|

시장보고서

상품코드

2066725

북미의 저전압 유도 전동기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Low Voltage Induction Motors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

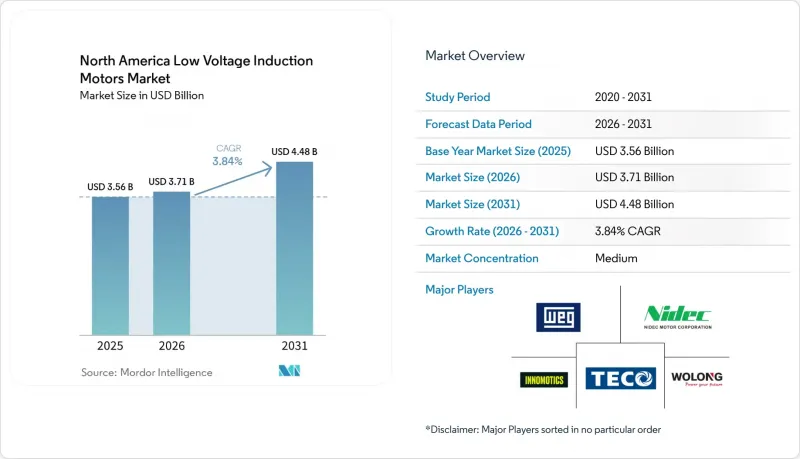

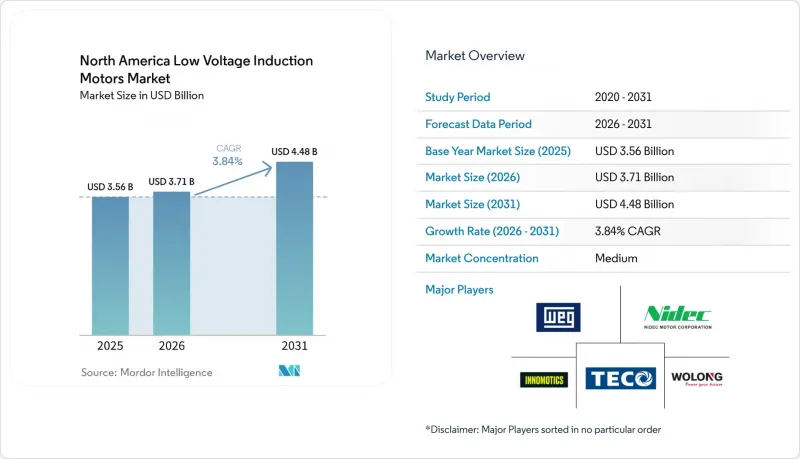

Mordor Intelligence에 의하면, 북미의 저전압 유도 전동기 시장 규모는 2025년 35억 6,000만 달러로 평가되었고, 2026년에는 37억 1,000만 달러로 추정되고, 2026-2031년 CAGR 3.84%로 성장을 지속할 전망이며, 2031년에는 44억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 모터의 유형별(단상 및 다상), 용도별(펌프 및 팬, 압축기, 컨베이어 및 자재관리, HVAC·냉동, 기타), 효율 등급별(IE1/표준 효율, 기타), 최종 사용자 산업별(석유 및 가스, 상하수도, 식품 및 음료, 기타), 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 저전압 유도 전동기 시장 동향 및 인사이트

적용 범위가 확대된 모터에 대한 미국 에너지부(DOE)의 효율 기준 강화

연방 정부의 효율 규제는 그 어떤 구조적 요인보다도 북미 저전압 유도 전동기 시장의 단기 전망에 더 큰 영향을 미치고 있습니다. 미국 에너지부(DOE)는 2025년 1월, 정격 출력 0.25-3마력의 단상 및 다상 유도 전동기를 대상으로 하는 ‘적용 범위 확대 전동기’에 관한 최종 규정을 공표했으며, 2029년 1월 1일까지 이를 준수해야 합니다. 한편, 100-250마력의 전동기에 대해서는 별도의 규제 절차가 마련되어 있으며, 2027년 6월의 준수 기한에 앞서 구매자들은 IE4 등급 설계로 전환해야 합니다. 이에 따라 각 산업 시설에서 계획 및 갱신 결정이 앞당겨지고 있습니다. 또한 DOE는 적용 범위가 확대된 기준에 따라 최종 사용자의 연간 운영 비용이 대폭 절감될 것으로 전망하고 있으며, 이에 따라 업그레이드를 미루기보다는 이미 설치된 구형 전동기를 조기에 교체하는 것이 경제적 이점이 더욱 커지고 있습니다. 실제로 북미의 저전압 유도 전동기 시장에서는 특히 조달 팀이 마감 기한을 앞두고 공급 병목 현상을 피하고자 할 때, 인증을 받은 고효율 모델, 규정 준수 시기, 그리고 공급업체의 준비 상태에 대한 관심이 높아지고 있습니다.

산업 자동화 및 브라운필드 개보수에 대한 지출

브라운필드의 현대화는 북미의 저전압 유도 전동기 시장을 뒷받침하고 있습니다. 이는 구형 플랜트의 경우, 주변 전기 시스템을 재설계하지 않고도 전동기나 드라이브를 교체할 수 있는 경우가 많기 때문입니다. 개조 프로젝트는 예측 유지보수 및 디지털 모니터링과 연계되는 경우가 늘어나고 있으며, 이를 통해 플랜트 팀은 에너지 손실을 측정하고, 보다 명확한 투자 회수 기간을 바탕으로 교체 필요성을 입증할 수 있게 되었습니다. ABB는 자사의 SP4 시리즈를 미국 에너지부(DOE) 기준에 부합하는 슈퍼 프리미엄 성능을 핵심으로 포지셔닝하고 있으며, 이는 신규 시설뿐만 아니라 업그레이드 주기에서도 해당 기준을 충족하는 모터가 점점 더 선호되는 추세와 부합합니다. 특히, 수명 주기 비용의 대부분을 전력 소비량이 차지하는 연속 운전형 펌프, 팬, 컨베이어의 용도에서는 업그레이드 수요가 매우 높습니다. 이에 따라 미국의 주요 생산 지역 전반에서 교체 수요가 활발히 이어지고 있으며, 그린필드 투자가 불안정한 상황 속에서도 북미 저전압 유도 전동기 시장이 꾸준한 성장을 유지하는 데 기여하고 있습니다.

구리 및 알루미늄 가격 변동

원자재 가격 변동은 북미 저전압 유도 전동기 시장에서 비용 측면에서 여전히 가장 뚜렷한 제약 요인으로 작용하고 있습니다. 구리나 알루미늄의 가격은 특히 프로젝트가 가격에 민감하고 자본 승인 기간이 짧은 경우, 제조업체의 이익률, 유통업체의 가격 책정, 그리고 최종 사용자의 교체 시기에 영향을 미칩니다. 이는 IE2에서 IE3 또는 IE4로 전환하는 과정에서 가장 중요한 문제가 됩니다. 왜냐하면 고효율 설계는 이미 초기 비용이 높기 때문에 원자재 가격이 불안정한 상황에서는 그 도입을 정당화하기 어려워지기 때문입니다. 그 결과, 구매자가 장기적인 에너지 절약 효과를 이해하고 있는 경우에도 저가형 제품과 프리미엄형 제품 간의 가격 차이가 확대되고 있습니다. 이에 따라 북미의 저전압 유도 전동기 시장은 성장을 이어가고 있지만, 일부 시설에서는 단순한 교체 구매에서 계획적인 고효율화로의 전환 속도가 둔화되고 있습니다.

부문별 분석

2025년, 북미 저전압 유도 전동기 시장에서 다상 전동기는 90.23%의 시장 점유율을 차지했으며, 지역별 매출 구성에서 단상 설계를 크게 앞질렀습니다. 이 위상은 3상 전력 시스템과의 높은 호환성, 뛰어난 토크 특성, 그리고 연속 운전 시 유지보수 요구 사항이 적다는 점을 반영하고 있습니다. 또한, 이 부문은 2031년까지 연평균 성장률(CAGR) 4.43%로 가장 높은 성장률을 나타낼 것으로 예상되며, 이러한 성장은 기존의 경쟁 우위뿐만 아니라 새로운 사양으로의 전환에 따른 모멘텀에 힘입은 것으로 나타났습니다. 식품 가공, 음료 제조 및 산업용 냉동 분야에서는 신뢰성과 안정적인 가동이 효율 향상만큼이나 중요하게 여겨지기 때문에 플랜트 담당 팀은 신규 라인에 다상 IE3 및 IE4 모터를 계속해서 표준 옵션으로 채택하고 있습니다. 이에 따라 북미의 저전압 유도 전동기 시장은 세분화된 소부하 이용 사례가 아닌, 산업용 듀티 사이클을 중심으로 계속해서 발전하고 있습니다.

5마력을 초과하는 다상 모터는 연속 운전이 요구되는 산업용 환경에서 실용적인 선택지가 되는 경우가 많으며, 이는 해당 범위 내에서 단상 전원을 사용할 경우 변환 손실 증가, 시스템 복잡성 증가 및 유지보수 지점 증가를 초래하기 때문입니다. 이러한 운영상의 현실이 펌프, 컨베이어, 압축기 및 플랜트의 유틸리티 시스템 전반에 걸친 안정적인 수요를 뒷받침하고 있습니다. 한편, 단상 모터는 3상 전원을 사용할 수 없거나 설치 비용이 지나치게 높은 경상용, 농업용 및 주거용 펌프 분야에서 여전히 널리 활용되고 있습니다. 또한, 미국 에너지부(DOE)가 2025년 1월에 공표한 ‘적용 범위 확대 모터’에 관한 최종 규정은 0.25-3마력 범위의 다양한 설계에 대한 성능 기준을 상향 조정함으로써, 저마력 단상 모터 분야에도 변화를 가져오고 있습니다. 그 결과, 판매 대수 측면에서는 다상 모터가 여전히 주도적인 위치를 유지하고 있는 반면, 단상 모터의 매출액은 판매 대수의 대폭적인 증가보다는 규제 준수를 목적으로 한 설계 업그레이드에 따라 좌우되는 경향이 강해지고 있습니다.

2025년, 북미 저전압 유도 전동기 시장 규모 중 펌프 및 팬이 35.78%를 차지했으며, 이 지역에서 가장 큰 용도 그룹을 형성하고 있습니다. 이러한 우위는 수처리, 석유 및 가스 처리, HVAC 냉각 루프, 냉각 시스템, 화학 플랜트 등 다양한 분야에 설치된 전동기의 수에서 비롯됩니다. 대부분의 시스템은 장기간의 가동 중단을 견디지 못하기 때문에 이러한 설치 기반은 설비 투자의 급격한 변화로부터 영향을 덜 받는 정기적인 교체 수요를 창출하고 있습니다. 또한, 시설에서 신뢰성 향상, 발열량 저감 및 인버터 구동 시 성능 강화가 요구되는 경우, 고효율 모델로 업그레이드해야 할 근거가 됩니다. 따라서 북미의 저전압 유도 전동기 시장은 다른 용도에서 주기적인 변동이 나타나더라도 펌프 및 팬 관련 서비스 분야에서 꾸준한 수요를 계속해서 확보하고 있습니다.

압축기는 콜드체인 시스템, 천연가스 처리, 그리고 AI 관련 데이터센터 건설에 따른 액체 냉각 시스템에서의 활용 확대에 힘입어, 2031년까지 연평균 성장률(CAGR) 4.25%라는 가장 높은 성장률을 보일 것으로 전망됩니다. 니덱이 2025년 11월에 TEFC 인버터 대응 클로즈드 커플링 펌프용 모터 제품 라인을 출시한 것도, 공급업체가 펌프 및 압축 용도와 유사한 가변 속도에서 전력 소비량이 많은 용도를 염두에 두고 설계를 진행하고 있음을 보여줍니다. 컨베이어 및 자재관리 분야는 공장 자동화 및 물류 산업의 성장에 따라 미국 및 멕시코 전역에서 모터를 많이 사용하는 이송 시스템이 계속 늘어나고 있기 때문에 여전히 중요한 분야입니다. 37 kW 미만의 HVAC 및 냉동 분야에서는 EC(에너지 효율형) 및 영구자석 기술을 활용한 대체가 진행되고 있지만, 유지보수 용이성이나 재권선의 경제성이 더욱 중요시되는 대형 프레임이나 가혹한 사용 조건의 시스템에서는 유도 전동기가 여전히 확고한 입지를 유지하고 있습니다. 일반 산업용 기계나 소규모 용도의 ‘롱테일’ 시장은 구매자가 공급망이나 가격 면에서 압박을 받기 쉬운 상황에 처해 있더라도 계속해서 폭넓은 수요를 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the north america low voltage induction motors market size is expected to grow from USD 3.56 billion in 2025 to USD 3.71 billion in 2026 and is forecast to reach USD 4.48 billion by 2031 at 3.84% CAGR over 2026-2031.

This report is Segmented by Motor Type (Single Phase, and Poly Phase), Application (Pumps and Fans, Compressors, Conveyors and Material Handling, HVAC and Refrigeration, and More), Efficiency Class (IE1/Standard Efficiency, and More), End-User Industry (Oil and Gas, Water and Wastewater, Food and Beverage, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America Low Voltage Induction Motors Market Trends and Insights

Tightening DOE Efficiency Standards for Expanded-Scope Motors

Federal efficiency regulation is shaping the near-term outlook of the North America low voltage induction motors market more than any other structural driver. The U.S. Department of Energy published a final rule in January 2025 for expanded-scope electric motors that covers single-phase and poly phase induction motors rated 0.25 to 3 horsepower, with compliance required by January 1, 2029. A separate rule path for 100-250 horsepower motors is pushing buyers toward IE4-class designs ahead of the June 2027 compliance date, which is pulling forward planning and replacement decisions across industrial sites. DOE also said the expanded-scope standards would generate material annual operating cost savings for end users, which strengthens the financial case for replacing older installed motors instead of delaying upgrades. The practical effect is that the North America low voltage induction motors market is seeing more attention on certified premium-efficiency models, compliance timing, and supplier readiness, especially where procurement teams do not want to face bottlenecks closer to the deadline.

Industrial Automation and Brownfield Retrofit Spending

Brownfield modernization is supporting the North America low voltage induction motors market because older plants can often replace motors and drives without redesigning the surrounding electrical system. Retrofit projects are increasingly tied to predictive maintenance and digital monitoring, which helps plant teams measure energy losses and justify changeouts on a clearer payback basis. ABB has positioned its SP4 line around DOE-ready super-premium performance, and that aligns with the growing preference for compliant motors in upgrade cycles rather than only in new facilities. The upgrade case is especially strong in continuous-duty pump, fan, and conveyor services where electricity use dominates lifecycle cost. This is keeping replacement activity active across manufacturing corridors in the United States and helping the North America low voltage induction motors market hold steady growth even when greenfield spending is uneven.

Copper and Aluminum Cost Volatility

Raw material volatility remains the clearest cost-side restraint for the North America low voltage induction motors market. Copper and aluminum costs affect manufacturer margins, distributor pricing, and end-user replacement timing, especially when projects are price-sensitive and capital approval windows are narrow. This matters most in the move from IE2 to IE3 or IE4, because higher-efficiency designs already carry a higher upfront cost and become harder to justify when input prices are unstable. The result is a wider price gap between lower-tier and premium-tier products, even when buyers understand the energy savings case over time. That keeps the North America low voltage induction motors market growing, but it slows the speed at which some facilities move from basic replacement buying to planned premium-efficiency upgrades.

Other drivers and restraints analyzed in the detailed report include:

- Water and Wastewater Infrastructure Upgrades

- Mexico Nearshoring and Plant Localization

- Higher First-Cost Barrier for Premium-Efficiency Retrofits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Poly phase motors held 90.23% of the North America low voltage induction motors market share in 2025, which kept them far ahead of single phase designs in the regional revenue mix. Their position reflects strong compatibility with three-phase power systems, better torque characteristics, and lower maintenance demands in continuous-duty operations. The segment is also forecast to post the fastest 4.43% CAGR through 2031, which shows that growth is not only coming from base dominance but also from new specification momentum. In food processing, beverage production, and industrial refrigeration, plant teams continue to make poly phase IE3 and IE4 motors the default choice for new lines because reliability and stable operation matter as much as efficiency gains. This keeps the North America low voltage induction motors market centered on industrial duty cycles rather than on fragmented small-load use cases.

Poly phase units above 5 horsepower are often the practical choice in continuous-duty industrial settings because single phase supply in that range adds conversion losses, more complexity, and extra maintenance points. That operating reality supports steady demand across pumps, conveyors, compressors, and plant utility systems. Single phase motors still serve light commercial, agricultural, and residential pump applications where three-phase power is unavailable or too costly to install. DOE's January 2025 final rule for expanded-scope motors is also reshaping the lower-horsepower single phase segment by raising the performance threshold for many designs in the 0.25-3 horsepower range. The result is that volume leadership remains with poly phase motors, while single phase revenue is being influenced more by compliance-driven design upgrades than by broad unit growth.

Pumps and fans accounted for 35.78% of the North America low voltage induction motors market size in 2025, making them the largest application group in the region. Their lead comes from the depth of installed motors across water treatment, oil and gas processing, HVAC chiller loops, cooling systems, and chemical plants. This installed base creates repeat replacement demand that is less exposed to abrupt changes in capital spending because many systems cannot tolerate long outages. It also supports the case for premium-efficiency upgrades when facilities need better reliability, lower heat generation, and stronger inverter-duty performance. The North America low voltage induction motors market, therefore, continues to draw stable demand from pump and fan services even when other applications move in cycles.

Compressors are projected to grow at the fastest 4.25% CAGR through 2031, supported by rising use in cold-chain systems, natural gas handling, and liquid cooling systems tied to AI-linked data center buildouts. Nidec's November 2025 launch of its TEFC Inverter Duty Closed Coupled Pump motor line also shows how suppliers are designing around variable-speed, utility-heavy applications that sit close to both pumping and compression duties. Conveyors and material handling remain important because factory automation and distribution growth continue to add motor-intensive movement systems across the United States and Mexico. HVAC and refrigeration below 37 kW face some substitution from EC and permanent-magnet technologies, but induction motors remain well placed in larger-frame and harsher-duty systems where serviceability and rewind economics matter more. General industrial machinery and the long tail of smaller applications continue to provide a broad demand floor, even if those buyers are more exposed to supply chain and pricing pressure.

List of Companies Covered in this Report:

- WEG S.A.

- Nidec Motor Corporation

- Innomotics GmbH

- TECO Electric & Machinery Co., Ltd.

- Wolong Electric Group Co., Ltd.

- Regal Rexnord Corporation

- Brook Crompton UK Ltd.

- VEM GmbH

- Hoyer Motors A/S

- Lafert S.p.A.

- Cantoni Motor S.A.

- CG Power and Industrial Solutions Limited

- ABB Ltd.

- Bharat Bijlee Limited

- Bonfiglioli Riduttori S.p.A.

- SEW-EURODRIVE GmbH & Co KG

- Getriebebau NORD GmbH & Co. KG

- Neri Motori S.r.l.

- OME Motors S.r.l.

- T-T Electric Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening DOE Efficiency Standards for Expanded-Scope Motors

- 4.2.2 Industrial Automation and Brownfield Retrofit Spending

- 4.2.3 Water and Wastewater Infrastructure Upgrades

- 4.2.4 Mexico Nearshoring and Plant Localization

- 4.2.5 AI Data Center Cooling Loop Expansion

- 4.2.6 Semiconductor and Battery Utility System Build-Out

- 4.3 Market Restraints

- 4.3.1 Copper and Aluminum Cost Volatility

- 4.3.2 Higher First-Cost Barrier for Premium-Efficiency Retrofits

- 4.3.3 EC and Permanent-Magnet Motor Substitution in HVAC

- 4.3.4 Tariff-Driven Component Sourcing Instability

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Motor Type

- 5.1.1 Single Phase

- 5.1.2 Poly Phase

- 5.2 By Application

- 5.2.1 Pumps and Fans

- 5.2.2 Compressors

- 5.2.3 Conveyors and Material Handling

- 5.2.4 HVAC and Refrigeration

- 5.2.5 General Industrial Machinery

- 5.2.6 Other Applications

- 5.3 By Efficiency Class

- 5.3.1 IE1/Standard Efficiency

- 5.3.2 IE2/High Efficiency

- 5.3.3 IE3/Premium Efficiency

- 5.3.4 IE4/Super-Premium Efficiency

- 5.4 By End-User Industry

- 5.4.1 Oil and Gas

- 5.4.2 Water and Wastewater

- 5.4.3 Chemicals and Petrochemicals

- 5.4.4 Food and Beverage

- 5.4.5 Discrete Manufacturing

- 5.4.6 Metal and Mining

- 5.4.7 Other End-User Industries

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 WEG S.A.

- 6.4.2 Nidec Motor Corporation

- 6.4.3 Innomotics GmbH

- 6.4.4 TECO Electric & Machinery Co., Ltd.

- 6.4.5 Wolong Electric Group Co., Ltd.

- 6.4.6 Regal Rexnord Corporation

- 6.4.7 Brook Crompton UK Ltd.

- 6.4.8 VEM GmbH

- 6.4.9 Hoyer Motors A/S

- 6.4.10 Lafert S.p.A.

- 6.4.11 Cantoni Motor S.A.

- 6.4.12 CG Power and Industrial Solutions Limited

- 6.4.13 ABB Ltd.

- 6.4.14 Bharat Bijlee Limited

- 6.4.15 Bonfiglioli Riduttori S.p.A.

- 6.4.16 SEW-EURODRIVE GmbH & Co KG

- 6.4.17 Getriebebau NORD GmbH & Co. KG

- 6.4.18 Neri Motori S.r.l.

- 6.4.19 OME Motors S.r.l.

- 6.4.20 T-T Electric Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment