|

시장보고서

상품코드

2066601

계단 리프트 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Stair Lift - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

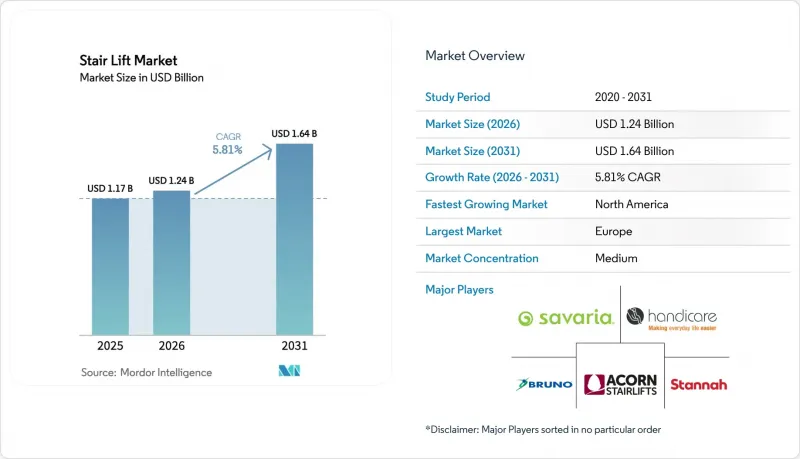

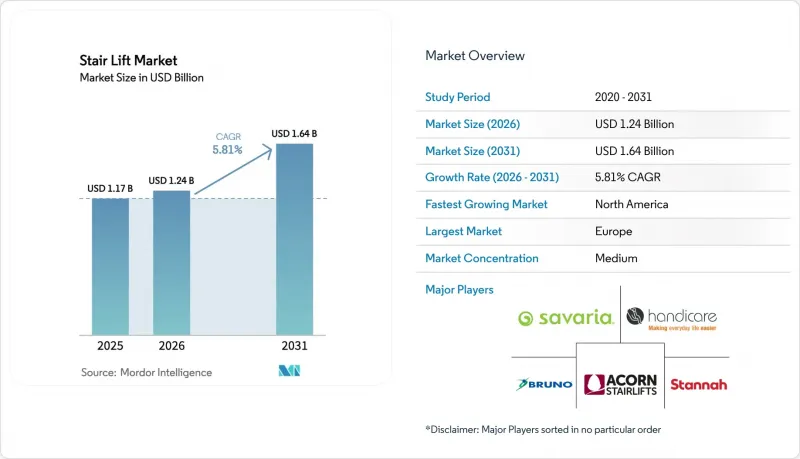

Mordor Intelligence에 의하면, 계단 리프트 시장 규모는 2025년 11억 7,000만 달러로 평가되었고, 2026년에는 12억 4,000만 달러로 추정되고, 2026-2031년 CAGR 5.81%로 성장을 지속하여, 2031년에는 16억 4,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 레일 방향별(직선형 및 곡선형), 이용 자세별(좌석형, 입식형 및 일체형), 설치 장소별(실내 및 실외), 용도별(주거, 의료, 정부 기관, 레저·오락) 및 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 계단 리프트 시장 동향 및 인사이트

인구 고령화의 가속화와 ‘자택에서의 노후 생활(에이징 인 플레이스)’ 보급

65세 이상 인구는 계속 증가하고 있으며, 이에 따라 주거용 이동 지원 솔루션의 잠재 고객층이 확대되면서 계단 리프트 시장의 판매 대수 증가를 뒷받침하고 있습니다. 전 세계적으로 고령화가 진행되고 있으며, 2050년까지 대부분의 지역에서 60세 이상 인구의 비율이 증가함에 따라 안전한 주거 환경을 확보하기 위한 대책에 대한 필요성이 높아지고 있습니다. 지난 수십 년과 비교해 시설에 입소하는 고령자의 수는 감소하고 있으며, 그 대신 계단 리프트나 경사로가 설치된 현관 등 주택 개보수 사업에 예산이 배정되고 있습니다. 3,000-5,000달러 가격대의 직선형 계단 리프트는 많은 가정에 있어 시설에서의 요양을 대체할 수 있는 실용적인 선택지가 되고 있습니다. 노인 친화적인 지역사회를 추진하는 국제적인 공중보건 이니셔티브에서는 배리어프리 주택 설계 및 개조의 중요성이 강조되고 있습니다.

2020년 이후 접근성 기준의 강화 및 건축기준법 개정

ASME A18.1-2023은 2024년 3월에 시행되었으며, 과속도에 대한 시험 기준이 강화되고 비상 통신 요건이 개정되었습니다. 이로 인해 안전성 기준이 높아지면서, 안전 신호만을 바탕으로 한 브랜드 간 차별화가 줄어들고 있습니다. 건축 기준의 조화와 명확한 허가 기준 덕분에 판매업체들은 주 경계를 넘어 지연을 최소화하며 사업을 전개할 수 있게 되었으며, 이를 통해 더 예측 가능한 리드타임과 고객 경험의 향상이 도모되고 있습니다. 이와 병행하여, EN 81-40 및 유럽 접근성 법(European Accessibility Act)과 같은 EU 조화 프로그램을 통해 회원국 간 설계 요건이 표준화되고 있습니다. 이를 통해 촉각식 조작 장치, 문서의 접근성, 일관된 안전 시스템을 위한 기술 로드맵이 명확해졌습니다. 안전성 및 설치 매개변수에 대한 명확성을 높이면 수정 작업을 줄일 수 있으며, 시공업체, 건축가, 검사관 간에 규격에 부합하는 경사 리프트에 대한 일관된 기대치를 공유할 수 있게 됩니다. 이러한 변화는 최종 사용자의 신뢰를 높이고, 위험에 대한 인식을 낮추며, 계단 리프트 시장의 교체 및 업그레이드 주기를 촉진할 것입니다.

메디케어의 제한적인 보장 범위와 높은 본인 부담금

오리지널 메디케어에서는 계단 리프트가 내구성 의료장비로 분류되지 않습니다. 즉, 대부분의 수급자에게는 연방 정부가 정한 표준화된 급여 지급 경로가 없습니다는 뜻입니다. 메디케어 어드밴티지 플랜에서는 보충적인 혜택이 제공되는 경우가 있으나, 그 대상은 플랜마다 다르며 사전 승인이 필요하고 적용 범위도 제한적이기 때문에 카운티별로 이용 격차가 발생하고 있습니다. 메디케이드 면제 제도에 따른 급여 범위는 주마다 다르며, 대기 명단이 길어지는 경우도 있어, 이로 인해 수급 자격이 있는 소비자라도 혜택 적용이 지연될 수 있습니다. 반면, 재향군인부의 주택 보조금은 기준을 충족하는 사람들에게는 상당한 금액이 될 수 있으며, 2026 회계연도에는 최대 12만 6,526달러의 ‘특별 개조 주택(Specially Adapted Housing)’ 보조금이 포함되어 있어, 이를 통해 종합적인 무장애 개조 비용을 충당할 수 있습니다. 직선형 계단 리프트의 가격은 보통 3,000-5,000달러이지만, 곡선형 승강기는 1만 달러를 훨씬 초과하는 경우도 있습니다. 공적·민간 보험 모두 적용되지 않는 경우, 고정 소득을 가진 가구에게는 막대한 본인 부담이 발생합니다.

부문별 분석

2025년 기준으로, 직선형 계단 리프트는 시장 점유율의 54%를 차지했습니다. 이는 설치 기간을 단축하고, 처음 구매하는 분들을 위해 가격을 낮출 수 있는 조립식 레일이 채택되었기 때문입니다. 계단 리프트 시장에서는 일반적인 주택 평면도를 반영한 리모델링 공사에서 직선형이 선호되는 경향이 있으며, 이것이 판매점의 대량 구매와 안정적인 재고 회전율을 뒷받침하고 있습니다. 곡선형 시스템은 모듈식 레일 설계로 인해 리드타임이 단축되고 대응 가능한 계단 유형이 확대됨에 따라, 2026-2031년 연평균 성장률(CAGR) 10.34%로 성장할 것으로 전망됩니다. Harmar가 도입한 모듈식 곡선 플랫폼은 연결형 진단 기능과 좁은 계단에 적합한 슬림형 레일을 채택하여, 이를 통해 일부 도시권에서는 익일 배송이 가능해졌습니다. 급커브에 대응하는 트윈 레일 구조는 유럽의 오래된 주택에서 프리미엄급 설치를 가능하게 하며, 이는 난이도가 높은 프로젝트를 전문으로 하는 딜러에게 이점이 됩니다. 재고가 있는 레일 부재를 활용해 현장에서 신속하게 조립함으로써 설치 속도가 향상되었으며, 긴 제작 기간 없이 맞춤형 곡선 레일을 원하는 구매자들에게 더 많은 선택지가 제공되었습니다.

도입 패턴을 비교해 보면, 일반적인 개보수 공사에서는 직선형 모델이 주류를 이루는 반면, 곡선형 엘리베이터는 나선형 계단, 중간 층계참, 장식적인 형태를 가진 주택에 집중되어 있습니다. 커브형 리프트 시장 규모는 납기 단축과 유지보수성 향상을 위한 모듈식 설계 개선에 힘입어 확대될 것으로 전망됩니다. 경첩이 달린 레일이나 접이식 구간은 계단 랜딩이나 출입구의 통행 폭을 확보하는 데 도움이 되며, 좁은 주거 공간이나 공용 계단에서 규정을 준수할 수 있도록 지원합니다. 실외용 곡선형 모델은 해안가나 자외선이 강한 환경에 적합하도록 내후성과 내식성을 갖추고 있어, 데크로 연결되는 통로나 다단식 실외 계단에서 사용하기에 더욱 매력적인 제품으로 주목받고 있습니다. 이러한 특징들이 복합적으로 작용하여 복잡한 프로젝트의 더 큰 비중이 곡선형 시스템으로 이동하고 있지만, 직선 레일은 여전히 계단 리프트 시장에서 대량 판매의 핵심을 차지하고 있습니다.

좌석형 리프트는 편안함, 직관적인 조작성, 무릎 가동 범위가 제한된 고령자에게 적합한 조절 가능한 좌석을 특징으로 하며, 2025년에는 48%의 시장 점유율을 차지했습니다. 전동 회전 기능과 인체공학적으로 설계된 팔걸이는 층계참에서 승하차를 돕고, 낙상 위험을 줄여줄 뿐만 아니라, 좁은 최상층 층계참에서도 편리하게 사용할 수 있게 해줍니다. 서 있는 형태 및 퍼치형(반쯤 앉은 형태)의 구성은 완전한 착석 자세를 유지할 수 없는 사용자에 대한 임상적 권고에 힘입어 2026-2031년 연평균 성장률(CAGR) 8.76%로 성장할 것으로 전망됩니다. 퍼치형 디자인은 반립자세를 채택하고, 접었을 때의 깊이가 콤팩트하기 때문에 좁은 계단, 특히 도심 밀집 지역에 많은 오래된 주택에서 그 효과를 발휘합니다. 좌식형과 입식형 옵션을 결합한 통합형 모델은 여러 사용자에 대한 유연한 대응이 필수적인 재활 현장에서 그 활용이 점점 더 확대되고 있습니다.

이러한 자세의 조합은 임상적 요구와 가정 환경의 제약을 반영하고 있으며, 계단 리프트 시장 전체의 제품 선정 및 가격 민감도에 영향을 미치고 있습니다. 서 있는 자세형 솔루션은 좁은 공간이나 특정 정형외과적 요구 사항에 적합한 반면, 앉은 자세형 모델은 가장 많은 사용자층에게 있어 편안함의 기준이 되고 있습니다. 개정된 안전 기준에는 시트의 높이 범위와 잡기 편한 그립감을 확보하기 위한 치수가 규정되어 있으며, 이를 통해 각 브랜드 간의 인체공학적 기준이 통일되어 구매자에게 제공되는 안전성이 한층 강화되었습니다. 서 있는 자세용과 앉아 있는 자세용 제품을 모두 취급하는 판매점은 단일 자세 유형에 특화된 브랜드보다 여러 명의 사용자가 있는 가정의 요구에 더 적절하게 대응할 수 있습니다. 앞으로 인체공학적 개선이 점진적으로 이루어짐에 따라, 계단 리프트 업계에서 두 구성 요소 모두에 대한 만족도가 향상되고, 서비스상의 문제도 줄어들 것으로 기대됩니다.

지역별 분석

2025년, 유럽은 전 세계 계단 리프트 시장을 주도하며 시장의 65%를 차지했습니다. 이는 영국, 독일 및 기타 서유럽 국가들에서의 도입이 대폭 확대된 데 기인합니다. EU의 안전 기준 및 문서화 기준의 조화를 통해 국경을 초월한 사업 운영이 효율화되었고, 제품 유형이 줄어든 동시에 여러 국가를 대상으로 한 판매점 전략이 가능해졌습니다. 부가가치세(VAT) 감면 프로그램과 지역별 보조금은 여전히 수요를 견인하고 있지만, 공공 예산의 변동이 분기별 판매량에 영향을 미치고 있습니다. 북유럽 국가들에서는 스마트 홈 도입이 지역 전체적으로 확산되고 있는 것을 반영하여, 커넥티드 모델과 프리미엄 모델에 대한 관심이 높아지고 있습니다. 반면, 동유럽에서는 경제적 제약으로 인해 해당 지역의 더 부유한 시장에 비해 성장이 제한되고 있습니다. 유럽의 명확한 정책 체계와 확립된 유통 네트워크 덕분에, 세계 매출 1위 기업으로서의 입지를 공고히 하고 있습니다.

북미 시장은 2025년 시점에서는 비교적 소규모였으나, 2031년까지 연평균 성장률(CAGR) 10.50%라는 견조한 성장이 예상됩니다. 해당 지역, 특히 미국에서의 가처분 소득 증가와 잘 구축된 판매점 네트워크가 자비로 구매하거나 자주 기종을 바꾸는 현상을 뒷받침하고 있습니다. 고령 인구 증가에 따라 이동 지원 솔루션 및 주택 안전 개보수의 잠재적 고객 기반이 확대되고 있습니다. 재향군인부의 주택 보조금이나 비영리 단체가 추진하는 주택 개보수 프로그램 등 연방 정부의 다양한 노력은 대상 가구의 경제적 부담을 줄이는 데 도움이 되고 있습니다. 또한, 멕시코 내 계단 리프트 제조업체들의 진출 확대에 따라 공급 유연성이 높아지면서, 미국의 선벨트 지역 및 중서부 지역 판매점 네트워크의 배송 비용이 절감되고 있습니다.

아시아태평양에서는 정책적 노력과 인구 동향의 변화가 시장 수요를 재편함에 따라 성장세가 가속화되고 있습니다. 판매점 네트워크의 확대와 배리어프리 주택에 대한 정책적 관심이 높아지면서, 이 지역의 성장을 이끌고 있습니다. 중국 등 주요 경제국의 급속한 고령화와 호주의 ‘익숙한 곳에서 노후를 보내기’라는 정책, 그리고 높은 가구 소득이 맞물려 도시 지역에서의 꾸준한 보급을 뒷받침하고 있습니다. 동남아시아 및 남아시아에서는 초기 도입이 주요 도시의 중산층 및 고소득층 가구에 집중되어 있으며, 이는 초기 시장 동향을 반영하고 있습니다. 공급망이 지역별 수요에 맞추어 변화함에 따라, 아시아태평양의 계단 리프트 시장은 2031년까지 지속적인 성장이 예상되는 유리한 위치에 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the stair lift market size is expected to grow from USD 1.17 billion in 2025 to USD 1.24 billion in 2026 and is forecast to reach USD 1.64 billion by 2031 at 5.81% CAGR over 2026-2031.

This report is Segmented by Rail Orientation (Straight, and Curved), User Orientation (Seated, Standing, and Integrated), Installation (Indoor, and Outdoor), Application (Residential, Healthcare, Government, and Leisure and Entertainment), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Stair Lift Market Trends and Insights

Accelerating Population Aging and Aging-In-Place Adoption

The 65-plus population continues to expand, which enlarges the addressable base for residential mobility solutions and supports unit growth for the stair lift market. Globally, aging is widespread with the share of individuals aged 60-plus rising across most regions through 2050, which increases the need for safe home access interventions. Fewer older adults reside in institutional settings compared with prior decades, which shifts budgets toward home modifications such as stair lifts and ramped entries. Straight stair lifts priced in the USD 3,000 to USD 5,000 range provide a practical alternative to facility-based care for many households. International public health initiatives promoting age-friendly communities emphasize the importance of accessible housing design and retrofits.

Stricter Accessibility Standards and Code Updates Since 2020

ASME A18.1-2023 came into effect in March 2024 with enhanced testing for overspeed and updated emergency communication requirements, which raises baseline safety and reduces brand differentiation based on safety signaling alone. Code harmonization and explicit permitting standards help dealers operate across states with fewer delays, which supports more predictable lead times and better customer experience. In parallel, EU harmonization programs such as EN 81-40 and the European Accessibility Act standardize design requirements across member countries, which channels engineering roadmaps toward tactile controls, documentation accessibility, and consistent safety systems. Greater clarity around safety and installation parameters helps reduce rework and aligns builders, architects, and inspectors with consistent expectations for compliant inclined lifts. These changes improve end-user trust and lower perceived risk, which supports replacement and upgrade cycles in the stair lift market.

Limited Medicare Coverage and High Out-of-Pocket Burden

Original Medicare does not classify stairlifts as durable medical equipment, which means there is no standardized federal coverage pathway for most beneficiaries. Medicare Advantage plans can offer supplemental benefits, yet inclusion is plan-specific, subject to prior authorization, and limited in scope, which produces uneven access across counties. Medicaid waiver coverage varies by state and can involve long waitlists, which slows conversion even for eligible consumers. By contrast, Veterans Affairs housing grants can be substantial for those who meet the criteria, including the Specially Adapted Housing grant of up to USD 126,526 in fiscal year 2026, which can fund comprehensive accessibility upgrades. Straight stairlifts typically cost USD 3,000 to USD 5,000, and curved lifts can reach well above USD 10,000, which places a significant out-of-pocket expense on fixed-income households when no public or private coverage applies.

Other drivers and restraints analyzed in the detailed report include:

- Residential Renovation and Retrofit Momentum in Multi-Story Homes

- Advancements in Battery Backup, Sensors, and Remote Diagnostics

- High Customization Costs for Curved Rails and Complex Installs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight stairlifts held 54% of the stair lift market share in 2025, with pre-fabricated rails that shorten installation windows and lower price points for first-time buyers. The stair lift market favors straight runs in retrofit scenarios that involve common residential layouts, which supports dealer volume purchases and consistent inventory turns. Curved systems are forecast to expand at a 10.34% CAGR from 2026 to 2031 as modular rail designs compress lead times and broaden eligible staircase types. Harmar's modular curved platform introduced connected diagnostics and a thin-rail profile for narrow runs, which helped enable next-day deliveries in select metro areas. Twin-rail configurations for tight bends support premium placements in older European housing stock, which benefits dealers that specialize in high-complexity projects. Faster on-site assembly using stock-able rail sections has improved installation speed and widened choice for buyers who require custom turns without extended fabrication windows.

Comparing adoption patterns shows straight models dominate standardized retrofits while curved lifts concentrate in homes with spirals, mid-landings, and ornate profiles. The stair lift market size for curved lifts is projected to rise in line with modular engineering improvements that cut delivery time and improve serviceability. Hinged rail options and fold-away sections help preserve egress widths at landings and entries, which supports compliance in smaller dwellings and shared stairways. Outdoor curved variants add weatherproofing and corrosion resistance for coastal and high-UV settings, which expands their appeal for deck access and multi-level exterior stairs. Collectively, these features tilt a larger share of complex projects toward curved systems while straight rails remain the high-volume core of the stair lift market.

Seated lifts held 48% share in 2025 based on comfort, intuitive controls, and adjustable seating that suits older adults with limited knee flexibility. Powered swivel options and ergonomic armrests aid transfers at landings, which reduces fall risk and eases use in tight top landings. Standing and perch configurations are projected to grow at an 8.76% CAGR from 2026 to 2031, supported by clinical recommendations for users who cannot tolerate full sitting. Perch designs utilize a semi-standing posture and compact folded depth, which works well on narrow staircases, particularly in legacy homes common in dense urban cores. Integrated models that combine seated and standing options are gaining more use in rehabilitation settings where multi-user flexibility is crucial.

This orientation mix reflects clinical needs and household constraints, which shape product selection and price sensitivity across the stair lift market. Standing solutions fit narrow spaces and certain orthopedic profiles, while seated models set the comfort baseline for the largest user group. Updated safety standards outline seat height ranges and graspability dimensions that help standardize ergonomics across brands, which raises the baseline safety signal for purchasers. Dealers that carry both standing and seated portfolios address multi-user households better than single-orientation brands. Over time, incremental ergonomic refinements are expected to lift satisfaction and reduce service issues in both configurations in the stair lift industry.

Geography Analysis

Europe led the global stair lift market in 2025, accounting for 65% of the market, driven by significant deployment in the United Kingdom, Germany, and other Western European countries. Harmonized EU safety and documentation standards have streamlined cross-border operations, reducing product variations and enabling multi-country dealer strategies. VAT relief programs and localized grants continue to drive demand, although fluctuations in public budgets impact quarterly volumes. Nordic countries are witnessing increased interest in connected and premium models, reflecting the region's advanced adoption of smart homes. In contrast, affordability constraints in Eastern Europe limit growth compared to wealthier markets in the region. Europe's clear policy framework and well-established distribution networks solidify its position as the global revenue leader.

Although North America represented a smaller market base in 2025, it is projected to grow at a robust CAGR of 10.50% through 2031. Higher disposable incomes and mature dealer networks in the region, particularly in the United States, support out-of-pocket purchases and frequent upgrades. The increasing older adult population expands the potential customer base for mobility solutions and home safety retrofits. Federal initiatives, such as Veterans Affairs housing grants and home modification programs facilitated by non-profits, help reduce affordability barriers for eligible households. Additionally, the growing presence of stair lift manufacturers in Mexico enhances supply flexibility and reduces delivery costs for dealer networks in the U.S. Sun Belt and Midwest regions.

The Asi-Pacific region is experiencing growing momentum as policy initiatives and demographic changes reshape market demand. Expanding dealer networks and increased policy focus on barrier-free housing are driving growth in the region. Rapid population aging in major economies like China and Australia's aging-in-place policies, coupled with high household incomes, support steady adoption in urban centers. In Southeast Asia and South Asia, early-stage adoption is concentrated among middle- and upper-income households in major cities, reflecting typical early-market trends. As supply chains adapt to localized demand, the Asia-Pacific stair lift market is well-positioned for sustained growth through 2031.

- Savaria Corporation

- Stannah Lifts Holdings Ltd.

- Acorn Mobility Services Limited

- Bruno Independent Living Aids, Inc.

- TK Access Solutions Limited

- Handicare AB

- Platinum Stairlifts Limited

- Bespoke Stairlifts Limited

- Otolift Trapliften B.V.

- Harmar Mobility, LLC

- AmeriGlide, Inc.

- Lehner Lifttechnik GmbH

- Hawle Treppenlifte GmbH

- HIRO LIFT Hillenkatter + Ronsieck GmbH

- Vimec S.r.l.

- Garaventa (Canada) Ltd.

- Lifeway Mobility Holdings LLC

- Brooks Stairlifts Limited

- Otis Worldwide Corporation

- TK Elevator GmbH

- Access BDD (TK Elevator)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Population Aging and Aging-In-Place Adoption

- 4.2.2 Stricter Accessibility Standards and Code Updates Since 2020

- 4.2.3 Residential Renovation and Retrofit Momentum in Multi-Story Homes

- 4.2.4 Advancements in Battery Backup, Sensors, and Remote Diagnostics

- 4.2.5 Medicaid Waivers and National Grants Unlocking Home Modifications

- 4.2.6 State-Level Adoption of ASME A18.1 and Permit Clarity Reducing Friction

- 4.3 Market Restraints

- 4.3.1 Limited Medicare Coverage and High Out-of-Pocket Burden

- 4.3.2 High Customization Costs for Curved Rails and Complex Installs

- 4.3.3 Egress and ADA Constraints in Non-Residential Stairways

- 4.3.4 Recalls and Liability Concerns Impacting Procurement Confidence

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Rail Orientation

- 5.1.1 Straight

- 5.1.2 Curved

- 5.2 By User Orientation

- 5.2.1 Seated

- 5.2.2 Standing

- 5.2.3 Integrated

- 5.3 By Installation

- 5.3.1 Indoor

- 5.3.2 Outdoor

- 5.4 By Application

- 5.4.1 Residential

- 5.4.2 Healthcare

- 5.4.3 Government

- 5.4.4 Leisure and Entertainment

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Sweden

- 5.5.3.9 Switzerland

- 5.5.3.10 Poland

- 5.5.3.11 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 New Zealand

- 5.5.4.7 Indonesia

- 5.5.4.8 Malaysia

- 5.5.4.9 Thailand

- 5.5.4.10 Vietnam

- 5.5.4.11 Philippines

- 5.5.4.12 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Israel

- 5.5.5.5 Qatar

- 5.5.5.6 Kuwait

- 5.5.5.7 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Morocco

- 5.5.6.5 Kenya

- 5.5.6.6 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Savaria Corporation

- 6.4.2 Stannah Lifts Holdings Ltd.

- 6.4.3 Acorn Mobility Services Limited

- 6.4.4 Bruno Independent Living Aids, Inc.

- 6.4.5 TK Access Solutions Limited

- 6.4.6 Handicare AB

- 6.4.7 Platinum Stairlifts Limited

- 6.4.8 Bespoke Stairlifts Limited

- 6.4.9 Otolift Trapliften B.V.

- 6.4.10 Harmar Mobility, LLC

- 6.4.11 AmeriGlide, Inc.

- 6.4.12 Lehner Lifttechnik GmbH

- 6.4.13 Hawle Treppenlifte GmbH

- 6.4.14 HIRO LIFT Hillenkatter + Ronsieck GmbH

- 6.4.15 Vimec S.r.l.

- 6.4.16 Garaventa (Canada) Ltd.

- 6.4.17 Lifeway Mobility Holdings LLC

- 6.4.18 Brooks Stairlifts Limited

- 6.4.19 Otis Worldwide Corporation

- 6.4.20 TK Elevator GmbH

- 6.4.21 Access BDD (TK Elevator)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment