|

시장보고서

상품코드

2066579

커넥티드카 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Connected Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

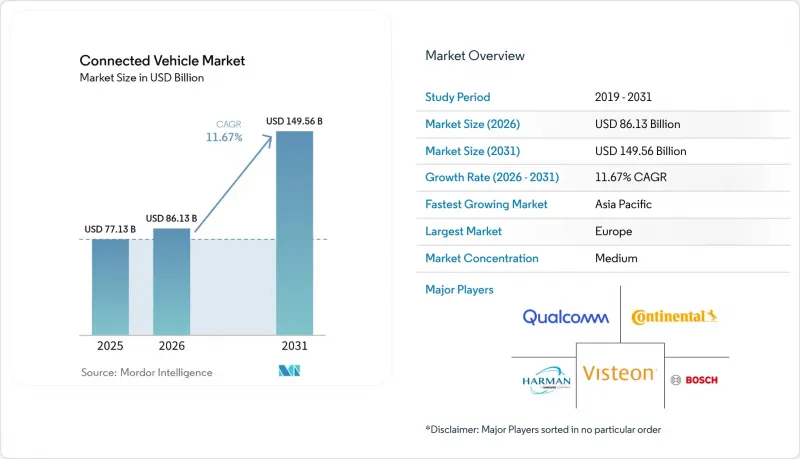

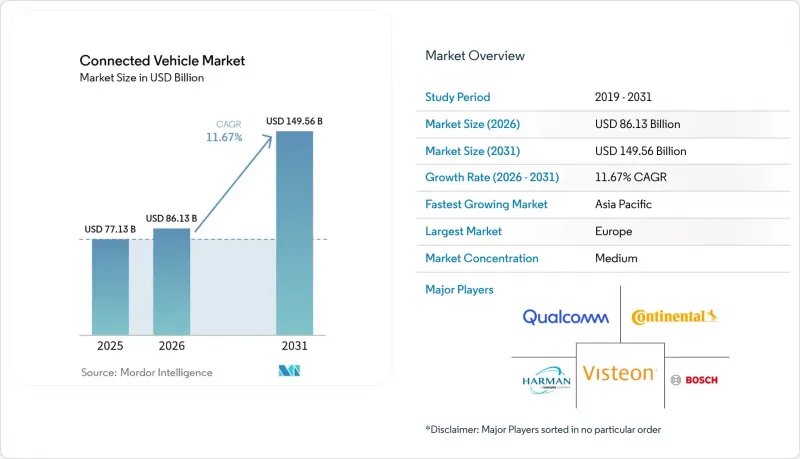

Mordor Intelligence에 의하면, 커넥티드카 시장 규모는 2025년 771억 3,000만 달러로 평가되었습니다. 2026년에는 861억 3,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 11.67%로 성장을 지속하여, 2031년에는 1,495억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 기술 유형(5G/C-V2X, 4G/LTE, 3G, 2G), 용도(운전 지원, 안전 및 보안, 텔레매틱스·진단, 기타), 연결 방식(통합형, 내장형, 테더링형), 차량 간 연결(V2V, V2I, V2P, V2C, V2G), 차종 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(대) 단위로 제시되어 있습니다.

세계의 커넥티드카 시장 동향 및 인사이트

전 세계 5G의 확산이 고대역폭 V2X 서비스를 실현합니다.

2024년 이후, 3GPP Release 16의 사이드링크 기능을 통해 지연 시간이 극히 짧은 차량 간(V2V) 직접 통신이 가능해졌습니다. 2025년 말까지, 다수의 5G 기지국을 가동 중인 중국이 주도적인 역할을 수행했으며, 많은 기지국이 C-V2X의 도로 측 기능을 뒷받침하게 되었습니다. 보행자 안전을 강화하기 위해 한국은 2025년에 막대한 자금을 투입해 다수의 교차로를 저지연 V2X 기술로 업그레이드했습니다. 한편, 미국에서는 연방고속도로청이 2025년에 주요 주간고속도로변에 여러 개의 도로변 장비를 설치하고, 화물 운송 회랑의 디지털화 노력을 강조했습니다. 이러한 발전 덕분에 차량은 현재 무선 펌웨어 업데이트, 고해상도 지도 정보, 그리고 적시에 제공되는 위험 경보의 혜택을 누릴 수 있게 되었습니다.

eCall 및 안전 텔레매틱스에 관한 규제 요건

2025년 1월에 발효된 유럽위원회 위임규정 2024/1180에 따라, 모든 신형 경차는 회선 교환 방식의 eCall에서 패킷 교환 방식의 IMS 네트워크로 전환해야 하며, 2G 및 3G 모뎀을 4G 또는 5G 칩셋으로 교체해야 합니다. 인도의 AIS-140 개정 제3호에 따르면, 2026년 4월까지 승용차에도 실시간 추적 기능 및 비상 버튼 요건이 적용되게 되어, 규정 준수에 대한 수요가 더욱 높아지고 있습니다. 러시아의 ERA-GLONASS 업그레이드에서는 2024년에 LTE 위치 측정 기능이 추가되었으며, 규제 최저 기준이 더욱 강화되었습니다. 이러한 규정은 최소한의 연결성을 보장하는 한편, UNECE WP.29 규정 155가 형식 승인 전에 인증된 사이버 보안 관리 시스템의 도입을 의무화하고 있기 때문에 엔지니어링 비용 증가를 초래하고 있습니다. 중소 OEM 기업들은 경쟁력을 유지하기 위해 이미 ISO/SAE 21434 인증을 취득한 Tier 1 공급업체와 제휴해야 합니다.

사이버 보안 및 데이터 개인정보 보호의 취약점

최근 유럽 사이버보안청은 커넥티드카의 게이트웨이를 표적으로 한 여러 건의 악용 사례를 보고했습니다. 여기에는 여러 차종에 영향을 미친 원격 잠금 해제 및 이모빌라이저에 대한 공격이 포함되어 있었습니다. ISO/SAE 21434는 프로세스 프레임워크를 제공하지만, TUV SUD의 감사 결과 상당수의 2차 공급업체가 이 표준을 완전히 준수하지 않는 것으로 드러나 잠재적인 취약점이 부각되었습니다. 일반 데이터 보호 규정(GDPR(EU 개인정보보호규정))은 막대한 벌금을 부과함으로써 과도한 데이터 수익화에 대한 억제력으로 작용하고 있습니다. 한편, 캘리포니아주 소비자 개인정보 보호법(CCPA)은 운전자가 자신의 주행 기록을 삭제해 달라고 요청할 권리를 인정하고 있어, 주행 거리 기반 보험 모델에 복잡성을 더하고 있습니다. 이에 대응하기 위해 OEM은 하드웨어 기반의 신뢰의 근원(Root of Trust) 모듈과 종단 간암호화를 도입하고 있습니다. 그러나 규정 준수 대응에 따른 부담으로 인해 신기능 도입이 지연되고 있으며, 연구개발(R&D) 예산이 방어적인 기술 대책에 할당되고 있습니다.

부문별 분석

4G/LTE 부문은 성숙기에 접어든 부품 가격과 전 세계적인 네트워크 커버리지의 혜택을 받아, 2025년 커넥티드카 시장 규모에서 43.47%의 점유율을 유지했습니다. 그러나 각 OEM 업체들이 자율주행 및 첨단 운전자 보조 시스템에 필수적인 지연 시간 개선을 추구하는 가운데, 5G/C-V2X를 탑재한 차량은 2031년까지 연평균 성장률(CAGR) 11.69%로 급속히 확대되고 있습니다. 2025년에 발표된 퀄컴의 ‘Snapdragon X85’는 4나노미터 공정으로 사이드링크 및 mm파 무선 기능을 통합하여, 기존의 디스크리트 설계에 비해 전력 소비를 소폭 줄이고 부품 원가를 35달러 절감했습니다. 기존의 3G 및 2G 기기는 지속적인 운영이 어려워질 미국 및 EU의 서비스 종료 일정에 맞추어 단계적으로 폐지되고 있습니다.

고급 승용차의 경우, 소형 상용차에 비해 5G 채택률이 2배 더 높은 반면, 화물 운송 업체에서는 여전히 전자 로그 기록 장치와 결합된 견고한 4G 칩셋이 선호되고 있습니다. 중국에서는 신에너지 차량에 LTE-V2X 탑재가 의무화되어 있어 4G 수요가 여전히 높은 수준을 유지하고 있지만, 유럽에서는 5G NR-V2X로의 전환이 빠르게 진행되고 있습니다. Release 14의 사이드링크와 Release 17의 위치 측정에 대응하는 듀얼 모드 반도체의 비용은 2023년 50달러에서 15달러로 하락했으며, 이는 지역을 초월한 세계 플랫폼 표준화를 촉진하고 있습니다. 규모의 경제가 확대됨에 따라, 커넥티드카 시장에서는 2028년까지 5G 모뎀의 점유율이 4G를 넘어설 것으로 예상되며, 이에 따라 공급망과 반도체 로드맵이 재편될 전망입니다.

2025년에는 규제에 따른 eCall 의무화로 인해 기초 수요가 확고해짐에 따라, 안전 및 보안 관련 서비스가 커넥티드카 시장 규모의 38.13%를 차지했습니다. 무선 업데이트(OTA)는 연평균 성장률(CAGR) 11.77%라는 가장 급격한 성장세를 보이고 있으며, 이는 수 기가바이트 규모의 펌웨어 패키지를 수신할 수 있는 소프트웨어 정의 차량으로의 전환을 반영한 것입니다. 2025년에는 테슬라 차량군에서만 4페타바이트 이상의 센서 데이터가 업로드되어, 클라우드 기반 훈련 및 기능의 신속한 출시가 가능해졌습니다. 운전 보조 기능은 V2X 피드와 통합되어 있으며, 예를 들어 BMW의 ‘하이웨이 어시스턴트’는 도로변 장치에서 스트리밍되는 실시간 공사 구간 데이터를 적응형 속도 프로파일에 반영하게 되었습니다.

인포테인먼트 및 휴먼-머신 인터페이스(HMI) 기능은 Apple CarPlay와 Android Auto의 지배 하에 상품화가 진행되면서, 각 OEM 업체들의 차별화 요소가 줄어들고 있습니다. 모빌리티 및 차량 관리 용도는 수백만 대에 달하는 상용 차량의 경로 최적화, 규정 준수, 유지보수를 최적화하는 대규모 공급업체를 중심으로 통합이 진행되고 있습니다. 한편, 텔레매틱스 및 진단 기능은 애프터마켓용 동글에서 차량 상태 데이터를 클라우드 분석으로 스트리밍하는 공장 출고 시 탑재된 게이트웨이로 전환되면서, 예정에 없던 정비 방문을 줄이고 있습니다. 단 한 번의 업데이트로 보안, 주행 성능, 엔터테인먼트를 하나의 페이로드로 처리할 수 있게 되면서, 기존 용도의 사일로화가 해소되고 있으며, 통합된 소프트웨어 파이프라인의 중요성이 점점 더 커지고 있습니다.

지역별 분석

2025년, 유럽은 커넥티드카 시장 점유율의 34.57%를 차지하며 압도적인 우위를 보였습니다. 이러한 급증은 eCall의 패킷 교환 방식 전환 기한과 다수의 C-Roads 도로변 장비 도입에 힘입어 이루어졌습니다. 이 장치들은 독일, 오스트리아, 네덜란드 전역에 걸쳐 위험 경보를 발령하고 있습니다. 독일은 아우토반을 따라 수많은 가동 중인 설비가 설치되어 있어, 가장 높은 설치 밀도를 자랑하고 있습니다. 반면, 영국에서는 브렉시트 이후 규제상의 차이로 인해 도입이 지연되고 있습니다. 남유럽 국가들에서는 이용료에 대한 소비자들의 거부감으로 인해 도입 속도가 둔화되고 있습니다.

아시아태평양은 2031년까지의 연평균 성장률(CAGR)이 11.75%로 가장 높은 성장세를 보이고 있습니다. 이는 중국이 신에너지 차량에 LTE-V2X 탑재를 의무화하고, 우시, 창사, 충칭에서 V2X 인프라 구축을 추진하고 있기 때문입니다. 우시에 설치된 1,200대의 도로변 장치를 통해 2025년에는 교차로 사고가 감소했으며, 안전 측면에서의 효과가 입증되었습니다. 일본과 한국은 수백 곳의 교차로를 개보수하는 도시 지역 V2X 시범 사업에 자금을 지원하고 있습니다. 한편, 인도의 AIS-140 개정 제3호에 따라 2026년까지 승용차에 대한 실시간 추적 범위가 확대됨에 따라 규정 준수를 촉진하는 요인이 추가될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the connected vehicle market size is expected to grow from USD 77.13 billion in 2025 to USD 86.13 billion in 2026 and is forecast to reach USD 149.56 billion by 2031 at an 11.67% CAGR over 2026-2031.

This report is Segmented by Technology Type (5G/C-V2X, 4G/LTE, 3G, and 2G), Application (Driver Assistance, Safety and Security, Telematics and Diagnostics, and More), Connectivity (Integrated, Embedded, and Tethered), Vehicle Connectivity (V2V, V2I, V2P, V2C, and V2G), Vehicle Type, and Geography. Market Forecasts are Provided in Value (USD) and Volume (Units).

Global Connected Vehicle Market Trends and Insights

Global 5G Roll-Outs Enabling High-Bandwidth V2X Services

Since 2024, the 3GPP Release 16 sidelink feature has enabled direct vehicle-to-vehicle messaging with extremely low latency. By the end of 2025, China, with a significant number of active 5G base stations, will lead the charge, with many stations facilitating C-V2X roadside functions . In a bid to enhance pedestrian safety, South Korea allocated substantial funding in 2025 to upgrade numerous intersections with low-latency V2X technology. Meanwhile, in the U.S., the Federal Highway Administration underscored its commitment to digitizing freight corridors by adding several roadside units along a major interstate in 2025 . Due to these advancements, vehicles can now benefit from over-the-air firmware updates, high-definition mapping, and timely hazard alerts.

Regulatory Mandates For eCall & Safety Telematics

European Commission Delegated Regulation 2024/1180, effective January 2025, compels all new light vehicles to migrate from circuit-switched eCall to packet-switched IMS networks, forcing the replacement of 2G and 3G modems with 4G or 5G chipsets . India's AIS-140 Amendment 3 extends real-time tracking and panic-button requirements to passenger cars by April 2026, deepening compliance demand. Russia's ERA-GLONASS upgrade added LTE positioning in 2024, further solidifying the regulatory floor. These rules guarantee baseline connectivity but also raise engineering costs, since UNECE WP.29 Regulation 155 mandates a certified cyber-security management system before type approval. Smaller OEMs must now partner with tier-1 suppliers that already hold ISO/SAE 21434 certification to stay competitive.

Cyber-Security & Data-Privacy Vulnerabilities

In recent times, the European Union Agency for Cybersecurity reported several exploits targeting connected-vehicle gateways. These included remote unlock and immobilizer attacks affecting multiple vehicle models. While ISO/SAE 21434 provides a framework for processes, a TUV SUD audit revealed that a significant portion of tier-2 suppliers were not fully compliant, highlighting potential vulnerabilities. The General Data Protection Regulation (GDPR) imposes substantial fines, acting as a deterrent against aggressive data monetization. Meanwhile, the California Consumer Privacy Act empowers drivers to request the deletion of their trip records, adding complexity to usage-based insurance models. In response, Original Equipment Manufacturers (OEMs) are implementing hardware root-of-trust modules and end-to-end encryption. However, the weight of compliance is delaying the rollout of new features and redirecting R&D budgets towards defensive engineering measures.

Other drivers and restraints analyzed in the detailed report include:

- Smart-Infrastructure Funding In United States, European Union, And China

- Consumer Demand for In-Car Infotainment & Connectivity

- High Cellular Data Costs And OEM-MNO Revenue Conflicts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 4G/LTE segment maintained a 43.47% slice of the connected vehicle market size in 2025, benefiting from mature component pricing and global network coverage. However, 5G/C-V2X units are scaling fast with an 11.69% CAGR through 2031 as OEMs chase latency improvements vital for autonomous driving and advanced driver assistance. Qualcomm's Snapdragon X85, announced in 2025, integrates sidelink and millimeter-wave radios on a 4-nanometer node, cutting power draw by a minimal amount and reducing bill-of-materials by USD 35 relative to earlier discrete designs. Legacy 3G and 2G devices are being sunset, aligning with U.S. and EU shutdown schedules that make continued operation unsustainable.

Premium passenger cars adopt 5G twice as often as light commercial vehicles, but freight operators still favor robust 4G chipsets paired with electronic logging devices. China's mandate for LTE-V2X in new-energy vehicles keeps 4G volumes high, while Europe leans straight into 5G NR-V2X. Dual-mode silicon that supports Release 14 sidelink and Release 17 positioning now adds only USD 15, down from USD 50 in 2023, helping global platforms standardize across regions. As economies of scale build, the connected vehicle market expects 5G modems to overtake 4G share before 2028, reshaping supply chains and semiconductor roadmaps.

Safety and security services held 38.13% of the connected vehicle market size in 2025 as regulatory eCall mandates locked in baseline demand. Over-the-air updates post the quickest climb at an 11.77% CAGR, reflecting the move to software-defined vehicles capable of receiving multi-gigabyte firmware packages. Tesla's fleet alone uploaded more than 4 petabytes of sensor data in 2025, enabling cloud training and rapid feature releases. Driver assistance merges with V2X feeds, as BMW's Highway Assistant now factors real-time work-zone data streamed from roadside units into adaptive speed profiles.

Infotainment and human-machine interface functions are commoditizing under Apple CarPlay and Android Auto dominance, compressing OEM differentiation. Mobility and fleet-management applications consolidate around scaled providers that optimize routing, compliance, and maintenance for millions of commercial vehicles. Meanwhile, telematics and diagnostics shift from aftermarket dongles to factory-installed gateways that stream health data to cloud analytics, cutting unscheduled service visits. Traditional application silos blur as a single update can address security, driveability, and entertainment in one payload, underscoring the growing importance of unified software pipelines.

Geography Analysis

Europe dominated with 34.57% of the connected vehicle market share in 2025. This surge was driven by the eCall packet-switched migration deadlines and the deployment of numerous C-Roads roadside units. These units stream hazard alerts across Germany, Austria, and the Netherlands. Germany boasts the highest density with a significant number of active units along its Autobahn corridors. In contrast, the United Kingdom faces delays, grappling with post-Brexit regulatory differences. Southern European nations are adopting at a slower pace, hindered by consumer resistance to subscription fees.

Asia Pacific posts the fastest 11.75% CAGR through 2031 as China mandates LTE-V2X on new-energy vehicles and channels into V2X infrastructure across Wuxi, Changsha, and Chongqing. Wuxi's 1,200 roadside units cut intersection accidents in 2025, proving safety dividends. Japan and South Korea fund urban V2X pilots that retrofit hundreds of intersections, while India's AIS-140 Amendment 3 extends real-time tracking to passenger cars by 2026, adding a compliance driver.

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Visteon Corporation

- Samsung Electronics (HARMAN)

- Qualcomm Technologies Inc.

- NXP Semiconductors

- Aptiv PLC

- ZF Friedrichshafen AG

- Magna International

- Infineon Technologies AG

- AT&T Inc.

- Verizon Communications Inc.

- TomTom N.V.

- Tesla Inc.

- Toyota Motor Corporation

- BMW Group

- Ford Motor Company

- General Motors Company

- Huawei Technologies Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global 5G Roll-Outs Enabling High-Bandwidth V2X Services

- 4.2.2 Regulatory Mandates for Ecall & Safety Telematics

- 4.2.3 Smart-Infrastructure Funding in US, EU, China

- 4.2.4 Consumer Demand for In-Car Infotainment & Connectivity

- 4.2.5 EV-Centric Software-Defined Vehicle Architectures

- 4.2.6 Insurance-OEM Usage-Based-Insurance Partnerships

- 4.3 Market Restraints

- 4.3.1 Cyber-Security & Data-Privacy Vulnerabilities

- 4.3.2 High Cellular Data-Costs And OEM - MNO Revenue Conflicts

- 4.3.3 Semiconductor Modem Shortages

- 4.3.4 DSRC Vs C-V2X Spectrum Uncertainty

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Technology Type

- 5.1.1 5G / C-V2X

- 5.1.2 4G / LTE

- 5.1.3 3G

- 5.1.4 2G

- 5.2 By Application

- 5.2.1 Driver Assistance (ADAS)

- 5.2.2 Safety and Security

- 5.2.3 Telematics & Diagnostics

- 5.2.4 Infotainment & HMI

- 5.2.5 Mobility & Fleet Management

- 5.2.6 Over-the-Air (OTA) Updates

- 5.3 By Connectivity

- 5.3.1 Integrated

- 5.3.2 Embedded

- 5.3.3 Tethered

- 5.4 By Vehicle Connectivity

- 5.4.1 Vehicle-to-Vehicle (V2V)

- 5.4.2 Vehicle-to-Infrastructure (V2I)

- 5.4.3 Vehicle-to-Pedestrian (V2P)

- 5.4.4 Vehicle-to-Cloud (V2C)

- 5.4.5 Vehicle-to-Grid (V2G)

- 5.5 By Vehicle Type

- 5.5.1 Passenger Cars

- 5.5.2 Light Commercial Vehicles

- 5.5.3 Medium and Heavy Commercial Vehicles

- 5.6 By End Market

- 5.6.1 OEM-Fitted

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 South Africa

- 5.7.5.4 Turkey

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 Denso Corporation

- 6.4.4 Visteon Corporation

- 6.4.5 Samsung Electronics (HARMAN)

- 6.4.6 Qualcomm Technologies Inc.

- 6.4.7 NXP Semiconductors

- 6.4.8 Aptiv PLC

- 6.4.9 ZF Friedrichshafen AG

- 6.4.10 Magna International

- 6.4.11 Infineon Technologies AG

- 6.4.12 AT&T Inc.

- 6.4.13 Verizon Communications Inc.

- 6.4.14 TomTom N.V.

- 6.4.15 Tesla Inc.

- 6.4.16 Toyota Motor Corporation

- 6.4.17 BMW Group

- 6.4.18 Ford Motor Company

- 6.4.19 General Motors Company

- 6.4.20 Huawei Technologies Co. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment