|

시장보고서

상품코드

2066614

마이크로 열병합발전(CHP) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Micro Combined Heat and Power (CHP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

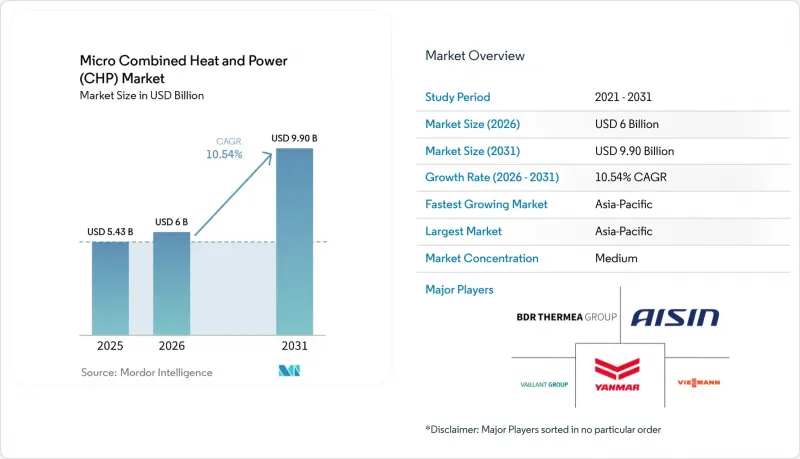

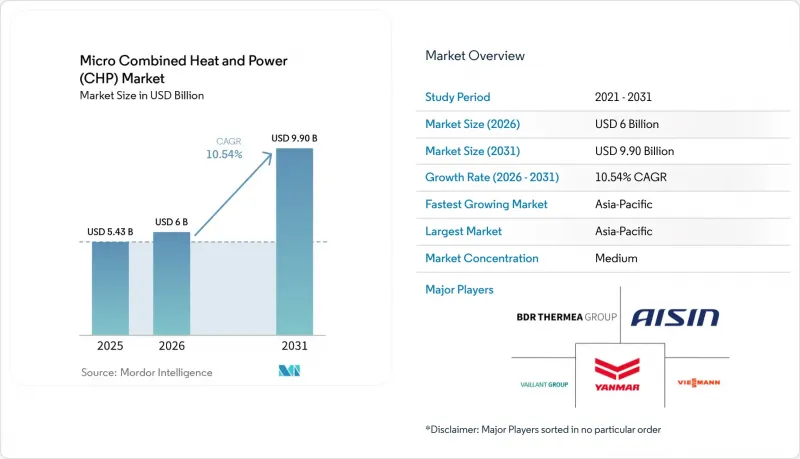

Mordor Intelligence에 의하면, 마이크로 열병합발전 시장 규모는 2025년 54억 3,000만 달러, 2026년 60억 달러에서 2031년까지 99억 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 10.54%를 나타낼 전망입니다.

본 보고서는 연료 유형별(천연가스, 바이오가스/바이오매스, 수소 대응/합성가스), 원동기 기술(내연기관(ICE) 등), 출력 등급(5 KWe 미만, 5-20 KWe, 20-50 KWe, 50-100 KWe), 용도(주택, 공동주택/지역난방, 상업, 산업), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

세계 마이크로 열병합발전(CHP) 시장 동향 및 인사이트

일본 및 EU에서 주거용 연료전지 마이크로 CHP 도입이 급증하고 있습니다.

마이크로 열병합발전 시장은 일본에서 오랫동안 시행되어 온 ‘ENE-FARM’ 제도의 지원을 받고 있으며, 이 제도는 주거용 연료전지의 대규모 도입을 지속적으로 주도하고 있습니다. 일본 경제산업성(METI)의 ‘2025년 절전 장려금’ 제도에 따르면, 기본 유닛 1대당 16만 엔(1,050달러), 계통 연계형 모델에는 4만 엔(260달러)의 보조금이 지급되고 있으며, 이 제도는 단순한 독립형 발전기로 기능하는 것이 아니라 계통 연계 운전이 가능한 유닛을 명백히 우대하는 것입니다. 이 설계는 보조금 지원 대상이 되는 각 설비가 주택 부문의 미래 가상 발전소 기반을 강화하는 데에도 기여하기 때문에 소규모 열병합발전 시장에 유익합니다. 독일도 연료전지 난방 지원 제도의 개정을 통해 비슷한 길을 걷고 있으며, 2024년 1월에 개정된 KfW 433 체계에서는 연료전지 설비에 대해 30-70%의 자금 지원이 제공되게 되었습니다. 아이신(AISIN)이 2026년 3월에 출시할 ‘ENE-FARM 유형 S’(태양광 발전 우선형)는 저발열량 기준에서 발전 효율이 55% 향상되었으며, 태양광 발전 우선 운전 제어 기능을 통합하고 있어, 마이크로 열병합발전 시장이 열 회수 범위를 넘어 가정용 에너지 관리 하드웨어로 전환되고 있음을 보여줍니다.

러시아·우크라이나 분쟁 이후 에너지 안보를 위한 현장 발전 추진

러시아·우크라이나 분쟁 이후 유럽의 에너지 정책 전환으로 인해 에너지 안보가 투자 판단의 핵심 요소로 부상하면서, 소규모 열병합 발전 시장이 강화되었습니다. 이 시장에서 현장 발전은 더 이상 단순한 탄소 감축 수단으로만 간주되지 않습니다. 많은 구매자들이 송전망이나 연료 공급이 중단되었을 때에도 열과 전력의 지속성을 보장하는 회복탄력성 자산으로서 그 가치를 높이 평가하고 있기 때문입니다. 병원, 호텔, 데이터센터 등 지속적인 에너지 수요가 있는 시설에서는 운영 위험을 줄일 수만 있다면 시스템 비용이 높아지더라도 이를 수용하려는 경향이 강해지고 있습니다. Capstone Green Energy가 2025년 10월 마이크로그리드 4AI와 체결한 양해각서(MOU)는 마이크로 열병합발전 시장이 기존의 주거용 난방 수요를 훨씬 뛰어넘어, AI 관련 데이터센터의 이중화 같은 이용 사례로까지 확대되고 있음을 보여줍니다. 이처럼 구매자층이 확대됨에 따라 특정 보조금 프로그램에 대한 의존도가 낮아지고, 상업, 공공기관, 특수 전력 용도에 걸쳐 마이크로 열병합발전 시장은 더욱 탄탄한 수요 기반을 구축할 수 있습니다.

응축식 보일러나 히트 펌프에 비해 높은 초기 비용

마이크로 열병합발전 시장은 주거용 분야에서 여전히 뚜렷한 비용 장벽에 직면해 있습니다. 그 이유는 많은 시스템이 응축식 보일러나 대부분의 일반적인 난방 대체 수단에 비해 설치 비용이 여전히 훨씬 비싸기 때문입니다. 이러한 가격 차이는 단독주택의 경우 특히 큰 문제가 됩니다. 이러한 주택의 경우, 투자 회수를 위해서는 높은 가동률, 유리한 전력 판매 요금, 그리고 넉넉한 보조금이 필수적이기 때문입니다. 또한, 마이크로 열병합발전 시장에서는 연료전지 시스템의 설치가 더욱 복잡하며, 숙련된 기술자가 부족한 지역에서는 프로젝트 비용이 상승하게 됩니다. 구매자들은 제품 수명 주기 전반에 걸친 가치가 아니라 표면적인 설치 가격만을 비교하는 경우가 많으며, 그 결과 훨씬 더 긴 가동 기간 동안 비용 절감 효과를 가져다주는 시스템의 판매 설득력이 약화되고 맙니다. 생산량이 충분히 증가하고 더 대규모의 제조 체제가 갖춰질 때까지는 가격에 민감한 지역에서 초기 비용이 마이크로 열병합발전 시장의 큰 걸림돌로 남아 있을 것입니다.

부문별 분석

2025년, 소규모 열병합발전 시장에서 천연가스는 64.1%의 점유율을 차지했습니다. 이는 유럽, 북미, 동아시아의 기존 가스 공급망 인프라의 보급 범위와, 이미 가스 이용에 최적화된 설비의 방대한 도입 실적을 반영한 것입니다. 마이크로 열병합발전 시장에서 도입 실적은 여전히 중요한 요소입니다. 왜냐하면 유지보수 노하우, 연료의 확보 가능성, 그리고 구매자의 익숙함 등의 측면에서 이미 확립된 가스 기반 시스템이 새로운 대안보다 우위에 있기 때문입니다. 도쿄가스는 이미 ENE-FARM 장치를 대상으로 한 20% 수소 혼합 시범 사업을 시작했으며, 이는 가스 부문이 고정된 것이 아니라 시간이 지남에 따라 점차 청정 연료를 도입하기 시작하고 있음을 보여줍니다. 바이오가스와 바이오매스는 여전히 규모는 작지만, 농업 잔여물과 지역 밀착형 연료 공급이 분산형 발전을 뒷받침하는 북유럽 및 중부 유럽에서는 전략적 가치를 지니고 있습니다. 2026년 3월에 완료된 µBIO CHP 프로젝트에서는 2.5 kWe의 SOFC와 15 kW의 목재 펠릿 가스화 장치를 결합하여 90% 이상의 종합 효율을 달성했습니다. 이는 Off-grid나 농촌 지역에서의 이용 사례를 통해 바이오매스를 연료로 사용하는 시스템의 유효성을 입증하는 것입니다.

수소 및 합성가스 플랫폼은 소규모 열병합발전 시장 내에서 가장 빠르게 성장하고 있는 연료 부문으로, 2031년까지 연평균 성장률(CAGR)이 15.3%를 나타낼 것으로 전망됩니다. 이러한 성장은 향후 규제 준수에 중점을 둔 구매 태도를 반영한 것으로, 구매자들은 수소 혼합 비율이 확대되거나 배출 규제가 강화되더라도 계속 가동할 수 있는 시스템을 원하고 있기 때문입니다. MWM사의 ‘25H2’ 개조 패키지는 기존 가스 엔진 소유주들에게 시스템 전체를 교체하지 않고도 혼합 연료 운전으로 전환할 수 있는 실용적인 방안을 제공하며, 이는 비용에 민감한 상업용 자산에 있어 중요한 요소입니다. ‘SO-FREE’ 프로젝트와 AISIN의 순수소 SOFC 실증 실험은 마이크로 열병합발전 업계가 시간이 지남에 따라 부분적인 혼합 연료 운전에서 완전한 수소 운전으로 전환할 수 있는 시스템으로 발전하고 있음을 보여줍니다. 상업 및 공공기관의 구매자들은 일반 가정보다 이 분야를 더 빠르게 도입하고 있습니다. 이는 자산의 사용 연한이 길기 때문에 비주거용 자산 조달 시 ‘좌초 자산’ 위험이 더욱 심각해지기 때문입니다.

2025년 현재, 내연 기관은 마이크로 열병합발전 시장의 40.7%를 차지하고 있으며, 서비스 네트워크가 잘 구축되어 있고, 교체 부품 조달이 용이하며, 설치 비용이 연료전지 시스템보다 저렴하다는 점 때문에 여전히 중요한 위치를 차지하고 있습니다. 이러한 도입 실적을 바탕으로, 내연기관 공급업체는 마이크로 열병합발전 시장, 특히 최대 발전 효율보다 유지보수 경험과 노하우가 더 중요시되는 상업시설 분야에서 확고한 입지를 다지고 있습니다. 2024년 『Nature Communications』에 게재된 연구에 따르면, 교류 전력 효율 35.2%, CHP 종합 효율 93%를 초과하는 대향 피스톤 엔진이 보고되었으며, 이는 엔진 혁신이 기존의 성능 수준에서 정체되지 않고 여전히 진전을 이어가고 있음을 보여줍니다. 스털링 엔진은 소음 저감이 더욱 요구되는 주거용 환경에서 계속해서 활용되고 있는 반면, 마이크로터빈은 다양한 연료를 사용할 수 있는 유연성과 체계적인 서비스 계약을 통한 원격 모니터링을 원하는 상업용 사용자들로부터 지지를 받고 있습니다. 즉, 관심이 고효율 전기화학 시스템으로 옮겨가고 있는 상황에서도, 기술의 조합은 여전히 다양합니다.

연료전지 시스템은 소규모 열병합발전 시장에서 가장 빠르게 성장하고 있는 동력원 부문으로, 2031년까지 13.2%의 성장률이 예상됩니다. SO-FREE 플랫폼은 수소 혼합률이 0-100% 범위에서 90-94%의 종합 효율을 달성하고 있으며, 이를 통해 연료전지는 효율을 중시하는 제품 포지셔닝 측면에서 뚜렷한 우위를 보이고 있습니다. Elcogen은 2026년 5월, elcoStack E3000 G2를 출시하고 탈린의 스택 생산 능력을 360 MW로 확대함으로써 한 걸음 더 나아갔습니다. 이 회사는 이 플랫폼의 전기 효율이 75%라고 주장하고 있습니다. 마이크로 열병합발전 시장에서 이러한 진전은 중요한 의미를 지닙니다. 왜냐하면 발전 출력이 향상되면 현장의 경제성이 개선되어, 계통 연계 운전 및 전력 판매를 통한 수익의 근거를 강화할 수 있기 때문입니다. 공급 규모가 더욱 확대됨에 따라, 경쟁상의 차별화 요소는 스택 생산 자체에서 제어, 통합, 디지털 서비스 및 현장 신뢰성으로 점차 이동할 것으로 보입니다.

지역별 분석

2025년 기준으로 아시아태평양은 소형 열병합발전 시장 규모의 49.2%를 차지하고 있으며, 이 지역은 2031년까지 연평균 성장률(CAGR) 10.8%로 성장할 것으로 전망됩니다. 일본에서는 ‘ENE-FARM’ 지원 제도를 통해 주택용 연료전지 및 계통 연계 설비에 대한 수요가 지속적으로 유도되고 있기 때문에 일본은 계속해서 지역 내 마이크로 열병합발전 시장의 중심적인 위치를 차지하고 있습니다. 경제산업성(METI)의 2025년도 보조금 제도는 계통 연계형 모델에 대한 추가 지원을 포함하고 있으며, 이를 통해 협력적인 분산형 에너지 서비스의 도입 기반이 더욱 확대될 것으로 기대됩니다. 일본의 제7차 에너지 기본계획에서는 수소가 차세대 에너지 운반체로 재확인되었으며, Tokyo Gas가 ENE-FARM 유닛을 대상으로 실시하고 있는 20% 수소 혼합 시범 사업은 정책의 야심과 실용적인 네트워크 시험이 어떻게 연계되어 있는지를 보여주고 있습니다. 중국은 분산형 에너지 정책을 지원함으로써 그 규모를 확대하고 있는 반면, 한국과 호주는 보다 광범위한 탈탄소화 목표와 연계된 회복탄력성을 중시하는 에너지 전략을 통해 수요를 견인하고 있습니다.

유럽은 마이크로 열병합발전 시장 점유율 구조에서 2위를 차지하는 지역 블록이며, 동시에 규제가 가장 엄격한 지역이기도 합니다. 독일은 주거용 및 상업용 분야 모두에서 지역 수요를 뒷받침하고 있는 반면, 영국은 소규모 상업용 및 주거용 시스템에 대한 유럽 수요 기반 중 일부로 남아 있습니다. 2028년부터 시행될 고효율 기준 강화 및 2035년부터 화석 연료 단독 사용 금지 등 EU 규제 준수 일정에 따라, 소형 열병합 발전 시장의 각 업체들은 단기적인 가스 사용뿐만 아니라 향후 더 청정한 연료에도 대응할 수 있도록 현행 시스템의 설계를 진행하고 있습니다. 프랑스, 이탈리아, 스페인, 네덜란드는 유럽 시장에서 다음 그룹을 형성하고 있으며, 2026년 1월부터 도입될 아일랜드의 디지털 고효율 CHP 인증 절차는 행정적 마찰을 줄임으로써 보다 안정적인 프로젝트 파이프라인을 뒷받침하고 있습니다.

북미에서는 풍부한 건축물 재고와 이에 따른 열 수요가 있음에도 불구하고, 마이크로 열병합발전 시장은 여전히 충분히 활용되지 못하고 있습니다. 미국에서는 낮은 가스 가격, 넷 미터링 규정의 불일치, 그리고 일본식 주택용 연료전지 보조금 제도의 부재로 인해 일반 가정으로의 보급이 제한되고 있어, 도입은 여전히 경공업 및 상업시설에 집중되어 있습니다. 캐나다에서는 추운 주를 중심으로 공동주택을 대상으로 한 더욱 강력한 이용 사례의 시범 도입이 시작되고 있습니다. 한편, 멕시코에서는 전력 비용 관리가 점점 더 전략적인 과제로 부상함에 따라 마이크로터빈 및 내연기관(ICE) 시스템에 새로운 시장 기회가 열리고 있습니다. 남미에서는 브라질의 바이오가스 연계형 CHP의 잠재력과 아르헨티나의 회복력에 대한 수요가 여전히 핵심을 이루고 있습니다. 한편, 중동 및 아프리카는 사우디아라비아와 아랍에미리트(UAE)의 산업 다각화, 그리고 남아프리카공화국의 송전망 신뢰성에 대한 우려를 배경으로 여전히 초기 단계 시장에 머물러 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the micro combined heat and power market size is projected to expand from USD 5.43 billion in 2025 and USD 6 billion in 2026 to USD 9.90 billion by 2031, registering a CAGR of 10.54% between 2026 and 2031.

This report is Segmented by Fuel Type (Natural Gas, Biogas/Biomass, Hydrogen-ready/Synthetic Gas), Prime-Mover Technology (ICE and More), Capacity Class (less Than 5, 5-20, 20-50, 50-100 KWe), Application (Residential, Multi-Family/District, Commercial, Industrial), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Value (USD).

Global Micro Combined Heat and Power (CHP) Market Trends and Insights

Surging Residential Fuel-Cell Micro-CHP Roll-outs in Japan and EU

The micro combined heat and power market is gaining support from Japan's long-running ENE-FARM framework, which continues to shape residential fuel-cell procurement at scale. METI's 2025 Kyutou Shoene subsidies provide JPY 160,000, USD 1,050, per base unit and JPY 40,000, USD 260, for network-connected models, and that structure clearly favors units that can participate in grid-interactive operation rather than act only as stand-alone generators. The micro combined heat and power market benefits from that design because each subsidized installation also strengthens a future virtual power plant base in the residential sector. Germany is following a similar path through revised fuel-cell heating support, with the KfW 433 framework updated in January 2024 to provide 30-70% funding coverage for fuel-cell appliances. AISIN's March 2026 launch of the solar-priority ENE-FARM type S, with 55% lower-heating-value electrical efficiency and integrated PV-priority dispatch, shows how the micro combined heat and power market is moving beyond heat recovery and into household energy-management hardware.

Energy-Security Push for On-site Generation Post-Russia-Ukraine

The micro combined heat and power market has been strengthened by the shift in European energy policy after the Russia-Ukraine conflict, which pushed energy security into the center of investment decisions. In this market, on-site generation is no longer viewed only as a carbon-saving option, because many buyers now value it as a resilience asset that protects heat and power continuity during grid or fuel disruptions. Hospitals, hotels, data centers, and other facilities with continuous energy loads are increasingly willing to accept a higher system cost when that cost reduces operational risk. Capstone Green Energy's October 2025 MOU with Microgrids 4 AI shows that the micro combined heat and power market is now also reaching AI-linked data-center redundancy use cases that sit well beyond traditional residential heating demand. This broader buyer mix reduces reliance on any single subsidy program and gives the micro combined heat and power market a more resilient demand base across commercial, institutional, and specialty power applications.

High Upfront Cost vs Condensing Boilers and Heat Pumps

The micro combined heat and power market still faces a clear cost barrier in residential applications because many systems remain far more expensive to install than condensing boilers and many standard heating alternatives. This price gap is especially difficult in single-family homes, where payback depends on high utilization, supportive export tariffs, and strong subsidy coverage. The micro combined heat and power market also carries additional installation complexity in fuel-cell systems, and that raises project costs where trained technicians are scarce. Buyers often compare headline installed price rather than full life-cycle value, which weakens the sales case for systems that deliver savings over a much longer operating period. Until production volumes rise enough to deliver broader manufacturing scale, upfront cost will remain a meaningful brake on the micro combined heat and power market in price-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- Emissions Regulations Rewarding High-Efficiency Cogeneration

- Hydrogen-Ready Micro-CHP Platforms Unlock Future Fuel Flexibility

- Rapid Cost Declines of Electric Heat Pumps and Storage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Natural gas commanded 64.1% of the micro combined heat and power market in 2025, reflecting the reach of existing gas-grid infrastructure in Europe, North America, and East Asia, and the large installed base of units already optimized around gas use. In the micro combined heat and power market, the installed base still matters because service know-how, fuel availability, and buyer familiarity all favor established gas-based systems over newer options. Tokyo Gas has already initiated a 20% hydrogen-blend pilot for ENE-FARM units, which shows that the gas segment is not fixed and is starting to absorb cleaner fuel content over time. Biogas and biomass remain smaller in volume, yet they hold strategic value in Northern and Central Europe, where agricultural residues and localized fuel supply can support distributed generation. The µBIO CHP project, completed in March 2026, demonstrated a 2.5 kWe SOFC combined with a 15 kW wood-pellet gasifier and achieved above 90% total efficiency, which supports the case for biomass-fed systems in off-grid or rural use cases.

Hydrogen-ready and synthetic-gas platforms are the fastest-growing fuel segment in the micro combined heat and power market, with a projected 15.3% CAGR through 2031. That growth reflects a purchasing mindset focused on future compliance, because buyers want systems that can continue operating as hydrogen blending expands and emissions rules tighten. MWM's 25H2 retrofit path gives existing gas-engine owners a practical route into blended-fuel operation without replacing complete systems, which is important for cost-sensitive commercial assets. The SO-FREE project and AISIN's pure-hydrogen SOFC demonstration show that the micro combined heat and power industry is also advancing toward systems that can move from partial blends to full hydrogen operation over time. Commercial and institutional buyers are adopting this segment faster than households because longer asset lives make stranded-asset risk more material in non-residential procurement.

Internal-combustion engines held 40.7% of the micro combined heat and power market in 2025, and they remain important because service networks are mature, replacement parts are easy to source, and installed costs are lower than for fuel-cell systems. This installed base gives ICE vendors a durable position in the micro combined heat and power market, especially in commercial sites where maintenance familiarity matters more than maximum electrical efficiency. A 2024 Nature Communications study reported an opposed-piston engine with 35.2% AC electrical efficiency and above 93% total CHP efficiency, which shows that engine innovation is still moving forward rather than stopping at legacy performance levels. Stirling engines continue to serve quieter residential settings, while micro-turbines appeal to commercial users who want multi-fuel flexibility and remote monitoring through structured service contracts. That means the technology mix remains broad even as attention shifts toward higher-efficiency electrochemical systems.

Fuel-cell systems are the fastest-growing prime-mover category in the micro combined heat and power market, with forecast growth of 13.2% through 2031. The SO-FREE platform reached 90-94% total efficiency across a 0-100% hydrogen range, which gives fuel cells a clear advantage in efficiency-led product positioning. Elcogen added another step in May 2026 by launching the elcoStack E3000 G2 and scaling stack manufacturing capacity to 360 MW at Tallinn, with a claimed 75% electrical efficiency for the platform. In the micro combined heat and power market, these gains matter because better electrical output improves on-site economics and can strengthen the case for grid-connected operation and export revenue. As supply scales further, competitive differentiation is likely to move away from stack production alone and more toward controls, integration, digital service, and field reliability.

Geography Analysis

Asia-Pacific represented 49.2% of the micro combined heat and power market size in 2025, and the region is projected to grow at a 10.8% CAGR through 2031. Japan remains the anchor of the regional micro combined heat and power market because ENE-FARM support continues to channel demand toward residential fuel cells and grid-connected installations. METI's 2025 subsidy design gives additional support to network-connected models, which helps build a broader installed base for coordinated distributed energy services. Japan's 7th Basic Energy Plan reaffirmed hydrogen as a next-generation energy carrier, and Tokyo Gas's 20% hydrogen-blend pilot for ENE-FARM units shows how policy ambition is being matched by practical network testing. China adds scale through distributed-energy policy support, while South Korea and Australia contribute demand through resilience-focused energy strategies tied to broader decarbonization goals.

Europe is the second-largest regional block in the micro combined heat and power market share structure, and it is also the most regulation-intensive. Germany anchors regional demand in both residential and commercial use, while the United Kingdom remains part of the European demand base for smaller commercial and residential systems. The EU's compliance timeline, with stricter high-efficiency thresholds from 2028 and fossil-only exclusion from 2035, is pushing vendors in the micro combined heat and power market to design current systems for cleaner future fuels rather than near-term gas use alone. France, Italy, Spain, and the Netherlands form the next group of European markets, and Ireland's digital HE CHP certification process from January 2026 supports a steadier project pipeline by lowering administrative friction.

North America remains underused in the micro combined heat and power market despite strong building stock and relevant thermal demand. The United States still concentrates deployment in light industrial and commercial settings because lower gas prices, uneven net-metering rules, and the absence of a Japan-style residential fuel-cell subsidy limit household penetration. Canada is beginning to test stronger multi-family use cases in colder provinces, while Mexico offers an emerging opening for micro-turbine and ICE systems where power-cost management is becoming more strategic. South America remains centered on Brazil's biogas-linked CHP potential and Argentina's resilience needs, while the Middle East and Africa stay early-stage markets led by industrial diversification in Saudi Arabia and the UAE and by grid-reliability concerns in South Africa.

- Vaillant Group

- Viessmann Group

- Yanmar Holdings

- BDR Thermea (Remeha)

- AISIN Corporation

- Navien Inc.

- Qnergy

- SOLIDpower Group

- 2G Energy AG

- EC Power A/S

- ATCO Ltd

- Enginuity Power Systems

- Helbio S.A.

- Enexor Bioenergy

- GRIDIRON LLC

- TEDOM A.S.

- M-TRONIC Microturbines

- Capstone Green Energy

- Axiom Energy Group

- Bosch Thermotechnology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Scope of the Study

- 1.2 Study Assumptions & Market Definition

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging residential fuel-cell Micro-CHP roll-outs in Japan & EU

- 4.2.2 Energy-security push for on-site generation post-Russia-Ukraine

- 4.2.3 Emissions regulations rewarding high-efficiency cogeneration

- 4.2.4 Hydrogen-ready Micro-CHP platforms unlock future fuel flexibility

- 4.2.5 Hybrid Micro-CHP?+?heat-pump solutions for cold-climate buildings

- 4.3 Market Restraints

- 4.3.1 High upfront cost vs condensing boilers & heat-pumps

- 4.3.2 Rapid cost declines of electric heat-pumps & storage

- 4.3.3 Installer skill-gap for fuel-cell maintenance

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Fuel Type

- 5.1.1 Natural Gas

- 5.1.2 Biogas / Biomass

- 5.1.3 Hydrogen-ready / Synthetic gas

- 5.2 By Prime-Mover Technology

- 5.2.1 Internal-Combustion Engine (ICE)

- 5.2.2 Stirling Engine

- 5.2.3 Micro-Turbine

- 5.2.4 Fuel Cell (PEM, SOFC)

- 5.3 By Capacity Class

- 5.3.1 Less than 5 kWe

- 5.3.2 5 - 20 kWe

- 5.3.3 20 - 50 kWe

- 5.3.4 50 - 100 kWe

- 5.4 By Application

- 5.4.1 Residential Single-Family

- 5.4.2 Multi-Family / District Housing

- 5.4.3 Commercial (Retail, Offices, Hospitality)

- 5.4.4 Industrial & Institutional Facilities

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Vaillant Group

- 6.4.2 Viessmann Group

- 6.4.3 Yanmar Holdings

- 6.4.4 BDR Thermea (Remeha)

- 6.4.5 AISIN Corporation

- 6.4.6 Navien Inc.

- 6.4.7 Qnergy

- 6.4.8 SOLIDpower Group

- 6.4.9 2G Energy AG

- 6.4.10 EC Power A/S

- 6.4.11 ATCO Ltd

- 6.4.12 Enginuity Power Systems

- 6.4.13 Helbio S.A.

- 6.4.14 Enexor Bioenergy

- 6.4.15 GRIDIRON LLC

- 6.4.16 TEDOM A.S.

- 6.4.17 M-TRONIC Microturbines

- 6.4.18 Capstone Green Energy

- 6.4.19 Axiom Energy Group

- 6.4.20 Bosch Thermotechnology

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment