|

시장보고서

상품코드

2066683

스페인의 실란트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Spain Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

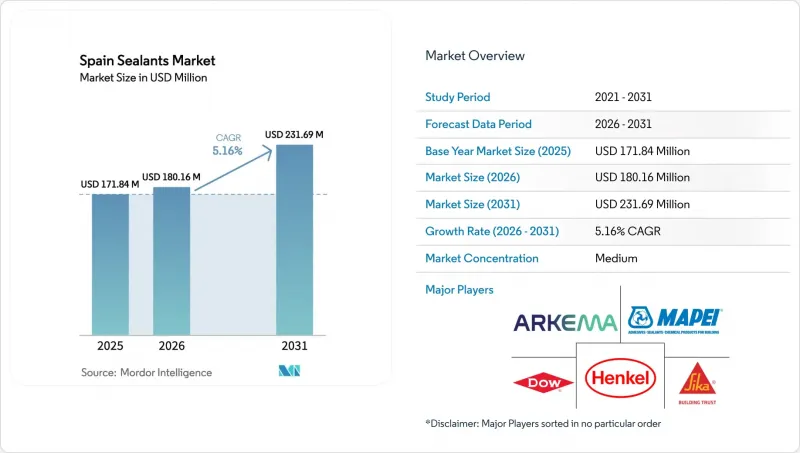

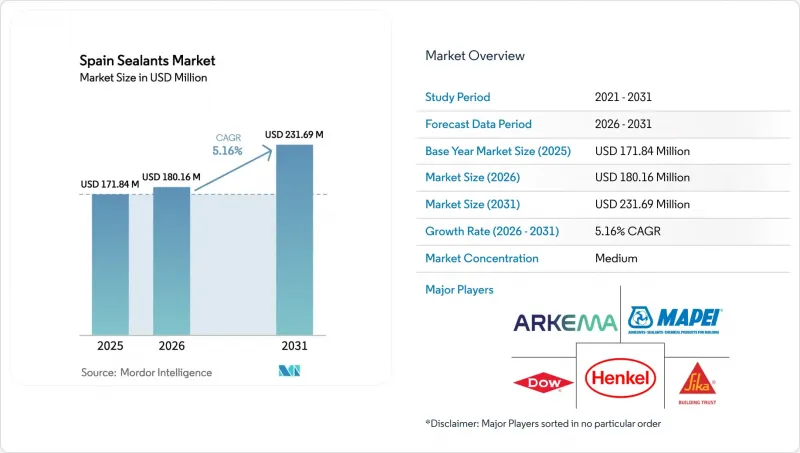

Mordor Intelligence에 의하면, 스페인의 실란트 시장 규모는 2025년에 1억 7,184만 달러로 평가되었습니다. 2026년에 1억 8,016만 달러에 달하고, 2031년까지 2억 3,169만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 5.16%로 성장할 전망입니다.

본 보고서는 수지 유형(아크릴, 에폭시, 폴리우레탄, 실리콘, 기타 수지) 및 최종 사용자 산업(항공우주, 자동차, 건축 및 건설, 의료, 기타 최종 사용자 산업)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러)으로 표시되어 있습니다.

스페인의 실란트 시장 동향 및 분석

스페인의 노후화된 주택 재고에서 리모델링 주도 수요 급증

스페인에서는 2025년에 185만 건의 주택 개보수가 완료되었으며, 대규모 개보수 허가 건수는 전년 대비 12.9% 증가했습니다. 주택의 약 80%가 에너지 효율 평가에서 낮은 수준을 기록하고 있어, 개보수 비용의 최대 100%를 지원하는 세제 혜택에 힘입어 창틀 주변, 신축 이음매, 기밀성 실링재에 대한 수요가 꾸준히 증가하고 있습니다. PNRE 2026에 따른 최소 에너지 성능 기준에 따르면, 2030년까지 비주거용 건축물이 2020년 시점의 기존 건축물 중 성능이 가장 낮은 16%를 상회하는 성능을 달성해야 하며, 이에 따라 예측 가능한 다년간의 수주 파이프라인이 형성되고 있습니다. 마드리드, 바르셀로나, 세비야에는 보조금 수혜자가 집중되어 있지만, 스페인 건설 업계에서는 70만 명의 인력 부족이 발생하고 있으며, 이로 인해 건설업체들은 조립식 외벽과 호환되는 공장 생산형 실란트 시스템으로 전환하고 있습니다. 그 결과로 인한 수요 증가에 힘입어, 스페인의 실란트 시장은 견조한 성장 궤도를 확고히 다지고 있습니다.

자동차 경량화 규제가 구조용 실란트의 사용을 촉진하고 있습니다.

유럽의 폐차 관련 규제로 인해, 자동차 제조업체들은 경량화를 위해 구조용 접착제에 의존하는 복합 소재 차체의 도입을 강요받고 있습니다. 스페인의 전기자동차 전환은 아라곤 주에 위치한 41억 유로 규모의 CATL-스텔란티스 합작 배터리 공장을 중심으로 진행되고 있으며, 이 공장은 2026년 말까지 연간 50GWh를 공급할 예정입니다. 이 프로젝트로 인해 UL 94 V-0 및 IEC 62368-1을 준수하는 난연성 폴리우레탄 및 실리콘계 화학제품에 대한 현지 수요가 증가하고 있습니다. 재활용을 가능하게 하기 위해 필요에 따라 박리할 수 있는 고신장성 실란트가 선호되는 솔루션으로 부상하고 있으며, 기술 선도 기업들은 스페인의 실란트 시장에서 높은 이익률을 확보할 수 있는 입지에 있습니다.

이소시아네이트 가격 변동이 폴리우레탄 실란트의 이익률을 압박하고 있습니다.

유럽의 에틸렌 가격은 톤당 평균 800달러로, 미국의 2배, 중동의 4배 수준이며, 지역 생산 능력의 최대 40%가 가동 중단 위험에 처해 있습니다. 스페인은 MDI(메틸렌디페닐디이소시아네이트)와 TDI(톨루엔디이소시아네이트)를 모두 수입하고 있기 때문에 분기마다 20-30%의 가격 변동이 발생하면 30일 결제 조건으로 사업을 영위하는 소규모 배합 제조업체의 이익률이 압박을 받게 됩니다. 국내에 크래커가 없기 때문에 원자재 가격 변동은 스페인의 실란트 시장에서 폴리우레탄 판매에 있어 계속해서 구조적인 걸림돌이 되고 있습니다.

부문별 분석

2025년, 실리콘계 실란트는 자외선 안정성과 곰팡이 방지 성능이 뛰어난 파사드 및 위생 설비 용도를 주력으로 하여, 스페인의 실란트 시장에서 38.15%의 점유율을 차지했습니다. Wacker사의 ‘ELASTOSIL eco 7770 P’는 바이오매스 유래 성분을 함유하고 있으며, EC1 플러스 인증을 획득하여 이 카테고리의 프리미엄 제품을 상징합니다. 폴리우레탄의 판매량은 현재로서는 소규모이지만, 아라곤 주의 신규 기가팩토리에서 생산되는 전기자동차 배터리 밀봉 및 풍력 발전용 블레이드 수리에 사용되는 고신장성 조인트에 대한 수요에 힘입어 연평균 성장률(CAGR) 6.96%로 증가할 것으로 전망됩니다. 시카사의 ‘Purform’ 시리즈는 이미 REACH 규정을 준수하며 낮은 모노머 함량을 실현하고 있으며, 이 회사는 이러한 성장의 흐름을 포착할 준비를 갖추고 있습니다.

에폭시계 제품은 항공우주 분야나 산업용 바닥재와 같은 틈새 시장에 국한되어 있는 반면, 아크릴계 제품은 가격 압박과 기계식 체결 부품에 의한 부분적인 대체에 직면해 있습니다. 하이브리드 시릴 변성 폴리머(SMP)나 보스틱사의 바이오카본 함유율 46% 배합 등, 새롭게 등장한 바이오 블렌드는 CPR 2024에 기반한 환경 등급을 중시하는 공공 프로젝트에서 새로운 기회를 열어가고 있습니다. 전반적으로, 범용 실리콘 및 아크릴계 제품은 스페인의 실란트 시장과 비슷한 수준이거나 그보다 낮은 추세를 보일 것으로 예상되지만, 특수 폴리우레탄 및 인증을 받은 하이브리드 시스템은 시장 동향을 상회하는 성장이 예상됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the spain sealants market size is projected to be USD 171.84 million in 2025, USD 180.16 million in 2026, and reach USD 231.69 million by 2031, growing at a CAGR of 5.16% from 2026 to 2031.

This report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, Silicone, and Other Resins) and End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, and Other End-User Industries). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Spain Sealants Market Trends and Insights

Renovation-Driven Demand Surge in Spain's Aged Housing Stock

Spain completed 1.85 million home renovations in 2025, and licenses for deep rehabilitation climbed 12.9% year on year. Roughly 80% of dwellings carry poor energy ratings, so fiscal incentives covering up to 100% of retrofit costs are channeling steady volumes toward window-perimeter, expansion-joint, and airtightness sealants. Minimum Energy Performance Standards under the PNRE 2026 require non-residential buildings to outperform the worst 16% of 2020 stock by 2030, creating a predictable multi-year order pipeline. Madrid, Barcelona, and Seville concentrate most subsidy beneficiaries, while a 700,000-worker shortfall in Spanish construction is steering contractors toward factory-applied sealant systems compatible with prefabricated facades. The resulting uplift cements a strong base trajectory for the Spain Sealants market.

Automotive Lightweighting Mandates Boosting Structural Sealant Usage

European End-of-Life Vehicle rules push automakers toward mixed-material bodies that depend on structural adhesives for weight savings. Spain's EV transition is centered on the EUR 4.1 billion CATL-Stellantis battery plant in Aragon, due to supply 50 GWh annually by end-2026. The project elevates local demand for flame-retardant polyurethane and silicone chemistries meeting UL 94 V-0 and IEC 62368-1. High-elongation sealants that debond on command to enable recycling are emerging as preferred solutions, positioning technology leaders to capture premium margins in the Spain Sealants market.

Volatile Isocyanate Prices Squeezing Polyurethane Sealant Margins

European ethylene costs average USD 800 per tons, double United States and quadruple Middle-East benchmarks, exposing up to 40% of regional capacity to closure risk. Spain imports all MDI (methylene diphenyl diisocyanate) and TDI (toluene diisocyanate), so 20-30% quarterly price swings erode margins for small formulators on 30-day terms. Absent domestic crackers, raw-material volatility remains a structural drag on polyurethane sales inside the Spain Sealants market.

Other drivers and restraints analyzed in the detailed report include:

- EU Fit-for-55 Energy-Efficiency Rules Raising Demand for Low-VOC Sealants

- Rapid Growth of On-Shore Wind-Blade Refurbishments

- Rising Substitution by Mechanical Fasteners in Low-Rise Construction

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone sealants held 38.15% of Spain Sealants market share in 2025, anchored by facade and sanitary applications that benefit from UV stability and mildew resistance. Wacker's ELASTOSIL eco 7770 P adds biomass-offset content and EC1 plus certification, illustrating the premium end of this category. Polyurethane volumes are smaller today yet forecast to climb at 6.96% CAGR, propelled by EV battery sealing at the new Aragon gigafactory and high-elongation joints in wind-blade repairs. Sika's Purform series, already REACH-compliant and low-monomer, positions the firm to capture this uplift.

Epoxy chemistries remain niche, serving aerospace and industrial flooring, while acrylics face price pressure and partial substitution from mechanical fasteners. Hybrid silyl-modified polymers (SMP) and emerging bio-based blends, such as Bostik's 46% bio-carbon formulation, are carving out opportunities in public projects that weigh environmental classes under CPR 2024. Overall, commodity silicones and acrylics will track or trail the Spain Sealants market, whereas specialty polyurethane and certified hybrid systems are primed for above-trend gains.

List of Companies Covered in this Report:

- 3M

- Adhesivas Centro

- Adhesivos del Segura

- Arkema

- Comercial Quimica Masso

- Dow

- Fischer Iberica

- Grupa Selena

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Industrias Quimicas del Adhesivo

- MAPEI S.p.A.

- Novasil SL

- Orbafoam

- QS Adhesives & Sealants SL

- RPM International Inc.

- Saint-Gobain Weber

- Sika AG

- Soudal Group

- Tremco Illbruck

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renovation-driven demand surge in Spain's aged housing stock

- 4.2.2 Automotive lightweighting mandates boosting structural sealant usage

- 4.2.3 EU "Fit-for-55" energy-efficiency rules raising demand for low-VOC sealants

- 4.2.4 Rapid growth of on-shore wind-blade refurbishments

- 4.2.5 Niche demand from Spanish EV gigafactories

- 4.2.6 Self-healing polymer RandD clusters in Catalonia attracting investors

- 4.3 Market Restraints

- 4.3.1 Volatile isocyanate prices squeezing polyurethane sealant margins

- 4.3.2 Rising substitution by mechanical fasteners in low-rise construction

- 4.3.3 Strict REACH restrictions on tin-catalyzed silicones

- 4.3.4 Limited domestic feedstock base

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Resins

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Adhesivas Centro

- 6.4.3 Adhesivos del Segura

- 6.4.4 Arkema

- 6.4.5 Comercial Quimica Masso

- 6.4.6 Dow

- 6.4.7 Fischer Iberica

- 6.4.8 Grupa Selena

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Industrias Quimicas del Adhesivo

- 6.4.12 MAPEI S.p.A.

- 6.4.13 Novasil SL

- 6.4.14 Orbafoam

- 6.4.15 QS Adhesives & Sealants SL

- 6.4.16 RPM International Inc.

- 6.4.17 Saint-Gobain Weber

- 6.4.18 Sika AG

- 6.4.19 Soudal Group

- 6.4.20 Tremco Illbruck

- 6.4.21 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment