|

시장보고서

상품코드

2066587

남성 불임 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Male Infertility - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

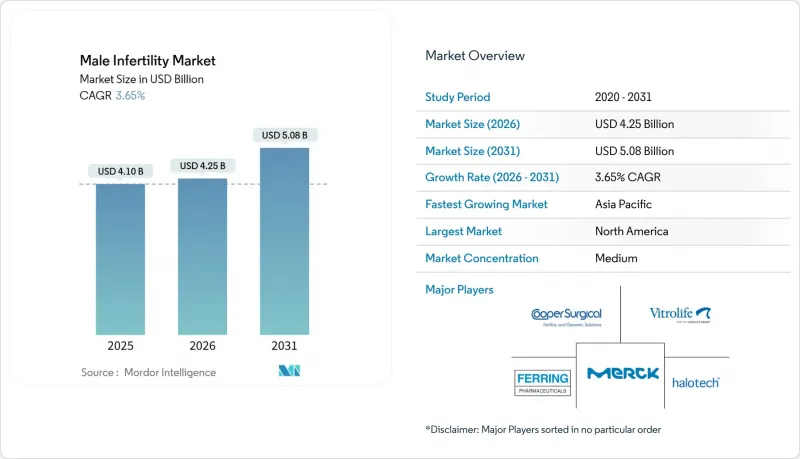

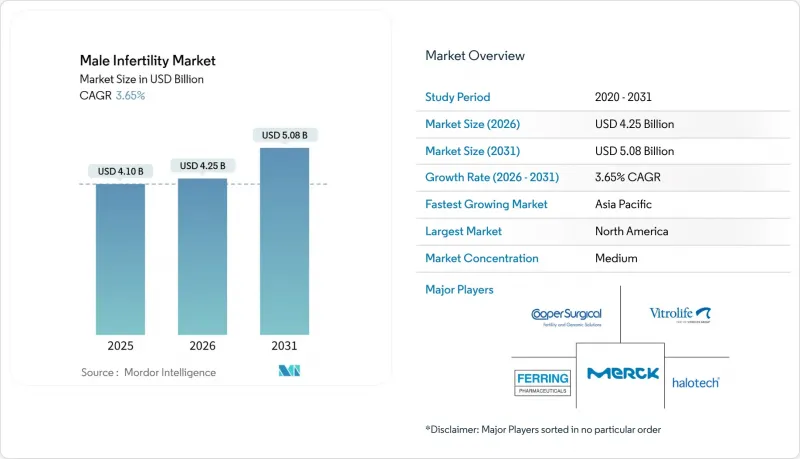

Mordor Intelligence에 의하면, 남성 불임 시장 규모는 2025년 41억 달러로 평가되었고, 2026년에는 42억 5,000만 달러로 추정되고, 2026-2031년 CAGR 3.65%로 성장을 지속할 전망이며, 2031년에는 50억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 검사 유형별(기존 정액 분석, CASA 등), 치료법별(약물 요법 및 호르몬 요법, ART 등), 제품별(진단 키트·기기, 치료제, ART 기기), 유통 채널별(병원·불임 치료 클리닉, 진단센터 등), 최종 사용자별(불임 치료 클리닉 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 남성 불임 시장 동향 및 인사이트

전 세계 남성 불임 유병률 증가

메타분석에 따르면, 1973년 이후 정자 농도는 연간 1.2%씩 감소해 왔으며, 2000년 이후에는 아프리카, 아시아, 남미 전역에서 그 감소세가 가속화되고 있는 것으로 확인되었습니다. 환경 유래의 내분비 교란 물질이나 비만 등의 생활 습관 요인은 정자의 운동 능력 및 DNA 무결성의 저하와 관련이 있는 반면, OECD 회원국 대부분에서는 아버지의 연령 중앙값이 현재 32세를 넘고 있습니다. 첫 아이를 가질 때 아버지가 되는 연령대의 확대는 유해 물질에 대한 누적적인 노출과 맞물려 남성 불임 치료 시장을 확대시키고 있습니다. 많은 국가에서 사회적 편견으로 인해 검사가 3-5년 늦어지기 때문에 진단 건수는 여전히 유병 수보다 적습니다.

고용주가 자금을 지원하는 불임 치료 급여 확대

2024년 말까지 미국 대기업의 4분의 1이 체외수정 비용을 부담하게 되었으며, 2025년에 발표된 연방 정부 지침을 통해 특정 진단 검사가 ‘의료보험합리화법(Affordable Care Act)’에 따라 보장 대상에서 제외된다는 점이 명확히 밝혀져 규제상의 모호함이 해소되었습니다. 보험 상품에서는 일반적으로 평생 지급 한도가 15,000-25,000달러로 설정되어 있지만, 이는 여러 차례의 치료 주기를 감당하기에는 불충분할 뿐만 아니라, 정밀 남성 불임 검사 비용이 보장 대상에서 제외되는 경우도 많아 본인 부담금이 증가하고 있습니다. 유럽 기업들은 독일의 ‘일부 비용 분담’ 모델을 따르고 있으며, 플랫폼 사업자들이 검사 서비스의 패키지화를 협상하도록 촉구하고 있습니다. 이에 따라 검사 방식이 재검토되면서 남성 인자 검사의 인지도가 높아지고 있습니다.

높은 본인 부담금과 불균등한 보상

미국에서는 1회의 세포질 내 정자 주입(ICSI) 주기에 15,000-3만 달러의 비용이 들지만, 그 전액을 부담하는 민간 보험 상품은 20% 미만입니다. 고도의 남성 불임 진단에는 추가로 1,000-2,500달러가 소요되지만, 이 비용이 환급되는 경우는 거의 없습니다. 프랑스와 이스라엘의 공적 의료 제도에서는 ART 비용의 대부분이 공적 자금으로 충당되고 있지만, 인도에서는 대상 부부의 10% 미만이 공적 지원을 받고 있습니다. 이러한 자금 부족으로 인해 커플의 42%가 1만 달러가 넘는 빚을 지고 있으며, 28%는 치료를 완전히 포기하고 있습니다.

부문별 분석

2025년에는 기존 정액 검사가 해당 부문 매출의 42.18%를 차지했으나, 유전학적 및 후성유전학적 검사 패널 하위 부문은 2031년까지 연평균 성장률(CAGR) 5.22%를 기록하며 다른 모든 검사 분야를 앞지르는 속도로 성장하고 있습니다. 시퀀싱 비용의 하락으로 인해, 현재는 1,000달러 미만의 비용으로 48시간 이내에 Y염색체 결손이나 CFTR 변이를 확인할 수 있게 되었습니다. AI 추적 기능을 갖춘 컴퓨터 지원 시스템은 기술자 간 작업의 편차를 줄이고, 검사실 내 프로토콜의 표준화를 촉진하고 있습니다. DNA 단편화 검사는 현재로서는 표준화되어 있지 않지만, 반복 착상 불량을 다루는 클리닉에서 채택되고 있으며, 이러한 추세는 2027년에 ISO 지침이 제정될 때 향후 보험 적용 가능성이 시사되는 것입니다. 산화 스트레스 검사 및 선체 반응 검사는 여전히 틈새 분야에 머물러 있으며, 연구 환경으로 한정되어 있습니다. 따라서 남성 불임 치료 시장은 예측 정확도가 더 높은 분자진단으로의 전환이 진행되는 한편, 여전히 기본적인 현미경 검사에 의존하고 있습니다.

검사실에서 개발된 유전자 검사는 현재 미국 식품의약국(FDA)이 2024년 5월에 제정한 규정의 적용을 받고 있으며, 이 규정에 따라 시판 전 심사가 확대됨에 따라 소규모 독립 검사 센터의 규정 준수 비용이 증가하고 있습니다. 각국의 의료 제도에 따른 보험 적용 범위에는 차이가 있습니다. 프랑스에서는 체외수정(IVF)이 두 번 실패한 후에 유전자 검사에 대한 보험 적용이 이루어지지만, 미국의 대부분의 보험 플랜에서는 먼저 기존 검사를 통해 이상이 확인되어야 한다는 조건을 두고 있어, 검사에 대한 접근이 늦어지고 있습니다. 이러한 차이는 첨단 진단법을 활용한 남성 불임 시장 규모에 영향을 미치고 있으며, 아시아태평양의 검사 기관에서는 대도시권의 환자층이 두텁고 민간 보험을 통한 지불 모델이 보급되어 있어, 다항목 검사 패널의 도입이 더욱 신속하게 진행되고 있습니다.

2025년에는 전 세계 체외수정(IVF) 주기의 70% 이상에서 세포질 내 정자 주입법(ICSI)이 적용됨에 따라, 보조생식기술(ART)이 해당 부문 매출의 55.21%를 차지했습니다. 한편, 비뇨기과 전문의들이 특발성 정자결핍증을 앓고 있는 남성들에게 클로미펜 시트레이트나 레트로졸을 처방하고 있는 만큼, 약물 및 호르몬 요법은 연평균 성장률(CAGR) 4.65%로 확대되고 있습니다. 2024년 무작위 대조 시험에서 크로미펜 구연산염 투여로 정자 농도가 840만/mL로 개선되었으며, 파트너의 32%에서 자연 임신이 확인되었습니다. 재조합 난포자극호르몬(rFSH)은 여전히 저고나도트로핀 증례로 사용이 제한되고 있지만, 유럽에서는 바이오시밀러의 등장으로 가격이 하락하고 있습니다.

현미경 수술을 통한 정삭정맥류 절제술은 임상적으로 만져질 수 있는 병변에 대해서는 여전히 중요한 역할을 하고 있지만, 2024년 미국비뇨기과학회(AUA) 지침에서는 무증상 환자에 대한 수술이 제한되고 있습니다. 생활 습관 개선이나 항산화 보충제에 대해서는 신뢰할 만한 근거가 제한적이기 때문에 이에 대한 대응은 여전히 제각각인 실정입니다. 개발 중인 유전자 치료 후보들은 유효성과 안전성이 확인된다면 2030년 이후 남성 불임 치료 시장 점유율에 변화를 가져올 가능성이 있지만, 현재로서는 그 도입이 임상시험 단계에 그치고 있습니다.

지역별 분석

2025년 북미는 전 세계 매출의 38.25%를 차지했습니다. 이는 미국 11개 주와 컬럼비아 특별구가 불임 치료에 대한 보험 적용을 의무화하고 있으며, 생식보조의료기술학회(SART)에 등록된 450개 이상의 클리닉이 존재한다는 점이 배경이 되고 있습니다. 고용주의 복리후생 강화와 AI 탑재 기기의 조기 도입으로 안정적인 성장이 유지되고 있지만, 보험 환급 격차로 인해 남성 대상 검사의 보급이 저해되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 5.68%로, 가장 빠른 성장이 전망되는 지역입니다. 중국은 2024년에 수입 ART 기기의 심사 기간을 9개월로 단축했으며, 일부 성에서는 남성 진단 검사를 성 의료보험 적용 목록에 추가했습니다. 인도의 ART법에 따라 2025년까지 인가 시설 수가 22% 증가했으나, 공공 자금은 여전히 제한적이기 때문에 수요가 민간 의료 기관으로 쏠리고 있습니다. 한국, 일본, 호주의 도시 지역에서는 부모 세대의 고령화에 따라 검사 건수가 증가하고 있으며, 이는 남성 불임 시장이 세계 평균을 웃도는 성장을 이루는 한 가지 요인이 되고 있습니다.

유럽은 규모 면에서 2위를 차지하는 지역입니다. 현재 프랑스에서는 미혼 여성과 동성 커플을 대상으로 보조생식술(ART)에 대한 공공 자금 지원이 이루어지고 있어, 파트너에 대한 선별 검사 건수가 증가하고 있습니다. 한편, 독일에서는 40세 미만의 기혼 부부에게 보조생식술(ART) 비용의 50%를 공적 보험으로 지원합니다. 중동 및 아프리카는 의료 인력 부족으로 인해 다른 지역에 뒤처져 있습니다. 남아프리카는 사하라 이남 아프리카의 ART 치료 건수의 60% 이상을 차지하고 있으며, 두바이의 클리닉은 해외 환자들을 유치하고 있습니다. 라틴아메리카에서는 브라질이나 아르헨티나의 제한적인 공공 의료 체계를 피하기 위해 환자들이 미국으로 건너가는 국경 간 환자 수가 증가하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the male infertility market size is expected to grow from USD 4.10 billion in 2025 to USD 4.25 billion in 2026 and is forecast to reach USD 5.08 billion by 2031 at 3.65% CAGR over 2026-2031.

This report is Segmented by Test Type (Conventional Semen Analysis, CASA, and More), Treatment (Medication & Hormone Therapy, ART, and More), Product (Diagnostic Kits & Devices, Therapeutic Drugs, ART Equipment), Distribution Channel (Hospitals & Fertility Clinics, Diagnostic Centres, and More), End User (Fertility Clinics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Male Infertility Market Trends and Insights

Rising Global Infertility Prevalence in Men

Meta-analysis confirms sperm concentration has fallen 1.2% yearly since 1973 and the decline accelerated after 2000 across Africa, Asia and South America. Environmental endocrine disruptors and lifestyle factors such as obesity are linked to poorer motility and DNA integrity, while the median paternal age now exceeds 32 years in most OECD nations. The wider age window for first-time fatherhood overlaps cumulative toxicant exposure, enlarging the male infertility market. Diagnosis still trails prevalence because stigma delays testing by three to five years in many countries.

Growth of Employer-Funded Fertility Benefits

A quarter of large United States employers paid for in-vitro fertilization by late 2024 and federal guidance issued in 2025 clarified that certain diagnostics are excepted benefits under the Affordable Care Act, removing regulatory ambiguity. Plans usually cap lifetime benefits between USD 15,000 and USD 25,000, insufficient for multiple cycles, and often exclude advanced male diagnostics, pushing out-of-pocket spending. European companies are following Germany's model of partial reimbursement, encouraging platform providers to negotiate bundled laboratory services, which realigns referral patterns and raises the profile of male factor testing.

High Out-of-Pocket Costs and Uneven Reimbursement

In the United States a single intracytoplasmic sperm injection cycle costs USD 15,000-30,000, and fewer than 20% of commercial plans pay the full amount. Advanced male diagnostics add USD 1,000-2,500 and are seldom reimbursed. Public systems in France or Israel fund most ART, while India covers fewer than 10% of eligible couples. The funding gap forces 42% of couples into debt greater than USD 10,000, and 28% abandon therapy altogether.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of At-Home Digital Semen Testing

- AI-Enabled Sperm Selection Improving ART Success

- Limited Specialist Workforce and Laboratory Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional semen analysis held 42.18% sector revenue in 2025 yet the sub-segment of genetic and epigenetic panels is growing at 5.22% CAGR through 2031, outpacing all other tests. Falling sequencing costs now allow identification of Y-chromosome deletions or CFTR variants in under 48 hours for less than USD 1,000. Computer-assisted systems equipped with AI tracking reduce technician variability and push laboratories toward standardized protocols. DNA fragmentation assays, although unstandardized today, are adopted in clinics managing recurrent implantation failure, a pattern that hints at future reimbursement when ISO guidance arrives in 2027. Oxidative stress testing and acrosome reaction assays remain niche, limited to research settings. The male infertility market therefore continues to hinge on basic microscopy while transitioning toward molecular diagnostics that promise higher predictive power.

Laboratory-developed genetic tests now fall under the United States Food and Drug Administration's May 2024 rule that expands pre-market review, increasing compliance costs for small stand-alone centers. National health systems diverge on coverage; France reimburses genetic workups after two failed IVF attempts, while most U.S. plans demand abnormal conventional results first, delaying access. These discrepancies influence the male infertility market size for advanced diagnostics, with Asia-Pacific labs adopting multiplex panels faster due to large urban patient pools and commercial pay models.

Assisted reproductive technology commanded 55.21% of segment revenue in 2025 because intracytoplasmic sperm injection is applied in more than 70% of global IVF cycles. Medication and hormone therapy, however, is expanding at 4.65% CAGR as urologists prescribe clomiphene citrate or letrozole to men with idiopathic oligospermia. A 2024 randomized trial showed clomiphene improved concentration by 8.4 million/mL and led to natural pregnancy in 32% of partners. Recombinant follicle-stimulating hormone remains limited to hypogonadotropic cases but biosimilars are reducing prices in Europe.

Microsurgical varicocelectomy retains a role for clinically palpable lesions, yet American Urological Association guidelines of 2024 limit surgery for subclinical cases. Lifestyle interventions and antioxidant supplements stay fragmented with limited high-quality evidence. Pipeline gene therapy candidates may shift the male infertility market share beyond 2030 if efficacy and safety hold, but current uptake is confined to clinical trials.

Geography Analysis

North America generated 38.25% of global revenue in 2025, supported by eleven United States states and the District of Columbia mandating infertility coverage and more than 450 Society for Assisted Reproductive Technology registered clinics. Rising employer benefits and early adoption of AI-enabled equipment sustain stable growth but reimbursement gaps restrain broader male testing.

Asia-Pacific is the fastest growing region at 5.68% CAGR through 2031. China cut review timelines for imported ART devices to nine months in 2024 and several provinces added male diagnostics to provincial insurance lists. India's ART Act spurred a 22% uptick in licensed centers by 2025 yet public funding remains limited, steering demand to private providers. Urban centers in South Korea, Japan and Australia add volume through aging parental demographics, helping the male infertility market outpace global averages.

Europe stands as the second largest region; France now funds ART for single women and same-sex couples, boosting partner screening volumes, while Germany reimburses 50% of ART cost for married couples under 40. The Middle East and Africa trail other regions due to workforce shortages; South Africa handles over 60% of Sub-Saharan cycles, and Dubai clinics draw international clients. Latin America sees growing cross-border traffic as patients bypass limited public capacity in Brazil and Argentina by traveling to the United States.

- AdvaCare

- Andrology Solutions

- Aytu BioScience

- Caerus Biotech

- CinnaGen

- The Cooper Companies

- Ferring International

- Genea Biomedx

- Halotech DNA

- Hamilton Thorne

- Intas Pharmaceuticals

- LabCorp

- Legacy

- Merck

- Microptic S.L.

- MotilityCount (SwimCount)

- Posterity Health

- Vitrolife

- Zydus Lifesciences

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global infertility prevalence in men

- 4.2.2 Growth of employer-funded fertility benefits

- 4.2.3 Rapid adoption of at-home digital semen testing

- 4.2.4 AI-enabled sperm-selection improving ART success

- 4.2.5 Government infertility?insurance mandates in new geographies

- 4.2.6 Pipeline gene- and cell-based therapies for spermatogenic failure

- 4.3 Market Restraints

- 4.3.1 High out-of-pocket costs & uneven reimbursement

- 4.3.2 Limited specialist workforce & lab infrastructure in LMICs

- 4.3.3 Social stigma deterring male testing in key cultures

- 4.3.4 Absence of globally-standardised advanced diagnostic protocols

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Test Type

- 5.1.1 Conventional Semen Analysis

- 5.1.2 Computer-Assisted Semen Analysis (CASA)

- 5.1.3 DNA Fragmentation Tests

- 5.1.4 Oxidative Stress Analysis

- 5.1.5 Genetic & Epigenetic Panels

- 5.1.6 Other Test Types

- 5.2 By Treatment

- 5.2.1 Medication & Hormone Therapy

- 5.2.2 Assisted Reproductive Technology (IVF, ICSI)

- 5.2.3 Varicocele & Microsurgical Procedures

- 5.2.4 Lifestyle, Supplements & Counselling

- 5.3 By Product

- 5.3.1 Diagnostic Kits & Devices

- 5.3.2 Therapeutic Drugs

- 5.3.3 ART Equipment & Disposables

- 5.4 By Distribution Channel

- 5.4.1 Hospitals & Fertility Clinics

- 5.4.2 Diagnostic Centres

- 5.4.3 At-home Testing / DTC Platforms

- 5.4.4 Online & Retail Pharmacies

- 5.5 By End User

- 5.5.1 Fertility Clinics

- 5.5.2 Hospitals

- 5.5.3 Diagnostic Laboratories

- 5.5.4 Home-care Users

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AdvaCare Pharma

- 6.3.2 Andrology Solutions

- 6.3.3 Aytu BioScience

- 6.3.4 Caerus Biotech

- 6.3.5 CinnaGen Co.

- 6.3.6 CooperSurgical

- 6.3.7 Ferring International

- 6.3.8 Genea Biomedx

- 6.3.9 Halotech DNA

- 6.3.10 Hamilton Thorne

- 6.3.11 Intas Pharmaceuticals

- 6.3.12 LabCorp

- 6.3.13 Legacy

- 6.3.14 Merck KGaA (EMD Serono)

- 6.3.15 Microptic S.L.

- 6.3.16 MotilityCount (SwimCount)

- 6.3.17 Posterity Health

- 6.3.18 Vitrolife AB

- 6.3.19 Zydus Lifesciences

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment