|

시장보고서

상품코드

2066583

섬유 강화 폴리머(FRP) 복합재료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Fiber-Reinforced Polymer (FRP) Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

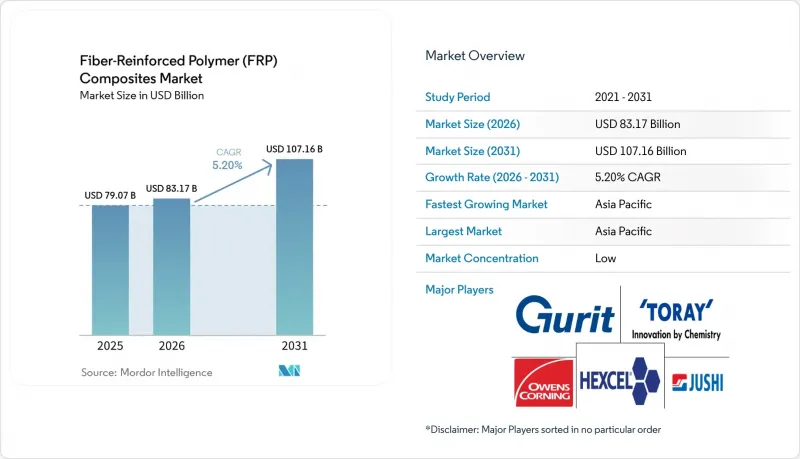

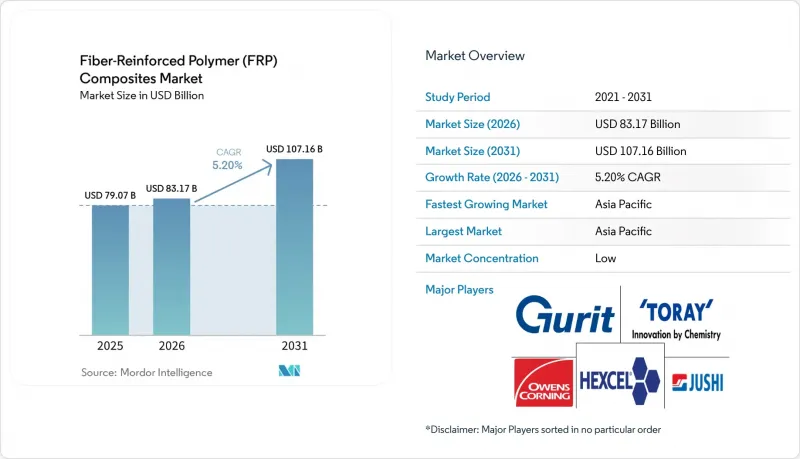

Mordor Intelligence에 의하면, 섬유 강화 폴리머 복합재료 시장 규모는 2025년 790억 7,000만 달러에서 2026년에는 831억 7,000만 달러로 확대되어 2031년까지 1,071억 6,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 5.20%로 성장할 전망입니다.

본 보고서는 수지 유형(열경화성 수지 및 열가소성 수지), 섬유 유형(유리섬유 강화 폴리머(GFRP), 탄소섬유 강화 폴리머(CFRP) 등), 보강재 형태(로빙, 프리프레그 등), 최종 사용 산업(운송, 건축 및 건설, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다.

세계 섬유 강화 폴리머(FRP) 복합재료 시장 동향 및 인사이트

건설 지출이 부식이 없는 철근 및 교량 데크판으로 전환

미국, 일본 및 걸프 연안 국가들의 관련 기관들은 염화물에 의한 부식으로 인한 교량의 수명 단축을 방지하기 위해, 유리섬유 및 현무암 섬유로 만든 철근을 사양으로 채택하는 경향이 강해지고 있습니다. 2025년 기준으로, 미국 내 61만 7,000개의 교량 중 42%가 건설된 지 50년 이상 되었으며, 부식으로 인한 보수 비용은 연간 83억 달러에 달할 전망입니다. 따라서 GFRP를 활용한 보수 공사는 수명 주기 비용 측면에서 35%의 우위를 차지합니다. 일본에서는 도쿄만 아쿠아라인 일대에서 15년에 걸친 노출 시험이 성공적으로 완료됨에 따라, 연안 지역의 고속도로에서 FRP 철근의 사용이 의무화되었습니다. 사우디아라비아의 NEOM 프로젝트에서는 주변 온도 45°C의 환경에서 강재의 산화를 방지하기 위해 콘크리트 구조물의 80%에 GFRP를 채택했습니다. 인발 성형된 교량 상판은 철근 콘크리트에 비해 무게가 75% 가볍고, 기초를 최대 30%까지 줄일 수 있으며, 2025년에는 웨스트버지니아주 2번 국도에서 40년의 설계 수명이 입증되었습니다.

120미터를 넘는 풍력 터빈 블레이드에는 초고강도 GFRP가 요구됩니다.

터빈 제조업체들은 현재 로터 직경이 240m를 넘는 기종을 도입하고 있으며, 이에 따라 블레이드 길이는 120m를 초과하게 되어 인장 강도가 1,200 MPa를 넘는 스파 캡이 필요하게 되었습니다. 베스타스는 2024년, 고탄성률 유리섬유를 채택한 115.5m 길이의 블레이드를 장착한 15MW 터빈을 발표했습니다. 이를 통해 블레이드 1개당 질량을 8t 줄였습니다. 중국에서는 2025년에 75GW 규모의 풍력 발전 설비가 도입되었으며, 그중 60%가 해상 풍력 발전이었습니다. 또한, 각 제조업체들은 1,000만 사이클의 피로 하중을 견딜 수 있도록, 기공률이 낮은 수지 전사 성형(RTM) 방식으로의 전환을 추진하고 있습니다. 지멘스 가메사의 열가소성 수지 소재 ‘RecyclableBlade’는 95%의 재료 회수율을 달성했으며, EU의 2028년 재활용 규정을 준수하고 있습니다.

탄소섬유 가격 변동이 자동차 업계의 원가 목표를 위협하고 있습니다.

러시아산 폴리아크릴로니트릴의 수출 규제로 인해 2025년에 전구체 가격이 18% 상승할 전망이며, 이에 따라 각 OEM 업체들은 1kg당 4-6달러의 가격 인상분을 감당할 수밖에 없게 되어, 3만 5,000달러 미만의 전기차 프로그램이 위태로워지고 있습니다. 도요타는 이익률을 유지하기 위해 2026년형 프리우스에 채택할 예정이었던 CFRP 재질의 루프 패널을 알루미늄 재질로 변경했습니다. SGL 카본과 도레이는 2024년 현물 가격보다 12% 높은 수준에서 5년간의 구매 계약을 체결하고, 가격 변동 위험을 업스트림 단계로 전가했습니다. ELG의 재생 섬유는 버진 섬유보다 비용이 40% 저렴하고 강도의 90%를 유지하지만, 비구조 부품에만 사용할 수 있습니다. 헥셀은 유럽의 에너지 가격 급등으로 인한 영향을 완화하기 위해, 전구체 생산량의 30%를 저비용의 미국 생산 기지로 이전했습니다.

부문별 분석

2025년 매출액 중 열경화성 수지가 71.06%를 차지했으며, 내식성과 저비용의 오픈 몰드 가공이 요구되는 에폭시 및 폴리에스터계 소재가 주류를 이루었습니다. 에폭시는 뛰어난 접착력 덕분에 항공우주용 프리프레그에서 탄소섬유와의 궁합을 높여주어, 열경화성 수지 수요의 대부분을 차지했습니다. 폴리에스터는 비용 효율을 중시하는 선박 및 탱크 시장에서 채택되었으며, 비닐에스테르는 부식성이 매우 높은 화학 플랜트에서 활용되었습니다.

자동차 제조업체들이 재활용 가능한 소재로의 전환을 추진하는 가운데, 열가소성 수지는 2031년까지 연평균 성장률(CAGR) 6.15%를 기록하며 성장할 것으로 전망됩니다. 유리 섬유를 40% 배합한 폴리프로필렌 컴파운드는 현재 도어 모듈 캐리어로 채택되어 있으며, 무게를 35% 줄이고 연간 생산량 50만 개 이상에서 90초 성형을 실현하고 있습니다. 폴리아미드 6 및 66은 최고 150°C의 환경에서 작동하는 엔진룸 내부 부품용 열가소성 수지 시장의 매출을 확보하고 있습니다. 고성능 PEEK는 비용이 높은 제품으로, 난연성·발연성·독성에 관한 규제를 준수해야 하는 항공기용 시트 구조재 분야에서 수요가 확대되었습니다. 코베스트로(Covestro)사의 ‘PolyLoop’는 2025년에 500톤의 사용 후 PA6-CFRP를 회수하여 90%의 강도를 유지하는 데 성공했습니다. 이는 열경화성 수지로는 구현할 수 없는 폐쇄 루프 방식의 실현을 입증하는 것입니다. BMW는 배터리 커버에 열가소성 수지 표면층과 에폭시 수지 코어를 결합함으로써 강성을 유지하면서도 충격 흡수성을 높였으며, 이는 섬유 강화 폴리머 복합재료 시장의 적용 범위를 더욱 확대하는 하이브리드 구조의 한 예입니다.

유리섬유 강화 폴리머(GFRP)는 2.50달러/kg의 원가와 2,400 MPa의 인장 강도로 건설, 풍력, 선박 분야 수요를 충족시켜 2025년 생산량의 91.18%를 차지했습니다. 중국의 Jushi사는 2025년에 생산 능력을 320만 톤으로 확대하고, 유리섬유 가격을 8% 인하함으로써 유럽과 미국공급업체들을 압박했습니다.

탄소섬유 강화 플라스틱(CFRP) 시장은 항공우주 OEM 업체들이 복합재 기체 생산을 확대하고, 고급 전기차에 구조용 배터리 인클로저가 채택됨에 따라 2031년까지 연평균 성장률(CAGR) 11.14%로 성장할 전망입니다. 보잉의 787 및 에어버스의 A350 프로그램에서는 2025년에 총 3,000톤의 섬유가 소비되었습니다. 포르쉐의 2024년형 ‘타이칸’의 루프와 벌크헤드는 무게 중심을 12mm 낮춤으로써 구조적 성능의 우월성을 입증했습니다. 표준 탄성률 등급은 CFRP 생산량 증가에 기여한 반면, 고탄성률 등급은 200 GPa를 초과하는 강성 대 중량비가 필요한 위성이나 F1 모노코크에 채택되었습니다. 현무암 섬유는 내화성 터널 내장재로 사용되며, 600°C에서도 강도의 85%를 유지합니다.

지역별 분석

아시아태평양은 2025년에 45.22%의 점유율로 섬유 강화 폴리머 복합재료 시장을 주도하며, 연평균 성장률(CAGR) 6.08%로 성장할 것으로 전망됩니다. 중국에서 75GW 규모의 풍력 발전 설비를 증설하는 과정에서 1kW당 18kg의 GFRP가 사용되었으며, 이는 지역 내 주요 기업들의 52만 톤 규모의 신규 유리섬유 생산 능력 확대를 뒷받침했습니다. 1조 4,000억 달러 규모의 인도 ‘국가 인프라 계획’에서는 내식성 자재에 12%가 배정되어 있으며, 이에 따라 2028년까지 연간 18만 톤의 GFRP 철근 수요가 예상됩니다. 일본에서는 15년에 걸친 노출 시험을 통해 열화가 전혀 발생하지 않는 것으로 입증됨에 따라, 연안 지역의 고속도로에서 FRP 철근의 사용이 의무화되어 있습니다.

북미에서는 미국의 교량 투자 프로그램이 2025년에 24억 달러를 책정하고 있으며, 이 중 18%가 1,200개의 교량에 대한 FRP 피복 공사에 배정되어 있습니다. 보잉사의 사우스캐롤라이나주 및 워싱턴주 공장에서는 2025년에 787 및 777X 프로그램을 위해 1,200톤의 CFRP를 사용했습니다. 온타리오주에서는 GM과 스텔란티스가 전기차(EV) 차체 하부 부품의 현지 생산을 추진함에 따라 4억 2,000만 달러 규모의 복합재료 관련 자본을 유치했습니다.

유럽에서는 독일이 2025년에 8.2GW 규모의 풍력 발전 설비를 도입했으며, 그중 55%가 해상 풍력 발전이었습니다. 이로 인해 하이브리드 탄소·유리 재질의 스퍼 캡이 장착된 100m가 넘는 블레이드에 대한 수요가 증가했습니다. EU의 폐기물 기본 지침에 따르면, 2028년까지 복합재료에 재활용 소재를 25% 포함해야 할 의무가 부과되었으며, 이에 따라 오웬스 코닝과 베올리아는 3,800만 유로를 투입해 열분해 설비에 투자했습니다. 에어버스는 A350의 월간 생산 대수를 9대로 늘려, 슈타데와 이레스카스에서 1,800톤의 CFRP 수요를 창출했습니다.

남미에서는 브라질의 풍력 발전 설비 용량이 28GW에 달하며, 그 중 85%가 대용량 발전소가 밀집해 있는 북동부 지역에 집중되어 있어, 2025년에는 9,600톤의 GFRP 블레이드 수요가 예상됩니다. 중동 및 아프리카의 합산 점유율은 낮은 편이지만, 가까운 미래에 성장이 기대되고 있습니다. 사우디아라비아의 NEOM 프로젝트에서는 2030년까지 14만 톤의 GFRP 철근이 필요할 것으로 예측됩니다. 남아프리카에서는 2024년부터 2025년까지 3.2GW의 풍력 발전 용량이 추가될 예정이며, 지멘스 가메사(Siemens Gamesa)사가 1kW당 16kg의 GFRP를 사용한 115m 길이의 블레이드를 공급하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the fiber-Reinforced polymer composites market size is expected to increase from USD 79.07 billion in 2025 to USD 83.17 billion in 2026 and reach USD 107.16 billion by 2031, growing at a CAGR of 5.20% over 2026-2031.

This report is Segmented by Resin Type (Thermoset and Thermoplastic), Fiber Type (Glass Fiber-Reinforced Polymer (GFRP), Carbon Fiber-Reinforced Polymer (CFRP), and More), Reinforcement Form (Rovings, Prepreg, and More), End-User Industry (Transportation, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Global Fiber-Reinforced Polymer (FRP) Composites Market Trends and Insights

Construction Spend Shifting to Corrosion-Free Rebar and Bridge Decks

United States, Japan, and Gulf agencies are increasingly specifying glass- and basalt-fiber rebar to prolong bridge life under chloride attack. In 2025, 42% of the 617,000 U.S. bridges were over 50 years old, and corrosion repairs cost USD 8.3 billion annually, giving GFRP retrofits a 35% life-cycle cost advantage. Japan mandated FRP rebar in coastal highways after 15 years of successful exposure testing along the Tokyo Bay Aqua-Line. Saudi Arabia's NEOM project adopted GFRP for 80% of concrete structures to avoid steel oxidation in 45°C ambient conditions. Pultruded bridge decks weigh 75% less than reinforced concrete, reduce foundations by up to 30%, and demonstrated a 40-year design life on West Virginia Route 2 in 2025.

Wind-Turbine Blade Length Exceeding 120 Meters Demanding Ultra-High-Strength GFRP

Turbine makers now deploy rotor diameters above 240 m, which push blade lengths past 120 m and require spar caps with tensile strength over 1,200 MPa. Vestas introduced a 15 MW turbine in 2024 featuring 115.5-m blades incorporating high-modulus glass fiber that cuts blade mass by 8 t per unit. China installed 75 GW of wind capacity in 2025, 60% offshore, and manufacturers shifted to low-void resin-transfer molding to withstand ten-million-cycle fatigue loads. Siemens Gamesa's thermoplastic RecyclableBlade enables 95% material recovery, aligning with the EU 2028 recycling rule.

Volatile Carbon-Fiber Prices Hurting Automotive Cost Targets

Export restrictions on Russian polyacrylonitrile raised precursor prices 18% in 2025, forcing OEMs to absorb USD 4-6 per-kg increases that jeopardize sub-USD 35,000 EV programs. Toyota replaced planned CFRP roof panels on the 2026 Prius with aluminum to protect margins. SGL Carbon and Toray fixed five-year offtake contracts at 12% above 2024 spot prices, transferring volatility upstream. Recycled fiber from ELG retains 90% strength at 40% below virgin cost but suits only non-structural parts. Hexcel shifted 30% of precursor output to a lower-cost U.S. site to blunt European energy spikes.

Other drivers and restraints analyzed in the detailed report include:

- Lightweighting Mandates in EV Platforms Favoring Thermoplastic CFRP

- Retrofitting of Aging Bridges in U.S., Japan, and EU With FRP Wraps

- EU End-of-Life Recycling Gap Triggering Landfill Restrictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermoset held 71.06% of 2025 revenue, dominated by epoxy and polyester chemistries specified for corrosion resistance and low-cost open-mold processing. Epoxy captured high thermoset demand because its superior adhesion pairs with carbon fiber in aerospace prepregs. Polyester served in cost-driven marine and tank markets, while vinyl ester filled in highly corrosive chemical plants.

Thermoplastic will grow at 6.15% CAGR through 2031 as carmakers pivot to recyclable matrices. Polypropylene compounds reinforced with 40% glass fiber now form door-module carriers that cut weight 35% and mold in 90 seconds at annual volumes above 500,000 units. Polyamide 6 and 66 secure thermoplastic revenue for under-hood parts operating up to 150 °C. High-performance PEEK, though costly, expanded in aircraft seat structures that demand flame-smoke-toxicity compliance. Covestro's PolyLoop recovered 500 t of end-of-life PA6-CFRP in 2025 with 90% strength retention, proving a closed-loop route unavailable to thermosets. BMW combines thermoplastic skins with epoxy cores in battery covers for higher impact absorption while retaining stiffness, illustrating hybrid architectures that deepen fiber reinforced polymer composites market adoption.

Glass Fiber-Reinforced Polymer (GFRP) accounted for 91.18% of 2025 volume because its USD 2.50/kg cost and 2,400 MPa tensile strength satisfy construction, wind, and marine needs. China Jushi raised capacity to 3.2 million t in 2025, lowering glass fiber prices 8% and squeezing Western suppliers.

Carbon Fiber-Reinforced Polymer (CFRP) will expand at an 11.14% CAGR to 2031 as aerospace OEMs ramp composite airframes and premium EVs adopt structural battery enclosures. Boeing's 787 and Airbus A350 programs jointly consumed 3,000 t of fiber in 2025. Porsche's 2024 Taycan roof and bulkhead lowered center-of-gravity 12 mm, validating structural performance premiums. Standard-modulus grades delivered higher CFRP volume, while high-modulus variants served satellites and Formula 1 monocoques requiring more than 200 GPa stiffness-to-weight ratios. Basalt fiber is used for fire-resistant tunnel linings, retaining 85% strength at 600 °C.

Geography Analysis

Asia-Pacific dominated the fiber reinforced polymer composites market with a 45.22% share in 2025 and is projected to grow at 6.08% CAGR. China's 75 GW wind additions used 18 kg GFRP per kW and spurred 520,000 t of new glass-fiber capacity by regional leaders. India's USD 1.4 trillion National Infrastructure Pipeline allocates 12% to corrosion-resistant materials, translating to 180,000 t annual GFRP rebar demand by 2028. Japan now mandates FRP rebar in coastal highways after 15-year exposure trials proved zero degradation.

In North America, U.S. Bridge Investment Program earmarked USD 2.4 billion in 2025, with 18% for FRP wraps on 1,200 bridges. Boeing's South Carolina and Washington plants consumed 1,200 t CFRP for 787 and 777X programs in 2025. Ontario attracted USD 420 million composite capital as GM and Stellantis localized EV underbody parts.

In Europe, Germany installed 8.2 GW of wind capacity in 2025, 55% offshore, demanding blades above 100 m with hybrid carbon-glass spar caps. The EU Waste Framework Directive requires 25% recycled content in composites by 2028, triggering EUR 38 million pyrolysis investments by Owens Corning and Veolia. Airbus increased A350 output to nine per month, adding 1,800 t CFRP demand at Stade and Illescas.

South America captured demand as Brazil's wind fleet reached 28 GW with 85% located in high-capacity Northeast zones demanding 9,600 t GFRP blades in 2025. Middle East and Africa together held lower share yet promise growth in the near future. Saudi Arabia's NEOM calls for 140,000 t GFRP rebar through 2030. South Africa added 3.2 GW wind capacity in 2024-2025, with Siemens Gamesa supplying 115-m blades using 16 kg GFRP per kW.

- AGY

- China Jushi Co., Ltd.

- Exel Composites

- Gurit Services AG

- Hexcel Corporation

- Hitachi, Ltd.

- Kineco Limited

- Kordsa Teknik Tekstil Anonim Sirketi

- KraussMaffei

- Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- Nippon Electric Glass Co., Ltd.

- Norplex Micarta

- Olin Corporation

- Owens Corning

- Park Aerospace Corp.

- SAERTEX GmbH & Co.KG

- SGL Carbon

- Solvay

- Strongwell Corporation

- TEIJIN LIMITED

- TORAY INDUSTRIES, INC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction Spend Shifting to Corrosion-Free Rebar and Bridge Decks

- 4.2.2 Wind-Turbine Blade Length More than 120 M Demanding Ultra-High-Strength GFRP

- 4.2.3 Lightweighting Mandates in EV Platforms Favouring Thermoplastic CFRP

- 4.2.4 Retrofitting of Aging Bridges in US, Japan, and EU With FRP Wraps

- 4.2.5 Modular Composite Rebar for 3-D-Printed Concrete Structures

- 4.3 Market Restraints

- 4.3.1 Volatile Carbon-Fiber Prices Hurt Automotive Cost Targets

- 4.3.2 Availability of Metal and Engineered-Wood Substitutes

- 4.3.3 EU End-of-Life Recycling Gap Triggering Landfill Restrictions

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Thermoset

- 5.1.2 Thermoplastic

- 5.2 By Fiber Type

- 5.2.1 Glass Fiber-Reinforced Polymer (GFRP)

- 5.2.2 Carbon Fiber-Reinforced Polymer (CFRP)

- 5.2.3 Aramid Fiber-Reinforced Polymer

- 5.2.4 Basalt Fiber-Reinforced Polymer

- 5.2.5 Other Fiber Types

- 5.3 By Reinforcement Form

- 5.3.1 Rovings

- 5.3.2 Woven Fabrics and Mats

- 5.3.3 Chopped Strands

- 5.3.4 Prepreg

- 5.3.5 SMC and BMC

- 5.4 By End-user Industry

- 5.4.1 Transportation

- 5.4.2 Building and Construction

- 5.4.3 Electrical and Electronics

- 5.4.4 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 NORDIC Countries

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AGY

- 6.4.2 China Jushi Co., Ltd.

- 6.4.3 Exel Composites

- 6.4.4 Gurit Services AG

- 6.4.5 Hexcel Corporation

- 6.4.6 Hitachi, Ltd.

- 6.4.7 Kineco Limited

- 6.4.8 Kordsa Teknik Tekstil Anonim Sirketi

- 6.4.9 KraussMaffei

- 6.4.10 Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- 6.4.11 Nippon Electric Glass Co., Ltd.

- 6.4.12 Norplex Micarta

- 6.4.13 Olin Corporation

- 6.4.14 Owens Corning

- 6.4.15 Park Aerospace Corp.

- 6.4.16 SAERTEX GmbH & Co.KG

- 6.4.17 SGL Carbon

- 6.4.18 Solvay

- 6.4.19 Strongwell Corporation

- 6.4.20 TEIJIN LIMITED

- 6.4.21 TORAY INDUSTRIES, INC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Development of New Advanced Forms of FRP Materials