|

시장보고서

상품코드

2066586

폴리프로필렌 포장 필름 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Polypropylene Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

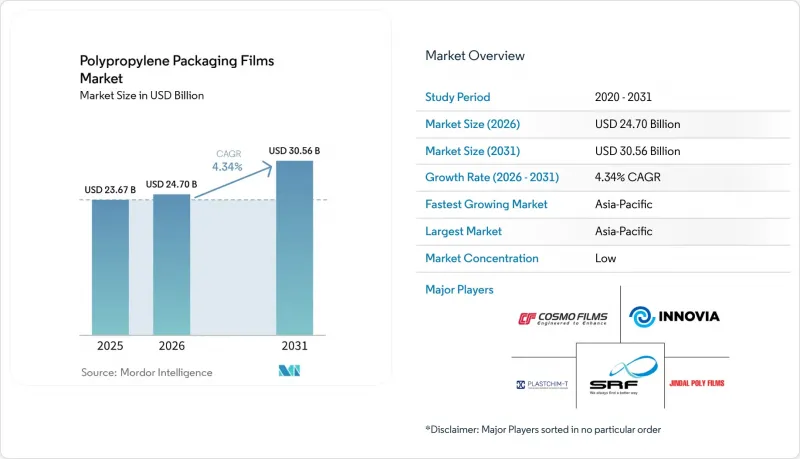

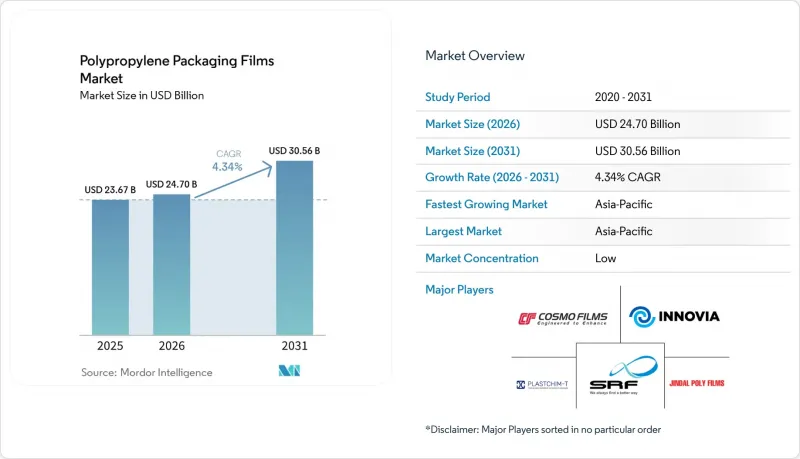

Mordor Intelligence에 의하면, 2026년 폴리프로필렌 포장 필름 시장 규모는 247억 달러로 추정되고 있어 2025년 236억 7,000만 달러에서 확대해, 2031년에는 305억 6,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 4.34%로 성장할 것으로 전망됩니다.

본 보고서는 필름 유형(이축연신 폴리프로필렌(BOPP)(BOPP) 필름 등), 포장 형태(랩 및 오버랩, 라벨 및 감압 테이프, 백 및 파우치 등), 최종 이용 산업(식품, 음료, 의약품 및 헬스케어 등), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다.

세계 폴리프로필렌 포장 필름 시장 동향 및 분석

경질 플라스틱에서 연포장 형태로의 지속 가능한 전환

경질 플라스틱에 비해 포장 중량을 최대 75%까지 줄일 수 있는 유연한 폴리프로필렌 필름은 브랜드 소유자가 운송 시 발생하는 배출 가스와 자재 비용을 절감하는 데 도움이 됩니다. 클록너 펜타플라스트(Clockner Pentaplast)사의 ‘kp FlexiFlow’ 시리즈는 93% 이상이 폴리프로필렌으로 구성된 재활용 가능한 플로우랩 구조를 구현하여, 기존 제품과 동등한 성능을 발휘하는 동시에 순환 경제에 부응하고 있습니다. 다국적 기업들은 홈케어 및 퍼스널케어 제품에 리필 파우치를 도입함으로써, 확대 생산자 책임(EPR) 규정에 따른 발생원 감축 비용을 절감하고 있습니다. 필름 제조업체들은 천공 저항성을 저해하지 않으면서 두께를 얇게 만들고, 사용 후 소비자 재활용 수지의 배합 비율을 높이는 데 주력하고 있으며, 이를 통해 전자상거래 및 소매 채널 전반에서 폴리프로필렌이 경량 대체 소재로서의 입지를 확고히 다지고 있습니다.

브랜드 소유주들의 단일 소재 재활용 라미네이트에 대한 수요

DNP의 폴리프로필렌 기반 단일 소재 라미네이트는 CEFLEX의 설계 지침을 충족하며, 고속 성형·충진·밀봉(FFS) 공정을 가능하게 할 뿐만 아니라 기존 재활용 시스템에 투입할 수도 있습니다. 유럽의 포장 및 포장 폐기물 규제의 목표가 도입을 가속화함에 따라, Saica Flex는 인증된 사용 후 소비자 유래 소재를 5% 함유한 100% 재활용 가능한 솔루션을 개발했습니다. ORMOCER 및 새로운 아크릴계 화학 기술 등 배리어 코팅 기술의 발전으로 산소 투과율이 0.1 cm³/m²·일·bar 미만을 달성하여, 보관 기간 요건과 재활용 가능성을 모두 충족시키고 있습니다. 각 브랜드 소유 기업들은 2030년 순환형 사회 실현이라는 공약을 달성하기 위해 소폭의 비용 증가를 감수하고 있으며, 이것이 혼합 소재 호일 라미네이트의 급속한 대체를 촉진하고 있습니다.

프로파일렌 및 나프타 원료 가격의 변동

2025년 초, 정유시설의 가동 중단으로 인해 공급이 부족해지자, 폴리머용 프로파일렌 가격은 파운드당 4-5센트 상승하여 가공업체의 이익률을 압박했습니다. 남아시아의 라피아 등급 가격은 원유 벤치마크에 대한 지정학적 압박을 반영하여 톤당 970-990달러까지 상승했습니다. 각 필름 제조업체들은 대중화된 스낵용 포장 필름 분야에서 추가 비용 전가에 어려움을 겪고 있으며, 일부 지역 포장 업체들은 가격 변동이 적은 폴리에틸렌 필름의 시범 도입을 추진하고 있습니다. 불확실성이 지속되는 상황은 연간 공급 입찰을 복잡하게 만들고, 새로운 확장 라인에 대한 설비 투자를 주저하게 하는 요인이 되고 있습니다.

부문별 분석

2025년, BOPP는 폴리프로필렌 포장 필름 시장에서 65.58%의 점유율을 차지하며 시장을 주도했습니다. 이는 스낵, 제과류, 담배 제품의 중첩 포장에 이 기술이 폭넓게 채택되고 있음을 반영한 것입니다. 아크릴 또는 PVDC 코팅이 된 BOPP 등급은 저밀도의 장점을 유지하면서 과자류의 유통기한을 연장합니다. 코스모필름스는 연간 196,000 t의 생산 능력을 운영하고 있으며, 이는 전 세계 유통을 뒷받침하고 BOPP공급 안정성을 강화하고 있습니다. 또한, 동남아시아의 신규 생산 라인을 통해 공급량이 증가하고 있어, 가격에 민감한 아프리카 시장으로의 납품 비용을 절감하고 있습니다.

CPP는 레토르트 파우치 및 금속 증착 가공된 스낵용 포장재의 성장에 힘입어 6.87%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 미쓰이물산의 RXC-22 캐스트 필름은 더 낮은 온도에서도 밀봉이 가능하여, 고속 FFS(Form-Fill-Seal) 기계의 에너지 소비를 줄여줍니다. 특수 CPP는 투명성, 내화학성 및 감마선 멸균 내성이 중요한 의료용 포장 분야에서 경쟁력을 발휘하고 있습니다. CPP 폴리프로필렌 포장 필름 시장 규모는 재활용 과정을 원활하게 하는 단일 소재 파우치 라미네이트에 대한 수요 증가에 따라 확대될 전망입니다. 농산물용 통기성 미세다공성 필름을 비롯한 기타 틈새 시장용 제품들은 특정 수분 및 가스 교환 요구 사항을 해결함으로써 추가 수익을 창출하고 있습니다.

지역별 분석

아시아태평양은 2025년에 전 세계 매출의 43.71%를 차지해, 2031년까지 연평균 성장률(CAGR) 6.23%로 성장할 전망입니다. 중국의 폴리프로필렌 수출량은 260만 톤으로 예상되며, 이는 필름용 수지의 풍부한 공급을 뒷받침하고 있습니다. 인도네시아의 내수 수요는 520만 톤에 달하고, 국내 생산 능력인 240만 톤을 초과하고 있기 때문에 지역 공급업체를 대상으로 한 반덤핑 관세가 부과되고 있음에도 불구하고 수입이 불가피한 상황입니다. 2025년 하반기에 베트남 롱손 크래커가 재가동되면, 연간 40만 톤의 폴리프로필렌이 추가로 공급되어 공급 부족이 완화되고, 지역 내 하류 가공업체들에 힘을 실어줄 것입니다. 비용 경쟁력이 있는 노동력과 확대되는 중산층 덕분에 FMCG(일용소비재), 제약, 전자 분야의 각 공급망에서 견조한 수요가 유지되고 있습니다.

유럽은 생산량 증가세가 완만하기는 하지만, 여전히 기술 분야의 선도적 지위를 유지하고 있습니다. 확대 생산자 책임(EPR)에 따른 수수료는 현재 재활용 가능성에 따라 변동하고 있으며, 각 브랜드는 단일 소재인 폴리프로필렌 솔루션으로의 전환을 요구받고 있습니다. 향후 도입될 ‘탄소 국경 조정 메커니즘(CBAM)’에 따라 수입 필름에 대해 보고 의무나 암묵적인 탄소 비용이 부과될 가능성이 있어, 동남아시아의 가격 경쟁력이 약화될 우려가 있습니다. 유럽의 각 변환 업체들은 소재 순환 고리를 완성하기 위해 첨단 탈잉크 처리 및 용제 기반 재활용 공장에 투자하고 있는 반면, Ineos사는 EU의 PPWR(폴리프로필렌 폐기물 규정) 요건을 충족하기 위해 프랑스 크래커에서 재활용 플라스틱 생산량을 확대되고 있습니다.

북미는 높은 식품 안전 기준과 전자상거래의 높은 보급률이라는 이점을 누리고 있는 반면, 원자재 가격에 연동된 비용 변동이라는 문제와 씨름하고 있습니다. 퓨어사이클사의 오하이오주 공장에서는 현재 연간 1억 700만 파운드의 초고순도 재생 폴리프로필렌을 생산하고 있으며, FDA 기준을 준수하는 재생 소재가 필요한 가공업체에 공급하고 있습니다. 2021년 미국의 폴리프로필렌 수입 총액은 7억 8,920만 달러에 달했으며, 국내 크래커가 폴리에틸렌 유도체를 우선적으로 생산하고 있는 탓에 해외산 모노머에 대한 의존도가 두드러지게 나타나고 있습니다. 각 주의 법규에 따라 연포장재의 재생 재료 함유율 기준이 설정됨에 따라, 화학 재활용 시범 라인에 대한 투자가 가속화되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, polypropylene packaging films market size in 2026 is estimated at USD 24.7 billion, growing from 2025 value of USD 23.67 billion with 2031 projections showing USD 30.56 billion, growing at 4.34% CAGR over 2026-2031.

This report is Segmented by Film Type (Biaxially Oriented Polypropylene (BOPP) Film and More), Packaging Format (Wraps and Over-Wraps, Labels and Pressure-Sensitive Tapes, Bags and Pouches and More), End-Use Industry ( Food, Beverage, Pharmaceutical and Healthcare and More) and Geography (North America, Europe, Asia-Pacific, South America and Middle East and Africa)

Global Polypropylene Packaging Films Market Trends and Insights

Sustainable Shift from Rigid to Flexible Formats

Reducing package weight by as much as 75% versus rigid plastics, flexible polypropylene films help brand owners curb freight emissions and material costs. Klockner Pentaplast's kp FlexiFlow range delivers recyclable flow-wrap structures containing more than 93% polypropylene, illustrating performance parity with legacy formats while offering circularity. Multinationals adopt refill pouches for home-care and personal-care goods, lowering source-reduction fees under Extended Producer Responsibility rules. Film producers leverage downgauging and higher post-consumer-recycled resin loads without sacrificing puncture strength, solidifying polypropylene's role as a lightweight alternative across e-commerce and retail channels.

Brand Owner Demand for Mono-Material Recycle-Ready Laminates

DNP's polypropylene-based mono-material laminates meet CEFLEX design guidelines, allowing high-speed form-fill-seal operations while entering existing recycling streams. European Packaging and Packaging Waste Regulation targets accelerate adoption, prompting Saica Flex to develop 100% recyclable solutions that incorporate 5% certified post-consumer content. Barrier-coating advances such as ORMOCER and new acrylic chemistries achieve oxygen transmission rates below 0.1 cm3/m2*day*bar, aligning shelf-life demands with recyclability. Brand owners accept small cost premiums to reach 2030 circularity pledges, spurring rapid substitution of mixed-material foil laminates.

Volatility in Propylene and Naphtha Feedstock Prices

Polymer-grade propylene rose 4-5 cents / lb in early 2025 after refinery closures tightened supply, squeezing converter margins. South Asian raffia grades climbed to USD 970-990 / t, reflecting geopolitical pressures on crude benchmarks. Film makers struggle to pass through surcharges in commoditized snack wraps, prompting some regional packers to trial less volatile polyethylene films. Persistent uncertainty complicates annual supply tenders and deters capital spending on new orientation lines.

Other drivers and restraints analyzed in the detailed report include:

- Retort-Grade CPP Replacing Multilayer High-Barrier Structures

- E-commerce Boom Driving High-Clarity Over-Wrap Films

- Growing PET and PE Mono-Material Barrier Film Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

BOPP led the polypropylene packaging films market with 65.58% share in 2025, reflecting broad adoption in snack, bakery, and tobacco over-wraps. Coated BOPP grades with acrylic or PVDC layers extend shelf life in confectionery while retaining low density advantages. Cosmo Films operates 196,000 t / y capacity that supports global distribution, reinforcing BOPP supply security. Volume also flows from new Southeast Asian lines that lower delivered costs into price-sensitive African markets.

CPP posted the quickest 6.87% CAGR forecast, propelled by retort pouches and metallized snack wraps. Mitsui's RXC-22 cast film seals at lower temperatures, trimming energy use on high-speed form-fill-seal machinery. Specialty CPP competes in medical packaging where clarity, chemical resistance, and gamma sterilization tolerance matter. The polypropylene packaging films market size for CPP is set to expand alongside demand for mono-material pouch laminates that facilitate recycling streams. Other niche grades, including breathable microporous films for produce, carve out incremental revenue by solving specific moisture and gas-exchange needs.

Geography Analysis

Asia-Pacific controlled 43.71% of global revenue in 2025 and is poised for a 6.23% CAGR through 2031. China's forecast 2.6 million-ton polypropylene export pool underpins ample film resin supply. Indonesia's national demand of 5.2 million t outstrips domestic capacity of 2.4 million t, necessitating imports even as anti-dumping duties target regional suppliers. Vietnam's Long Son cracker restart in late 2025 will add 400,000 t / y of polypropylene, narrowing deficits and supporting regional downstream processors. Cost-competitive labor and an expanding middle class sustain robust demand across FMCG, pharmaceutical, and electronics supply chains.

Europe remains a technology leader despite modest volume growth. Extended Producer Responsibility fees now vary by recyclability, nudging brands toward mono-material polypropylene solutions. The forthcoming Carbon Border Adjustment Mechanism may impose reporting obligations and implicit carbon costs on imported films, potentially eroding Southeast Asian price advantages. European converters invest in advanced de-inking and solvent-based recycling plants to close material loops, while Ineos ramps recycled-plastic output at its French cracker to comply with EU PPWR mandates.

North America benefits from high food-safety standards and deep e-commerce penetration but battles feedstock-linked cost swings. PureCycle's Ohio plant now produces 107 million lb / y of ultra-pure recycled polypropylene, supplying converters that need FDA-compliant recyclate. US polypropylene imports totaled USD 789.2 million in 2021, revealing reliance on overseas monomer when domestic crackers prioritize polyethylene derivatives. Investment in chemical recycling pilot lines accelerates as state legislation sets recycled-content thresholds for flexible packaging.

- Amcor Plc

- Jindal Poly Films Ltd

- Innovia Films

- Cosmo Films Ltd

- Taghleef Industries LLC

- UFlex Ltd

- Polyplex Corporation Ltd

- SRF Ltd

- Plastchim-T

- Toray Plastics (America) Inc.

- ProAmpac LLC

- Inteplast Group

- Oben Holding Group

- Profol GmbH

- Treofan GmbH

- Vibac Group

- Chiripal Poly Films

- Polinas

- Stenta Films

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustainable shift from rigid to flexible formats

- 4.2.2 Brand owner demand for mono-material recycle-ready laminates

- 4.2.3 Retort-grade CPP replacing multilayer high-barrier structures

- 4.2.4 E-commerce boom driving high-clarity over-wrap films

- 4.2.5 Rapid capacity additions in Southeast Asia lowering film prices

- 4.2.6 Chemical-recycling derived PP resin commercialization

- 4.3 Market Restraints

- 4.3.1 Volatility in propylene and naphtha feedstock prices

- 4.3.2 Growing PET and PE mono-material barrier film substitutes

- 4.3.3 Trade-flow disruptions from carbon-border-adjustment tariffs

- 4.3.4 Extended Producer Responsibility (EPR) compliance costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Film Type

- 5.1.1 Biaxially Oriented Polypropylene (BOPP) Film

- 5.1.1.1 Coated BOPP (PVDC, Acrylic, EVOH)

- 5.1.1.2 Uncoated BOPP

- 5.1.2 Chlorinated Polypropylene (CPP) Film

- 5.1.2.1 General-purpose CPP

- 5.1.2.2 Retort-grade CPP

- 5.1.2.3 Metalized CPP

- 5.1.3 Other Polypropylene (PP) Packaging Films

- 5.1.1 Biaxially Oriented Polypropylene (BOPP) Film

- 5.2 By Packaging Format

- 5.2.1 Wraps and Over-wraps

- 5.2.2 Labels and Pressure-sensitive Tapes

- 5.2.3 Bags and Pouches

- 5.2.4 Lidding and Flow-wrap Films

- 5.2.5 Blister and Strip Packs

- 5.3 By End-use Industry

- 5.3.1 Food

- 5.3.1.1 Bakery and Confectionery

- 5.3.1.2 Snacks and Breakfast Cereals

- 5.3.1.3 Fresh Produce

- 5.3.1.4 Meat, Poultry and Seafood

- 5.3.1.5 Dairy Products

- 5.3.2 Beverage

- 5.3.2.1 Non-Alcoholic

- 5.3.2.1.1 Bottled Water

- 5.3.2.1.2 Carbonated Drinks

- 5.3.2.1.3 Juices

- 5.3.2.1.4 Other Non-Alcoholic Beverages

- 5.3.2.2 Alcoholic

- 5.3.2.2.1 Beer

- 5.3.2.2.2 Spirits

- 5.3.2.2.3 Other Alcoholic Beverages

- 5.3.2.1 Non-Alcoholic

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Personal Care and Cosmetics

- 5.3.5 Industrial

- 5.3.6 Other End-use Industry

- 5.3.1 Food

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 Middle East

- 5.4.4.1.1 Saudi Arabia

- 5.4.4.1.2 United Arab Emirates

- 5.4.4.1.3 Turkey

- 5.4.4.1.4 Rest of Middle East

- 5.4.4.2 Africa

- 5.4.4.2.1 South Africa

- 5.4.4.2.2 Kenya

- 5.4.4.2.3 Rest of Africa

- 5.4.4.1 Middle East

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amcor Plc

- 6.4.2 Jindal Poly Films Ltd

- 6.4.3 Innovia Films

- 6.4.4 Cosmo Films Ltd

- 6.4.5 Taghleef Industries LLC

- 6.4.6 UFlex Ltd

- 6.4.7 Polyplex Corporation Ltd

- 6.4.8 SRF Ltd

- 6.4.9 Plastchim-T

- 6.4.10 Toray Plastics (America) Inc.

- 6.4.11 ProAmpac LLC

- 6.4.12 Inteplast Group

- 6.4.13 Oben Holding Group

- 6.4.14 Profol GmbH

- 6.4.15 Treofan GmbH

- 6.4.16 Vibac Group

- 6.4.17 Chiripal Poly Films

- 6.4.18 Polinas

- 6.4.19 Stenta Films

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment