|

시장보고서

상품코드

2066739

프랑스의 전기 버스 배터리 팩 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)France Electric Bus Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

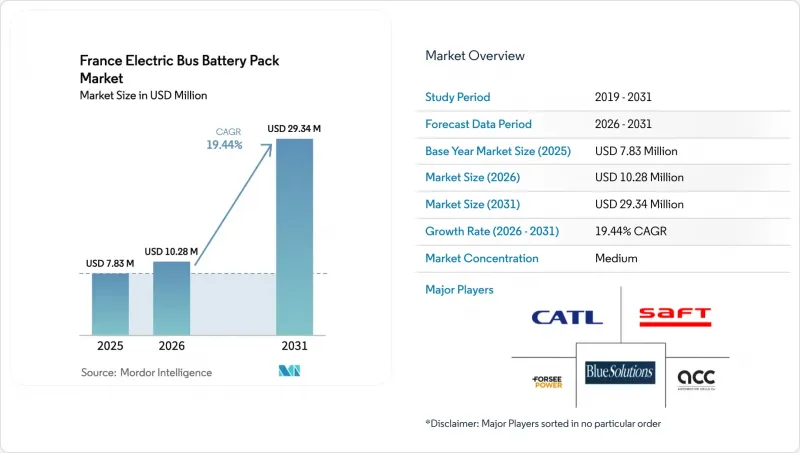

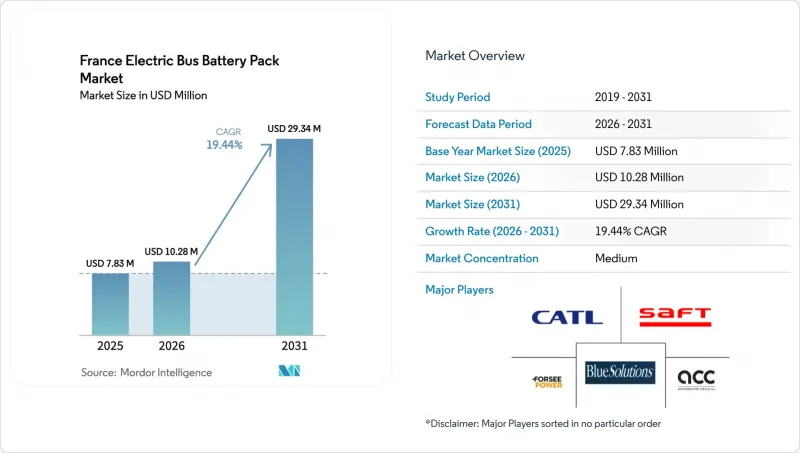

Mordor Intelligence에 의하면, 프랑스의 전기 버스 배터리 팩 시장 규모는 2025년에 783만 달러로 평가되었고, 2026년 1,028만 달러로 추정되고, 2031년까지 2,934만 달러로 확대될 전망이며, 2026-2031년 CAGR 19.44%를 나타낼 것으로 예측되고 있습니다.

본 보고서는 차량 유형별(미니버스/마이크로버스 등), 구동 방식별(배터리 전기차 등), 배터리 화학 조성별(인산철 리튬 등), 용량별(15 KWh 미만 등), 배터리 형태별(원통형 등), 전압 등급별(400V 미만 등), 모듈 구성별, 구성 부품별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(대) 단위로 제시되어 있습니다.

프랑스의 전기 버스 배터리 팩 시장 동향 및 분석

도시 지역의 저배출 구역 내 전기화 의무화

12개 ZFE-m 가맹 도시에서는 제로 에미션 버스로의 완전한 전환이 의무화되어 있어, 잔여 사용 연한이 남아 있는 경우에도 디젤 버스의 퇴역이 가속화되고 있습니다. 현재 다수의 전기 버스를 운행하고 있는 RATP는 목표를 달성하기 위해 연간 납품 대수를 대폭 늘려야 하는 과제에 직면해 있습니다. 주요 사업자들은 이베코사와 체결한 다수의 버스 관련 다년 계약에서 볼 수 있듯이, 장기 계약을 통해 입지를 공고히 하고 있습니다. 반면, 소규모 도시에서는 리스 계약을 선택하여 배터리 소유권을 포시 파워(Forsy Power)와 같은 공급업체에 양도하고 있습니다. 게다가, 새로운 포장 설계 승인을 받는 데 상당한 시간이 소요되는 유엔 R100 Rev 3 승인 절차의 장기화는 시장에 새로 진입하려는 기업들에게 큰 장벽이 되고 있습니다.

LMFP(리튬 망간 인산염) 및 LFP(리튬 철 인산염) 화학 계열 배터리의 1kWh당 비용 절감

시간이 지남에 따라 리튬철인산염(LFP) 배터리의 비용은 현저히 낮아져, 다양한 용도에서 비용 대비 효율이 높은 선택지가 되고 있습니다. 한편, 에너지 밀도 향상이 특징인 리튬-망간-철 인산염(LMFP) 배터리도 점점 더 저렴한 가격으로 출시되고 있습니다. 이러한 효율 향상과 에너지 저장 능력의 증대로 인해, 교외나 도시 간 장거리 노선을 운행하는 버스 사업자에게 특히 매력적인 선택지가 되고 있습니다. 또한, LMFP 배터리 채택 확대는 운송 부문에서 지속 가능하고 효율적인 에너지 솔루션에 대한 수요 증가와 부합합니다.

2025년 이후 니켈 및 코발트 가격의 변동

수출 규제 가능성에 대한 추측이 난무하는 가운데, 니켈 가격이 급등하면서 NMC 배터리의 원가 구조에 큰 변화를 가져왔습니다. 이러한 가격 변동에 따라, 교통 기관들은 보다 안정적인 원가 구조를 갖추고 니켈 의존도가 낮은 LMFP 배터리로 전환하는 내용을 조달 방침에 반영하기 시작했습니다. LMFP 배터리는 비용 효율성이 뛰어나고 안전성이 향상됨에 따라 실현 가능한 해결책으로서 점점 더 주목받고 있습니다. 한편, 자원과 헤지 능력이 제한적이어서 원자재 가격 변동에 효과적으로 대응하지 못하는 중소 배터리 통합업체들은 대규모의 수직 통합형 경쟁사들에 비해 점점 더 불리한 입장에 놓이고 있습니다. 이러한 대기업들은 규모의 경제와 공급망에 대한 보다 강력한 관리 능력의 혜택을 누리고 있어, 원자재 가격 변동에 따른 영향을 완화할 수 있습니다. 이러한 지속적인 변화는 현지 경쟁력을 약화시킬 뿐만 아니라, 프랑스 전기 버스용 배터리 시장에서 단기적인 비용 증가를 초래하고 있어, 밸류체인 전반의 이해관계자들에게 과제를 안겨주며, 해당 지역의 전기 버스 보급률에 영향을 미칠 가능성이 있습니다.

부문별 분석

2025년에는 표준 12미터 버스가 도입된 배터리 팩의 48.82%를 차지했습니다. 이는 기존 차고의 구조 및 운행 일정과의 호환성을 반영한 것입니다. 100-150 kWh 용량의 배터리는 주행 거리와 차량 총중량의 제한 사이에서 균형을 잘 맞추고 있어, 도심 버스 사업자에게 신속한 투자 회수를 실현해 줍니다. 파리와 툴루즈의 버스 운영사들은 저상 설계로 인한 접근성과 밀집된 도심 지역에서의 기동성을 이유로 이러한 사양을 선호하고 있습니다. 18미터 길이의 연결형 버스는 비용은 비싸지만, 피크 시간대의 수송 능력이 인프라 비용에 대한 우려를 상회하는 BRT 노선에서 도입이 확대되고 있습니다. 연절 버스 부문의 연평균 성장률(CAGR) 23.69%는 일드프랑스 모빌리티의 ‘Tzen 4’와 같은 프로젝트에 기인합니다. 이 프로젝트에서는 차고 내 체류 시간을 최소화하기 위해, 800V로 충전 가능한 220kWh 용량의 LMFP 배터리 팩을 탑재한 30대의 더블 연결 버스가 도입되었습니다. 미디버스(8-10.5m)는 역사 지구에서 일정한 입지를 유지하고 있지만, 차체 하부 공간이 제한적이어서 배터리 팩 용량이 80-100kWh로 제한되고 있으며, 더 큰 규모의 버스에 비해 보급 속도가 둔화되고 있습니다. 미니버스 및 마이크로버스 부문은 주행 거리가 짧은 셔틀 순환 노선을 위한 틈새 시장에 그치고 있으며, 주문형 밴이 새로운 보행자 전용 구역 수요를 충족시킬 수 있는 경우가 많기 때문에 프랑스의 전기 버스 배터리 팩 시장에서는 거의 성장이 보이지 않습니다.

이러한 용량 격차는 배터리 화학 시스템의 선택에도 영향을 미치고 있습니다. 표준 버스에서는 180 Wh/kg의 고밀도 LFP 셀이 점점 더 많이 채택되고 있는 반면, 연결형 버스에서는 주행 거리 연장을 위해 LMFP나 NMC가 선호되고 있습니다. Heuliez Bus 등 각 OEM 업체들은 루프 장착형 배터리 팩을 탑재할 수 있도록 섀시 레이아웃을 개조하고 있습니다. BRT 노선이 보르도와 니스 등으로 확대됨에 따라, 굴절버스의 장기적인 성장이 예상되며, 이는 고에너지 밀도 배터리 화학 시스템과 급속 충전 인프라에 대한 수요를 촉진하고 있습니다.

2025년 출하 대수에서 배터리 전기차(BEV)가 차지하는 비중은 83.16%에 달했으며, 플러그인 하이브리드차(PHEV)에 대한 정책 지원이 축소됨에 따라 이 비중은 더욱 높아질 것으로 보입니다. 2025년 4월에 통과된 국가 기후 법안에 따르면, 2027년 이후 도시 지역에서 신규 발주되는 버스는 100% 무공해 차량으로 도입해야 하며, 이에 따라 주요 조달 사업에서 하이브리드 구동 시스템이 사실상 배제될 것입니다. 업계 관계자들은 BEV(배터리 전기차) 차량군의 수명 주기 유지 비용이 18% 낮다고 지적하며, 이러한 비용 절감 요인으로 회생 제동 및 보다 단순한 구동계 구조를 꼽고 있습니다. 플러그인 하이브리드 차량은 극심한 기온 변동으로 인해 전압 저하가 발생하여 순수 전기 주행 거리가 단축될 우려가 있는 고산 지대나 해안 노선에서 여전히 제한적인 역할을 수행하고 있습니다.

하이브리드 차량의 퇴출은 배터리 사후 장착 개조 계약의 기회를 창출하고 있습니다. 이 계약에 따라, 시스템 통합사업자는 노후화된 디젤-전기 하이브리드 모듈을 모듈식 100 kWh LFP 팩으로 교체합니다. 이러한 개조를 통해 섀시의 수명이 8-10년 연장되며, 보조금 수급 자격도 얻을 수 있습니다. 그 결과, 애프터마켓 솔루션은 프랑스의 전기 버스 배터리 팩 시장에서 규모는 작지만 꾸준히 성장하는 하위 시장을 형성하고 있으며, 신차 수요가 회복되지 않는 상황에서도 플러그인 하이브리드 차량의 감소세를 완화하는 데 일조하고 있습니다.

LFP가 61.29%의 시장 점유율을 차지하고 있는 것은 타의 추종을 불허하는 열적 안정성과 사이클 내구성을 반영한 결과이며, 해외의 NMC 차량에서 발생한 몇 건의 주목할 만한 열폭주 사고 이후 이러한 특성들이 높이 평가받고 있습니다. 지속적인 기술 혁신을 통해 LFP의 셀 에너지 밀도는 190 Wh/kg까지 향상되어 NMC-622와의 성능 격차를 상당 부분 좁힌 한편, 코발트를 사용하지 않음으로써 비용 경쟁력을 유지하고 있습니다. LMFP의 연평균 성장률(CAGR) 23.73%는 LFP에 비해 15-20% 더 높은 에너지 밀도를 확보할 여지가 있으며, 동등한 안전성을 갖추고 있기 때문입니다. 프랑스의 각 시스템 통합 업체들은 공급 리스크를 헤지하기 위해 SEQENS사와 BTR사의 LMFP 셀을 사전 인증한 반면, Blue Solutions사는 LMFP 양극재와 황계 고체 전해질을 결합한 고체 전지의 파일럿 라인을 가동하고 있습니다. NMC는 장거리 연결 버스 용도에서 여전히 중요하지만, 니켈 및 코발트 가격 변동이 그 경쟁력을 약화시키고 있어, 각 기관은 망간 함량이 높은 혼합물로 전환해야 하는 상황에 직면해 있습니다.

화학 성분을 둘러싼 경쟁이 공급업체의 입지를 형성하고 있습니다. Forsee Power는 ‘화학 조성에 구애받지 않는’ 전략을 내세워, LFP, LMFP, NMC 셀에 대응 가능한 모듈식 팩 설계를 제공합니다. CATL과 BYD는 양산 가격 경쟁력을 바탕으로 표준 버스용 LFP 기반 CTP 아키텍처를 중시하고 있습니다. Saft사는 초고속 충전용 사례에 초점을 맞추어 수익성이 높은 NCA에 주력하고 있는 반면, LG Energy Solution사는 차세대 플랫폼용으로 파우치형 LMFP를 판매하고 있습니다. 보조금 규제로 인해 함유율 기준이 강화되는 가운데, LFP 및 LMFP 양극재의 국내 공급이 전략적 필수 과제로 대두되고 있으며, 알자스와 프로방스에서는 새로운 사업이 시작되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

제8장 EV 배터리 팩 기업 CEO를 향한 중요 전략적 과제

제9장 누가 누구에게 공급하고 있을까(OEM·Tier 맵)

제10장 로컬라이즈 및 비용 구성

제11장 생산능력 및 가동률 트래커

제12장 무역 흐름 및 수입 의존도

제13장 재활용과 세컨드 라이프 에코시스템

AJY 26.06.30According to Mordor Intelligence, the french electric bus battery pack market size was valued at USD 7.83 million in 2025 and is expected to grow from USD 10.28 million in 2026 to USD 29.34 million by 2031, at a CAGR of 19.44% over 2026-2031.

This report is Segmented by Vehicle Type (Mini/Microbus, and More), Propulsion Type (Battery Electric, and More), Battery Chemistry (Lithium Iron Phosphate, and More), Capacity (Below 15 KWh, and More), Battery Form (Cylindrical, and More), Voltage Class (Below 400 V, and More), Module Architecture, Component. Market Forecasts are Provided in Terms of Value (USD) and Volume in Units.

France Electric Bus Battery Pack Market Trends and Insights

Electrification Mandates in Urban Low-Emission Zones

Twelve ZFE-m cities mandate a complete transition to zero-emission buses, hastening the retirement of diesel fleets even if they have remaining usable life. RATP, currently operating a significant number of electric buses, faces the challenge of substantially increasing its annual deliveries to meet its target. Major operators secure their positions with long-term commitments, exemplified by a multi-year contract with Iveco for a large number of buses. In contrast, smaller cities are opting for leasing arrangements, transferring battery ownership to suppliers such as Forsee Power. Additionally, the protracted UN R100 Rev 3 approvals, which can take considerable time for new pack designs, pose a significant hurdle for new entrants to the market .

Falling USD/kWh for LMFP (Lithium Manganese Iron Phosphate)/ LFP (Lithium Iron Phosphate) Chemistries

Over time, the cost of lithium iron phosphate (LFP) cells has seen a notable decline, making them a cost-effective option for various applications. Meanwhile, lithium manganese iron phosphate (LMFP) cells, which boast enhanced energy density, are also becoming more affordable. This heightened efficiency and improved energy storage capabilities render them particularly appealing to bus operators catering to extended suburban and inter-city routes. Additionally, the growing adoption of LMFP cells aligns with the increasing demand for sustainable and efficient energy solutions in the transportation sector.

Nickel and Cobalt Price Volatility Post-2025

As speculation swirled around potential export restrictions, nickel prices surged, significantly altering the cost dynamics for NMC batteries. This price volatility prompted transit agencies to pivot their tenders towards LMFP alternatives, which offer a more stable cost structure and reduced dependency on nickel. LMFP batteries are increasingly being viewed as a viable solution due to their cost-effectiveness and improved safety profile. Meanwhile, smaller battery integrators, unable to effectively navigate fluctuations in raw material prices due to limited resources and hedging capabilities, find themselves increasingly disadvantaged compared to larger, vertically integrated competitors. These larger players benefit from economies of scale and greater control over their supply chains, enabling them to mitigate the impact of raw material price swings. This ongoing shift not only strains local competitiveness but also increases short-term costs in France's electric bus battery market, creating challenges for stakeholders across the value chain and potentially affecting the adoption rate of electric buses in the region.

Other drivers and restraints analyzed in the detailed report include:

- French "Buy-European Battery" Subsidies

- Secondary-Life Battery Leasing Business Models

- Lengthy EU Homologation for New Cell Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standard 12-meter buses accounted for 48.82% of installed packs in 2025, reflecting compatibility with existing depot geometry and route scheduling. Their 100-150 kWh batteries balance range and curb-weight limits, yielding rapid operational payback for city fleets. Fleet operators in Paris and Toulouse favor such formats for low-floor accessibility and maneuverability in dense urban cores. Articulated 18-meter designs, though costlier, capture BRT corridors where peak-period capacity overshadows infrastructure cost concerns. The articulated class's 23.69% CAGR stems from projects like Ile-de-France Mobilites' Tzen 4, which deploys 30 double-articulated units with 220 kWh LMFP packs that charge at 800 V to minimize depot dwell times. Midi buses (8-10.5 m) retain a foothold in heritage districts, but limited under-floor space constrains pack capacity to 80-100 kWh, slowing expansion relative to larger formats. Mini and micro segments remain niche, serving shuttle loops with shorter trip ranges, yet find little growth in the French electric bus battery pack market, as on-demand vans can often serve newer pedestrian zones.

The capacity divergence influences the chemistry choice: standard buses increasingly adopt higher-density LFP cells with 180 Wh/kg, whereas articulated units prefer LMFP or NMC for a longer range. OEMs such as Heuliez Bus retrofit chassis layouts to accommodate roof-mounted packs. As BRT corridors expand to Bordeaux and Nice, articulated buses signal long-term upside, reinforcing demand for higher-energy chemistries and faster-charging infrastructure.

Battery electric vehicles accounted for 83.16% of 2025 unit shipments and will climb further as plug-in hybrids lose policy backing. The national climate bill passed in April 2025 mandates 100 % zero-emission buses for new urban orders from 2027, effectively excluding hybrid drivetrains from major procurements. Operators cite 18% lower lifecycle maintenance costs for BEV fleets, attributing the savings to regenerative braking and a simpler driveline architecture. Plug-in hybrids retain a residual role on alpine or coastal routes, where voltage sags during extreme temperature swings can shorten the all-electric range.

Hybrid fleet attrition creates opportunities for battery-retrofit contracts, where integrators swap out aging diesel-electric modules for modular 100 kWh LFP packs. Such conversions extend chassis life by 8-10 years and unlock eligibility for subsidies. As a result, aftermarket solutions form a small yet growing sub-segment of the French electric bus battery pack market, helping to taper the decline in plug-in hybrids without reviving new-build demand.

LFP's 61.29% share reflects unmatched thermal stability and cycle durability, features highly valued after several high-profile thermal-runaway incidents in overseas NMC fleets. Continuous innovation raises LFP cell density to 190 Wh/kg, closing much of the performance gap to NMC-622 while retaining cobalt-free cost resilience. LMFP's 23.73% CAGR stems from its 15-20 % energy-density headroom over LFP and similar safety profile. French integrators pre-qualify LMFP cells from SEQENS and BTR to hedge against supply risk, while Blue Solutions runs pilot solid-state lines that blend LMFP cathodes with sulfur-based solid electrolytes. NMC remains relevant for long-haul articulated applications, yet nickel and cobalt price swings erode its competitiveness, nudging agencies toward manganese-rich blends.

The chemistry battleground shapes supplier positioning. Forsee Power stakes a "chemistry-agnostic" strategy, offering modular pack designs adaptable to LFP, LMFP, or NMC cells. CATL and BYD emphasize CTP architectures using LFP for standard buses, leveraging volume pricing. Saft focuses on higher-margin NCA for extreme fast-charge use cases, while LG Energy Solution markets pouch-format LMFP for next-generation platforms. As subsidy rules tighten content thresholds, domestic supply of both LFP and LMFP cathodes becomes a strategic imperative, sparking new ventures in Alsace and Provence.

List of Companies Covered in this Report:

- Contemporary Amperex Technology Co. Ltd. (CATL)

- BYD Company Ltd.

- Forsee Power SA

- Saft Groupe S.A.

- LG Energy Solution Ltd.

- Akasol AG (Borgwarner Inc.)

- Automotive Cells Company (ACC)

- Blue Solutions SA

- IRIZAR S.COOP.

- Microvast Holdings Inc.

- Panasonic Holdings Corp.

- Samsung SDI Co. Ltd.

- SK Innovation Co. Ltd.

- Proterra Inc.

- CALB Co. Ltd.

- Toshiba Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Key Industry Trends

- 4.2.1 Electric Vehicle Sales

- 4.2.2 Electric Vehicle Sales By OEMs

- 4.2.3 Best-selling EV Models

- 4.2.4 OEMs With Preferable Battery Chemistry

- 4.2.5 Battery Pack Price

- 4.2.6 Battery Material Cost

- 4.2.7 Battery Chemistry Price Comparison

- 4.2.8 EV Battery Capacity and Efficiency

- 4.2.9 Upcoming EV Models

- 4.2.10 Cell and Pack Capacity vs Utilization

- 4.3 Regulatory Framework

- 4.3.1 Type Approval and Pack Safety Standards

- 4.3.2 Market Access: Incentives, Local Content and Trade

- 4.3.3 End-of-Life: EPR, Second-Life and Recycling Mandates

- 4.4 Market Drivers

- 4.4.1 Electrification Mandates in Urban Low-Emission Zones

- 4.4.2 Falling USD/kWh for Lithium Iron Phosphate and Lithium Manganese Iron Phosphate Chemistries

- 4.4.3 French "Buy-European Battery" Subsidies (2025-30)

- 4.4.4 Inter-City Zero-Emission Public-Transport Tenders

- 4.4.5 Next-Gen Solid-State Pilot Lines at Paris-Saclay

- 4.4.6 Secondary-Life Battery Leasing Business Models

- 4.5 Market Restraints

- 4.5.1 Nickel and Cobalt Price Volatility Post-2025

- 4.5.2 Slow Build-Out of 600-800 V Depot Chargers

- 4.5.3 Skills Gap in Pack Thermal-Management Design

- 4.5.4 Lengthy EU Homologation for New Cell Formats

- 4.6 Value / Supply-Chain Analysis

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Vehicle Type

- 5.1.1 Mini / Microbus (Below 8 m)

- 5.1.2 Midi (8-10.5 m)

- 5.1.3 Standard (12 m)

- 5.1.4 Articulated (18 m)

- 5.2 By Propulsion Type

- 5.2.1 Baterry Electric Vehicle

- 5.2.2 Plug-in Hybrid Electric Vehicle

- 5.3 By Battery Chemistry

- 5.3.1 LFP (Lithium Iron Phosphate)

- 5.3.2 LMFP (Lithium Manganese Iron Phosphate)

- 5.3.3 NMC (Nickel Manganese Cobalt Oxide)

- 5.3.4 NCA (Nickel Cobalt Aluminum Oxide)

- 5.3.5 LTO (Lithium Titanium Oxide)

- 5.3.6 Others (LCO, LMO, NMX, Emerging Battery Technologies, etc.)

- 5.4 By Capacity

- 5.4.1 Less than 15 kWh

- 5.4.2 15 kWh - 40 kWh

- 5.4.3 40 kWh - 60 kWh

- 5.4.4 60 kWh - 80 kWh

- 5.4.5 80 kWh - 100 kWh

- 5.4.6 100 kWh - 150 kWh

- 5.4.7 Above 150 kWh

- 5.5 By Battery Form

- 5.5.1 Cylindrical

- 5.5.2 Pouch

- 5.5.3 Prismatic

- 5.6 By Voltage Class

- 5.6.1 Below 400 V (48-350 V)

- 5.6.2 400-600 V

- 5.6.3 600-800 V

- 5.6.4 Above 800 V

- 5.7 By Module Architecture

- 5.7.1 Cell-to-Module (CTM)

- 5.7.2 Cell-to-Pack (CTP)

- 5.7.3 Module-to-Pack (MTP)

- 5.8 By Component

- 5.8.1 Anode

- 5.8.2 Cathode

- 5.8.3 Electrolyte

- 5.8.4 Separator

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.2 BYD Company Ltd.

- 6.4.3 Forsee Power SA

- 6.4.4 Saft Groupe S.A.

- 6.4.5 LG Energy Solution Ltd.

- 6.4.6 Akasol AG (Borgwarner Inc.)

- 6.4.7 Automotive Cells Company (ACC)

- 6.4.8 Blue Solutions SA

- 6.4.9 IRIZAR S.COOP.

- 6.4.10 Microvast Holdings Inc.

- 6.4.11 Panasonic Holdings Corp.

- 6.4.12 Samsung SDI Co. Ltd.

- 6.4.13 SK Innovation Co. Ltd.

- 6.4.14 Proterra Inc.

- 6.4.15 CALB Co. Ltd.

- 6.4.16 Toshiba Corporation

7 Market Opportunities and Future Outlook

8 Key Strategic Questions for EV Battery Pack CEOs

9 Who Supplies Whom (OEM-Tier Map)

10 Localization and Cost Stack

- 10.1 BoM Split (USD/kWh)

- 10.2 Local vs Imported Content

- 10.3 Tariff/Subsidy Pass-Through

11 Capacity and Utilization Tracker

- 11.1 Cell GWh (Installed/Under-Build)

- 11.2 Utilization and Bottlenecks

- 11.3 New Plant Pipeline