|

시장보고서

상품코드

2066737

미국의 의약품 창고 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Pharmaceutical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

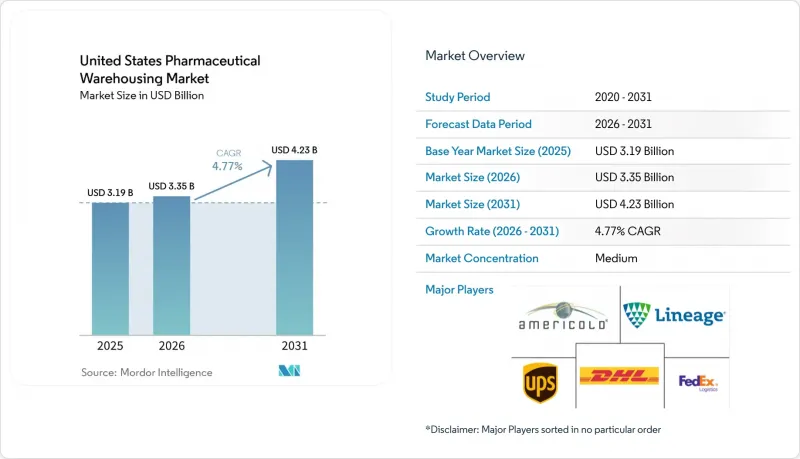

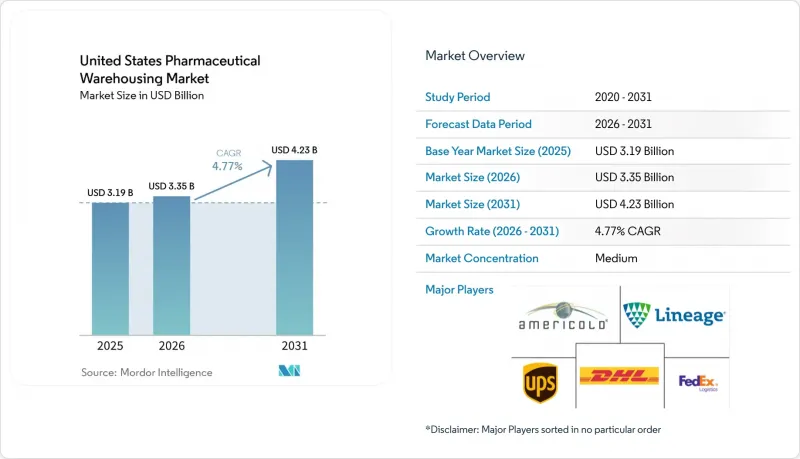

Mordor Intelligence에 의하면, 미국의 의약품 창고 시장 규모는 2025년 31억 9,000만 달러로 평가되었고, 2026년 33억 5,000만 달러로 추정되고, 2031년까지 42억 3,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 4.77%를 나타낼 전망입니다.

본 보고서는 서비스 유형별(보관, 유통·재고 관리 등), 창고 유형별(콜드체인 창고(냉장, 냉동 등), 비콜드체인 창고), 제품 유형별(처방약, 일반의약품 등) 및 최종 사용자별(제약사, 의료 제공업체 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 의약품 창고 시장 동향 및 인사이트

의료 분야에 특화된 3PL로의 아웃소싱이 급증하고 있습니다.

제조업체들이 보관 인프라를 직접 보유하기보다는 혁신과 제품 개발에 자원을 집중함에 따라, 창고 업계에서는 아웃소싱 및 계약 기반 모델로의 뚜렷한 전환이 나타나고 있습니다. 이러한 전환은 대형 물류 통합업체, 특히 헬스케어 물류 분야에서 사업을 확장하고 있는 기업들에 의해 가속화되고 있습니다. 이 기업들은 콜드체인 전문 기업을 인수하여 통합된 종단간 공급망 솔루션을 구축하고 있습니다. 이러한 통합을 통해 엄격한 규정 준수 요건을 충족하면서, 온도 관리가 필요한 의약품 및 바이오의약품을 보다 효과적으로 관리할 수 있게 됩니다. 시설 검증 및 제품 추적성 등 규제 요건이 강화됨에 따라 규정 준수 비용이 상승하여, 소규모 틈새 시장 창고 사업자에게는 유지하기 어려운 수준에 이르렀습니다. 이로 인해 자본력이 탄탄한 대형 물류 업체로의 전환이 더욱 가속화되고 있습니다.

국내 백신·항체 생산 능력 확대가 물류 센터 수요를 견인

미국의 제약 기업들은 생산 인프라를 대폭 확대하고 있으며, 특히 바이오의약품 제조 분야에서는 현재 물류 및 창고 수요의 주요 원동력이 되고 있습니다. 첨단 바이오 제조의 부상으로 인해, 생산 및 유통 사이클 전반에 걸쳐 온도에 민감한 자재를 관리할 수 있는 전문적인 콜드체인 시설에 대한 수요가 증가하고 있습니다. mRNA 및 기타 생물학적 제제를 보관하기 위해서는 초저온 보관 시스템이 필수적입니다. 이는 더 큰 에너지 용량이 필요할 뿐만 아니라, 이러한 저장 서비스에 상대적으로 높은 요금이 책정되어 있어 높은 수익을 창출합니다. 그 결과, 콜드체인 창고는 해당 부문의 자본 전략에서 핵심적인 요소가 되었으며, 바이오 제조의 성장과 물류 투자가 직접적으로 연결되어 있습니다.

배상책임보험 및 제품 리콜 보험의 보험료 급등

특히 세포 및 유전자 치료제의 유통 분야에서 인수 회사가 위험 증가에 대응함에 따라 의약품 물류를 둘러싼 보험 환경은 점점 더 어려워지고 있습니다. 제품 단가의 상승과 복잡한 취급 요건으로 인해 리콜 보험료가 대폭 치솟고 있어, 물류 사업자들은 품질 관리와 추적성 대책을 강화해야 하는 상황에 직면해 있습니다. 동시에, 시리얼화 및 추적성에 관한 규제의 시행으로 인해 기존 창고 시스템의 취약점이 드러나고 있습니다. 상호 운용이 가능한 실시간 추적 기능을 갖추지 못한 시설에는 고액의 보험료 할증금이 부과되고 있으며, 이는 의약품 공급망 전반에 걸친 신속한 디지털화 추진의 강력한 동기가 되고 있습니다.

부문별 분석

2025년, 보관 서비스는 미국 의약품 창고 시장의 66.38% 점유율을 유지했으나, 일련번호 부여, 키트 구성, 임상시험용 포장으로 인해 평방피트당 수익이 40-60% 증가함에 따라 부가가치 서비스 시장은 연평균 성장률(CAGR) 5.74%로 확대되고 있습니다. 이러한 프리미엄 서비스는 소규모 시설에서는 대응할 수 없는 검증된 IT 및 품질 관리 인프라에 의존하고 있으며, 업계의 통합 추세를 가속화하고 있습니다. 클라우드 대시보드와 원활한 ERP 통합을 통해 실시간 재고 가시성을 제공하는 창고에서는 고객의 90%가 이를 도입하고 있으며, 장기적이고 견고한 계약 관계를 구축하고 있습니다. 또한, 업계의 엄격한 재일련번호 부여 요건을 고려할 때, DSCSA와 관련된 반품 처리도 지속 가능한 수익원으로 부상하고 있습니다.

미국의 의약품 창고는 부가가치가 더 높은 서비스로 진화하고 있으며, 환자 맞춤형 포장 및 규제 컨설팅이 중요한 차별화 요소로 자리 잡고 있습니다. 온도 매핑, 검증, 감사 대응 지원을 제공하는 업체들은 지속적인 수익원을 구축하는 동시에, 규정 준수 및 유통 분야의 탁월성을 추구하는 파트너로서의 역할을 강화하고 있습니다.

2025년, 미국 의약품 창고 시장 규모의 75.06%를 비콜드체인 시설이 차지했으며, 평방피트당 약 9달러라는 낮은 운영비의 혜택을 누리고 있습니다. 한편, 콜드체인 시장은 2℃에서 -196℃까지의 온도 관리가 필요한 바이오의약품, 백신 및 맞춤형 치료제에 힘입어 2031년까지 연평균 성장률(CAGR) 5.91%를 나타낼 것으로 전망됩니다. 초저온 및 극저온 구역은 상온 구역에 비해 수 배 더 높은 이익률을 가져오지만, 창고 전체 전력 소비량의 79%를 차지하고 있습니다. 따라서 에너지 효율 향상을 위한 개보수 및 자동 반출 시스템은 수익성과 지속가능성에 관한 규제 준수에 있어 매우 중요합니다.

통합형 운영사는 자산 회전율을 극대화하기 위해 동일한 부지 내에서 상온 구역과 콜드체인 구역을 통합하고 있으며, IoT를 활용한 예측 유지보수를 통해 예기치 못한 가동 중단 시간을 60% 줄이고 있습니다. 미국 의약품 창고 시장에서 초저온 보관의 점유율은 여전히 낮은 편이지만, 팔레트당 50-75달러의 수수료를 고려하면 이익에서 차지하는 비중은 불균형할 정도로 큽니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the united states pharmaceutical warehousing market size is projected to expand from USD 3.19 billion in 2025 and USD 3.35 billion in 2026 to USD 4.23 billion by 2031, registering a CAGR of 4.77% between 2026 and 2031.

This report is Segmented by Service Type (Storage, Distribution and Inventory Management, and More), by Warehouse Type (Cold-Chain Warehouse [Chilled, Frozen, and More], Non-Cold-Chain Warehouse), by Product Type (Prescription, OTC Drugs, and More), and by End User (Pharmaceutical Manufacturers, Healthcare Providers, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Pharmaceutical Warehousing Market Trends and Insights

Outsourcing Surge to Healthcare-Focused 3PLs

The warehousing landscape is witnessing a clear shift toward outsourced and contract-based models as manufacturers focus their resources on innovation and product development instead of owning storage infrastructure. This transition is being accelerated by major logistics integrators, particularly those expanding in healthcare logistics, who are acquiring cold-chain specialists to build integrated, end-to-end supply solutions. Such consolidation allows them to manage temperature-sensitive pharmaceuticals and biologics more effectively while meeting stringent compliance requirements. Increasing regulatory demands, such as those related to facility validation and product traceability, have raised the cost of compliance to levels that smaller, niche warehouse operators often find difficult to sustain, further reinforcing the move toward large, well-capitalized logistics providers.

Ramp-up of Domestic Vaccine & Antibody Capacity Fueling DC Demand

Pharmaceutical companies in the United States are significantly expanding their production infrastructure, particularly in biologics manufacturing, which is now a key driver of logistics and warehousing demand. The rise of advanced biomanufacturing has intensified the need for specialized cold-chain facilities capable of managing temperature-sensitive materials throughout the production and distribution cycle. Ultra-low-temperature storage systems are essential for supporting mRNA and other biologic formulations, not only requiring higher energy capacity but also generating strong returns due to the premium pricing of such storage services. As a result, cold-chain warehousing has become a central component of the sector's capital strategy, linking biomanufacturing growth directly with logistics investment.

Escalating Liability & Product-Recall Insurance Premiums

The insurance environment for pharmaceutical logistics is tightening as underwriters respond to rising exposure risks, particularly in cell and gene therapy distribution. High product values and complex handling requirements have made recall insurance significantly more expensive, pushing logistics operators to strengthen quality and traceability measures. At the same time, enforcement of serialization and traceability regulations is exposing weaknesses in legacy warehouse systems. Facilities lacking interoperable, real-time tracking capabilities are facing steep premium surcharges, creating strong incentives for rapid digital modernization across the pharmaceutical supply chain.

Other drivers and restraints analyzed in the detailed report include:

- Automation & Robotics Deployments Improving GMP Accuracy

- Expansion of Specialty-Pharmacy Distribution Networks

- Construction-Material Shortages Delaying Warehouse Build-outs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Storage retained 66.38% of the United States Pharmaceutical Warehousing market share in 2025, but value-added services are expanding at a 5.74% CAGR as serialization, kitting, and clinical-trial packaging deliver 40-60% higher revenue per ft2. These premium services rely on validated IT and quality-management infrastructures that smaller facilities cannot match, reinforcing consolidation trends. Warehouses offering real-time inventory visibility through cloud dashboards and seamless ERP integrations report 90% client adoption, cementing sticky long-term contracts. Returns processing tied to DSCSA has also emerged as a sustainable profit pool, given the industry's strict re-serialization requirements.

The United States pharmaceutical warehousing is evolving toward higher-value services, with custom patient packaging and regulatory consulting becoming key differentiators. Providers offering temperature mapping, validation, and audit-readiness support are building recurring revenue streams while reinforcing their role as partners in compliance and distribution excellence.

Non-cold-chain sites accounted for 75.06% of the United States Pharmaceutical Warehousing market size in 2025, benefiting from lower operating expenses of roughly USD 9/ft2. Cold-chain, however, is set to post a 5.91% CAGR through 2031, pulled by biologics, vaccines, and personalized therapies that require temperatures from 2 °C down to -196 °C. Ultra-low and cryogenic zones yield margins several times higher than ambient space but consume 79% of total warehouse electricity. Energy-efficiency retrofits and automated retrieval systems are therefore critical for profitability and sustainability compliance.

Integrated operators blend ambient and cold-chain zones inside the same campus to maximize asset turns, while IoT-enabled predictive maintenance slashes unplanned downtime by 60%. The United States Pharmaceutical Warehousing market share in ultra-low storage remains small but represents a disproportionate share of profits given per-pallet fees of USD 50-75.

List of Companies Covered in this Report:

- United Parcel Service Inc.

- DHL Group

- FedEx Corp.

- GEODIS SA

- CEVA Logistics

- Lineage Logistics

- Americold Logistics

- Cencora

- BioPharma Logistics

- Rhenus SE & Co. KG

- Kuehne + Nagel

- XPO Logistics

- KRC Logistics

- GXO Logistics

- MD Logistics

- Langham Logistics

- Crown LSP Group

- LifeScience Logistics

- Go Freight

- DSV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Outsourcing Surge to Healthcare-Focused 3PLs

- 4.2.2 Ramp-Up of Domestic Vaccine & Antibody Capacity Fueling DC Demand

- 4.2.3 Automation & Robotics Deployments Improving GMP Accuracy

- 4.2.4 Expansion of Specialty-Pharmacy Distribution Networks

- 4.2.5 ESG-Driven Retrofits for Low-Carbon, Energy-Efficient Cold Stores

- 4.2.6 Drone/EV Last-Mile Pilots Requiring Forward-Staged Micro Cold Sites

- 4.3 Market Restraints

- 4.3.1 Escalating Liability & Product-Recall Insurance Premiums

- 4.3.2 Construction-Material Shortages Delaying Warehouse Buildouts

- 4.3.3 Patchwork of New State Data-Privacy Laws Limiting IoT Analytics

- 4.3.4 Extreme-Weather Volatility Raising HVAC Redundancy CAPEX

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape (FDA, DSCSA, DEA, OSHA)

- 4.6 Technological Outlook (WMS, IoT, Automation, Robotics)

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geopolitics and Pandemic on Warehousing

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Storage

- 5.1.2 Distribution and Inventory Management

- 5.1.3 Value-added Services and Others

- 5.2 By Warehouse Type

- 5.2.1 Cold-Chain Warehouse

- 5.2.1.1 Chilled (0-5°C)

- 5.2.1.2 Frozen (-18-0°C)

- 5.2.1.3 Ambient

- 5.2.1.4 Deep-Frozen / Ultra-Low (less than-20 °C)

- 5.2.2 Non-Cold-Chain Warehouse

- 5.2.1 Cold-Chain Warehouse

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics and Biosimilars

- 5.3.4 Vaccines and Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell and Gene Therapies

- 5.3.7 Specialty Medicine (non-biologic)

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

- 5.4 By End User

- 5.4.1 Pharmaceutical Manufacturers

- 5.4.2 Healthcare Providers

- 5.4.3 Retail and Pharmacies

- 5.4.4 Distributors and Wholesalers

- 5.4.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves and Investments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 United Parcel Service Inc.

- 6.4.2 DHL Group

- 6.4.3 FedEx Corp.

- 6.4.4 GEODIS SA

- 6.4.5 CEVA Logistics

- 6.4.6 Lineage Logistics

- 6.4.7 Americold Logistics

- 6.4.8 Cencora

- 6.4.9 BioPharma Logistics

- 6.4.10 Rhenus SE & Co. KG

- 6.4.11 Kuehne + Nagel

- 6.4.12 XPO Logistics

- 6.4.13 KRC Logistics

- 6.4.14 GXO Logistics

- 6.4.15 MD Logistics

- 6.4.16 Langham Logistics

- 6.4.17 Crown LSP Group

- 6.4.18 LifeScience Logistics

- 6.4.19 Go Freight

- 6.4.20 DSV

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment