|

시장보고서

상품코드

2066731

원자 시계 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Atomic Clock - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

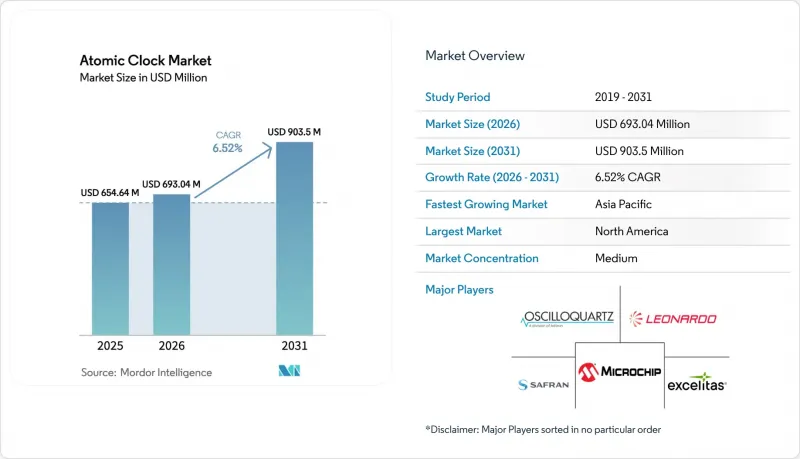

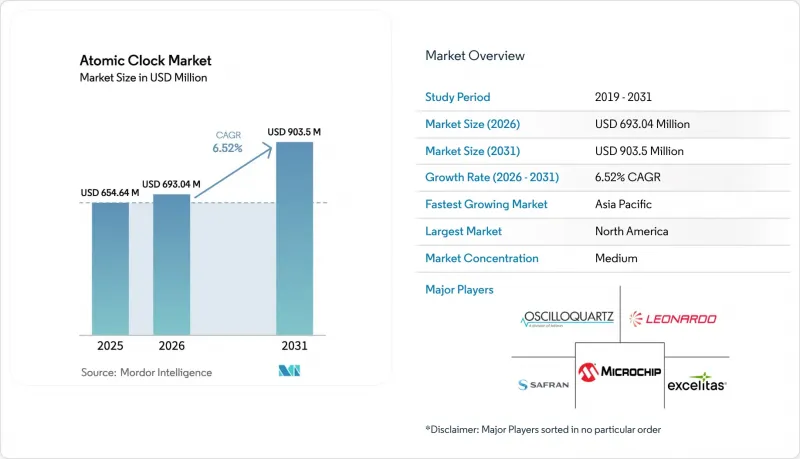

Mordor Intelligence에 의하면, 원자 시계 시장 규모는 2025년 6억 5,464만 달러로 평가되었습니다. 2026년에는 6억 9,304만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 5.44%로 성장을 지속하여, 2031년에는 9억 350만 달러에 이를 것으로 예측됩니다.

본 보고서는 유형별(루비듐, 세슘, 수소 메저), 최종 사용자별(국방, 우주, 민생·상업), 용도별(항법, 감시, 전자전, 통신, 금융 거래·데이터센터, 방송·미디어 등), 지역별(북미, 유럽, 아시아태평양 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 원자 시계 시장 동향 및 인사이트

위성항법시스템(GNSS) 위성군 확대

GNSS 위성군 확장과 다중 주파수 수신기 설계로 인해 우주 탑재형 시계에 대한 장기 안정성 및 내방사선성 기준이 높아지고 있으며, 이에 따라 중궤도 및 고궤도에서 루비듐 및 수소 메저 탑재 장치에 대한 수요가 지속적으로 증가하고 있습니다. 록히드 마틴사는 2026년 초, 10호기인 GPS III 위성을 통해 디지털 원자 시계의 비행 시험을 실시할 계획이며, 이를 통해 일일 안정성을 현재 루비듐 시계의 기준치 이상으로 높여, GPS 현대화를 위한 궤도상 시간 관리 성능의 다음 단계를 보여줄 것입니다. 유럽에서는 2025년 12월에 갈릴레오 위성 2기가 발사됨에 따라 서비스의 지속성이 강화되었습니다. 또한, 프로그램 설명회에 따르면, 갈릴레오 2세대에서는 견고성과 정밀도를 향상시키기 위해 디지털 페이로드, 위성 간 링크 및 실험적인 시계 기술이 추가될 것으로 확인되었습니다. 중국은 2024년 9월, 차세대 시간·주파수 성능을 검증하고 더 깊은 우주로의 커버리지 확대를 목표로 하는 ‘북두 4’ 로드맵을 지원하기 위해, 개량형 수소 원자 시계를 탑재한 제59호 및 제60호 북두 위성을 발사했습니다. 이러한 각국의 투자는 원자 시계 시장이 앞으로도 위성 플랫폼의 업데이트 주기와 사용자 기기에서 다중 위성군(multi-constellation)의 광범위한 채택으로 인한 혜택을 계속 누릴 것이라는 분명한 신호를 보내고 있습니다.

5G/6G 네트워크의 위상 동기화 요구 사항

5G Advanced 및 초기 6G 로드맵에 포함된 새로운 무선 기능들은 위치 파악, 센싱 및 상호작용 서비스를 위해 서브나노초 수준의 네트워크 동기화와 서브밀리초 수준의 종단 간 지연으로 수렴하고 있으며, 이에 따라 루비듐 기준 시계 및 에지 환경에서의 고정밀 시간 전송에 대한 투자가 촉진되고 있습니다. 6G에 관한 벤더들의 비전 성명서에서는 상호작용형 지도와 분산형 지능을 구현하기 위해서는 물리 계층에서 고정밀 시간 정보가 필요하다고 강조하고 있습니다. 이러한 요건으로 인해 통신 사업자들은 GNSS 장애 발생 시 홀드오버 기능을 강화하고, 내장애성을 향상시켜야 할 필요에 직면해 있습니다. 이러한 기술적 변화에 따라 통신 사업자들이 기지국을 업그레이드하고, 엣지 컴퓨팅 노드를 구축하며, 데이터센터로의 시간 전송을 확대함에 따라, 원자 시계 시장은 통신 현대화 주기와 밀접하게 연계된 상태를 유지하고 있습니다. 공공 기관 역시 중요 인프라를 위한 대체적이고 보완적인 PNT(위치·항법·시간) 접근 방식을 정리하고 있으며, 이를 통해 신호 손실 시 드리프트를 허용할 수 없는 네트워크에서 여러 공급업체를 대상으로 고정밀 타이밍 기술 평가가 이루어지고, 해당 기술의 조달이 촉진되고 있습니다. 위상 코히런트 무선, 엣지 추론 및 시간 민감형 네트워킹이 확대됨에 따라, 원자 시계 시장에는 방위 분야 주요 기업을 넘어 더 폭넓은 기업들의 진출이 예상됩니다.

높은 단가와 설비 투자의 집중도

틈새 시장용 조립, 장기간의 번인 테스트, 그리고 광범위한 인증이 필요한 임무 전용 원자 시계의 경우, 가격 책정이 여전히 제약 요인으로 작용하고 있어, 이로 인해 대량 생산되는 통신용 타이밍 장치에 비해 비용 곡선이 높은 수준을 유지하고 있습니다. 광격자 시계는 현재 상용화의 초기 단계에 있으며, 시범 생산품의 가격은 50만 달러를 초과하고 있습니다. 반면, 네트워크 동기화에 사용되는 루비듐 원자 시계는 5,000달러 미만으로 구입할 수 있습니다. 칩 스케일 원자 시계는 저전력으로 작동하면서도 휴대성을 향상시키고 있지만, 장기적인 안정성과 드리프트 간의 상충 관계로 인해 비용과 통합의 복잡성을 증가시키는 하이브리드 아키텍처가 필요한 경우가 적지 않습니다. 프로그램 공개 정보에서는 성능 향상이 강조되어 있을 뿐, 명확한 단가가 제시되어 있지 않아 신규 진출기업이나 소규모 시스템 통합사업자의 경우 경쟁사 벤치마킹이 어렵습니다. 프리퀀시 일렉트로닉스사가 최근 항공기용 타이밍 분야에서 수상한 실적은 수요의 강세를 뒷받침하고 있지만, 공개 문서에 포함된 단가 데이터는 여전히 비공개로 남아 있습니다. 이러한 경제적 요인으로 인해 구매자들은 성능, SWaP(크기·무게·전력 소비량) 및 수명 주기 지원의 균형을 고려하여, 선택적 도입이나 단계적 확대를 추진하는 경향을 보이고 있습니다.

부문별 분석

세슘 원자 시계는 2025년 기준 40.50%의 시장 점유율을 차지했으며, 계량학 및 국방 분야의 교정, 그리고 네트워크 마스터 클럭으로서의 역할에 힘입어 2031년까지 연평균 성장률(CAGR) 5.90%로 성장할 것으로 전망됩니다. 세슘 원자시의 위상은 국가 기준의 업그레이드를 통해 더욱 공고해지고 있습니다. 그 예로, 2025년 4월에 10^16분의 2.2라는 정확도를 달성한 NIST-F4를 들 수 있으며, 이는 UTC(NIST)의 운영을 주도하고 중요 인프라의 타이밍 제어를 지원하기 위한 데이터를 제공합니다. 또한, 각 벤더사는 세슘 플랫폼의 단기 정확도 향상에도 힘쓰고 있으며, 그 예로 Oscilloquartz사가 광학식 세슘 시계에 적용한 개량을 들 수 있습니다. 이는 서브나노초 수준의 홀드오버와 1초에 걸친 펨토초 수준의 안정성을 실현하는 것을 목표로 한 것입니다. 고가용성 네트워크에서는 세슘이 장기적인 기준으로 계속 기능하는 한편, 시간 전송 및 네트워크 아키텍처가 중복성을 담당함으로써, 원자 시계 시장은 단일 표준이 아닌 하이브리드 시계군을 중심으로 한 구성을 유지하고 있습니다. 이 부문의 전망은 안정적입니다. 왜냐하면, 시기적 일관성이 법적 및 운영상의 영향을 미치는 분야에서 세슘은 규정 준수 및 서비스 수준 의무의 기반이 되기 때문입니다.

루비듐 및 칩 스케일 원자 시계(CSAC)가 나머지 시장을 차지하고 있으며, 휴대성, 전력 효율, 그리고 합리적인 비용으로 수년에 걸쳐 안정성을 보장하는 점을 중시하는 우주 및 방위 임무에 적합합니다. 마이크로칩의 2세대 저잡음 CSAC는 현장 사용을 위해 전력 및 온도 내성을 향상시켰으며, GNSS 장애 발생 시에도 홀드오버 기능을 통해 운영을 지속해야 하는 무인 시스템이나 도보 통신의 선택지를 넓혀주고 있습니다. 우주 프로그램에서는 SWaP(크기·무게·전력 소비)와 장기적인 드리프트 및 노화 현상에 따른 타협점을 고려하여, 루비듐 및 수소 메저 시계를 보완적인 탑재체로 계속해서 사용하고 있습니다. 한편, 지상에서는 운영자가 비용과 성능을 관리하기 위해 세슘, 루비듐 및 네트워크 기반 시간 전송 방식을 조합하여 사용하고 있습니다. 중국의 연구 기관 역시 우주 탑재형 수소 시계의 질량과 전력 소비를 줄이는 것을 목표로 하고 있으며, 기존의 23kg 설계에서 차세대 위성에 적합한 새로운 15kg 구성으로 전환하고 있습니다. 이러한 동향을 통해, 세슘은 여전히 주요 기준으로 자리 잡고 있는 반면, 루비듐과 CSAC는 SWaP 제약이 있는 역할로 그 영역을 확대하며, 플랫폼과 임무 프로파일을 초월한 균형 잡힌 원자 시계 시장을 뒷받침하고 있습니다.

지역별 분석

북미는 2025년에 31.91%의 점유율을 확보했습니다. 이는 국방, 우주, 중요 인프라 분야의 현대화 프로그램이 정밀 계시의 대규모 도입 기반을 뒷받침했기 때문입니다. NIST의 활동과 NASA 관련 프로그램을 비롯해 국가 표준의 업그레이드 및 우주 시계 실험을 통해, 계측학 및 심우주 항법 분야에서 해당 지역의 리더십이 강화되고 있습니다. 항공기 및 위성용 타이밍 장치와 관련된 계약 활동도 계속되고 있으며, 각 OEM 업체들은 정부 고객을 대상으로 한 안정적인 PNT(위치·항법·시간) 및 고정밀 동기화 요건과 관련된 추가 수주를 발표하고 있습니다. 이러한 투자를 통해 원자 시계 시장 수요 기반이 유지되는 한편, 사업자들에 의한 네트워크 동기화 및 시간 전송의 적용 범위도 확대되고 있습니다.

아시아태평양은 중국이 궤도상에서 차세대 수소 시계의 검증을 수행하고, 2035년까지 심우주를 커버하는 것을 목표로 북두 4호 계획을 확대하고 있는 만큼, 2026년부터 2031년에 걸쳐 연평균 성장률(CAGR) 5.87%라는 가장 빠른 성장 궤도를 그리고 있습니다. 인도 및 지역 파트너국들은 자국의 PNT(위치·항법·시간) 전략을 지속적으로 강화하고 있으며, 항공우주 및 통신 분야 전반에 걸쳐 시간 동기화 기능이 강화된 인프라에 대한 투자를 이어가고 있습니다. 호주는 2024년, AUKUS의 ‘제2의 기둥’에 따라 국방용 양자 광학 시계 개발에 자금을 지원하며, 2025년까지 납품을 계획했습니다. 이는 동맹국들의 프로그램이 타이밍 기술의 기반을 다각화하고 있음을 보여주는 것입니다. 각국의 프로그램이 국내 개발과 선택적 수입을 병행하는 가운데, 아시아태평양의 원자 시계 시장은 정책 주도형 현지화와 상용 플랫폼 확대라는 두 가지 측면에서 모두 혜택을 보고 있습니다.

유럽에서는 갈릴레오 프로젝트의 전개와 우주 기반 시간 전송 및 계량학 분야의 실험 확대가 착실히 진행되고 있습니다. 2025년 12월, 위성 군집의 내결함성을 강화하기 위해 아리안 6호 로켓을 통해 갈릴레오 위성 2기가 발사되었습니다. 또한, 유럽우주국(ESA)의 브리핑에 따르면, 갈릴레오 2세대에는 더욱 정교한 탑재체와 실험적인 시계 유형이 추가될 것으로 확인되었습니다. 국제우주정거장(ISS)에서 진행 중인 ESA의 ACES 임무는 고정밀 시간 전송을 추진하며, 세계 최고 수준의 지상 시계들과 연동하고 있어, 이를 통해 유럽의 계량학이 새로운 과학적·상업적 활용 사례를 모색할 수 있게 되었습니다. 영국은 2025년에도 양자 기술을 활용한 PNT(위치·항법·시간) 연구에 대한 자금 지원을 계속했으며, 이는 향후 인프라 구축을 위한 광학 시계 및 시간 전송 솔루션의 개발 파이프라인을 뒷받침했습니다. 이러한 활동 덕분에 우주, 통신, 과학 등 다양한 분야에 걸친 유럽의 원자 시계 시장은 계속해서 밝은 전망을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the atomic clock market size is expected to grow from USD 654.64 million in 2025 to USD 693.04 million in 2026 and is forecasted to reach USD 903.50 million by 2031 at a 5.44% CAGR over 2026-2031.

This report is Segmented by Type (Rubidium, Cesium, and Hydrogen Maser), End User (Defense, Space, and Civil and Commercial), Application (Navigation, Surveillance, Electronic Warfare, Telecommunication, Financial Trading and Data Centers, Broadcast and Media, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Atomic Clock Market Trends and Insights

Satellite Navigation Constellation Expansion

Expanding GNSS constellations and multi-frequency receiver design raise the bar on long-term stability and radiation tolerance for space-borne clocks, which sustains premium demand for rubidium and hydrogen-maser payloads across medium and high orbits. Lockheed Martin plans to flight test a digital atomic clock on the tenth GPS III satellite in early 2026 to push daily stability beyond the baseline for current rubidium clocks, signaling a next step in on-orbit timekeeping performance for GPS modernization. Europe strengthened service continuity when two Galileo spacecraft launched in December 2025, and program briefings confirm that Galileo Second Generation will add digital payloads, inter-satellite links, and experimental clock technologies to improve robustness and precision. China launched the 59th and 60th BeiDou satellites in September 2024 with upgraded hydrogen atomic clocks to validate next-generation time-frequency performance and support a BeiDou-4 roadmap toward deeper space coverage. These national investments send a clear signal that the atomic clock market will continue to benefit from satellite platform refresh cycles and broader multi-constellation adoption across user equipment.

5G/6G Network Phase-Synchronization Requirements

New radio features in 5G Advanced and early 6G roadmaps are converging on sub-nanosecond network synchronization and sub-millisecond end-to-end latency for positioning, sensing, and interactive services, directing spending toward rubidium references and high-grade time transfer at the edge. Vendor vision statements for 6G highlight the need for precise time at the physical layer to enable interactive maps and distributed intelligence. This requirement pushes operators to harden holdover and improve resilience during GNSS disruptions. This technical shift keeps the atomic clock market closely tied to telecom modernization cycles as operators upgrade base stations, deploy edge compute nodes, and extend time distribution into data centers. Public agencies also catalogue alternative and complementary PNT approaches for critical infrastructure, which sustains multi-vendor evaluation and uplifts procurement for precision timing in networks that cannot tolerate drift during signal loss. As phase-coherent radio, edge inference, and time-sensitive networking scale, the atomic clock market sees broader enterprise participation beyond defense primes.

High Unit Costs and Capital Expenditure Intensity

Pricing remains a limiting factor for mission-specific atomic clocks that require niche assemblies, long burn-in, and extensive qualification, which keeps the cost curve elevated relative to volume telecom timing. Optical lattice clocks are currently in the early stages of commercialization, with pilot production units priced at over USD 500,000. In contrast, rubidium atomic clocks used for network synchronization are available for less than USD 5,000. Chip-scale atomic clocks improve portability while operating on low power budgets, though long-term stability and drift trade-offs often require hybrid architectures that add cost and integration complexity. Program disclosures highlight performance improvements without transparent unit pricing, making competitive benchmarking difficult for new entrants and smaller integrators. Frequency Electronics' recent awards in airborne timing underscore the strength of demand, yet per-unit cost data remains proprietary in public filings. These economics encourage selective deployments and staged rollouts as buyers balance performance, SWaP, and lifecycle support.

Other drivers and restraints analyzed in the detailed report include:

- Defense Modernization Programs and Ultra-Precise Timing

- Quantum-Sensing Integration and Increased R&D Funding

- Strict Export-Control Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cesium atomic clocks held a 40.50% share in 2025 and are projected to grow at a 5.90% CAGR through 2031, supported by their role as the primary frequency reference in metrology, defense calibration, and network master-clock duties. Cesium's standing is reinforced by national-reference upgrades, including NIST-F4, which reached 2.2 parts in 10^16 accuracy in April 2025 and contributes data to steer UTC(NIST) and support critical infrastructure timing. Vendors also advance short-term precision on cesium platforms, as shown by Oscilloquartz's enhancements to optical cesium clocks that target sub-nanosecond holdover and femtosecond stability over 1 second. In high-availability networks, cesium remains the long-term anchor, while time transfer and network architecture handle redundancy, keeping the atomic clock market oriented around hybrid clock ensembles rather than a single standard. The segment's outlook is stable because cesium underpins regulatory compliance and service-level obligations in sectors where timing integrity carries legal and operational consequences.

Rubidium and chip-scale atomic clocks make up the balance and align with space and defense missions that prize portability, power efficiency, and multi-year stability at moderate cost. Microchip's second-generation low-noise CSAC improves power and temperature resilience for field use, broadening options for unmanned systems and dismounted communications that require holdover to survive GNSS outages. Space programs continue to use rubidium and hydrogen maser clocks as complementary payloads that trade SWaP against long-term drift and aging. At the same time, on the ground, operators mix cesium, rubidium, and network-based time transfer to manage cost and performance. Chinese research institutes also target mass and power reductions in space-borne hydrogen clocks, moving from legacy 23 kg designs to new 15 kg configurations to fit next-generation satellites. Across these paths, cesium remains the primary anchor, while rubidium and CSACs expand into SWaP-constrained roles, supporting a balanced atomic clock market across platforms and mission profiles.

Geography Analysis

North America secured a 31.91% share in 2025 as modernization programs in defense, space, and critical infrastructure anchored a large installed base of precision timing. National reference upgrades and space-clock experiments, including NIST efforts and NASA-linked programs, reinforce the region's leadership in metrology and deep-space navigation. Contract activity for airborne and satellite timing also continued, with OEMs announcing follow-on awards tied to assured PNT and high-precision synchronization requirements for government customers. These investments maintain demand depth in the atomic clock market while operators broaden network synchronization and time-transfer footprints.

Asia-Pacific charts the fastest trajectory, with a 5.87% CAGR from 2026 to 2031, as China validates next-generation hydrogen clocks in orbit and scales up plans for BeiDou-4 to achieve deep-space coverage by 2035. India and regional partners continue to strengthen sovereign PNT agendas and invest in timing-enhanced infrastructure across the aerospace and telecommunications sectors. Australia funded quantum-optical clock efforts for defense under AUKUS Pillar II in 2024, with deliveries planned through 2025, a signal that allied programs are diversifying their timing technology base. As national programs mix domestic development with selective imports, the atomic clock market in Asia-Pacific benefits from both policy-driven localization and commercial platform scaling.

Europe maintains steady progress with Galileo deployments and expanded experimentation in space-based time transfer and metrology. Two Galileo satellites were launched in December 2025 on an Ariane 6 to bolster constellation resilience, and ESA briefings confirm that Galileo Second Generation will add more advanced payloads and experimental clock types. ESA's ACES mission on the ISS advances precise time transfer and links world-leading ground clocks, which helps European metrology engage with new scientific and commercial use cases. The UK continued to fund quantum-enabled PNT research in 2025, which supports a pipeline of optical-clock and time-transfer solutions for future infrastructure deployments. These activities sustain a healthy outlook for the atomic clock market in Europe across space, telecoms, and scientific domains.

- AccuBeat Ltd.

- Excelitas Technologies Corp.

- IQD Frequency Products Limited

- Leonardo S.p.A.

- Microchip Technology Incorporated

- Oscilloquartz SA (Adtran Networks SE)

- Stanford Research Systems

- VREMYA-CH JSC

- Safran SA

- MacQsimal (CSEM) (accelopment Schweiz AG)

- Thermo Fisher Scientific Inc.

- Frequency Electronics, Inc.

- Abracon LLC

- AOSense, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Satellite navigation constellation expansion

- 4.2.2 5G/6G network phase-synchronization requirements

- 4.2.3 Defense modernization programs and ultra-precise timing

- 4.2.4 Emergence of chip-scale atomic clocks for IoT edge devices

- 4.2.5 Quantum-sensing integration and increased R&D funding

- 4.2.6 Growth of secure communications and electronic warfare systems

- 4.3 Market Restraints

- 4.3.1 High unit costs and capital expenditure intensity

- 4.3.2 Strict export-control regulations

- 4.3.3 Supply bottlenecks of enriched isotopes

- 4.3.4 Complexities in specialized infrastructure and external disruptions

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Rubidium (Rb) Atomic Clock

- 5.1.2 Cesium (Cs) Atomic Clock

- 5.1.3 Hydrogen (H) Maser Atomic Clock

- 5.2 By End User

- 5.2.1 Defense

- 5.2.1.1 Combat Aircraft and Helicopters

- 5.2.1.2 Unmanned Vehicles

- 5.2.1.3 Armoured Vehicles

- 5.2.1.4 Portable Systems

- 5.2.1.5 Naval Ships (Destroyers, Frigates)

- 5.2.1.6 Submarines

- 5.2.1.7 Patrol Vessels

- 5.2.2 Space

- 5.2.3 Civil and Commercial

- 5.2.1 Defense

- 5.3 By Application

- 5.3.1 Surveillance

- 5.3.2 Navigation

- 5.3.3 Electronic Warfare

- 5.3.4 Telemetry

- 5.3.5 Telecommunication

- 5.3.6 Financial Trading and Data Centers

- 5.3.7 Broadcast and Media

- 5.3.8 Industrial and Scientific Instrumentation

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 United Arab Emirates

- 5.4.5.1.2 Saudi Arabia

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 AccuBeat Ltd.

- 6.4.2 Excelitas Technologies Corp.

- 6.4.3 IQD Frequency Products Limited

- 6.4.4 Leonardo S.p.A.

- 6.4.5 Microchip Technology Incorporated

- 6.4.6 Oscilloquartz SA (Adtran Networks SE)

- 6.4.7 Stanford Research Systems

- 6.4.8 VREMYA-CH JSC

- 6.4.9 Safran SA

- 6.4.10 MacQsimal (CSEM) (accelopment Schweiz AG)

- 6.4.11 Thermo Fisher Scientific Inc.

- 6.4.12 Frequency Electronics, Inc.

- 6.4.13 Abracon LLC

- 6.4.14 AOSense, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment