|

시장보고서

상품코드

2066649

서지 보호 장치 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Surge Protection Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

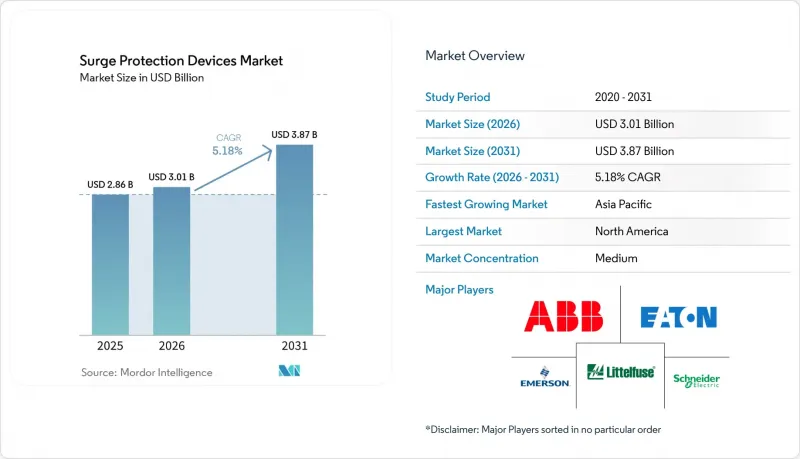

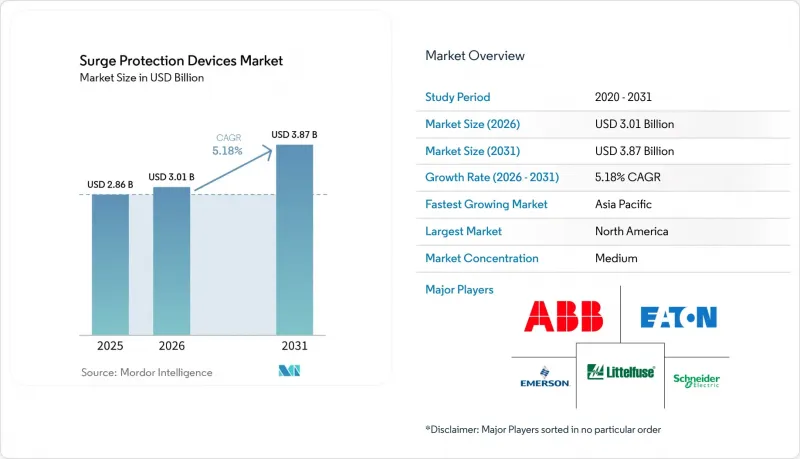

Mordor Intelligence에 의하면, 2026년 서지 보호 장치 시장 규모는 30억 1,000만 달러로 추정되고 있어 2025년 28억 6,000만 달러에서 확대해, 2031년에는 38억 7,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 5.18%로 성장할 것으로 전망됩니다.

본 보고서는 설치 유형(하드와이어드, 플러그인, 라인 코드), 방전 전류 정격(10KA 이하, 10KA-25KA, 25KA 이상), 전압 등급(저전압(1 kV 미만), 중전압(1-35 kV), 고전압(35 kV 이상)), 최종 사용자 업종(산업용, 상업용, 주거용) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 서지 보호 장치 시장 동향 및 인사이트

스마트 홈 및 IoT 기기의 보급 확대

현재 스마트 홈 생태계에는 1만 5,000달러 이상의 가치를 지닌 전자 기기가 탑재되어 있는 경우가 많으며, 서지가 발생할 경우 가정은 심각한 경제적 위험에 노출됩니다. 연결된 조명, 가전제품, 보안 시스템에 탑재된 마이크로프로세서는 전압 과도 현상에 매우 민감하여, 하나의 노드에 손상을 주는 서지가 네트워크 전체로 파급될 가능성이 있습니다. 따라서 개별 콘센트용 서지 보호 장치 대신 주택 전체를 대상으로 한 서지 보호가 주류를 이루고 있으며, 각 제조업체는 설치를 간소화하기 위해 전원 라인과 데이터 라인의 보호 기능을 하나의 케이스에 통합하고 있습니다. 보험사들도 보호 조치가 취해진 주택의 보험료를 인하함으로써 이러한 추세를 뒷받침하고 있으며, 이는 주택 부문 수요를 끌어올리고 있습니다. 홈 오토메이션 플랫폼에 대한 친숙도가 높아짐에 따라, 기능이 풍부하면서도 설치가 간편하고, 모바일 앱과 연동하여 상태 알림을 받을 수 있는 플러그인형 SPD의 사용자층이 더욱 확대되고 있습니다.

재생에너지 도입에 따른 전력 계통의 불안정성 확대

2030년까지 풍력 및 태양광 발전이 전 세계 발전량의 40% 이상을 공급할 것으로 예상되지만, 인버터 기반 전원에는 기존 보호 릴레이가 요구하는 높은 고장 전류가 부족합니다. 전력 회사가 변동하는 출력에 맞추어 발전량을 조절함에 따라, 스위칭으로 인한 과도 현상이 더욱 빈번하게 발생하게 되어, 기존의 보호 방식에 있어 과제가 되고 있습니다. 디지털 릴레이와 데이터 기반 아크 플래시 제어 방식이 주목을 받으면서, 더 넓은 전압 범위와 변동하는 파형에서도 확실하게 작동하는 서지 보호 장치에 대한 수요가 생겨나고 있습니다. 현재의 혁신은 낙뢰로 인한 현상과 스위칭으로 인한 현상 모두에 대응할 수 있는 장치에 초점을 맞추고 있으며, 열 차단 기술을 통해 MOV 소자의 조기 열화를 방지하고 있습니다.

기존 시설의 개보수 및 설치 비용이 높다는 점

수십년전에 건설된 플랜트에 건물 전체에 걸친 서지 보호 시스템을 도입하려면, 대부분의 경우 배전반 업그레이드, 배관 경로 변경, 심지어 일시적인 가동 중단까지 필요하게 됩니다. 상업용 등급 장비의 자재비는 300-700달러이며, 전문 업체에 의뢰할 경우 배전반 1대당 시공비는 100-200달러가 소요되지만, 생산 중단으로 인한 손실은 하드웨어 비용을 훨씬 초과할 가능성이 있습니다. 많은 시설은 낮은 수익률로 운영되고 있어, 법규 개정이나 보험 갱신에 따라 의무화될 때까지 시설 개선을 미루고 있습니다. 각 벤더사는 설치 기간을 단축하는 버스 마운트형 개조 키트나 스플릿 코어 방식의 전류 감지 설계 등을 제안하며 대응하고 있지만, 특히 인프라가 노후화된 성숙한 산업국에서는 투자 회수 기간이 길어질 것으로 간주되고 있다는 점이 여전히 도입의 걸림돌이 되고 있습니다.

부문별 분석

시설 엔지니어들은 배전반이나 분배반에 영구적으로 내장된 장치를 선호하기 때문에 2025년 매출액 중 하드와이어드 방식이 45.40%를 차지했습니다. 이 구성은 투과 전압이 가장 낮기 때문에 가동 시간이 최우선으로 고려되는 생산 라인, 클린룸, 데이터센터에서는 기본 선택 사항으로 자리 잡고 있습니다. 스마트형에는 현재 현장에서 교체 가능한 모듈과 유지보수 일정을 간소화하는 웹 기반 대시보드 등이 포함되어 있습니다.

플러그인형 SPD는 시장 점유율 면에서는 뒤처져 있지만, 스마트 홈 열풍이 지속되는 가운데 2026년부터 2031년까지 6.05%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 보험료 우대 조치와 앱을 통한 전력 품질 분석 기능 덕분에 주택 소유자들은 기본적인 멀티탭에서 네트워크 연결형 모델로 업그레이드하도록 권장받고 있습니다. 라인 코드 유형은 슬림한 본체와 내장된 RJ45 포트를 활용하여 전력과 신호를 모두 보호함으로써, 중요한 서버와 AV 기기를 확실하게 지켜줍니다. 규제 기관이 보호 요건을 확대하는 가운데, 시스템 전반의 연동을 요구하는 상업용 빌딩에서는 유선식 서지 모듈과 하류의 멀티탭을 결합한 하이브리드형 장치가 등장하고 있습니다.

중용량(10 kA-25 kA) 제품은 사무실 건물, 소매 체인점, 경공업 작업장에서 가격과 성능의 균형을 잘 맞춘 덕분에 2025년 매출의 51.30%를 차지했습니다. 각 제조업체는 IEC 61643-11 유형 2의 제한 사항을 충족하면서도 설치 면적을 콤팩트하게 유지하기 위해 부품 수를 최적화하고 있습니다. 이 부문은 서비스 입구 장치가 고에너지 현상에 대응하고, 하류의 배전반이 10 kA-25 kA 모듈을 통한 정밀한 클램프 보호에 의존하는 협력적 접근 방식의 기반을 형성합니다.

25 kA를 초과하는 장치는 캐비닛당 15 kW를 초과하는 데이터센터의 랙 밀도 및 배터리 저장 장치를 통합한 재생 에너지용 변전소의 보급에 힘입어, 2031년까지 연평균 성장률(CAGR) 6.32%로 증가할 전망입니다. 배터리 시스템의 경우 연속 작동 정격 전압이 1,500 V DC까지 상승함에 따라, 서지 보호 설계에는 더 광범위한 MOV 스택 및 스파크 갭 소자가 추가되었습니다. 한편, 최대 10 kA의 서지 보호 장치는 가정용 전자기기 및 SOHO(소규모 사무실·홈 오피스) 기기를 보호합니다. 소비자들이 TV, 게임기, 스마트 가전 등을 통합된 엔터테인먼트 허브에 연결함에 따라, 합리적인 가격에 신뢰할 수 있는 보호 기능이 요구되면서 이 분야 수요는 꾸준히 확대되고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 39.60%를 차지했습니다. 그 중심에는 미국이 있으며, 미국의 ‘국가전기규정(NEC)’에 따르면 현재 모든 주거용 전력 설비에 대해 유형 1 또는 유형 2 보호 장치를 설치해야 합니다. 데이터센터 확장에 따라 대용량 서비스 입구용 SPD에 대한 수요가 증가하고 있습니다. 캐나다의 서지 보호 장치 시장 규모는 각 주에서 유사한 규격을 채택하고, 전력 회사가 가전제품 1대당 최대 5,000달러의 보상을 제공하는 ‘전체 주택 대상 프로그램’을 추진하고 있기 때문에 미국의 동향과 유사한 추이를 보이고 있습니다.

아시아태평양에서는 제조 투자가 인도와 동남아시아로 이동함에 따라, 2031년까지 연평균 성장률(CAGR) 5.98%라는 가장 높은 성장률을 나타낼 것으로 전망됩니다. 중국과 일본은 편의점이나 마이크로 데이터센터에 소형 DIN 레일형 SPD를 도입하는 등, 호황을 누리고 있는 플러그인형 상용 부문을 주도하고 있습니다. 또한, 정부의 재생에너지 도입 확대 계획은 전력 계통의 안정성과 관련된 문제를 더욱 심화시키고 있으며, 인버터 스테이션에서 25 kA 이상의 제품에 대한 수요를 촉진하고 있습니다. 지역 내 각 OEM 기업들은 다국적 브랜드와 제휴하여 생산의 현지화를 추진하고 있으며, 건설 주기의 단축에 따라 리드 타임을 단축하고 있습니다.

유럽은 엄격한 설비 기준과 전력망 토폴로지를 재구축하는 적극적인 탈탄소화 목표 덕분에 견고한 시장 점유율을 유지하고 있습니다. 독일의 ‘에너지 전환(Energiewende)’ 및 덴마크의 해상 풍력 발전소에서는 새로운 66 kV 송전 케이블이 도입되었으며, 전압 안정을 위해 각 케이블에 라인 서지 어레스터가 필요합니다. 기업의 지속가능성 목표에 따라 SF6를 사용하지 않는 친환경 서지 아레스터의 도입이 더욱 촉진되고 있습니다. 한편, 남미, 중동 및 아프리카는 도시 지역의 전기화 및 통신 인프라 현대화가 수요의 점진적인 증가를 가져오는 신흥 시장으로 부상하고 있습니다. 태양광 발전과 에너지 저장을 결합한 마이크로그리드를 구축하는 민관 파트너십에서는 자산의 가동 시간을 극대화하기 위해, 연계된 서지 대책 솔루션의 도입이 점점 더 요구되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the surge protection devices market size in 2026 is estimated at USD 3.01 billion, growing from 2025 value of USD 2.86 billion with 2031 projections showing USD 3.87 billion, growing at 5.18% CAGR over 2026-2031.

This report is Segmented by Installation Type (Hard-Wired, Plug-In, and Line Cord), Discharge-Current Rating (up To 10KA, 10KA-25KA, and Above 25KA), Voltage Class (Low-Voltage [Less Than 1 KV], Medium-Voltage [1-35 KV], and High-Voltage [More Than 35 KV]), End-User Vertical (Industrial, Commercial, and Residential), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Surge Protection Devices Market Trends and Insights

Rising adoption of smart-home and IoT devices

Smart-home ecosystems now often hold electronics worth more than USD 15,000, exposing households to material financial risk when surges occur. Microprocessors in connected lighting, appliances, and security systems are highly sensitive to voltage transients, and a surge harming one node can propagate through the network. Whole-house surge protection therefore is replacing point-of-use strips, and manufacturers are bundling power-line and data-line protection in a single enclosure to simplify installation. Insurance carriers reinforce this trend by lowering premiums for protected homes, boosting demand in the residential segment. Growing familiarity with home-automation platforms further widens the audience for feature-rich but easy-to-install plug-in SPDs that sync with mobile apps for status alerts.

Growing grid-instability from renewables integration

Wind and solar are projected to supply over 40% of global generation by 2030, yet inverter-based resources lack the high fault currents required by traditional protective relays. As utilities cycle generation to match variable output, switching-induced transients become more frequent, challenging legacy protection schemes. Digital relays and data-driven arc-flash controls are gaining favor, creating demand for surge devices that perform reliably across wider voltage envelopes and fluctuating waveforms. Innovation now centers on devices capable of handling both lightning-induced and switching-induced events, with thermal-disconnect technology protecting MOV elements from accelerated aging.

High retrofit installation cost in legacy facilities

Installing whole-building surge protection in plants built decades ago often necessitates panelboard upgrades, conduit rerouting, or even brief shutdowns. Material costs for a commercial-grade unit run USD 300-700, and professional labor adds USD 100-200 per board, but production downtime can dwarf hardware expense. Many facilities operate on tight margins and defer upgrades until mandated by code revisions or insurance renewals. Vendors are countering with bus-mounted retrofit kits and split-core current-sensing designs that shorten installation windows, yet the perceived payback period still slows adoption, especially in mature industrial economies with aging infrastructure.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of data-center and telecom power density

- EV-charging infrastructure mandates service-entrance SPDs

- Low end-user awareness of hidden SPD failure rates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The hard-wired category accounted for 45.40% of 2025 revenue as facility engineers prefer devices permanently integrated into switchboards and distribution panels. This configuration offers the lowest let-through voltage, making it a default choice for production lines, cleanrooms, and data halls where uptime is paramount. Smart variants now include field-replaceable modules and web-based dashboards that simplify maintenance schedules.

Plug-in SPDs trail in share but will register the fastest CAGR at 6.05% between 2026-2031 as the smart-home boom continues. Insurance premium incentives and app-enabled power-quality analytics coax homeowners to upgrade from basic strips to networked models. The line-cord niche secures critical servers and audiovisual gear, leveraging slim enclosures and integrated RJ45 ports for combined power-and-signal defense. As code bodies widen protection mandates, hybrid devices that merge hard-wired surge modules with downstream receptacle strips are appearing in commercial buildings seeking whole-system coordination.

Medium-capacity (10 kA-25 kA) products captured 51.30% of turnover in 2025 by balancing price and performance for office towers, retail chains, and light-industrial workshops. Manufacturers optimize component counts to keep footprints compact while meeting IEC 61643-11 Type 2 limits. This segment anchors coordinated-level approaches where service-entrance units handle high-energy events and downstream boards rely on 10 kA-25 kA modules for fine clamping.

Above-25 kA units will rise at a 6.32% CAGR through 2031, propelled by data-center rack densities that exceed 15 kW per cabinet and renewable-energy substations integrating battery storage. Continuous-operating-voltage ratings climb to 1,500 V DC in battery systems, so surge designs add wider MOV stacks and spark-gap elements. At the other end, up-to-10 kA strips protect home electronics and SOHO gear. Demand here expands steadily as consumers connect televisions, gaming consoles, and smart appliances into unified entertainment hubs that require affordable yet reliable protection.

Geography Analysis

North America contributed 39.60% of global revenue in 2025, anchored by the United States, where the National Electrical Code now mandates Type 1 or Type 2 protection for all dwelling services. Data-center expansion amplifies demand for high-capacity, service-entrance SPDs. The surge protection devices market size in Canada mirrors the U.S. trajectory as provinces adopt similar code language and utilities promote whole-home programs offering coverage up to USD 5,000 per appliance.

Asia-Pacific will post the fastest 5.98% CAGR to 2031 as manufacturing investment shifts toward India and Southeast Asia. China and Japan drive a thriving plug-in commercial segment, equipping convenience stores and micro-data centers with compact, DIN-rail SPDs. Government plans to lift renewable-energy penetration also accentuate grid-stability challenges, spurring demand for 25 kA-plus products at inverter stations. Regional OEMs partner with multinational brands to localize production, reducing lead times as construction cycles tighten.

Europe maintains a solid share thanks to tight equipment standards and aggressive decarbonization targets that remake grid topology. Germany's Energiewende and Denmark's offshore wind arrays entail new 66 kV export cables, each requiring line-surge arresters for voltage stabilization. Corporate sustainability goals further encourage the adoption of eco-friendly arresters that eschew SF6. Meanwhile, South America, the Middle East, and Africa represent emerging pockets where urban electrification and telecom modernization seed incremental volumes. Public-private partnerships building solar-plus-storage microgrids increasingly specify coordinated surge solutions to maximize asset uptime.

- ABB Ltd

- Eaton Corporation plc

- Emerson Electric Co.

- Schneider Electric SE

- Siemens AG

- Littelfuse Inc.

- Legrand SA

- Leviton Manufacturing Co. Inc.

- Hubbell Inc.

- Tripp Lite (Eaton brand)

- Belkin International Inc.

- General Electric Co.

- Phoenix Contact GmbH and Co. KG

- Citel Electronics Inc.

- OBO Bettermann Holding GmbH

- Mersen SA

- Raycap Corporation

- nVent Electric plc (ERICO)

- Hager Group

- Delta Electronics Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of smart-home and IoT devices

- 4.2.2 Growing grid-instability from renewables integration

- 4.2.3 Expansion of data-center and telecom power density

- 4.2.4 EV-charging infrastructure mandates service-entrance SPDs

- 4.2.5 Insurance-premium incentives for installing SPDs

- 4.3 Market Restraints

- 4.3.1 High retrofit installation cost in legacy facilities

- 4.3.2 Low end-user awareness of hidden SPD failure rates

- 4.3.3 Confusion over evolving SPD certification schemes

- 4.3.4 Geopolitical shortages of metal-oxide varistors

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Impact of COVID-19 and Long-COVID Effects

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Installation Type

- 5.1.1 Hard-Wired

- 5.1.2 Plug-In

- 5.1.3 Line Cord

- 5.2 By Discharge-Current Rating

- 5.2.1 Up to 10 kA

- 5.2.2 10 kA-25 kA

- 5.2.3 Above 25 kA

- 5.3 By Voltage Class

- 5.3.1 Low-Voltage (Less than 1 kV)

- 5.3.2 Medium-Voltage (1-35 kV)

- 5.3.3 High-Voltage (More than 35 kV)

- 5.4 By End-User Vertical

- 5.4.1 Industrial

- 5.4.2 Commercial

- 5.4.3 Residential

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Eaton Corporation plc

- 6.4.3 Emerson Electric Co.

- 6.4.4 Schneider Electric SE

- 6.4.5 Siemens AG

- 6.4.6 Littelfuse Inc.

- 6.4.7 Legrand SA

- 6.4.8 Leviton Manufacturing Co. Inc.

- 6.4.9 Hubbell Inc.

- 6.4.10 Tripp Lite (Eaton brand)

- 6.4.11 Belkin International Inc.

- 6.4.12 General Electric Co.

- 6.4.13 Phoenix Contact GmbH and Co. KG

- 6.4.14 Citel Electronics Inc.

- 6.4.15 OBO Bettermann Holding GmbH

- 6.4.16 Mersen SA

- 6.4.17 Raycap Corporation

- 6.4.18 nVent Electric plc (ERICO)

- 6.4.19 Hager Group

- 6.4.20 Delta Electronics Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis