|

시장보고서

상품코드

2066757

플렉서블 중간 벌크 컨테이너(FIBC) 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Flexible Intermediate Bulk Container (FIBC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

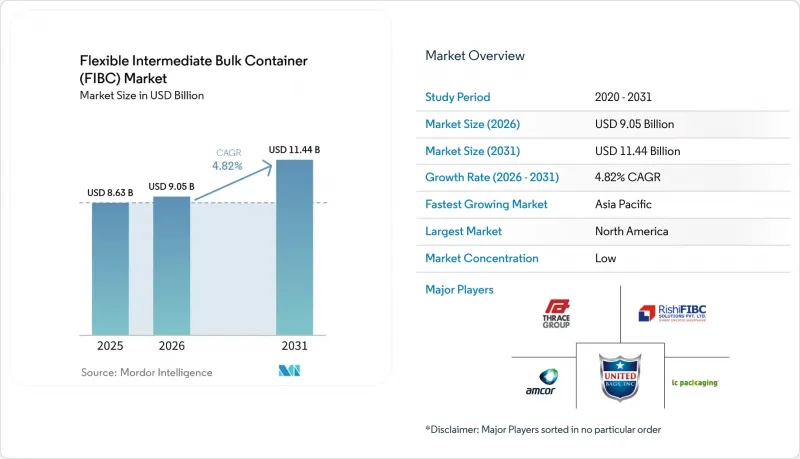

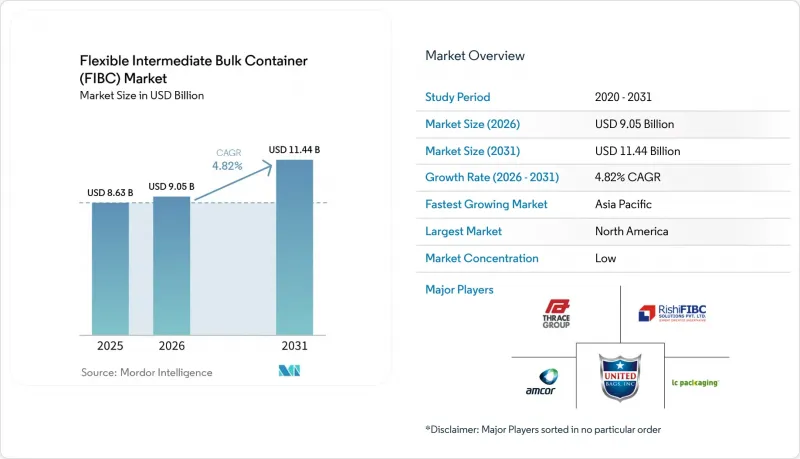

Mordor Intelligence에 의하면, 플렉서블 중간 벌크 컨테이너(FIBC) 시장 규모는 2025년에 86억 3,000만 달러로 평가되었고, 2026년에 90억 5,000만 달러로 추정되고, 2031년까지 114억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 4.82%로 성장할 전망입니다.

본 보고서는 유형별(A, B, C, D), 설계별(U 패널, 배플, 원형, 4 패널, 기타), 최종 사용자별(식품, 화학, 제약, 건설, 광업, 기타), 용량별(500kg 이하, 500-1,000kg, 1,000-1,500kg, 1,500kg 초과), 재질별(버진 PP, 재생 PP, UV PP, 종이, 바이오), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 플렉서블 중간 벌크 컨테이너(FIBC) 시장 동향 및 분석

식품 및 농산물의 대량 수출 붐

곡물 및 특수 작물공급망에서 전 세계적으로 리쇼어링이 진행됨에 따라, 단위당 운송 비용을 절감하고 교차 오염을 방지할 수 있는 식품 등급의 플렉서블 벌크백에 대한 수요가 증가하고 있습니다. 2024년에 시행될 미국 농업용수 관련 개정 규정에 따라 농산물의 추적 가능성이 더욱 엄격해짐에 따라, 수출업체들은 디지털 기록 시스템과 원활하게 연동되는 바코드 지원 FIBC를 도입해야 할 압박을 받고 있습니다. 브라질이나 인도 등 항만 인프라를 확충하고 있는 국가들은 FIBC 배출 설비에 맞추어 설계된 벌크 처리용 사일로에 투자하고 있으며, 이는 중기적인 성장을 뒷받침하고 있습니다. 상품 가격의 변동은 생산자들이 포장 비용을 절감하면서도 이익률을 유지할 수 있는 유연한 중간 벌크 컨테이너 시장 솔루션을 선택하도록 더욱 부추기고 있습니다. 따라서 식품 안전 규제와 비용 관리의 시너지 효과가 이 부문의 회복력을 뒷받침하고 있습니다.

유해 화학물질 취급 규제가 수요를 끌어올리고 있습니다.

OSHA(미국 직업안전보건청)가 2024년에 유엔 GHS 제7판 개정안을 준수함에 따라, 가연성 분말 및 용제를 운송하는 컨테이너에 대한 기술적 요건이 강화되었습니다. 전도성 실이나 CROHMIQ 원단을 사용한 유형 C 및 유형 D 가방은 현재 화학 플랜트, 제약용 믹서, 리튬 광석 가공 시설에서 표준으로 자리 잡고 있습니다. 조달 담당자는 20-30% 정도 가격이 비싸다는 느낌이 들지만, 일반 봉투에서 인증 제품으로의 전환을 추진하고 있습니다. 이는 가동 중단 시간이나 보험 리스크를 줄여주는 리스크 완화 자산으로 간주되기 때문입니다. 18개월이라는 짧은 규정 준수 대응 기간으로 인해 발주가 앞당겨졌으며, 북미 및 유럽의 특수 제품 라인 가동률은 높은 수준을 유지하고 있습니다. 그 결과, 정전기 방지 사양의 플렉서블 중간 벌크 컨테이너 시장에서 지속적인 수요 증가가 예상됩니다.

PP 수지 가격 변동

원유 가격 변동과 정유시설 가동 중단에 따라 변동하는 폴리프로필렌 원료 가격은 봉투 제조 비용의 60-70%를 차지하고 있어, 헤지 수단이 없는 중소 가공업체들을 압박하고 있습니다. 2024년 6월 수지 가격 하락은 일시적인 안도감을 주었지만, 만성적인 불확실성으로 인해 구매자들은 포괄 발주를 연기하거나 분기마다 재협상을 진행할 수밖에 없는 상황에 처해 있습니다. 대기업들은 수지 컴파운딩 분야로의 후방 통합과 재생 PP의 도입 가속화를 통해 리스크를 상쇄하고 있지만, 중견 기업들은 이익률 압박에 직면해 있습니다. 선물 기반 계약과 재생 원료의 사용이 확대됨에 따라, 플렉서블 중간 벌크 컨테이너 시장에 미치는 단기적인 부정적 영향은 점차 완화되고 있습니다.

부문별 분석

A형 컨테이너는 2025년 수요의 65.74%를 차지했으며, 이는 곡물, 시멘트, 불연성 화학물질 운송 분야에서 이 컨테이너가 차지하는 중요한 위치를 입증하고 있습니다. 한편, 정전기 대책이 적용된 유형 D 백은 리튬 광석 정제 업체나 제약용 건조기 제조업체들이 발화 위험을 피하기 위해 접지가 되지 않은 제품을 지정하고 있기 때문에 연평균 성장률(CAGR) 7.53%로 성장하고 있습니다.

규제 감독의 강화와 외부 접지선이 필요 없습니다는 점 덕분에, 유형 D는 최적의 선택지로 자리매김하고 있으며, 외딴 지역의 광산이나 해양 시추 시설에서 규정 준수 관련 복잡성을 줄일 수 있게 되었습니다. 고강도 CROHMIQ 원단은 4,000만 회 이상의 안전한 운송 실적을 자랑하며, 가혹한 환경에서도 신뢰성이 입증되었을 뿐만 아니라, 유연한 중간 벌크 컨테이너 시장의 향후 성장을 뒷받침하고 있습니다.

배플형과 Q-Bag형은 팽창을 방지하고 적재 밀도를 높이는 내부 패널을 갖추고 있어, 2025년에는 34.12%의 시장 점유율을 차지했습니다. 이는 선박의 화물창이나 도시 지역의 물류 센터에 있어 결정적인 장점입니다. U-Panel형 파우치는 로봇화 된 충전 프레임과 원활하게 연동되는 엄격한 치수 공차에 힘입어, 2031년까지 연평균 성장률(CAGR) 8.28%를 나타낼 것으로 전망됩니다.

서큘러 및 4패널 설계는 최대 용량이나 정밀한 배출이 요구되는 상황에서 여전히 그 입지를 유지하고 있지만, 지속적인 린 창고화 노력에 힘입어 배플형이 주목받고 있습니다. 팔레트를 스캔하는 자동화 시설에서는 균일한 설치 면적이 선호되고 있으며, 이로 인해 특수한 형태의 유연한 중간 벌크 컨테이너 시장의 성장세가 유지되고 있습니다.

지역별 분석

북미는 2025년에 전 세계 매출의 38.25%를 차지한 것으로 평가되었으며, 성숙한 화학제품 공급망, 높은 농업 수출량, 그리고 높은 수익률을 보이는 인증 제품을 뒷받침하는 엄격한 OSHA(미국 직업안전보건청) 규정 준수에 힘입고 있습니다. 자산 소유자들이 스마트 패키징으로의 개조에 재투자하고 있으며, 국내 셰일 화학제품 생산이 견조한 추세를 보이고 있어, 해당 지역은 안정적인 성장 궤도를 유지하고 있습니다.

아시아태평양은 배터리용 금속 제련에 대한 막대한 투자와 광범위한 제조업의 확장에 힘입어 7.78%라는 가장 빠른 연평균 성장률(CAGR)을 기록하고 있습니다. 중국의 바오터우 희토류 허브, 인도의 생산 연계형 인센티브, 그리고 동남아시아의 농업 관련 제품 수출이 맞물리면서, 전도성 및 고적층 설계 제품에 대한 지역 내 수주가 증가하고 있습니다. Bulkcorp International 등 현지 제조업체들은 생산 능력을 확대하고 수출 계약을 확보하고 있으며, 이는 플렉서블 중간 벌크 컨테이너(FIBC) 시장을 주도하는 그들의 강력한 경쟁력을 보여줍니다.

유럽은 ‘그린 딜’에 따라 재생 소재 규격을 선도적으로 도입하고, 멀티트립 모델을 보완하는 역물류 시스템을 구축함으로써 여전히 큰 시장 점유율을 유지하고 있습니다. 남미는 대두, 옥수수, 리튬 염수 등 식품 등급 또는 고강도용 포대가 필요한 수출 품목의 혜택을 받고 있으며, 중동 및 아프리카는 석유화학 산업의 확대와 대규모 인프라 프로젝트로부터 이익을 얻고 있습니다. 따라서 지역의 다양화로 인해 유연한 중간 벌크 컨테이너(FIBC) 시장 전반에 걸쳐 기회가 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the flexible intermediate bulk container market size is projected to be USD 8.63 billion in 2025, USD 9.05 billion in 2026, and reach USD 11.44 billion by 2031, growing at a CAGR of 4.82% from 2026 to 2031.

This report is Segmented by Type (A, B, C, D), Design (U-Panel, Baffle, Circular, 4-Panel, Others), End-User (Food, Chemicals, Pharma, Construction, Mining, Others), Capacity (Up To 500kg, 500-1000kg, 1000-1500kg, Above 1500kg), Material (Virgin PP, Recycled PP, UV PP, Paper, Bio-Based), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Flexible Intermediate Bulk Container (FIBC) Market Trends and Insights

Food and Agro Commodities Bulk-Export Boom

Global reshoring of grain and specialty-crop supply chains is boosting demand for food-grade flexible bulk bags that lower per-unit freight cost and prevent cross-contamination. Updated U.S. agricultural-water rules effective 2024 require tighter produce traceability, pushing exporters toward barcode-ready FIBCs that integrate seamlessly with digital record systems. Countries expanding port infrastructure, such as Brazil and India, are investing in bulk-handling silos designed around FIBC discharge equipment, reinforcing mid-term growth. Commodity-price swings further encourage growers to choose flexible intermediate bulk container market solutions that cut packaging spend while protecting margins. The confluence of food-safety regulation and cost discipline therefore underpins the segment's resilience.

Hazardous-Chemical Handling Rules Boosting Demand

OSHA's 2024 alignment with UN GHS revision 7 raises the technical bar for containers that carry flammable powders and solvents. Type C and Type D bags with conductive yarns and CROHMIQ fabrics are now standard at chemical plants, pharmaceutical mixers and lithium-ore processors. Procurement managers are switching from commodity sacks to certified units despite premiums of 20-30%, viewing them as risk-mitigation assets that reduce downtime and insurance exposure. Short 18-month compliance windows have pulled forward orders, keeping utilization high for specialty lines in North America and Europe. The result is a durable uplift in the flexible intermediate bulk container market for electrostatic-safe variants.

PP Resin Price Volatility

Polypropylene feedstock swings, driven by crude-oil moves and refinery outages, make up 60-70% of bag production cost, undermining smaller converters that lack hedging tools. June 2024 resin drops offered brief relief, yet chronic uncertainty compels buyers to delay blanket orders or renegotiate quarterly. Larger manufacturers offset exposure by backward integrating into resin compounding and accelerating adoption of recycled PP, but mid-tier players face margin squeeze. The short-term drag on the flexible intermediate bulk container market gradually eases as futures-based contracts and recycled feedstocks gain traction.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Fulfilment Shift to Bulk Secondary Packaging

- Smart-FIBC Rollout for Real-Time Traceability

- Growth of Rigid-IBC Rental Pools

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Type A containers supplied 65.74% of 2025 demand, underscoring their value positioning across grain, cement and non-flammable chemical flows. Electrostatic-safe Type D bags, however, expand at 7.53% CAGR as lithium-ore refiners and pharmaceutical dryers specify non-grounded solutions to avert ignition risks.

Intensifying regulatory oversight and the absence of external grounding wires position Type D as the premium choice, enabling remote mines and offshore rigs to cut compliance complexity. High-tensile CROHMIQ fabrics have clocked more than 40 million safe trips, validating reliability in harsh environments and reinforcing future gains for the flexible intermediate bulk container market.

Baffle or Q-Bag variants held 34.12% share in 2025 owing to internal panels that stop bulging and unlock higher stack density, a decisive benefit for ship holds and urban DCs. U-Panel sacks track at 8.28% CAGR through 2031, supported by tight dimensional tolerances that mate smoothly with robotized filling frames.

Circular and 4-Panel designs maintain presence where maximum volume or precise discharge is required, yet continual lean-warehouse initiatives favor baffles. Automated facilities scanning pallets welcome the uniform footprint, sustaining the flexible intermediate bulk container market momentum for engineered geometries.

Geography Analysis

North America generated 38.25% of global revenue in 2025, underpinned by a mature chemical supply chain, high agricultural export volumes, and strict OSHA compliance that favors higher-margin certified bags. The region keeps a stable growth path as asset owners reinvest in smart-packaging retrofits and domestic shale-chemicals output holds firm.

Asia-Pacific records the most rapid 7.78% CAGR due to heavy investment in battery metal refining and broad-based manufacturing expansion. China's Baotou rare-earth hub, India's production-linked incentives and Southeast Asia's agribusiness exports converge to lift regional orders for conductive and high-stack designs. Local producers such as Bulkcorp International scale capacity and secure export contracts, testifying to competitive depth that fuels the flexible intermediate bulk container (FIBC) market.

Europe retains a significant share by pioneering recycled-material specifications under the Green Deal and by deploying reverse logistics that complement multi-trip models. South America benefits from soy, corn and lithium-brine exports that require food-grade or heavy-duty sacks, while the Middle East and Africa gain from petrochemical expansions and infrastructure megaprojects. Regional diversification therefore spreads opportunity across the flexible intermediate bulk container (FIBC) market landscape.

- Greif Inc.

- Amcor Plc

- LC Packaging International BV

- Thrace Group

- Rishi FIBC Solutions Pvt Ltd

- United Bags Inc.

- Bag Corp

- Bulk Lift International LLC

- Conitex Sonoco

- Intertape Polymer Group

- Emmbi Industries Ltd

- Schoeller Allibert Group BV

- BAG Supplies Canada Ltd

- Southern Packaging LP

- Plastipak Group

- FlexiTuff International Ltd

- Bulk Pack Exports Ltd

- J&HM Dickson Ltd

- Houston Bulk Bag Co.

- Jumbo Bag Corporation

- Mule Bag Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Food and agro commodities bulk export boom

- 4.2.2 Hazardous-chemical handling regulations boosting demand

- 4.2.3 E-commerce fulfilment shift to bulk secondary packaging

- 4.2.4 Smart-FIBC (IoT/RFID) rollout for real-time traceability

- 4.2.5 Paper and recycled-PP FIBC adoption under circular-economy mandates

- 4.2.6 Mining super-sack standardisation in lithium and rare-earth supply chains

- 4.3 Market Restraints

- 4.3.1 PP resin price volatility

- 4.3.2 Stringent static-dissipation certification costs

- 4.3.3 Ocean-freight container shortages disrupting FIBC supply

- 4.3.4 Growth of rigid-IBC rental pools cannibalising one-way FIBC demand

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Type A

- 5.1.2 Type B

- 5.1.3 Type C

- 5.1.4 Type D

- 5.2 By Design Type

- 5.2.1 U-Panel

- 5.2.2 Baffle / Q-Bag

- 5.2.3 Circular

- 5.2.4 4-Panel

- 5.2.5 Other Designs

- 5.3 By End-user Industry

- 5.3.1 Food and Agriculture

- 5.3.2 Chemicals and Petrochemicals

- 5.3.3 Pharmaceuticals

- 5.3.4 Building and Construction

- 5.3.5 Mining and Minerals

- 5.3.6 Others

- 5.4 By Capacity

- 5.4.1 Up to 500 kg

- 5.4.2 500 - 1,000 kg

- 5.4.3 1,000 - 1,500 kg

- 5.4.4 Above 1,500 kg

- 5.5 By Material / Polymer Type

- 5.5.1 Virgin PP

- 5.5.2 Recycled-content PP

- 5.5.3 UV-stabilized PP

- 5.5.4 Paper-based Composite

- 5.5.5 Bio-based Polymer Blends

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Greif Inc.

- 6.4.2 Amcor Plc

- 6.4.3 LC Packaging International BV

- 6.4.4 Thrace Group

- 6.4.5 Rishi FIBC Solutions Pvt Ltd

- 6.4.6 United Bags Inc.

- 6.4.7 Bag Corp

- 6.4.8 Bulk Lift International LLC

- 6.4.9 Conitex Sonoco

- 6.4.10 Intertape Polymer Group

- 6.4.11 Emmbi Industries Ltd

- 6.4.12 Schoeller Allibert Group BV

- 6.4.13 BAG Supplies Canada Ltd

- 6.4.14 Southern Packaging LP

- 6.4.15 Plastipak Group

- 6.4.16 FlexiTuff International Ltd

- 6.4.17 Bulk Pack Exports Ltd

- 6.4.18 J&HM Dickson Ltd

- 6.4.19 Houston Bulk Bag Co.

- 6.4.20 Jumbo Bag Corporation

- 6.4.21 Mule Bag Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment