|

시장보고서

상품코드

2066573

원자력 발전 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Nuclear Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

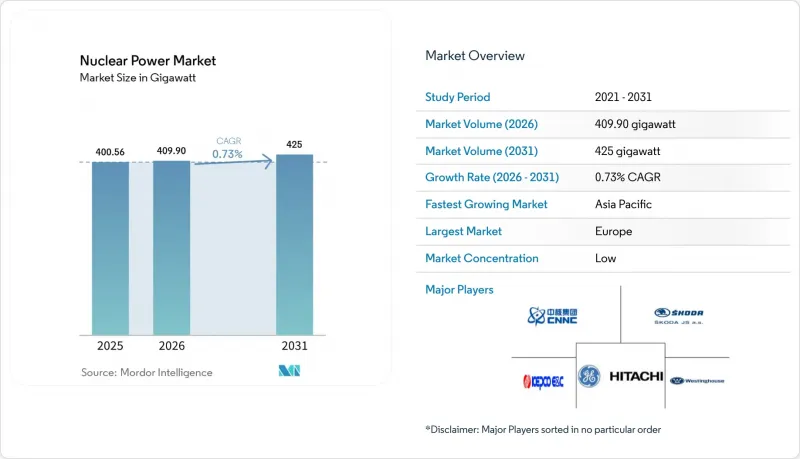

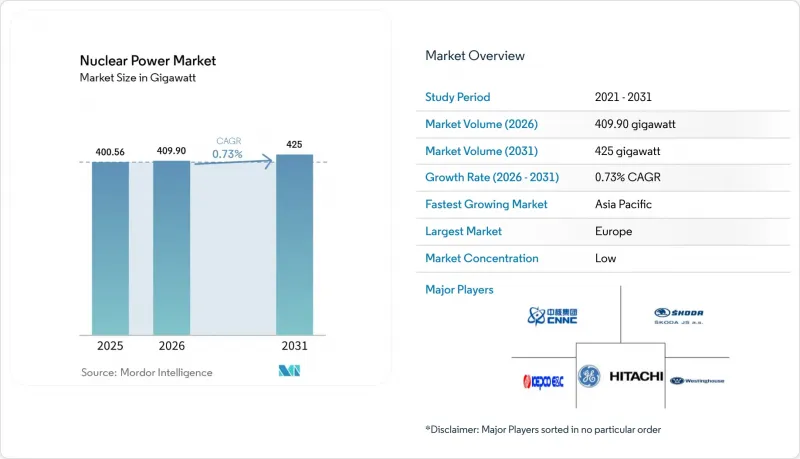

Mordor Intelligence에 의하면, 원자력발전 시장 규모는 2025년 400.56기가와트로 평가되었습니다. 2026년 409.90기가와트에서, 2031년까지 425기가와트로 확대될 것으로 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 0.73%를 나타낼 전망입니다.

본 보고서는 원자로 유형(가압경수로, 고속증식로 등), 원자로 규모(대형, 중형, 소형), 연료 유형(저농축 우라늄 등), 용도(계통 연계 발전, 산업용 공정 열·증기 등), 최종 사용자(전력 회사 및 독립 발전 사업자(IPP), 산업·석유화학 업계 등), 지역(유럽, 아시아태평양 등)에 따라 분류되어 있습니다.

세계의 원자력 발전 시장 동향 및 인사이트

청정 기저부하 전력에 대한 수요 증가

탄소 예산 축소를 추진하고 있는 각국 정부는 현재 원자력을, 간헐적인 재생에너지를 보완할 수 있을 만큼 충분히 빠르게 규모를 확대할 수 있는 유일한 조절 가능한 무배출 전력원으로 간주하고 있습니다. 프랑스의 2024년 에너지법에서는 6기의 신규 EPR2 원자로 건설이 의무화되어 있으며, 영국의 ‘그레이트 브리티시 뉴클리어’ 프로그램은 2050년까지 24GW를 목표로 하고 있으며, 또한, 미국의 ‘인플레이션 억제법’에 따른 생산 세액 공제는 규제 완화된 시장에서 프로젝트의 경제성을 높이고 있습니다. 이러한 조치들이 맞물려 지난 10년 동안 신규 건설을 웃도는 속도로 발전소 폐쇄가 진행되면서 약화되었던 투자 근거가 회복되고 있습니다. 또한, 영국의 규제 자산 기반 모델과 같은 현대적인 정책 수단을 통해, 과거에는 프로젝트 중단을 초래했던 차입 비용이 낮아짐에 따라 투자자들의 심리도 개선되고 있습니다. 그 결과, 세계 원자력 발전 시장은 각국의 탈탄소화 로드맵에서 다시금 중요한 위치를 차지하고 있으며, 특히 재생에너지 비중이 높은 시나리오에서 전력 저장 비용이 여전히 터무니없이 높은 수준인 지역에서는 그 중요성이 더욱 두드러지고 있습니다.

운행 기간 연장 및 출력 향상 프로그램

기존 원자로의 운전 수명을 40년에서 60년, 나아가 80년으로 연장함으로써 수십억 달러 규모의 대체 발전소 건설을 미룰 수 있습니다. 미국 원자력규제위원회(NRC)는 2024년부터 2025년에 걸쳐 11건의 운전 허가 갱신을 승인함으로써, 국내 원자로군의 평균 잔여 운전 연한을 28년으로 늘렸습니다. 프랑스의 494억 유로 규모 ‘그랑 카레나주’ 개보수 프로젝트 역시 신규 건설 비용의 극히 일부만으로 수십 년에 걸친 발전량을 확보하고 있습니다. 출력 향상 프로젝트에서는 설비 교체를 통해 발전량을 5-20% 증가시키고, 신규 건설에 수반되는 인허가 절차를 피함으로써, 대형 신규 원자로의 1MWh당 70달러 이상에 비해 1MWh당 30달러 미만의 균등화 발전 비용을 실현하고 있습니다. 그러나 이 전략은 원자로군의 노후화 위험을 집중시키기 때문에 비용 면에서의 우위를 훼손하는 예기치 못한 정지를 피하기 위해서는 탁월한 운영 관리와 예측 유지보수가 필수적입니다.

비용 초과와 자금 조달의 과제

높은 자본 비용과 건설 지연은 계속해서 투자자들의 신뢰를 훼손하고 있습니다. 보그톨 3·4호기는 예산의 2배 이상인 350억 달러를 투입해 가동을 시작했으며, 프랑스 플라망빌 3호기는 17년 동안 191억 유로를 소요했습니다. 이러한 비용 초과로 인해 신용등급이 하향 조정되었고, 정부는 전력회사의 대차대조표를 보증할 수밖에 없는 상황에 몰리게 되었습니다. 세계 최초의 기술적 위험, 공급망의 단절, 그리고 끊임없이 진화하는 안전 규제가 모두 비용의 급등을 초래하고 있습니다. 연속 건설을 통해 프로젝트 수행 능력이 향상되지 않는 한, 세계 원자력 발전 시장은 균등화 발전 원가 패리티를 여전히 달성하기 어려운 규제 완화 시장에서 더 저렴한 재생에너지에 시장 점유율을 빼앗길 위험에 직면하게 될 것입니다.

부문별 분석

가압경수로(PWR)는 표준화된 공급망과 수십 년에 걸친 운전 데이터를 바탕으로, 2025년에는 전 세계 원자력 발전 시장 점유율의 72.8%를 차지했습니다. 고속증식로는 규모는 작지만, 폐쇄형 연료 주기를 실증하는 러시아의 BN-800 및 중국의 CFR-600 프로그램에 힘입어 연평균 성장률(CAGR) 21.4%로 성장할 것으로 전망됩니다. 가압중수로의 설계는 천연 우라늄의 자급자족을 실현한다는 점에서 인도와 캐나다에 있어 여전히 전략적으로 중요합니다. 한편, 비등수형 원자로는 후쿠시마 사고 이후의 개보수로 인해 가동 중단 기간이 길어지고, 운전·유지보수(O&M) 비용이 증가함에 따라 뒤처지고 있습니다.

고속증식로의 상승세는 세계 원자력 발전 시장의 구조적 전환을 시사하고 있습니다. 증식로는 우라늄 1Kg당 최대 60배의 에너지를 추출할 수 있으므로, 수요 증가에 따라 자원 제약을 완화합니다. 또한, 플루토늄 비축분을 소모할 수 있는 능력은 핵비확산 목표와도 부합합니다. 그러나 복잡한 나트륨 냉각 시스템은 화재 예방상의 문제를 야기하며, 높은 건설 비용은 정부의 지원 없이는 도입을 가로막는 요인이 됩니다. 그 결과, 2031년까지는 경수로 설계가 규모의 경제성을 유지할 것으로 보이지만, 증식로의 부상은 경쟁에 긴장감을 불러일으킬 것이며, 2035년 이후에는 공급업체의 판도를 완전히 뒤바꿀 가능성이 있습니다.

2025년 세계 원자력 발전 시장 규모에서 500-1,000 MWe 규모의 중형 발전소가 가장 큰 점유율을 차지했으며, 규모의 경제와 계통 연계의 유연성 사이에서 균형을 이루었습니다. 그러나 500 MWe 미만의 소규모 원자로는 현장 작업 부담과 자금 조달 위험을 대폭 줄여주는 공장 생산 방식에 힘입어 연평균 성장률(CAGR) 20.1%로 급증할 것으로 전망됩니다.

자본 부담이 적은 모듈은 재무 기반이 취약한 신흥국에게 매력적이며, 반면 산업용 구매자는 자사 수요를 충당하기 위해 불과 수백 메가와트만 필요로 합니다. NuScale사의 77 MWe 모듈과 GE-히타치사의 300 MWe BWRX-300이 상용화를 위한 파이프라인의 핵심을 이루고 있습니다. 1,000 MWe를 초과하는 대형 원자로는 정책을 통해 장기적인 전력 구매가 보장될 경우 kW당 비용 측면에서 우위를 유지하고 있지만, 건설 기간이 10년에 달하기 때문에 투자자는 수요의 불확실성에 노출됩니다. 따라서 이러한 규모별 구분은 단순한 기술적 차이가 아니라, 대조적인 비즈니스 모델을 부각시키고 있습니다. 즉, 분산형 수요에 대응하기 위한 단계적인 증설 용량과, 집중형 송전망을 위한 대량의 베이스로드 공급의 차이입니다.

지역별 분석

2025년, 유럽은 발전 용량의 39.1%를 유지했으며, 그 중심에는 국내 전력의 65%를 공급하는 프랑스의 56기 원자로가 있습니다. 영국, 폴란드, 체코 공화국에서의 신규 건설이 독일과 벨기에에서의 원전 폐쇄를 상쇄하여, 2031년까지 해당 지역의 발전 용량을 안정적으로 유지했습니다. 프랑스는 2026년에 펜리에서 첫 번째 EPR2 원전의 토목 공사를 시작할 예정이며, 한편 영국의 힌클리 포인트 C는 노후화된 AGR 원자로를 대체하기 위해 2031년 가동을 목표로 하고 있습니다.

아시아태평양은 성장의 원동력이 되고 있으며, 2024년부터 2025년에 걸쳐 중국이 22기의 원자로를 가동했고 인도가 국산 700 MWe 중수로 2기를 가동함에 따라 연평균 성장률(CAGR) 7.2%로 확대되고 있습니다. 일본의 단계적 재가동과 한국의 정책 전환도 발전 용량 증가에 기여하고 있습니다. 이 지역의 규제 측면에서의 유연성과 정부 주도의 자금 조달 체계가, 자유화된 유럽 및 미국 시장보다 더 대규모의 프로젝트 파이프라인을 뒷받침하고 있습니다.

북미의 전망은 SMR 실증 실험에 달려 있습니다. 보글(Vogtle)의 AP1000형 원자로 2기로 2.2 GW가 추가되었지만, 향후 규모 확대는 테라파워(TerraPower)의 ‘나트륨(Natrium)’이나 온타리오 파워 제너레이션(Ontario Power Generation)의 ‘BWRX-300’과 같은 비용 분담형 실증 프로젝트의 성과에 달려 있습니다. 중동 및 아프리카는 도입 초기 단계에 있습니다. UAE의 바라카 발전소는 5.6GW의 기저부하 전력을 공급하고 있으며, 사우디아라비아에서는 2.8 GW 규모의 입찰을 위한 공급업체 사전 자격 심사가 진행되고 있습니다. 남미의 프로젝트 파이프라인은 브라질의 앙그라 3호기와 아르헨티나의 CAREM-25가 주를 이루고 있으며, 이 지역에 대해 신중하면서도 지속적인 관심을 보이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the nuclear power market size is projected to expand from 400.56 gigawatt in 2025 and 409.90 gigawatt in 2026 to 425 gigawatt by 2031, registering a CAGR of 0.73% between 2026 to 2031.

This report is Segmented by Reactor Type (Pressurized Light-Water Moderated and Cooled Reactor, Fast Breeder Reactor, and More), Reactor Size (Large, Medium, and Small), Fuel Type (Low-Enriched Uranium, and More), Application (Grid-Connected Power, Industrial Process Heat and Steam, and More), End-User (Utilities and IPPs, Industrial and Petro-Chemical, and More), and Geography (Europe, Asia-Pacific, and More).

Global Nuclear Power Market Trends and Insights

Increase in Demand for Clean Baseload Power

Governments tightening carbon budgets now view nuclear as the only dispatchable zero-emission source that can scale quickly enough to back up intermittent renewables. France's 2024 energy law mandates six new EPR2 units, the United Kingdom's Great British Nuclear program targets 24 GW by 2050, and U.S. production tax credits under the Inflation Reduction Act improve project economics in deregulated markets. These measures collectively restore an investment thesis that had eroded after a decade of retirements outpacing new builds. Investor sentiment is also improving because modern policy instruments, such as U.K. regulated asset-base models, lower borrowing costs that previously drove project cancellations. As a result, the Global nuclear power market is regaining relevance in national decarbonization roadmaps, particularly where storage costs for high-renewables scenarios remain prohibitive.

Lifetime Extension & Uprate Programs

Extending the operating life of existing reactors from 40 to 60 or even 80 years defers multi-billion-dollar replacement builds. The U.S. Nuclear Regulatory Commission approved 11 subsequent license renewals in 2024-2025, lifting the average remaining life of the domestic fleet to 28 years. France's EUR 49.4 billion Grand Carenage upgrades similarly add decades of output at a fraction of new-build cost. Uprate projects boost generation by 5-20% through equipment replacements that avoid greenfield permitting, achieving levelized costs below USD 30 per MWh versus more than USD 70 per MWh for new large reactors. This strategy, however, concentrates fleet-age risk, making operational excellence and predictive maintenance critical to avoid unplanned outages that erode cost advantages.

Cost Overruns & Financing Challenges

High capital costs and construction delays continue to erode investor confidence. Vogtle 3-4 entered service at USD 35 billion, more than double the budget, while France's Flamanville 3 consumed EUR 19.1 billion over 17 years. These overruns led to credit downgrades and forced governments to backstop utility balance sheets. First-of-a-kind engineering risk, supply-chain fragmentation, and evolving safety regulations all drive cost blowouts. Unless serial builds improve project delivery, the Global nuclear power market risks ceding ground to cheaper renewables in deregulated markets where levelized cost parity remains elusive.

Other drivers and restraints analyzed in the detailed report include:

- Commercialization of Advanced SMRs

- Industrial Decarbonization Process-Heat Demand

- HALEU Fuel-Supply Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pressurized light-water reactors captured 72.8% of the Global nuclear power market share in 2025, underpinned by standardized supply chains and decades of operational data. Fast breeder reactors, although a minor base, are forecast to grow at 21.4% CAGR, driven by Russia's BN-800 and China's CFR-600 programs that validate closed fuel cycles. Pressurized heavy-water designs remain strategically important for India and Canada, offering natural-uranium autonomy. Boiling water reactors lag due to post-Fukushima retrofits that extend outages and inflate O&M costs.

Fast breeder momentum signals a structural pivot for the Global nuclear power market. Breeders extract up to 60 times more energy per kilogram of uranium, easing resource constraints as demand climbs. Their ability to burn plutonium stockpiles also aligns with non-proliferation objectives. However, complex sodium-cooling systems pose fire-safety challenges, and high capital costs deter adoption without sovereign backing. Consequently, light-water designs will preserve scale advantage through 2031, but breeders introduce competitive tension that could reshape vendor landscapes after 2035.

Medium-sized plants between 500 and 1,000 MWe represented the largest slice of the Global nuclear power market size in 2025, balancing economies of scale with grid integration flexibility. Yet small reactors below 500 MWe are projected to surge at 20.1% CAGR, propelled by factory fabrication that slashes onsite labor and financing risk.

Capital-light modules appeal to emerging economies with weaker balance sheets, while industrial buyers need only a few hundred megawatts for captive loads. NuScale's 77 MWe module and GE-Hitachi's 300 MWe BWRX-300 anchor the commercial pipeline. Large reactors above 1,000 MWe retain a cost-per-kilowatt edge where policy guarantees long-term offtake, but decade-long build times expose sponsors to demand uncertainty. The size segmentation, therefore, emphasizes contrasting business models rather than mere engineering: incremental capacity for distributed demand versus bulk baseload for centralized grids.

Geography Analysis

Europe retained 39.1% of capacity in 2025, anchored by France's 56-unit fleet that supplied 65% of national electricity. New builds in the United Kingdom, Poland, and the Czech Republic offset retirements in Germany and Belgium, stabilizing the region's capacity through 2031. France started civil works on its first EPR2 at Penly in 2026, while Hinkley Point C in the U.K. targets a 2031 start to replace aging AGR reactors.

Asia-Pacific is the growth engine, expanding at 7.2% CAGR as China connected 22 reactors in 2024-2025 and India commissioned two indigenous 700 MWe heavy-water units. Japan's phased restarts and South Korea's policy reversal also add incremental capacity. The region's regulatory agility and sovereign financing structures underpin bigger project pipelines than in liberalized Western markets.

North America's outlook hinges on SMR demonstrations. Vogtle's two AP1000 units added 2.2 GW, but future scale depends on cost-shared pilots such as TerraPower's Natrium and Ontario Power Generation's BWRX-300. The Middle East and Africa are early-cycle adopters: the UAE's Barakah delivers 5.6 GW of baseload power, and Saudi Arabia has pre-qualified vendors for a 2.8 GW tender. South America's pipeline centers on Brazil's Angra 3 and Argentina's CAREM-25, signaling a cautious but persistent regional interest.

- Electricite de France SA (EDF)

- Rosatom State Atomic Energy Corporation

- China National Nuclear Corporation (CNNC)

- Westinghouse Electric Company LLC

- GE-Hitachi Nuclear Energy

- Framatome SA

- Mitsubishi Heavy Industries Ltd

- Korea Hydro & Nuclear Power / KEPCO E&C

- BWX Technologies Inc.

- Bechtel Corporation

- Doosan Enerbility Co. Ltd

- Fluor Corporation (NuScale)

- SKODA JS a.s.

- Holtec International

- TerraPower LLC

- Rolls-Royce SMR Ltd

- X-Energy LLC

- General Fusion Inc.

- Ontario Power Generation

- Babcock International Group

- Bilfinger SE

- Duke Energy Corporation

- Japan Atomic Power Company

- Ansaldo Nucleare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in demand for clean baseload power

- 4.2.2 Lifetime extension & uprate programs

- 4.2.3 Commercialization of advanced SMRs

- 4.2.4 Industrial decarbonization process-heat demand

- 4.2.5 Nuclear-produced hydrogen & ammonia initiatives

- 4.2.6 Emergence of nuclear-powered data-center & marine applications

- 4.3 Market Restraints

- 4.3.1 Cost overruns & financing challenges

- 4.3.2 Competition from low-cost renewables

- 4.3.3 HALEU fuel-supply bottlenecks

- 4.3.4 Export-control & proliferation scrutiny

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Reactor Type

- 5.1.1 Pressurized Light-Water Moderated and Cooled Reactor (PWR)

- 5.1.2 Pressurized Heavy-Water Moderated and Cooled Reactor (PHWR)

- 5.1.3 Boiling Light-Water Cooled and Moderated Reactor (BWR)

- 5.1.4 Gas Cooled, Graphite Moderated Reactor (GCR)

- 5.1.5 High-Temperature Gas-Cooled Reactor (HTGR)

- 5.1.6 Light-Water Cooled, Graphite Moderated Reactor (LWGR)

- 5.1.7 Fast Breeder Reactor (FBR)

- 5.1.8 Others

- 5.2 By Reactor Size

- 5.2.1 Large (Above 1,000 MWe)

- 5.2.2 Medium (500 to 1,000 MWe)

- 5.2.3 Small (Below 500 Mwe; includes SMRs and Micro-reactors)

- 5.3 By Fuel Type

- 5.3.1 Low-Enriched Uranium (Below 5% U-235)

- 5.3.2 High-Assay LEU (5 to 20% U-235)

- 5.3.3 Mixed Oxide (MOX)

- 5.3.4 Thorium-based Fuels

- 5.4 By Application

- 5.4.1 Grid-Connected Power

- 5.4.2 Off-grid/Remote Electrification

- 5.4.3 Industrial Process Heat and Steam

- 5.4.4 Desalination and District Heating

- 5.4.5 Defense and Military Bases

- 5.5 By End-User Sector

- 5.5.1 Utilities and IPPs

- 5.5.2 Industrial and Petro-chemical

- 5.5.3 Mining and Remote Operations

- 5.5.4 Government/Defense

- 5.5.5 Research Institutions

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Sweden

- 5.6.2.4 Spain

- 5.6.2.5 Ukraine

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 South Africa

- 5.6.5.3 Egypt

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Electricite de France SA (EDF)

- 6.4.2 Rosatom State Atomic Energy Corporation

- 6.4.3 China National Nuclear Corporation (CNNC)

- 6.4.4 Westinghouse Electric Company LLC

- 6.4.5 GE-Hitachi Nuclear Energy

- 6.4.6 Framatome SA

- 6.4.7 Mitsubishi Heavy Industries Ltd

- 6.4.8 Korea Hydro & Nuclear Power / KEPCO E&C

- 6.4.9 BWX Technologies Inc.

- 6.4.10 Bechtel Corporation

- 6.4.11 Doosan Enerbility Co. Ltd

- 6.4.12 Fluor Corporation (NuScale)

- 6.4.13 SKODA JS a.s.

- 6.4.14 Holtec International

- 6.4.15 TerraPower LLC

- 6.4.16 Rolls-Royce SMR Ltd

- 6.4.17 X-Energy LLC

- 6.4.18 General Fusion Inc.

- 6.4.19 Ontario Power Generation

- 6.4.20 Babcock International Group

- 6.4.21 Bilfinger SE

- 6.4.22 Duke Energy Corporation

- 6.4.23 Japan Atomic Power Company

- 6.4.24 Ansaldo Nucleare

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Advanced Small Modular Reactors

- 7.3 Floating Nuclear Plants

- 7.4 Nuclear Hydrogen & Ammonia Production

- 7.5 Data-Center & Marine Micro-reactors

- 7.6 Lifetime Extension Services Market

- 7.7 Decommissioning & Waste-Management Services