법 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Compression Therapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

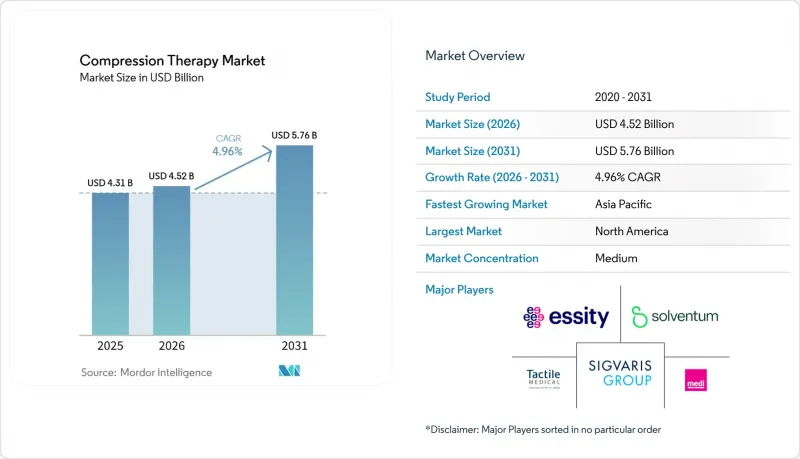

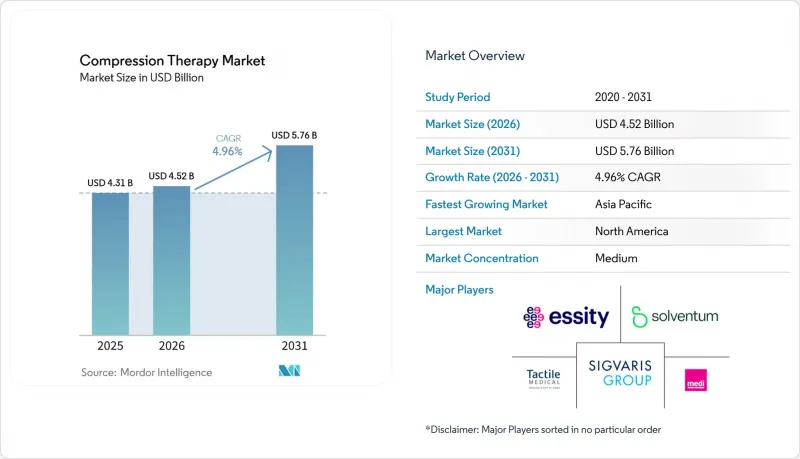

Mordor Intelligence에 의하면, 2026년 압박 요법 시장 규모는 45억 2,000만 달러에 달할 것으로 예상됩니다. 2025년 43억 1,000만 달러에서 확대해, 2031년에는 57억 6,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 4.96%로 성장할 것으로 전망됩니다.

본 보고서는 기술별(정적 압박 요법, 동적 압박 요법), 제품별(압박 의류, 압박 펌프, 압박 보조기), 용도별(하지 정맥성 궤양, 심부정맥 혈전증 치료 등), 최종 사용자별(병원, 전문 클리닉, 재택 간호, 기타), 지역별(북미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 압박 요법 시장 동향 및 인사이트

정맥 질환 및 림프부종의 유병률 증가

미국에서는 2,500만 명의 성인이 만성 정맥 부전을 앓고 있어, 1차 치료법으로 꼽히는 압박 요법에 대한 지속적인 수요가 발생하고 있습니다. 고압 단계형 스타킹은 혈전후 증후군을 예방하며, 2025년 SCAI 임상 지침에서는 정맥성 궤양에 대한 이 스타킹의 사용을 강력히 권장하고 있습니다. 이러한 공식적인 지지에 힘입어, 병원 및 보험사의 조달 계획이 안정화되고 있습니다. 치료 수요가 지속됨에 따라 예측 가능한 교체 주기가 형성되어, 제조업체는 생산 능력을 계획하고 장기적으로 압박 요법 시장을 유지할 수 있게 됩니다.

고령화의 진행

인구 고령화는 혈관 건강에 구조적인 부담을 주고 있습니다. 특히 아시아태평양에서는 65세 이상 인구가 연간 4%의 속도로 증가하고 있습니다. 임상시험에 따르면, 고령자의 87.5%가 공기압식 압박 장치를 사용함으로써 삶의 질이 향상되었다고 보고했습니다. 메디케어의 2024년 림프부종 급여 제도로 인해, 미국에서는 비용 측면의 장벽이 해소되었습니다. 이러한 인구 동향의 필연성과 정책적 지원이 맞물리면서, 만성적인 부종 및 운동 기능 제한에 대한 압박 요법 솔루션의 보급 확대가 확실해질 것입니다.

환자의 치료 순응도 부족과 사용 시 불편감

치료 순응도 저하는 여전히 임상적 과제로 남아 있습니다. 조사에 따르면, 많은 환자들이 더위나 착용의 어려움 등을 이유로 몇 주 이내에 스타킹 사용을 중단하고 있습니다. SIGVARIS사는 흡습·발산성이 뛰어난 원사를 사용하거나 온도 조절 기능을 갖춘 가공 처리를 통해 착용자의 쾌적성을 높여 이 문제를 해결하고 있습니다. 현재는 디지털 컴패니언이 사용 현황을 추적하여, 처방된 착용 시간보다 적게 착용한 경우 의료진에게 알리는 시스템도 도입되어 있습니다. 재료 과학의 발전에 따라 치료 순응도와 관련된 장벽이 해소되고, 연평균 성장률(CAGR)에 미치는 부정적인 영향도 완화될 것으로 예측됩니다.

부문별 분석

2025년 매출액 중 정적 시스템이 67.74%를 차지하며, 기술별로는 압박 요법 시장에서 가장 큰 점유율을 기록했습니다. 다이나믹 펌프는 규모는 작지만, 병원 및 재택 간호 서비스 제공업체들이 압력 주기를 조절할 수 있는 장치로 전환함에 따라 연평균 성장률(CAGR) 5.68%로 성장을 지속하고, 있습니다. Kendall SCD SmartFlow 플랫폼은 혈관의 재충혈을 감지하여 치료를 개인화하고 시술 시간을 단축합니다. 압박 요법 업계에서는 스마트 텍스타일과 공기압 컨트롤러가 연동되는 기술적 융합이 진행되고 있으며, 이는 향후 하이브리드 솔루션의 등장을 예고하고 있습니다.

다이나믹형 기기는 임상 연구에서 뛰어난 부종 완화 효과와 환자의 쾌적성이 확인되었기 때문에 고가 제품군으로 제공되고 있습니다. 병원의 상처 치료 센터에서는 궤양 데브리드먼트 후 공기압식 슬리브를 사용하는 경우가 많으며, 재택 간호 기관에서는 만성 부종으로 고생하는 환자에게 휴대용 펌프를 대여해 주고 있습니다. 정적 랩은 비용이 저렴하고 사용법을 익히기 쉬워 여전히 널리 보급되어 있으며, 압박 요법 시장에서 핵심적인 수요를 유지하고 있습니다.

2025년 매출의 52.02%를 압박 의류가 차지하며, 일상 생활에서 가장 인기 있는 치료법으로서의 입지를 확고히 다졌습니다. 단계적 압박 스타킹이 판매량의 대부분을 차지하고 있지만, 림프부종 환자들 사이에서는 몸통용이나 팔용 슬리브도 주목을 받고 있습니다. 펌프 시장은 5.52%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. Tactile Medical사의 ‘Nimbl’ 시스템은 52주간의 임상시험에서 사지의 부피를 현저히 감소시키는 성과를 거두었습니다. 보험사의 임대 비용 상환 승인 및 원격 모니터링을 통한 치료 준수 확보가 진행됨에 따라, 펌프 분야의 압박 요법 시장 규모는 확대되고 있습니다.

브레이스와 랩은 특히 스포츠 정형외과 분야에서 제한적인 틈새 시장을 차지하고 있습니다. 제조업체들은 안정성과 압박 효과를 하나의 제품에서 모두 원하는 운동선수들의 관심을 끌기 위해, 브레이스에 흡습·발산성이 뛰어난 원단을 결합하는 경우가 많습니다. 예방 관리에 대한 소비자의 인식이 높아짐에 따라, 제품 라인은 패션성을 중시한 압박 양말 등으로 다양화되고 있으며, 이는 점진적인 성장을 뒷받침하는 동시에 압박 요법 시장에서 의류 제품의 우위를 더욱 공고히 하고 있습니다.

지역별 분석

북미는 메디케어에 의한 환급, 임상 지식의 광범위한 보급, 그리고 잘 구축된 유통 네트워크 덕분에 2025년 매출의 40.55%를 차지했습니다. 병원에서는 6개월마다 스타킹을 보충하고 있으며, 이는 지속적인 주문을 뒷받침하고 압박 요법 시장의 안정화에 기여하고 있습니다. 유럽에서는 공적 의료 제도 하에서 꾸준한 보급이 진행되고 있으며, 이에 발맞추어 나아가고 있습니다. 독일의 법정 건강보험 기금에서는 연간 2켤레의 의료용 스타킹을 보험 적용 대상으로 하고 있어, 예측 가능한 판매량을 확보하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 5.72%를 나타낼 것으로 전망됩니다. 고령화와 당뇨병 유병률의 상승이 맞물리면서, 정맥 및 림프계 합병증이 증가하고 있습니다. 현재 중국의 도시 지역 병원에서는 스마트 텍스타일 소재의 스타킹을 시범 도입하고 있으며, 일본의 재택 간병 업체에서는 고령 입소자를 위해 공기압 펌프가 내장된 제품을 도입하고 있습니다. 이러한 변화가 외국인 직접 투자를 유치하여 현지 제조 클러스터를 활성화시키고 있습니다.

남미 및 중동 및 아프리카에서는 보험 보상 제한과 수입 관세로 인해 성장이 억제되고 있습니다. 그렇긴 하지만, 의료진을 위한 교육 프로그램과 신흥 시장을 겨냥해 가격이 책정된 모듈식 펌프 덕분에 보급률은 서서히 높아지고 있습니다. 이 지역들에 혈관 관리 인프라가 구축됨에 따라, 압박 요법 시장의 판매량이 더욱 증가할 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the compression therapy market size in 2026 is estimated at USD 4.52 billion, growing from 2025 value of USD 4.31 billion with 2031 projections showing USD 5.76 billion, growing at 4.96% CAGR over 2026-2031.

This report is Segmented by Technology (Static Compression Therapy, Dynamic Compression Therapy), Product (Compression Garments, Compression Pumps, Compression Braces), Application (Venous Leg Ulcers, Deep Vein Thrombosis Treatment, and More), End User (Hospitals, Specialty Clinics, Home Care, Others), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Compression Therapy Market Trends and Insights

Rising prevalence of venous disorders and lymphedema

Chronic venous insufficiency affects 25 million adults in the United States, creating continuous demand for compression therapy as a first-line intervention . High-pressure graduated stockings prevent post-thrombotic syndrome, and 2025 SCAI clinical guidelines strongly endorse their use for venous ulcers . This formal backing stabilizes procurement plans for hospitals and payers. Persistent therapeutic need produces predictable replacement cycles, allowing manufacturers to plan capacity and sustain the compression therapy market over the long term.

Growing geriatric population

Population aging places structural pressure on vascular health, especially in Asia-Pacific where the 65+ cohort is climbing at 4% annually. Clinical trials show 87.5% of older adults report improved quality of life with pneumatic compression devices. Medicare's 2024 lymphedema benefit removes cost barriers in the United States. Together, demographic inevitability and policy support ensure expanding uptake of compression solutions for chronic swelling and mobility limitations.

Lack of patient compliance and discomfort during use

Non-adherence remains a clinical hurdle; surveys show many patients discontinue stockings within weeks due to heat and difficulty donning. SIGVARIS counters with moisture-wicking yarns and temperature-regulating finishes that improve wearer experience. Digital companions now track usage and alert clinicians when wear time falls below prescription. As material science advances, the compliance barrier is expected to recede, tempering the negative CAGR impact.

Other drivers and restraints analyzed in the detailed report include:

- Increasing awareness about compression therapy benefits

- Advancements in compression garments

- Limited reimbursement in developing markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Static systems accounted for 67.74% of 2025 revenue, giving them the largest compression therapy market share among technologies. Dynamic pumps, though smaller, are charting a 5.68% CAGR as hospitals and home-care providers migrate to devices that tailor pressure cycles. The Kendall SCD SmartFlow platform delivers vascular refill detection to personalize therapy and cut session times. The compression therapy industry is experiencing a technological convergence where smart textiles interface with pneumatic controllers, signaling future hybrid solutions.

Dynamic devices earn premium pricing because clinical studies cite superior edema reduction and patient comfort. Hospital wound centers frequently adopt pneumatic sleeves following ulcer debridement, while home-care agencies lease portable pumps to chronic-swelling patients. Static wraps remain prevalent for their low cost and ease of training, ensuring they retain core demand within the compression therapy market.

Compression garments generated 52.02% of 2025 revenue, cementing their role as the most popular modality for daily use. Graduated stockings constitute the bulk of volume, although torso and arm sleeves are gaining attention among lymphedema patients. Pumps are forecast to post the highest 5.52% CAGR; Tactile Medical's Nimbl system achieved meaningful limb-volume reductions in 52-week trials. The compression therapy market size for pumps is expanding as payers approve rental reimbursement and remote monitoring assures adherence.

Braces and wraps hold discreet niches, especially within sports orthopedics. Manufacturers often bundle braces with moisture-managing fabrics to attract athletes seeking stabilization and compression in one product. As consumer literacy on prophylactic care rises, product lines diversify to include fashion-oriented compression socks, fueling incremental growth and reinforcing garments' dominance in the compression therapy market.

Geography Analysis

North America contributed 40.55% of 2025 revenue due to Medicare reimbursement, broad clinical literacy, and well-developed distributor networks. Hospitals replenish stockings every six months, supporting recurring orders that stabilize the compression therapy market. Europe follows with consistent adoption under public health systems; Germany's statutory funds reimburse two pairs of medical stockings per year, ensuring predictable volume.

Asia-Pacific is forecast for a 5.72% CAGR through 2031. Aging demographics intersect with rising diabetes prevalence, elevating venous and lymphatic complications. Urban hospitals in China now pilot smart-textile stockings, while Japanese home-care providers integrate pneumatic pumps for aged residents. These shifts attract foreign direct investment and spur local manufacturing clusters.

In South America and the Middle East & Africa, growth is tempered by limited reimbursement and import duties. Nonetheless, physician education programs and modular pumps priced for emerging markets are gradually elevating penetration. As these regions upgrade vascular-care infrastructure, the compression therapy market is expected to capture incremental volume gains.

- Solventum

- Essity AB (BSN medical)

- medi

- SIGVARIS Group

- Tactile Systems Technology, Inc.

- Arjo AB (ArjoHuntleigh)

- DJO Global (Enovis Corporation)

- Smiths Group

- Hartmann Group

- Julius Zorn GmbH (Juzo)

- Gottfried Medical

- Bio Compression Systems

- Thuasne SAS

- Lohmann & Rauscher

- Cardinal Health

- Molnlycke Health Care

- DeRoyal Industries

- Koya Medical

- Hyperice

- LIPOELASTIC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of venous disorders and lymphedema

- 4.2.2 Growing geriatric population

- 4.2.3 Increasing awareness about compression therapy benefits

- 4.2.4 Advancements in compression garments

- 4.2.5 Expanding use in sports and fitness recovery

- 4.2.6 Favorable Reimbursement policies in developed markets

- 4.3 Market Restraints

- 4.3.1 Lack of patient compliance and discomfort during use

- 4.3.2 Limited reimbursement in developing markets

- 4.3.3 Availability of alternative therapies

- 4.3.4 High cost of advanced products

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 Static Compression Therapy

- 5.1.2 Dynamic Compression Therapy

- 5.2 By Product

- 5.2.1 Compression Garments

- 5.2.2 Compression Pumps

- 5.2.3 Compression Braces

- 5.3 By Application

- 5.3.1 Venous Leg Ulcers

- 5.3.2 Deep Vein Thrombosis Treatment

- 5.3.3 Lymphedema Treatment

- 5.3.4 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Specialty Clinics

- 5.4.3 Home Care

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.3.1 Solventum

- 6.3.2 Essity AB (BSN medical)

- 6.3.3 medi GmbH & Co. KG

- 6.3.4 SIGVARIS Group

- 6.3.5 Tactile Systems Technology, Inc.

- 6.3.6 Arjo AB (ArjoHuntleigh)

- 6.3.7 DJO Global (Enovis Corporation)

- 6.3.8 Smith & Nephew plc

- 6.3.9 Paul Hartmann AG

- 6.3.10 Julius Zorn GmbH (Juzo)

- 6.3.11 Gottfried Medical, Inc.

- 6.3.12 Bio Compression Systems, Inc.

- 6.3.13 Thuasne SAS

- 6.3.14 Lohmann & Rauscher GmbH & Co. KG

- 6.3.15 Cardinal Health, Inc.

- 6.3.16 Molnlycke Health Care AB

- 6.3.17 DeRoyal Industries, Inc.

- 6.3.18 Koya Medical

- 6.3.19 Hyperice

- 6.3.20 LIPOELASTIC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment